By D. Kenton Henry editor, agent, broker 12 October 2022

In a year in which the annual inflation rate is over 9%, and the core inflation rate over 6%, there is some good news relative to Medicare Part D 2023 Drugs and Plan costs. And it comes just in time as the approximately 64 million Americans on Medicare will be electing their drug coverage during the “Annual Election Period” from October 15th through December 7th, for coverage to begin January 1.

While Medicare Part A (hospital and skilled nursing facility) coverage has been paid for during the working careers of most Americans or their spouses, Part B (out-patient coverage) has not. Medicare accesses an income-adjusted monthly premium based on a “two-year look-back at one’s income tax return. (for details refer to Chart 1, and Feature Article 1, below)

The base premium for individuals earning $97,000 or less, and couples filing jointly earning $194,00 or less, will be down $5.20 per month from $170.10 to $164.90. The Medicare Part B out-patient deductible will be down $7.00 from $233.00 to $226.00 in 2023. Although these decreases are nominal, to say the least, they are a move in the right direction.

The “not as good news” is that Part A Inpatient hospital costs to the beneficiary will be increasing. The inpatient hospital deductible is going to $1,600 for each admission – due to a different medical condition – or the same medical condition separated by 60 days or more. And the daily coinsurance for days 61-90 is going to $400 and for lifetime reserve days to $800. It is easy to see that most can ill afford to be liable for the cost of an extended hospital stay without supplemental coverage, such as Medicare Supplement or Medicare Advantage, to pay these expenses. (for details, refer to Chart 2 below)

Relative to Medicare Part D Prescription Drug Plans, the headline subject of this article, the best news is probably not that premiums are actually decreasing for many of the approximately 30 plan options available. Surveys show that Americans are more concerned about the price of their drugs than their plan premiums. So, more good news is that the cost of insulin – which has historically created something of a hardship for dependent diabetic patients – will be limited to a $35.00 monthly cap on insulin copays for Part D enrollees. In addition, all vaccines recommended for adults by the CDC will be available at no cost.

If not reversed, even greater cost savings are scheduled for 2024 and beyond. Here are some of the highlights:

2024

i) Part D enrollees entering the “catastrophic” phase of coverage will not owe any additional copays for the year. In other words, they will have 100% coverage.

ii) Part D premiums will be capped at a maximum price increase of 6% annually through 2029. Additionally, the government will expand eligibility for financial assistance.

2025

i) Out-of-pocket Medicare drug costs will be capped at $2,000 each year.

ii) Additionally, Part D enrollees will be able to spread out copay costs over the entire year, preventing hardship created by extremely high one-time bills.

2026

This will be the first year Medicare will be permitted to negotiate the cost of drugs. This will be limited to 10 drugs in 2026, increasing to 60 drugs by 2029.

These proposed changes all sound encouraging. Let us hope they survive to fruition. In the meantime, it is my job to assist my clients, and prospective clients, in identifying their lowest “total” cost Part D Drug plan for each calendar year. While people get fixated with monthly premium, one’s lowest total cost is the sum of their plan’s premium + any deductible due before their drugs become available for copays or coinsurance + their copays or coinsurance. We are seeking the lowest sum. It can be a tedious and confusing task for many and I assume that task for any client or prospective client requesting assistance.

For 2023 plan marketing, Medicare mandates I post the following disclaimer:

While I offer most, “I do not offer every plan available in your area. Please contact Medicare.gov or call 1-800-MEDICARE to get information on all your options.”

That being dispensed with, permit me to add – When someone requests I research the market for their lowest “total” cost drug or Medicare Advantage Plan, I not only employ proprietary software, but I utilize Medicare’s own data to make my recommendation. So rest assured, I have thoroughly reviewed all their options in the market before making my recommendation.

I do not charge a fee for my services. If you do not take advantage of my recommendation, you are out of nothing but the time we have spent together in arriving at it. However, if I introduce you to an insurance product, and you elect to apply for it, I only hope you will go through me to do so. You are not obligated to. Then, and only then, will I be compensated directly by the insurance company whose product you elect. The key to you is – you will pay no more premium for that product than if you were to walk in the front door of that company and purchase it directly from them. All companies in the Medicare Part D and Medicare Advantage market pay me the same so my objectivity is assured. Therefore, I like to think, you gain all the expertise my 36 years in the industry has to offer you at no additional charge. This is as opposed to a different person each time at the end of a toll-free number. I encourage you to take advantage of my offer and I look forward to establishing a working relationship with you.

