By D Kenton Henry, editor of HealthandMedicareInsurance.com, agent, and Independent Insurance Broker

When most people compare Medicare Advantage plans, they focus on premiums, dental benefits, vision coverage, hearing aids, grocery cards, or over-the-counter allowances.

Those benefits certainly have value. However, after nearly four decades in the health insurance business, I have found that the biggest differences between Medicare Advantage and Medicare Supplement plans often become apparent only when a beneficiary actually needs medical care.

As Medicare Advantage enrollment continues to grow and healthcare costs continue to rise, provider networks and prior authorization requirements are becoming increasingly important issues for Medicare beneficiaries.

Provider Networks Continue to Change

One of the primary advantages of a Medicare Supplement policy is flexibility.

Generally speaking, a Medicare Supplement policyholder may receive treatment from any physician or hospital in the United States that accepts Medicare patients.

Medicare Advantage plans operate differently.

Most Medicare Advantage plans utilize provider networks. Those networks may change from year to year as insurance companies renegotiate contracts with physicians, specialists, hospitals, and healthcare systems.

A doctor who participates this year may not participate next year.

A hospital system that is in-network today could become out-of-network in the future.

For beneficiaries who travel frequently, maintain residences in multiple states, or simply want maximum freedom in choosing healthcare providers, network changes can sometimes create unexpected challenges.

Prior Authorization Remains a Concern

Another issue receiving increased attention is prior authorization.

Many Medicare Advantage plans require advance approval before certain services are performed. These may include:

MRI scans

CT scans

Physical therapy

Skilled nursing facility care

Certain surgical procedures

Some specialty medications

The concern is not always whether a service is ultimately approved.

Rather, the concern is that treatment may be delayed while additional documentation is gathered and reviewed.

Physicians across the country have frequently expressed frustration regarding the administrative burden associated with prior authorization requirements.

By contrast, beneficiaries covered under Original Medicare with a Medicare Supplement policy generally encounter fewer authorization hurdles because Medicare itself determines coverage.

An Aging Population Means More Healthcare Utilization

The first wave of Baby Boomers entered Medicare in 2011.

Every year, Medicare beneficiaries grow older, utilize more healthcare services, and gain access to increasingly sophisticated—and expensive—medical treatments.

Insurance companies face growing pressure to control costs while keeping premiums competitive.

Common tools used to manage those costs include:

Narrower provider networks

Increased care management programs

Expanded prior authorization requirements

More intensive utilization review

These trends are unlikely to disappear anytime soon.

Rural Beneficiaries May Face Additional Challenges

Provider access can be especially important for beneficiaries living outside major metropolitan areas.

While beneficiaries in cities such as Houston, Dallas, Austin, or San Antonio may have numerous participating providers available, individuals living in smaller communities may have fewer options.

When specialty care is needed, network limitations can sometimes require additional travel or create fewer choices regarding where treatment is received.

A Medicare Supplement policy largely eliminates those concerns because coverage follows Medicare rather than a specific provider network.

The Hidden Value of Medicare Supplement Coverage

Consumers naturally focus on premium.

Insurance professionals often focus on risk and long-term flexibility.

When affordable, Medicare Supplement plans provide several advantages:

Predictability

Generally lower out-of-pocket exposure

Fewer surprise medical bills

Greater budgeting certainty

Provider Freedom

No network restrictions

No referrals required

Coverage that travels with you throughout the United States

Administrative Simplicity

Fewer authorization requirements

Less paperwork

Fewer coverage-related obstacles when seeking care

Medicare Advantage Still Has an Important Role

None of this means Medicare Advantage is a poor choice.

For many beneficiaries:

Monthly budgets are limited.

Medicare Supplement premiums may be unaffordable.

Health conditions may make medical underwriting difficult or impossible.

In those situations, Medicare Advantage plans can provide valuable protection at little or no additional premium.

The key is understanding the tradeoff.

Medicare Supplement

Higher monthly premium

Broad provider access

Minimal prior authorization concerns

Predictable healthcare costs With certain Medicare Supplement Plans (F and G) out-of-pocket costs–with the exception of RX drugs at the pharmacy counter–can be a little as $0 to Medicare’s current Part B out-patient calendare year deductible of $282

Medicare Advantage

Lower monthly premium

Network restrictions may apply

Prior authorization requirements are more common

Cost-sharing occurs as healthcare services are utilized If using an MAPD PPO and going both in and outside the network in 2026 your out-of-pocket maximum expenses can be over $13,000 with certain plans

Final Thoughts

As healthcare continues to evolve, I believe annual reviews are becoming more important than ever.

The Medicare Advantage plan that works well today may not be identical next year. Networks change. Benefits change. Drug formularies change.

For beneficiaries who can comfortably afford the premium and qualify for coverage, Medicare Supplement insurance continues to offer the broadest provider access, the greatest flexibility, and the fewest obstacles to receiving care.

As always, each individual’s circumstances are different. If you have questions about your Medicare coverage options, I encourage you to contact me for a personalized review.

D Kenton Henry Independent Medicare Insurance Broker Since 1986

Dental Insurance: Worth the Premium — or Just a Payment Plan?

“Is dental insurance really worth what I pay for it?”

That’s a question I hear often—and it’s usually followed by:

“Or am I just spreading the cost of my dental work over time?”

My answer? It depends—but it doesn’t have to be a losing proposition.

Employer vs. Individual Coverage

If you receive dental insurance through an employer, part (or all) of your premium is subsidized. That makes the value proposition much more favorable.

However, if you are:

Self-employed

Retired

Or purchasing coverage on your own

…then you’re paying the full premium—and the math becomes more important.

Without the right strategy, dental insurance can become nothing more than a time-payment plan. Worse yet, you could end up paying more in premiums than you ever receive in benefits.

The Reality of Dental Costs

Let’s be honest—dental work is expensive.

A single dental implant can cost anywhere from $3,500 to $7,000. And unlike medical insurance, dental plans come with strict limitations.

Before choosing a plan, there are three key concepts you need to understand:

1. “Reasonable and Customary” Limits

No insurance company pays unlimited fees.

Instead, they base payments on what is considered “reasonable and customary” for your geographic area.

A crown in Beverly Hills will cost more than one in Brenham, Texas

If a dentist charges above the accepted range, you pay the difference

Understanding this concept is critical to avoiding unexpected costs.

2. Network vs. Non-Network Plans

Dental plans fall into two categories:

Network Plans (Recommended)

PPO (DPPO): Flexibility to go out-of-network (at higher cost)

HMO (DHMO): Must stay in-network for coverage

These plans offer lower negotiated fees because dentists agree to discounted rates.

Non-Network Plans

“Any dentist” plans

Typically higher premiums

Often result in higher out-of-pocket costs

Why? Because dentists are free to charge above what the insurance company considers reasonable—and you’re responsible for the difference.

3. The Most Important Rule: Avoid Excess Charges

Here’s where many people get burned:

With a non-network plan, you can be billed above what insurance pays

With a network plan, dentists must write off excess charges

That means:

If your share is 20% or 50%—that’s all you pay. No surprises.

Finding the Right Dentist (and Plan)

As an individual, you don’t have the bargaining power of a large employer.

So how do you gain access to lower fees and quality care?

You choose an insurance company that:

Has a large, reputable network

Pays claims promptly and reliably

Attracts high-quality dentists

Then you select a dentist based on:

Credentials

Technology used

Patient reviews

Location and convenience

Understanding Benefit Limits

Dental insurance is not unlimited coverage.

Typical plans:

Cover $1,000–$1,500 per year

Higher-end plans may go up to $5,000 annually

Often include waiting periods for major work

A smarter strategy is to choose a plan that:

Starts affordable

Increases benefits over time

Aligns with your expected dental needs

A Real-World Strategy (From Experience)

After decades in the business—and personal experience with extensive dental work—I approached my own coverage strategically.

I selected:

A financially strong insurance company

A plan that started at $1,500, then increased to $2,500, and ultimately $5,000 annually

A highly qualified dentist within the network

This allowed me to:

Stage treatment over time

Maximize benefits

Avoid excessive out-of-pocket costs

Bottom Line: How to Make Dental Insurance Work

To get real value from dental insurance:

✔ Choose a network plan

✔ Match benefits to your expected needs

✔ Select a skilled, in-network dentist

✔ Work with a knowledgeable advisor

How I Can Help

With over 30 years of experience in health, Medicare, and dental insurance, I help clients:

Compare plans from top-rated carriers

Avoid costly mistakes

Maximize benefits relative to premium

I represent companies such as: Aetna, Ameritas, Anthem, Blue Cross Blue Shield, Cigna, Delta Dental, Humana, and UnitedHealthcare.

Let’s Talk

If you’re considering dental coverage—or wondering if your current plan is worth it—I’d be happy to help.

D.Kenton Henry

TheWoodlandsTXHealthInsurance.com 📞 281-367-6565 Text my cell 24/7 @ 713-907-7984

Final Thought

Dental insurance can either be:

A smart financial tool or

An expensive payment plan

The difference lies in how you choose—and how you use—it.

(What Consumers Need to Know for the 2026 Marketplace)

D. Kenton Henry – editor, agent, broker

As we approach the 2026 plan year, one of the biggest questions in individual and family health insurance is what will happen to Advance Premium Tax Credits (APTCs)—the subsidies that lower monthly premiums for millions of Marketplace enrollees.

Why This Is Happening

During the COVID era, Congress passed temporary legislation — most recently extended under the Inflation Reduction Act (IRA) — which made Marketplace subsidies more generous and available to more households. These enhanced subsidies are scheduled to expire at the end of 2025, unless Congress acts to extend them.

If they expire, the Marketplace will revert to pre-COVID subsidy rules, which means:

1. Lower income thresholds for subsidy eligibility

Some households who qualified for subsidies under the temporary rules will no longer qualify at all.

2. Smaller subsidies for many who remain eligible

People who received very large subsidies during 2021–2025 would see higher net premiums for 2026, even if their income has not changed.

3. The return of the “subsidy cliff”

Under pre-COVID rules, households with income even slightly above 400% of the Federal Poverty Level received no subsidy. The COVID-era rules removed that cliff. If not renewed, the cliff returns.

This is why some people are seeing early projections showing their 2026 premiums rising sharply.

Where Things Stand in Congress

Both parties publicly acknowledge that the expiration would lead to large premium increases for many families. As of today:

There is broad interest in finding a solution, but

No final legislation has been passed,

No guarantee exists that the enhanced subsidies will continue, and

Any resolution will likely be tied to larger budget negotiations.

In short: Congress is still debating it, and the outcome directly affects what consumers will pay for Marketplace coverage in 2026.

What Consumers Should Expect

Until Congress acts, the Marketplace must begin preparing 2026 rates under the assumption that the enhanced subsidies expire. This means:

Preliminary quotes may show dramatically higher net premiums

Some currently subsidized families may temporarily appear ineligible for assistance

Final 2026 subsidy amounts cannot be known until legislation is passed — if it is passed

It is important to remember that this may change, depending on Congressional action in the coming months.

Practical Guidance for Individuals and Families

Don’t panic if early projections show large increases.

Stay informed — subsidy rules may be extended or modified.

Review your 2026 options with a licensed, experienced broker who can calculate subsidies under both scenarios.

Update income estimates accurately during Open Enrollment; small changes can affect substantial tax credit differences.

Bottom Line

The enhanced ACA subsidies that helped make Marketplace coverage more affordable since 2021 are set to expire after 2025, and Congress has not yet determined whether they will be renewed. Until a resolution is reached, 2026 Marketplace premiums may appear significantly higher for many Americans.

I will continue to monitor developments closely and provide updates as soon as new information becomes available.

Additionally—

It has come to my attention that my clients have been told the First Health PPO network plan is being mistakenly interpreted by them as being an Affordable Care Act (ACA) compliant PPO network. As such, they incorrectly believe any and all of their pre-existing health conditions will be covered and that all preventive exams and medicine will be covered at no out-of-pocket cost to them. This is wrong and here is the truth, as confirmed by me and ChatGPT:

✅ 1. There are no ACA-compliant PPO plans available in Texas individual/family (On- or Off-Exchange)

Texas has not had a true ACA-compliant individual market PPO option for several years. All carriers (BCBSTX, Ambetter, United/Optum, Aetna CVS, Oscar, Cigna, Moda, etc.) offer only:

EPOs

HMOs

These networks limit out-of-network benefits and require referrals or tighter network management.

A PPO requires:

National or multi-state contracted provider access

True out-of-network benefits

No referral requirement

No carrier has offered this in the ACA individual Texas market since around 2017–2018.

✅ 2. Aetna is not selling ACA individual/family plans in Texas for 2026 (and has already exited)

Your clients may be confused because Aetna offers:

Medicare Advantage PPOs

Employer-based PPOs

First Health networks tied to group/other products

But Aetna does NOT offer ACA individual/family plans in Texas for 2026.

So if someone believes they have an “Aetna PPO” under an ACA plan, they are mistaken. It is either not an ACA plan, or they are misinterpreting the network type.

✅ 3. If their plan is marketed as “PPO-like,” it is almost certainly:

a) A short-term medical plan

These frequently use PPO networks—including Aetna’s First Health—but they are:

NOT ACA-compliant

Do NOT cover pre-existing conditions

Can cap benefits

Can deny claims based on underwriting

b) A health-sharing ministry

Often marketed as “PPO plans” because they use rented networks, but also:

Not insurance

Not regulated as insurance

No claim guarantees

No ACA protections

c) A fixed-benefit plan that uses First Health or MultiPlan PPO

Again:

Not insurance

No ACA protections

No out-of-pocket maximums

No guaranteed coverage

d) A direct primary care + medical indemnity bundle

These are sometimes misrepresented as “PPO plans,” but they are not.

✅ 4. How to confirm instantly whether the client is on ACA-compliant coverage

Ask for one of the following:

A) The name of the carrier.

If it’s not:

BCBSTX

Cigna

Ambetter

UnitedHealthcare (UHC Marketplace)

Aetna CVS (in some states, but NOT Texas 2026)

Moda

Oscar (until exit)

…then it’s almost certainly not ACA-compliant.

B) A copy of the Summary of Benefits & Coverage (SBC).

All ACA plans must include an SBC — short-term plans and sharing ministries do not.

C) Their monthly bill or ID card.

If it says things like:

First Health Network

MultiPlan PPO

PHCS PPO

Aetna PPO

United Healthcare Choice/Choice Plus PPO

…that is almost certainly a non-ACA plan.

✅ 5. Bottom line for you:

If you believe you they are on an ACA-compliant “Aetna PPO” for individual/family coverage:

You are not. No such product exists in the Texas ACA market. You are almost certainly on a short-term plan, health-sharing product, or fixed-benefit plan using a rented PPO network.

This is an excellent opportunity for ne to help you transition to true ACA coverage, where you will regain:

Pre-existing condition protection

Essential health benefits

No annual/lifetime caps

And – perhaps most importantly – Out-of-pocket maximum protection

Please feel free to call me with any questions you may have or for assistance in obtaining 2026 ACA compliant health insurance. I will make the quoting and application process go as quickly and smoothly as possible whether you quailify for a subsidy or not.

The Open Enrollment Period for a January 1 effective date ends December 15th. You have until January 15th to obtain an effective date of February 1.

D. Kenton Henry Office: 281-367-6565 Text my cell 24/7@ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

By D. Kenton Henry, Editor / Agent / Broker — TheWoodlandsTXHealthInsurance.com, AllPlanHealthInsurance.com, HealthandMedicareInsurance.com 30 October 2025

Each November in Texas marks more than just the start of the new health insurance year—it’s your gateway to securing coverage for the year ahead. This time around, the 2026 individual and family health insurance market is undergoing noticeable changes. Here’s what you need to know—and how you can be ready.