D. Kenton Henry

All Plan Med Quote

Https://TheWoodlandsTXHealthInsurance.com Https://Allplanhealthinsurance.com Https://HealthandMedicareInsurance.com Office: 281-367-6565 Text my cell 24/7 @ 713-907-7984

******************************************************************************

CHART 1

| Full Part B Coverage | |||

| Beneficiaries who file individual tax returns with modified adjusted gross income: | Beneficiaries who file joint tax returns with modified adjusted gross income: | Income-Related Monthly Adjustment Amount | Total Monthly Premium Amount |

| Less than or equal to $97,000 | Less than or equal to $194,000 | $0.00 | $164.90 |

| Greater than $97,000 and less than or equal to $123,000 | Greater than $194,000 and less than or equal to $246,000 | $65.90 | $230.80 |

| Greater than $123,000 and less than or equal to $153,000 | Greater than $246,000 and less than or equal to $306,000 | $164.80 | $329.70 |

| Greater than $153,000 and less than or equal to $183,000 | Greater than $306,000 and less than or equal to $366,000 | $263.70 | $428.60 |

| Greater than $183,000 and less than $500,000 | Greater than $366,000 and less than $750,000 | $362.60 | $527.50 |

| Greater than or equal to $500,000 | Greater than or equal to $750,000 | $395.60 | $560.50 |

CHART 2

| Part A Deductible and Coinsurance Amounts for Calendar Years 2022 and 2023 by Type of Cost Sharing | ||

| 2022 | 2023 | |

| Inpatient hospital deductible | $1,556 | $1,600 |

| Daily coinsurance for 61st-90th Day | $389 | $400 |

| Daily coinsurance for lifetime reserve days | $778 | $800 |

*******************************************************************

FEATURE ARTICLE 1

CMS: Medicare Part B Premiums, Deductibles Will Decrease in 2023

Monthly Medicare Part B premiums will fall to $164.90 in 2023, marking a $5.20 decrease from this year, while Part A premiums are set to increase by $4 to $7.

Source: CMS Logo

September 27, 2022 – Medicare Part B premiums and deductibles will decrease in 2023, while Part A costs will rise, according to a fact sheet released by CMS.

Medicare Part B offers coverage for physician services, outpatient hospital services, certain home healthcare services, durable medical equipment (DME), and other medical services not covered by Medicare Part A.

The standard monthly premium for Part B enrollees will be $164.90 compared to $170.10 in 2022. The annual deductible will be $226, decreasing $7 from $233 in 2022.

Dig Deeper

- Increasing Medicare Spending Calls For Short, Long Term Financing Solutions

- How Do Medicare Advantage Plans Compare to Traditional Medicare?

- CMS May Use 2022 Savings to Lower 2023 Medicare Part B Premiums

The 2022 premiums included a contingency margin for projected Part B spending on the Alzheimer’s disease drug Aduhelm. However, 2022 saw lower-than-expected spending on Aduhelm and other Part B services, leading to larger reserves in the Part B account of the Supplementary Medical Insurance (SMI) Trust Fund. This trust fund helps limit Part B premium increases, resulting in lower premiums for 2023.

Individuals with Medicare who take insulin through a pump supplied through the Part B DME benefit will not have to pay a deductible starting on July 1, 2023. In addition, cost-sharing will be capped at $35 for a one-month supply of covered insulin.

In 2023, Medicare beneficiaries who are 36 months post-kidney transplant can choose to continue Part B coverage of immunosuppressive drugs despite no longer being eligible for full Medicare coverage. These individuals will have to pay a monthly premium of $97.10 for immunosuppressive drug coverage.

Medicare beneficiaries with incomes greater than $97,000 will have higher Part B premiums. For example, monthly premiums will range from $230.80 to $560.50 for high-income beneficiaries. Similarly, monthly immunosuppressive drug coverage premiums will vary from $161.80 to $485.50 for high-income beneficiaries.

The While Part B costs will decrease in 2023, Part A costs are set to increase.

Medicare Part A offers coverage for inpatient hospital services, skilled nursing facility care, hospice care, inpatient rehab, and home healthcare services.

The Medicare Part A inpatient hospital deductible for beneficiaries admitted to the hospital will be $1,600 in 2023, rising from $1,556 in 2022. This deductible covers beneficiaries’ share of costs for the first 60 days of inpatient hospital care.

For days 61 through 90 of hospitalization, beneficiaries will have to pay a coinsurance amount of $400 per day, up from $389 in 2022. Past 90 days, the coinsurance will rise to $800 per day. The daily coinsurance for individuals in skilled nursing facilities will be $200 for days 21 through 100 of extended care services, up from $194.50 in 2022.

The majority of Medicare beneficiaries do not have to pay a Part A premium because they have worked at least 40 quarters in their life, the fact sheet noted. However, for those who have not, 2023 premiums are increasing.

Individuals who have at least 30 quarters of coverage or were married to someone with at least 30 quarters of coverage will have a Part A monthly premium of $278 in 2023, compared to $274 in 2022.

Individuals with less than 30 quarters and those with disabilities will have to pay the full 2023 premium of $506 per month, which is $7 higher than in 2022.

The fact sheet also shared 2023 information on Medicare Part D costs. Premiums for Medicare Part D, which offers drug coverage, vary from plan to plan. Around two-thirds of beneficiaries pay premiums directly to their plan, while the other third have their premiums deducted from their Social Security benefit checks.