1. Why 2026 matters

Open enrollment for 2026 policies begins November 1, 2025, and runs until January 15, 2026 for most Texas consumers. If you don’t act in this window, you could be locked out of making changes until next year unless a qualifying life event occurs. Given major shifts among carriers and plan options, early action is more important than ever.

2. Carrier changes you should track

One of the major headlines: Aetna will exit the Texas individual and family market beginning in 2026. That means if you currently have an Aetna plan, your policy will not renew for 2026. You’ll need to select a different carrier in the upcoming enrollment period.

Other carriers are repositioning their offerings, adjusting networks, benefits, and rates. Even if your carrier is staying, plan names and design may change. As your broker, I’ll review all available options from multiple carriers and ensure you’re not simply renewing by default.

3. What this means for you

No automatic renewal: If your carrier exits the market, your current plan will not carry over. You’ll receive a Notice of Change—or termination—and need to select a new plan.

Shop your options: Differences between plans are not only about monthly premiums. Review networks, cost-sharing, deductibles, out-of-pocket maximums, and whether benefits match your healthcare needs.

Subsidy changes: The federal subsidy rules continue to evolve. Even small changes in income, household, or eligibility can shift your subsidy level. I’ll help you analyse eligibility for Advance Premium Tax Credits (APTC) and other cost-saving tools.

Timing matters: Beginning November 1, I’ll be available to assist you through the selection process—not just on carriers and plans, but on ensuring accurate enrollment to avoid coverage gaps.

4. Why working with a broker matters

As an independent broker specializing in medical insurance since 1986, I work with virtually every major carrier licensed in Texas. My services to you are free of charge. My goal is to ensure you get the best plan that fits your health needs, budget, and preferences—especially in a year of significant market change. Rather than navigating dozens of plan names on your own, let me do the heavy lifting and help you make an informed choice.

5. What to do now

Gather your information – your current health plan, recent premium receipts, summary of benefits, and any health changes.

Schedule your review – open enrollment kicks off November 1. If you’d like early preparation, I’m available now to pre-review your situation so you’re ready to act.

Act during the window – November 1 through January 15 is your open period. Plans go into effect January 1, 2026, or, depending on carrier rules, as early as December 1, 2025.

Don’t wait – with carrier exits and plan redesigns in motion, the sooner you start the review, the better your chance of finding the optimal match.

Working together, we’ll turn these market shifts into an advantage—so instead of scrambling when notices arrive, you’ll move confidently into 2026 with coverage aligned to your needs.Let me handle the complexity so you can focus on your life, your health, and your goals.

If it’s after hours, or you simply prefer, you can do preliminary research before calling me by obtaining quotes from my quoting engine. You do NOT have to log in to obtain them but be certain to call me afterwards with questions, and assistance in finding your providers within the networks, as well as applying. CLICK HERE: https://allplaninsurance.insxcloud.com/get-a-quote

D. Kenton Henry Editor · Agent · Broker TheWoodlandsTXHealthInsurance.com * AllPlanHealthInsurance.com * HealthandMedicareInsurance.com

D. Kenton Henry Editor, agent, broker 30 SEPTEMBER 2025

Medicare 2026: Welcome clients and prospective clients! Before reading this (if you have not already), you should go to your mail box and retrieve your 2026 Annual Notice of Change from Medicare. You were due to receive it no later than today per Center For Medicare Rules and Regulations. If will give you a good idea if you need to re-shop your Medicare Advantage or Part D Drug plan for the coming calendar year. If not, the following changes may.

10 changes to review before the Annual Election period, often referred to as the Open Enrollment (Oct 15–Dec 7)

If you’re on Medicare, 2026 brings important updates—especially to prescription drug coverage. The Part D out-of-pocket cap rises to $2,100, the standard deductible becomes $615, and Medicare’s first negotiated drug prices start on January 1, 2026. Medicare Advantage also gets new guardrails around prior authorization and appeals, and some supplemental “perks” are being narrowed. Check your Annual Notice of Change (ANOC) (it should arrive by Sept 30) and compare your plan options—small differences can mean big savings. If you’d like help, I’ll review your medications, doctors, and benefits to make sure you’re in the right fit for January 1.

Here is an itemized list of the 10 Key Changes:

Medicare changes your 2026 plan review should cover

1) Part D’s annual out-of-pocket cap rises to $2,100. Once a member’s 2026 Part D out-of-pocket spending reaches $2,100, they’ll pay $0 for covered Part D drugs for the rest of the calendar year.

2) The standard Part D deductible increases to $615. Plans can’t set a deductible higher than $615 in 2026 under the redesigned Part D rules.

3) Drug price negotiations start showing up at the counter. Medicare’s first set of negotiated Maximum Fair Prices (MFPs) for 10 widely used Part D drugs take effect January 1, 2026. Members should review their ANOC and plan formularies to determine how these prices impact their medications.

4) Insulin and adult vaccines: protections continue. Part D insulin remains capped and no-deductible; starting in 2026, the cap is the lesser of $35, 25% of the MFP, or 25% of the negotiated price. ACIP-recommended adult vaccines remain $0 under Part D.

5) “Pay-over-time” for prescriptions auto-renews. The Medicare Prescription Payment Plan (monthly billing instead of paying large amounts at the pharmacy) auto-renews in 2026 unless the member opts out. It smooths payments but doesn’t lower total costs—good to remind clients who tried it in 2025.

6) Medicare Advantage prior-auth and appeals guardrails tighten. For 2026, CMS says MA plans must honor previously approved inpatient admissions (can only reopen for obvious error or fraud), and CMS closes appeals loopholes so members and providers receive required notices and can appeal adverse coverage decisions. Expect fewer mid-stay reversals. Centers for Medicare & Medicaid Services

7) Limits on certain “extra perks” in MA (SSBCI) take effect. CMS codified non-allowable Special Supplemental Benefits for the Chronically Ill—examples include non-healthy food, alcohol, tobacco, and life insurance. Some plans may rebalance extras as a result.

8) Star Ratings update: new/returning measures. 2026 Stars add or reintroduce measures like Kidney Health Evaluation for Patients with Diabetes plus Improving/Maintaining Physical and Mental Health (weight = 1). Tougher cut points in 2026 may shift plan bonuses and benefit richness—worth watching locally.

9) Part D benefit design shifts behind the scenes. Liability shares change across phases (plans, manufacturers, CMS), and there’s a new subsidy for selected (negotiated) drugs. Members may see formulary/tier adjustments—another reason to compare plans.

10) ANOC timing: what to tell clients. Remind everyone: Annual Notice of Change (ANOC) letters arrive by September 30 each year; if they didn’t see one, call the plan. Open Enrollment runs Oct 15 – Dec 7 for Jan 1 effective dates.

Check your Annual Notice of Change (ANOC) (it should arrive by Sept 30) and compare your plan options—small differences can mean big savings. If you’d like help, I’ll review your medications, doctors, and benefits to make sure you’re in the right fit for January 1.

Other Developments

Some Medicare Advantage supplemental benefits (i.e. nutrition support, OTC medicine) may be reduced in favor of core services.

In six states, prior authorizations for certain Original Medicare services will be tested.

Part B and Part D premiums and deductibles are both set to increase—Part B premium up ~11.6%, and Part D premium by about 6%.

Who Am I?

In addition to being the editor of this blog I have has been helping individuals and families navigate the health and Medicare insurance landscape since 1986. With nearly four decades of experience, he specializes in Medicare Supplement, Medicare Advantage, and Medicare Part D prescription drug plans.

As an independent broker, I am appointed with virtually every competitive, A-rated Medicare insurance company in Texas, Indiana, Ohio, and Michigan. This broad access allows him to recommend the plan that truly best fits each client’s needs.

Above all, I work for my clients—not the insurance companies. You will never pay more by enrolling through me than you would if you purchased an insurance product directly from the carrier. My mission is to provide clear guidance, personalized recommendations, and ongoing support to ensure my clients get the coverage and peace of mind they deserve.

If you have any questions about 2026 Medicare Part D prescription drug plans, Medicare Advantage, or Medicare Supplement (Medi-Gap) policies, please give me a call.

Average premiums, benefits and plan choices for Medicare Advantage and the Medicare Part D prescription drug program should remain relatively stable next year, CMS said in a Sept. 26 news release. But MA enrollment is projected to decrease 900,000 in 2026.

Despite a slight dip in available MA plans nationally, over 99% of Medicare beneficiaries will still be able to access an MA plan.

The agency estimates the premiums for MA plans to drop from $16.40 to $14.00. On average, the total premium for standalone Part D is estimated to fall $3.81. CMS’ July forecast predicted elevated Medicare Part D base premium increases in the neighborhood of 6%.

Finding Your Doctor and Understanding Subsidies in HMO Plans

Shopping for individual or family health insurance can feel like navigating a maze—with dead ends, confusing signs, and few clear answers. Two of the most common pain points for shoppers are (1) trying to keep your current doctor while limited to an HMO network and (2) figuring out whether you qualify for a subsidy, known as an advance premium tax credit (APTC). Both challenges can make the process frustrating and overwhelming, especially during open enrollment when time is limited.

The HMO Headache: “Will My Doctor Be Covered?”

One of the biggest shocks people face when shopping for health insurance is realizing that their trusted doctor or medical provider might not be covered under a new plan—especially if it’s an HMO (Health Maintenance Organization). Unlike PPOs (Preferred Provider Organizations), which offer broader provider access and out-of-network options, HMO plans restrict coverage to a specific network of doctors and hospitals. If your doctor isn’t in the network, you may have to pay the full cost of your visit out of pocket—or switch doctors entirely.

Unfortunately, trying to find this information is often easier said than done.

Outdated or Inaccurate Provider Directories: Online directories can be incomplete or outdated. It’s not uncommon for a provider to be listed as “in-network” only for you to find out later they’ve left the plan.

Hard-to-Navigate Insurance Websites: Many insurance carrier sites don’t make it easy to search by doctor name, location, or specialty. Even worse, each plan may have its own “network tier,” adding another layer of complexity.

No Universal Search: There’s no centralized tool that lets you enter your doctor’s name and see every marketplace plan that includes them. You have to check each insurance company or plan individually.

For people with ongoing care needs—like managing chronic conditions or continuing with a trusted pediatrician or specialist—the possibility of switching providers isn’t just inconvenient, it can feel risky.

The Subsidy Puzzle: “Do I Qualify for Help Paying My Premium?”

The Affordable Care Act (ACA) made health insurance more accessible by offering subsidies for people who meet certain income guidelines. These subsidies, officially called advance premium tax credits, lower your monthly premium based on your household size and income.

The good news is that many people qualify.

The bad news is that determining whether you qualify can feel like filling out a tax return just to get a quote.

Income Guesswork: Subsidy eligibility is based on your estimated household income for the upcoming year. That’s right—you must predict your future income, even if you’re self-employed or work variable hours.

Family Dynamics Matter: Your household size includes dependents—even if they don’t need insurance—and income from every working member. This means getting it right often requires gathering data from multiple people.

Mid-Year Changes Complicate Things: If your income or family size changes mid-year, you may need to report it or risk having to repay part of your subsidy at tax time.

The ACA “Cliff” and “Glide Path”: Previously, you could lose your subsidy entirely if your income was even $1 over the limit. Recent changes have smoothed this out, but they are still complicated and frequently misunderstood.

And while tools like Healthcare.gov’s calculator are helpful, they often rely on broad estimates. They can’t account for all variables, such as gig work, investment income, or multiple part-time jobs.

Why It Feels So Frustrating

When you shop for health insurance, you’re not just picking a product—you’re making decisions that affect your finances, your family’s well-being, and your access to care. The stakes are high, yet the process often feels opaque and unnecessarily complicated.

You’re expected to:

Compare dozens of plans with unfamiliar terms,

Check if your providers are covered (without reliable tools),

Predict your income a year in advance,

And hope you don’t make a mistake that costs you money or coverage.

Tips for a Smoother Experience

While the system isn’t perfect, there are ways to reduce frustration:

Use a Licensed Agent or Broker: Agents specializing in ACA plans can often help you find plans that include your provider and determine if you qualify for subsidies—all at no extra cost.

Call Your Doctor’s Office: Don’t rely solely on insurance directories. Call your provider’s office directly to confirm if they accept a specific plan.

Keep Documentation: If your income fluctuates, keep clear records. This will help you provide accurate estimates and support your case in the event of an audit or dispute.

Update Changes Promptly: If your income or household size changes mid-year, report it on your health insurance marketplace to avoid surprise bills or tax penalties.

In Summary

Shopping for individual or family health insurance can be a stressful process—especially when you’re trying to keep your doctor and figure out if you qualify for financial help. Between restrictive HMO networks and confusing subsidy rules, it’s easy to feel stuck. But with a little extra diligence, some expert help, and the right questions, you can find a plan that fits your needs without sacrificing peace of mind.

If the process still feels overwhelming, you’re not alone. Many Americans share the same frustrations—and continue to hope for a more user-friendly system in the future.

Below is a chart outlining estimated income thresholds for qualifying for an Advance Premium Tax Credit (APTC) in 2025. These thresholds are based on a percentage of the Federal Poverty Level (FPL), which is adjusted annually. For simplicity, the chart includes 2024 FPL figures (used for 2025 coverage) and the income ranges (100%–400%+ of FPL) where most people qualify for subsidies under the ACA.

📝 Note: Due to the American Rescue Plan and Inflation Reduction Act, subsidies may extend beyond 400% of the FPL, with a sliding scale that caps the percentage of income spent on premiums. These extended subsidies are currently in place through 2025.

2024 Federal Poverty Level (FPL) and APTC Income Guidelines for 2025 Coverage

Household Size100% / FPL400% / FPLTypical APTC Eligibility Range

Minimum Income: You must earn at least 100% of the FPL to qualify for a subsidy in most states. In Medicaid expansion states, if you earn less than 138% FPL, you may qualify for Medicaid instead.

Upper Limit Removed: Thanks to temporary reforms, people earning above 400% FPL may still qualify for a subsidy if the cost of the benchmark plan exceeds ~8.5% of their income.

Household Size: Includes you, your spouse, and any dependents claimed on your tax return.

💡 What This Means for You

If your estimated annual income falls between the ranges shown above, you likely qualify for help paying your monthly health insurance premium.

Households earning more than 400% of the FPL may still qualify if their premiums exceed about 8.5% of income, thanks to current federal subsidy expansions.

Eligibility is based on your tax household — including you, your spouse, and dependents you claim on your tax return.

If your income is below 138% FPL, you may qualify for Medicaid (in most states).

DO NOT CALL AN 800 NUMBER and talk to some anonymous employee of an insurance company. Not only are they restricted to limiting you exclusively to their company’s options—but your personal information will be instantly sold and shared. Your phone is going to begin ringing off the hook!

I’ve been specializing in Medicare-related insurance for over thirty years, right here in The Woodlands, Texas, USA! I represent every Medicare-related product, including Supplement, Advantage, and Part D Drug plans, from virtually every “A” rated company doing Medicare-related business in Texas. And I CHARGE NO FEE for my services! Deal with a local agent/broker who values your business enough not to share it with anyone!