Beneficiaries with incomes above $97,000 must also pay an income-related monthly adjustment amount in addition to their Part D premium. The amounts will range from $12.20 to $76.40 for high-income beneficiaries.

*******************************************************************

FEATURE ARTICLE 2

6 Policies To Reduce Prescription Drug Prices, Boost Competition

As prescription drug spending climbs, ACHP is calling on policymakers to reduce high prescription drug prices and enhance market competition.

September 02, 2021 – The Alliance of Community Health Plans (ACHP) is urging the federal government to take action and lower prescription drug prices with a set of recommended actions.

The costs of prescription drugs continue to rise each year, but policymakers have done little to address it. ACHP’s list of suggestions ranges from increasing drug pricing transparency to expanding the use of biosimilars.

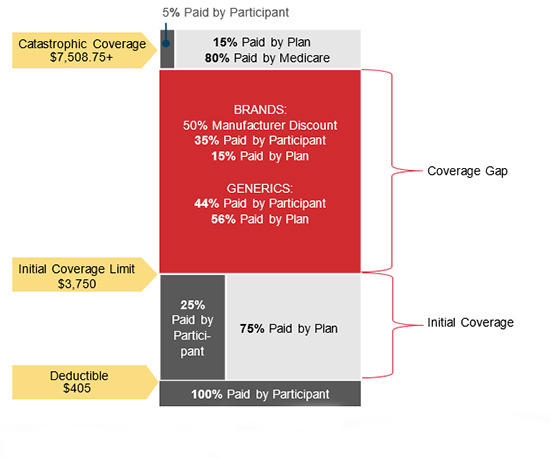

Catastrophic Medicare Part D prescription drug spending has been on the rise for over a decade. Seniors do not have an out-of-pocket cap for Medicare Part D, which can leave them with high costs in the catastrophic phase.

Dig Deeper

- Employers Support Empowering Medicare to Negotiate Drug Prices

- Why Catastrophic Medicare Part D Drug Spending Is On The Rise

- AHIP Blasts Pharmaceutical Industry as Drug Prices Increase

ACHP’s first recommendation is to redesign the Medicare Part D benefit including creating an out-of-pocket healthcare spending cap for seniors and to ensure that consumers will not owe anything during the catastrophic phase. Drug companies should also have to assume financial responsibility for each Part D phase and take some of the pressure off of Medicare.

Medicare should also receive resources to allow the program to negotiate lower drug prices for their beneficiaries, ACHP suggested.

ACHP’s next recommendation was for the federal government to allow the US Department of Health and Human Services (HHS) to negotiate prices for expensive prescription drugs that have no generic or biosimilar competition. These drugs were responsible for 60 percent of Part D spending in 2019, the fact sheet noted.

Currently, HHS has no power over competitive drug pricing.

Policymakers should also extend price negotiation to the commercial market to keep drug companies from shifting costs to non-Medicare consumers.

High-cost drugs that face no competition should also have an International Pricing Index applied that will limit the price to no more than 120 percent of its average international market price. The previous administration supported a similar approach through its Most Favored Nation model, but the Biden administration has proposed to rescind that model.

ACHP also urged the federal government to increase the use of biosimilars by informing clinicians and patients of the products and by persuading the Federal Trade Commission to increase biosimilar presence on the drug market. There are 29 FDA-approved biosimilars that are more affordable than other prescription drugs, but less than 12 are available on the market.

Increasing reimbursement rates for biosimilars could also improve utilization, the fact sheet stated.

ACHP’s suggestions also targeted drug companies’ unjustifiable raising of drug prices. At the beginning of 2021, 735 drugs prices increased up to 10 percent without reason.

Prescription drug prices often increase faster than the inflation rate, therefore ACHP recommended that drug manufacturers should have to provide rebates for drug price increase above the inflation rate.

Drug companies should also have to follow a price transparency rule that would require manufacturers to report and justify price increases, ACHP stated.

One example is the FAIR Drug Pricing Act, introduced in the Senate in 2019 and referred to the Committee on Health, Education, Labor, and Pensions. This Act would require drug manufacturers to notify HHS and submit a transparency and justification report 30 days before increasing the price of certain drugs by more than 10 percent.

Lastly, the ACHP recommended that the federal government encourage the use of transparent fee-based pharmacy benefit managers (PBMs). Traditional PBMs are typically not transparent about rebates, which can encourage high-cost drug use, whereas transparent fee-based PBMs pass rebates and discounts onto payers and earn revenue through a clear administrative fee.

Payer organizations have turned to the federal government to get prescription drug prices under control, as pharmaceutical companies are not budging.

In January 2021, AHIP called on the Biden Administration to focus on solutions that would protect Americans from higher drug prices.

The issue is pressing, not only for the seniors on whom some of ACHP’s recommendations focused but for all Americans. AHIP reported that the highest portion of commercial health insurance premiums goes toward prescription drug costs, making prescription drug pricing a widespread concern.

Leave a comment