D. Kenton Henry Editor, Agent, Broker Office: 281.367.6565 Text my cell 24/7 @713.907.7984 Email: Allplanhealthinsurance.com@gmail.com

By D. Kenton Henry Editor, HealthandMedicareRelatedInsurance.com Agent, Broker 28 January 2025

Hello again, and welcome to 2025! Early last October, just prior to the Medicare Annual Election Period (AE), I informed you of the many changes coming to Medicare Part D Prescription Drug Plans in the coming calendar year in which we now find ourselves. I explained the pros and cons that many of you are now experiencing in real time. On the positive side, I am certain many are celebrating that their annual drug costs (for Part D covered drugs) can never go beyond the new annual maximum out-of-pocket (OOP) of $2,000! And, hopefully, you are not experiencing the negatives—such as learning your Rx drug (which was previously covered) is no longer or its price has increased dramatically! Once again, we realize the government can giveth or taketh away.

But there is one thing in which you have a certain amount of control, and this is the ideal time of year to exercise that control. During the AEP, insurance companies, agents, and brokers work overtime seven days a week to see that their clients, and prospective clients, are guided to the Medicare Advantage and Part D Drug plans that best meet their needs. To do this correctly, an agent must understand the client’s needs and objectives and then do, what is often, extensive research to ensure a person’s drugsare covered and they have access to their preferred providers. In some cases, this can take minutes and, in others, hours over repeated phone calls. In most cases, you won’t get the latter from a company employee on the end of an 800 number, but you will get it from me.

Now that the AEP ended December 7th, agents have much more time to assist you in improving the cost of your Medicare Supplement coverage. As you may know, Medicare Supplement is not subject to annual enrollment periods in Texas or most states. What this means, is you can re-shop your Supplement coverage to find identical (or improved) coverage 365 days per year. The incentive for doing so is that you may save 30% or more in premiums. Because Medicare Supplement premiums go up each year as we age, it doesn’t take too many years before most of us begin to wonder if our premium is still reasonable or competitive. The reality is, if your policy is three years or older, you will indeed safe significantly by switching to a policy with the same letter designation, e.g., Plan G. I have many clients whose policy premiums had increased to well over $300 per month that I was able to lower (with new coverage) to less than $200 per month!

Additional reasons to re-shop now are that a few “A” rated companies are particularly interested in expanding their block of business. This does not imply a compromise in the quality of their customer service or rate stability. It simply means that through prudent management and staff expansion, they can be more competitive, significantly lowering your premium. Additionally, you may now have a spouse, or in some cases, simply another adult living with you—making your new policy available for a “Household Discount”. Typically, these discounts can lower your premium 7-12%, and—if the other person is covered by the same company—that discount will apply to their existing policy also!

So what is the catch? The catch is that now that you have been in Medicare Part B 6 months or more, you must go through underwriting and be approved for the new coverage based on your current health and relatively recent health history. The bottom line is, if your current conditions are well controlled with medication, you do not suffer from any chronic condition that poses a long-term liability to the insurance company, and you have no pending surgeries or hospitalizations—you are a good candidate for replacement coverage. The worst scenario is you are declined. In this case, all you are out of is the small amount of time you took to complete the application.

THE FOLLOWING IS A SYNOPSIS OF THE PROS AND CONS OF RE-SHOPPING YOUR COVERAGE:

Re-shopping a Medicare Supplement (Medigap) policy can provide several advantages for recipients, especially if their needs or circumstances have changed since they first enrolled. Here are the key benefits:

1. Cost Savings

Premium Reduction: Medigap premiums can vary significantly between providers for the same coverage. Shopping around may uncover lower premiums for the same plan (e.g., Plan G or Plan N).

Health Status Discounts: If your health has improved since your initial enrollment, you might qualify for a lower premium rate with another insurer.

Household Discounts: Some insurers offer discounts if multiple members of the household enroll in their Medigap plans.

2. Better Coverage Options

Change in Needs: If your healthcare needs have increased or decreased, you might find a plan that better aligns with your current situation, such as switching from a high-deductible plan to one with lower out-of-pocket costs.

Additional Benefits: New Medigap plans might include perks like fitness programs, telehealth, or wellness benefits that weren’t available when you initially enrolled.

3. Access to New Insurers

Competitive Market: New insurers entering the market may offer attractive rates or better customer service than your current provider.

Provider Reputation: Switching to a more reputable insurer can improve your overall satisfaction and ensure reliable claims processing.

4. Avoiding Rate Increases

Age-Based Increases: Some policies increase rates as you age. Shopping around may allow you to switch to a community-rated policy where premiums are based on a group average rather than individual age.

Annual Adjustments: If your current insurer has raised premiums significantly, exploring alternatives can help you lock in a more stable rate.

5. Improved Customer Service

If your current insurer has poor customer service or limited support, switching to a provider with higher satisfaction ratings can enhance your overall experience.

6. Medicare Advantage Comparison

While re-shopping Medigap policies, some recipients may realize that a Medicare Advantage (Part C) plan is more cost-effective or suitable for their needs. These plans often include additional benefits like dental, vision, and hearing coverage.

7. Regulatory Benefits

Guaranteed Issue Rights: In some situations (e.g., losing coverage or moving), recipients have guaranteed issue rights, allowing them to switch Medigap plans without medical underwriting.

Trial Rights: If you tried a Medicare Advantage plan for less than 12 months and decide to switch back to Original Medicare, you may have a guaranteed right to re-enroll in a Medigap plan.

8. Customizing for Future Needs

Planning ahead for potential healthcare changes can ensure that you are prepared for costs that might arise later, such as skilled nursing care or extensive outpatient services.

Considerations When Re-Shopping

Medical Underwriting: Outside of guaranteed issue periods, you may need to answer health questions, which could affect your eligibility or rates.

Plan Standardization: All Medigap plans with the same letter (e.g., Plan G) offer identical core benefits, regardless of the insurer, making it easier to compare prices.

Timing: The best time to switch is typically during your open enrollment period or when you have guaranteed issue rights.

By re-shopping their Medigap policy, Medicare recipients can ensure they are getting the best value and coverage for their evolving needs.

I am an independent agent with more than three decades in the medical insurance industry. As I have aged, so have my clients, and Medicare-related insurance (Supplement, Advantage, Part D) has become my specialty. I represent virtually every “A” rated insurance company in Texas as well as three others. I provide objective advice based on empirical numbers inclusive of costs and satisfaction surveys.

Significantly, I do not charge a fee for my service. You are charged no more for acquiring a product through me than if you went in the front door of the insurance company whose product you elected and acquired it directly from them!

Please allow me to assist you in lowering the cost of your Medicare-related insurance. I look forward to working with you!

If the administration and main stream media will not tell you–I will:

You can go through me–or any licensed health insurance agent or broker to acquire health insurance. NOW. And this is whether you qualify for a subsidy or not. And, importantly, there will be no, I repeat – $0 difference in your cost (premium) for doing so vs. the government website Healthcare.gov or a private insurance company’s. Period. Now where have you heard “Period” before and it turned out to be true? Well . . . in this case it is.

There is only ONE reason to go to the still basically inoperable, security in doubt, aforementioned federal government health insurance website known as The Marketplace:

1) You qualify for a subsidy of your 2014 health insurance premium and you would like to take advantage of that subsidy as you pay your premiums. I.e., you qualify and would like the premium you pay to your insurance company to be reduced by the amount of your subsidy as you pay the premium. (This as opposed to paying the gross premium (cost before your subsidy is applied) then declaring your subsidy on your 2014 tax return and having your tax liability reduced accordingly.)

If you this does not describe you – there is absolutely no reason to go to healthcare.gov!

Neither do you need to go through a state appointed, federally funded Navigator, hired by the State and required to complete only 20 hours of online education and be subjected to no background check. Why replicate and risk the possible insecurity of your personal information which includes your address; birth date; social security number and reported income by going through someone not even vetted by the Department of Health and Human Services (HHS) or the Center for Medicare Services (CMS)? As the Secretary for HHS, Kathleen Sebelius, admitted under oath and questioning from Texas Senator John Cornyn during Congressional, hearings just last week – “It is possible (for a convicted felon to be hired as a Navigator and take your personal and vital information).”

This begs the question: Why is the administration and main stream media not advertising, and barely mentioning, that a health insurance shopper can go through a licensed and vetted insurance agent who has passed a background check with every company with whom they are appointed and do so at no additional cost? Or that the shopper can then have all the expertise that that agent’s time in the industry (27 years in my case) brings to bear on their needs and situation? Or how about a “go to” advocate in their behalf they can call whenever there is an issue relating to claims; rates or general service related issues such as changes in address or dependents. This as opposed to a different unknown service rep at the end of a toll free number each time they call an insurance company directly?

I will let you speculate on the answers to these questions but (while the purpose of this blog is to educate the follower on issues relating to health and Medicare insurance) indulge me while I for once engage in a little shameless self-promotion on behalf of myself and all licensed agents and brokers:

If you reside in Texas; Indiana; or Ohio – please visit my website at http://allplaninsurance.com and click on the bold red “Get A Quote!” button on the home page or–better yet–call me toll free @ 800.856.6556 and let’s have an intelligent dialogue about your true wants and needs relative to coverage and then get some meaningful quotes and information for you. All without submitting the equivalent of a home mortgage application!

If you reside in any other state – do yourself a favor and call a well recommended licensed health insurance agent or broker in your community.

Again, call me even if you do qualify for a subsidy. I can help you just the same and–as without a subsidy–your cost for insurance will be the same. If you do not want to take the subsidy now but would rather take it on your 2014 tax return (when you actually know what your income will have been) we can apply for you now and have your coverage issued immediately.

If you want the subsidy applied upfront, to reduce the premium you pay each month, we will still have to enter the healthcare.gov website. But we will do so only after we have obtained your gross quotes via my website. I know the formula and can do a pretty fair job of estimating your net premium (after your subsidy is applied). If this scenario describes you, as the federal website is still inoperable, we should wait and see if HHS and CMS have the site fixed and secure by November 30th as promised. Let’s keep our fingers crossed and–if so–we should sail (wink, wink) through the application and have your coverage issued by January 1. But remember, if all government deadlines remain as now, we will need to complete your application no later than December 15th!

Well folks, here we are into the third week since the highly touted, much anticipated opening of the federal and state exchanges for purposes of enrolling in a health care act compliant insurance plan for 2014. And guess what? While a few state exchanges are experiencing some, generally small, measure of success – the federal exchange, or Marketplace, remains a dismal failure. It is, however, an excellent painful and protracted self-flagellating exercise in frustration. For an analogy–imagine having a root canal absent anesthesia while listening to Debbie Boone’s, “You Light Up My Life” on a continuous sound track loop through the entire procedure. Just to make the comparison more accurate, imagine you are Dustin Hoffman’s character who is tortured with a dentist’s drill in the movie Marathon Man but your experience is enhanced as your hygienist pulls your toe nails out with a pair of needle nose pliers in order to distract you from your oral discomfort. And that, I believe, is a pretty fair comparison to the enjoyment of opening an account and obtaining quotes for health insurance in the Marketplace to date. The tax payer’s cost to deliver this electronic equivalent of a Halloween visit to a House of Horrors? Current estimates are over $500 million and growing as desperate measures are being made to fix all its glitches as this goes to press. This after the Department of Health and Human Services accepted the low bid of $55 million with a ceiling of $93.7 million from Canadian software company, CGI Federal. Canadian? Really? All that U.S. taxpayer money to a Canadian firm? (I’m not even going there.)

But relax, dear patient. Let’s apply a little Novocain to your orifice. Let’s give you a subsidy to help ease the pain you will suffer when you see the highly inflated cost of health insurance you are now commanded to purchase under threat of penalty.

People making between 100 and 400 percent of federal poverty level can qualify for the premium tax credit health insurance subsidy. Federal poverty level changes every year, and is based on your income and family size.

Using 2013 FPL levels, you’ll qualify as an individual with an income range of $11,490-$45,960, a couple with an income of $15,510-$62,040, and a family of three earning $19,530-$78,120.

Just how do you calculate your subsidy?

In order to calculate how much your premium tax credit (subsidy) will be – you have to know 2 things:

(A) Your expected contribution toward the cost of your health insurance (available at the end of this article); and

(B) The cost of your BENCHMARK health plan. (Your health insurance exchange–assuming you succeed in opening an account and obtaining quotes–can tell you which plan this is and how much it costs. Your benchmark plan is the silver-tiered health plan with the second lowest monthly premiums in your area. The Affordable Care Act classifies health plans based on how much of your health care costs they’re expected to cover. A bronze health plan will cover about 60 percent of the average person’s health care costs. A silver health plan will cover about 70 percent.)

Your subsidy amount is the difference between your expected contribution and the cost of the benchmark plan. But just because the benchmark plan is used to calculate your subsidy doesn’t mean you have to buy the benchmark plan. You may buy any plan listed on your health insurance exchange, but your subsidy amount stays the same.

If you choose a more expensive plan, you’ll pay the difference plus your expected contribution. If you choose a plan that’s cheaper than the benchmark plan, you’ll pay less since the subsidy money will cover a larger portion of the monthly premium. If you choose a plan so cheap that costs less than your subsidy, you won’t have to pay anything for health insurance. However, you won’t get the excess subsidy back.

If you’re trying to save money so you choose a plan with a lower value, (like a bronze plan instead of a silver plan), you’ll likely have higher coinsurance and copays when you use your health insurance.

There’s another reason to choose a silver-tier plan. There’s a different subsidy that lowers copays, coinsurance, and deductibles for some low-income people. Eligible people can use it in addition to the premium tax credit subsidy. However, it’s only available to people who choose a silver-tier plan.

One question I am frequently asked is, “Do I have to wait until I file my income tax return in order to get the subsidy?”

Answer: “No”

You can get the premium tax credit in advance. If your income is so low you don’t have to file a tax return, you can still get the subsidy. But bear in mind–if you underestimate your income and take a subsidy–you will be forced to pay it back or, if you are due a refund, have it reduce such respectively when you file your return. (Income verification was put back in 2014 subsidy provisions after being suspended for one year along with the Administration’s one year suspension of the mandate that large employers must purchase health insurance for their employees. And remember–the IRS is in charge of monitoring your enrollment and expenditure.)

Consider opting to get the subsidy along with your tax refund if:

Your income is very close to 400 percent of FPL.

Your income varies from year to year so you’re not sure how much you’ll make.

When the subsidy is paid in advance, the amount of the subsidy is based on an estimate of your income for the coming year. If the estimate is wrong, the subsidy amount will be incorrect.

If you earn less than estimated, the advanced subsidy will be lower than it should have been. You’ll get the rest as a tax refund.

If you earn more than estimated, the government will send too much subsidy money to your health insurance company. You’ll have to pay back part or all of the excess subsidy money when you file your taxes. Even worse, if your actual income ended up more than 400 percent of FPL, you’ll have to pay back every penny of the subsidy. This could be thousands of dollars.

If you get your subsidy when you file your income taxes rather than in advance, you’ll get the correct subsidy amount because you’ll know exactly how much you earned that year. You won’t have to pay any of it back.

The Marketplace’s software will (supposedly) calculate your subsidy. Perhaps, as time goes by, it will even do so accurately. But for those of you who scored at least 600 on your high school SAT math test and enjoy such things – here is the exact formula for keeping the government honest:

Figure out how your income compares to FPL.

Find your expected contribution rate in the table below.

Calculate the dollar amount you’re expected to contribute.

Find your subsidy amount by subtracting your expected contribution from the cost of the benchmark plan.

Here is an example:

Mary is single with an income of $22,800 per year. FPL for 2013 is $11,490 for single people.

To figure out how Mary’s income compares to FPL, use: income ÷ FPL x 100.

$22,800 ÷ $11,490 x 100 = 198.4.

Mary’s income is 198 percent of FPL.

Using the table below, Mary is expected to contribute 4-6.3 percent of her income. Since she’s almost at the top of her category in the table, she uses the 6.3 percent figure.

To calculate how much Mary is expected to contribute, use this equation: 6.3 ÷ 100 x income.

6.3 ÷ 100 x $22,800 = $1,436.

Mary is expected to contribute $1,436 per year, or about $120 per month, toward the cost of her health insurance. The premium tax credit subsidy pays the rest of the cost of the benchmark health plan.

The benchmark health plan at Mary’s health insurance exchange costs $3,900 per year or $325 per month. Use this equation to figure out the subsidy amount: cost of the benchmark plan – expected contribution = amount of the subsidy.

$3,900 – $1,436 = $2,464.

Mary’s premium tax credit subsidy will be $2,464 per year or about $205 per month.

If Mary chooses the benchmark plan, or another $325 per month plan, she’ll pay $120 per month for her health insurance. If she chooses a plan costing $425 per month, she’ll pay $220 monthly for her health insurance. If she chooses a plan costing $225 per month, she’ll only pay $20 per month for her health insurance.

FEDERAL POVERTY LIMIT BASED ON NUMBER OF FAMILY IN HOUSEHOLD:

(Click on image to enlarge.)

Table of Your Expected Contribution Percentage:

If your income is

Your expected contribution will be

100%-133% of FPL

2% of your income

133%-150% of FPL

3%-4% of your income

150%-200% of FPL

4%-6.3% of your income

200%-250% of FPL

6.3%-8.05% of your income

250%-300% of FPL

8.05%-9.5% of your income

300%-400% of FPL

9.5% of your income

I hope your weather is not as beautiful as it is here in my part of Texas on this Sunday afternoon. If so, you are probably regretting you took the time to get this far into this hopefully informative piece. If it is – do not blame me and certainly–do not shoot the messenger.

As for me, I’m getting out on my motor bike and will take my mind off this monumental cross I bear being . . .

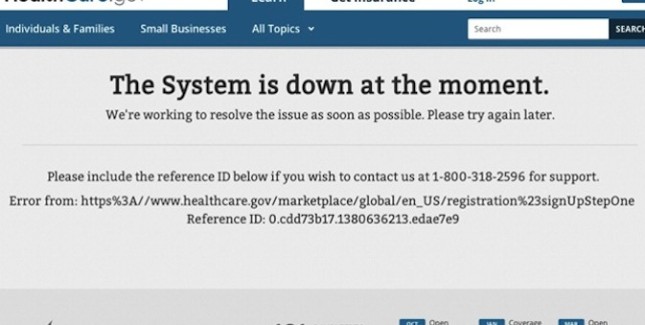

The Healthcare.gov website requires that individuals looking for coverage enter personal information before comparing plans. IT experts believe that this requirement is causing the website to crash.

A growing consensus of IT experts, outside and inside the government, have figured out a principal reason why the website for Obamacare’s federally-sponsored insurance exchange is crashing. Healthcare.gov forces you to create an account and enter detailed personal information before you can start shopping. This, in turn, creates a massive traffic bottleneck, as the government verifies your information and decides whether or not you’re eligible for subsidies. HHS bureaucrats knew this would make the website run more slowly. But they were more afraid that letting people see the underlying cost of Obamacare’s insurance plans would scare people away.

HHS didn’t want users to see Obamacare’s true costs

“Healthcare.gov was initially going to include an option to browse before registering,” report Christopher Weaver and Louise Radnofsky in the Wall Street Journal. “But that tool was delayed, people familiar with the situation said.” Why was it delayed? “An HHS spokeswoman said the agency wanted to ensure that users were aware of their eligibility for subsidies that could help pay for coverage, before they started seeing the prices of policies.” (Emphasis added.)

As you know if you’ve been following this space, Obamacare’s bevy of mandates, regulations, taxes, and fees drives up the cost of the insurance plans that are offered under the law’s public exchanges. A Manhattan Institute analysis I helped conduct found that, on average, the cheapest plan offered in a given state, under Obamacare, will be 99 percent more expensive for men, and 62 percent more expensive for women, than the cheapest plan offered under the old system. And those disparities are even wider for healthy people.

That raises an obvious question. If 50 million people are uninsured today, mainly because insurance is too expensive, why is it better to make coverage even costlier?

Political objectives trumped operational objectives

The answer is that Obamacare wasn’t designed to help healthy people with average incomes get health insurance. It was designed to force those people to pay more for coverage, in order to subsidize insurance for people with incomes near the poverty line, and those with chronic or costly medical conditions.

But the laws’ supporters and enforcers don’t want you to know that, because it would violate the President’s incessantly repeated promise that nothing would change for the people that Obamacare doesn’t directly help. If you shop for Obamacare-based coverage without knowing if you qualify for subsidies, you might be discouraged by the law’s steep costs.

So, by analyzing your income first, if you qualify for heavy subsidies, the website can advertise those subsidies to you instead of just hitting you with Obamacare’s steep premiums. For example, the site could advertise plans that cost “$0″ or “$30″ instead of explaining that the plan really costs $200, and that you’re getting a subsidy of $200 or $170. But you’ll have to be at or near the poverty line to gain subsidies of that size; most people will either not qualify for a subsidy, or qualify for a small one that, net-net, doesn’t make up for the law’s cost hikes.

This political objective—masking the true underlying cost of Obamacare’s insurance plans—far outweighed the operational objective of making the federal website work properly. Think about it the other way around. If the “Affordable Care Act” truly did make health insurance more affordable, there would be no need to hide these prices from the public.

Subsidy verification created a traffic bottleneck

Comparable private-sector e-commerce sites, like eHealthInsurance.com, allow you to shop for plans and compare prices simply by entering your age and your ZIP code. After you’ve selected a plan you like, you fill out an on-line application. That substantially winnows down the number of people who rely on the site for network-intensive tasks.

The federal government’s decision to force people to apply before shopping, Weaver and Radnofsky write, “proved crucial because, before users can begin shopping for coverage, they must cross a busy digital junction in which data are swapped among separate computer systems built or run by contractors including CGI Group Inc., the healthcare.gov developer, Quality Software Services Inc., a UnitedHealth Group Inc. unit; and credit-checker Experian PLC. If any part of the web of systems fails to work properly, it could lead to a traffic jam blocking most users from the marketplace.”

Jay Angoff, a former federal official at the agency that oversees the exchange, told the Journal that he was surprised by the decision. “People should be able to get quotes” without entering all of that information upfront.

Weaver and Radnofsky say that the core problem stems from “the slate of registration systems [that] intersect with Oracle Identity Manager, a software component embedded in a government identity-checking system.” The main Healthcare.gov web page collects information using the CGI Group technology. Then that data is transferred to a system built by Quailty Software Services. QSS then sends data to Experian, the credit-history firm. But the key “identity management system” employed by QSS was designed by Oracle, and according to the Journal’s sources, the Oracle software isn’t playing nicely with the other information systems.

Oracle hotly denies these claims. “Our software is the identical product deployed in most of the world’s most complex systems…our software is running properly,” said an Oracle spokeswoman in a statement.

‘It’s awful, just awful’

Robert Pear and colleagues at the New York Times have a piece up today detailing the serious problems with the federal exchange, problems that may get worse, not better. They confirm what we already knew: that the Obama administration refused to delay the implementation of the exchanges, despite the well-known problems, because they were afraid of the political blowback. “Former government officials say the White House, which was calling the shots, feared that any backtracking would further embolden Republican critics who were trying to repeal the health care law.”

As I documented last week, IT and insurance experts have been saying for at least eight months that implementation of the exchanges was going badly, that as early as February officials were warning of a “third world experience.” The Times’ sources are just as blunt. “These are not glitches,” said one insurance executive. “The extent of the problems is pretty enormous. At the end of our [conference calls with the administration], people say, ‘It’s awful, just awful.’”

“We foresee a train wreck,” said another executive in a February interview with the Times. “We don’t have the IT specifications. The level of angst in health plans is growing by leaps and bounds. The political people in the administration do not understand how far behind they are.” Richard Foster, the former chief actuary at the Centers for Medicare and Medicaid Services, said last week that “so much testing of the new system was so far behind schedule, I was not confident it would work well.”

Henry Chao, the deputy chief information officer at CMS who made the “third world experience” comment, was told by his superiors that failure to meet the October 1 launch deadline “was not an option,” according to the Times.

White House knowingly chose to court disaster

Think about it. It’s quite possible that much of this disaster could have been avoided if the Obama administration had been willing to be open with the public about the degree to which Obamacare escalates the cost of health insurance. If they had, then a number of the problems with the exchange’s software architecture would never have arisen. But that would require admitting that the “Affordable Care Act” was not accurately named.

The White House knew that its people on the front lines, people like Henry Chao, were worried that the exchanges would get botched. They saw the Congressional Research Service memorandum detailing that the administration has missed half of the statutory deadlines assigned by the law. But they were more afraid of the P.R. disaster of disclosing Obamacare’s high premiums than they were of the P.R. disaster of crashing websites. What you see is the result.

************************

Tech experts: Health exchange site needs total overhaul

Kelly Kennedy, USA TODAY 5:36 p.m. EDT October 17, 2013Health and Human Services Secretary Kathleen Sebelius calls the rollout of the health care exchanges rocky. (Photo: Jose Luis Magana, AP)

WASHINGTON — The federal health care exchange was built using 10-year-old technology that may require constant fixes and updates for the next six months and the eventual overhaul of the entire system, technology experts told USA TODAY.

The site could be perfect, but if the systems from which it draws data are not up to speed, it doesn’t matter, said John Engates, chief technology officer at Rackspace, a cloud computer service provider.

“It is a core problem in the sense of it’s fundamental to this thing actually working, but it’s not necessarily a problem that the people who wrote HealthCare.gov can get to,” Engates said. “Even if they had a perfect system, it still won’t work.”

Recent changes have made the exchanges easier to use, but they still require clearing the computer’s cache several times, stopping a pop-up blocker, talking to people via Web chat who suggest waiting until the server is not busy, opening links in new windows and clicking on every available possibility on a page in the hopes of not receiving an error message. With those changes, it took one hour to navigate the HealthCare.gov enrollment process Wednesday.

“I have never seen a website — in the last five years — require you to delete the cache in an effort to resolve errors,” said Dan Schuyler, a director at Leavitt Partners, a health care group by former Health and Human Services secretary Mike Leavitt. “This is a very early Web 1.0 type of fix.”

“The application could be fundamentally flawed,” said Jeff Kim, president of CDNetworks, a content-delivery network. “They may be using 1990s technology in 2.0 world.”

Outsiders acknowledged they can’t see the whole system, but they said they feared HHS built a system that will need an expensive overhaul that would cause more headaches for people trying to buy insurance.

“I will be the first to tell you that the website launch was rockier than we wanted it to be,” HHS Secretary Kathleen Sebelius said Wednesday at Cincinnati State Technical and Community College, adding that people have until Dec. 15 to enroll to ensure coverage beginning Jan. 1.

HHS officials did not respond to a request about the nature of the problems. However, they reiterated that wait times have been reduced or even eliminated as they continue to work to fix the system. As of Thursday, the site had received 17 million unique visitors.

“We continue to work around the clock to improve the consumer experience on HealthCare.gov,” HHS spokeswoman Joanne Peters said. “We are seeing progress: wait times to begin the online process have been virtually eliminated, and more consumers are creating accounts, completing applications and ultimately enrolling in coverage if they choose to do so at this time. However, we will not stop addressing issues and improving the system until the doors to HealthCare.gov are wide open.”

Engates said HHS has been opaque about the problems, and the tech industry doesn’t know the extent of the issues. “There’s no secrets leaking out,” he said. “I’m sure everyone’s looking for something to change the direction of the conversation, but it’s just not there.”

“I think it’s a data problem,” Kim said. “It always comes down to that.”

And if that’s the case, the problems are beyond “rocky,” he said. Instead, it would require a “fundamental re-architecture.” In the meantime, “I think they’re just trying to shore up as quickly as possible. They don’t have time to start from scratch.”

“If I was them, and I’m just conjecturing, I would probably come up with some manual way of saying, ‘Only people with the last name starting with ‘A’ can sign up today,” he said.

But come March 31, when the first enrollment period ends, the “shore up” period may become a “re-architecting” period, Kim said.

On a good note, he said, after looking at available code, the site is “very secure.”

Clearing the cache, which has helped make it easier for some people to enroll, could ultimately strain the system more, Kim said. That’s because a “cookie” is stored on a person’s computer that contains data, such as the person’s name and address, that can then be quickly accessed when that person gets on the website again instead of having to be retrieved from the government’s server.

But as HHS fixes errors, the cookies may not correspond with the updated website, so rather than allowing someone to quickly log in, they instead cause an error message. And every time a person clears his computer’s cache, the government’s website has to work that much harder to grab more data.

Requiring people who may not be Web savvy to use the site in any way other than a step-by-step easy process defeats the point of the whole system, Schuyler said. That includes laws mandating that insurers provide clear explanations about policies to people may make sound decisions and understand what they’re buying.

“Most consumers will have no idea what ‘clearing the cache’ is and this will just cause more confusion and frustration,” he said.

So far, the site’s problems have not driven away potential customers, according to a poll conducted by uSamp — United Sample Inc. The survey found that among the 832 people who attempted to log in, 38% received an error message, 50% were asked to try again later, 25% were unable to create an account, 31% were told the system was down, and 19% had no problems. About 83% said they would try again later, while 15% said they would wait until they heard the website was working well. About 70% of those who said they had no issues said they still waited to enroll because they want to think about their options.

Engates said he believes most of the problems are caused by systems integration with other sites, such as the IRS. And that could be causing some of the problems people see as they make it past the initial application process. It’s a series of questions meant to verify a person’s identity and income. But after that questionnaire, visitors often encounter a series of error messages, or the page a person tries to click to doesn’t come up. The data requests to other sites could be causing those problems, Engates said, which would mean the problem isn’t with the HHS site itself.

“Maybe the site is submitting a request for more data, and that puts you in that trap again,” he said. “It’s a giant integration problem that they have to solve.”

And as they try to fix those problems, there’s another issue lurking in the background: Some HHS personnel were named essential, and not subject to furloughs because of the government shutdown. But that didn’t apply to the other organizations they were working with, Engates said. So as HHS techs work around the clock to fix the problems, IRS techs may be prohibited from working at all.

In the meantime, HHS personnel can’t say anything about the situation, it can be played politically as “bad,” he said. If they say it will take two weeks to fix, they will be criticized because it’s taking too long. But he expects that it’s a problem that will be resolved soon, especially as the volume of visitors goes down.

“If you can get the system below some sort of threshold, it will perform as it’s supposed to,” Engates said. “It won’t get any worse. It’s going to get better little by little by little.”

I have just completed my Affordable Care Act (ACA) training and certification in order to offer ACA compliant plans to my clients, and the public in general, beginning October 1. However, even in this final hour with only eight days until the new plans are to be available – the insurance companies have still not released the premiums the insure will pay for these options. “Any day now” is what I am being told. However, I will share with you a thing or two I do know based on what I have studied.

Most of it came as no surprise to me. One major company (whose name I cannot divulge as the information they provided was yet to be approved by the Department of Health and Human Services (HHS) who will be in charge of the Federal-Run Exchange–Marketplace–in Texas, Indiana and Ohio–where I have clients) previewed plans. The lowest plan deductible available was $1,500. All plans will be limited to a maximum out-of-pocket of $6,350 per individual and $12,700 per family. While older people will probably find a $1,500 deductible acceptable in terms of affordability, I am not certain how twenty year olds are going to feel about that. I certainly don’t think that and higher deductible options will be an incentive for them to enroll even with the convenience of doctor’s office co-pays and prescription drug cards. I can almost guarantee you that unless they receive a subsidy – they won’t be signing up.