Well, here we are, two days from Obamacare Open Enrollment. Tuesday, November 1st, the starting gun goes off for Americans to shop for 2017 health insurance and we cross the finish line January 31st, at which point, our health insurance―barring a significant life change―will be locked in the remainder of the year. This month is my 30th year in the industry and it is my job to help you identify and elect your best health insurance option for 2017.

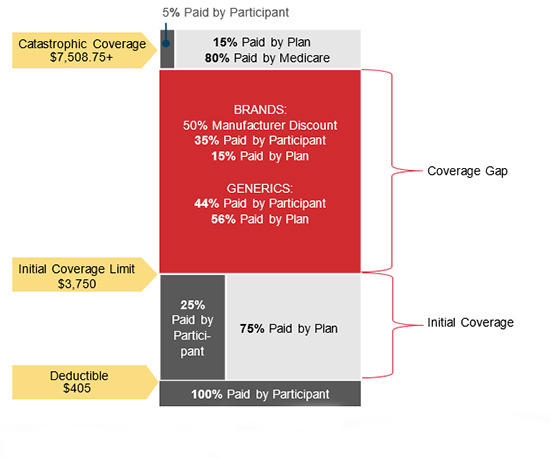

Here are the challenges ahead of us. As those of you who were in Under Age 65 health insurance market last year well know, you were forced off your PPO plan (assuming you were in one) and into HMO coverage. And you learned it was extremely difficult to find your doctors and hospitals in any HMO plan network. (In an HMO plan, you must utilize providers in your network or you have no coverage whatsoever.) Hence, you found your doctors, hospitals, and, effectively, your treatment rationed. Previews of the 2017 plans and premiums indicate most insurance companies have withdrawn from the market and those remaining are continuing to offer HMO coverage only. To add insult to injury, they are offering it at dramatically higher premiums. In Texas, premiums are 25% higher on average. And they are much higher in many other states.

As I write, plan and premium change notices are arriving in the mail and pushing the edge out of the sticker shock envelope. My own arrived, and while a 23% increase sounds good relative to what many of my clients are experiencing, the insurance company is also raising the deductible on my plan by a thousand dollars. A client left a message in my voicemail late Friday evening informing me his premium is increasing 58.9%. He went on to say, “That is unsustainable and I will pay the penalty before I pay that premium! We will have to find something else!” What he may not know yet―and what I will have to inform him―is that he will only have plans for two companies to choose from in his county. One is the company he is with. Regardless, all the options he will have are at significantly higher premiums than last year. Since 2014 (the first year Americans whose net income fell below a certain threshold were able to receive subsidies to offset a portion of their health insurance premium) I have said―if you qualify for a significant one―you may be happy with your health insurance premium. However, if you are one of the millions of hard working Americans making just above that threshold―in all likelihood―you are, like my client who left the voicemail, distraught over what is happening to your health insurance costs.

That being said, and as was already said, it is my job to help you identify your best option. And to do so without foregoing health insurance protection and paying the ensuing penalty for doing so. The strategy I employed for myself in 2016 is the same I will be utilizing in 2017. It is not what I would prefer, but what I would prefer is not an option. It is, however, the best option in light of the circumstances. Finances may not be your concern but access to your providers may be. Or, access to your providers may not be your concern but finances may be. Both may be your concern. My strategy may work for you or it may not. But I feel it provides the least compromise and is the best for adapting to this current state of affairs. At least until better options avail themselves in the individual and family health insurance market. Please contact me at 281–367–6565 to discuss it. If you feel it, or another approach, is the way you would like to proceed, I can make the application process go as quickly and smoothly as possible. And that is whether you qualify for a subsidy or not and without you having to personally deal with healthcare.gov.

ATTENTION SMALL BUSINESS OWNERS: You have possible recourse regarding the poor options in the individual and family health insurance market. If you are the owner of a legal business entity, e.g., LLC or corporation, you have an alternative. During the Small Business Open Enrollment Period (SBOEP)―from November 1 through December 15th―you may enroll your employer group and still have access to quality coverage and, more importantly, quality PPO provider networks where you are in control of who your providers are and, therefore, your treatment. During this SBOEP you will not have to meet the participation or contribution requirements which apply to small business group enrollment during the remainder of the year. In other words, you need only cover a minimum of two employees and you can require they pay 100% of their personal and family premium which will then be payroll deducted from their compensation. Please contact me if you have an interest in pursuing this strategy.

For those who are strictly in the market for individual and family health insurance, as of Tuesday, you may go to my website at http://TheWoodlandsTXHealthInsurance.com to review your options. While this site focuses on our hometown, it will provide quotes for residents of all 50 states. I can be the agent for residents of Texas, Indiana, Ohio and Michigan. Once there, you may apply online or call me to discuss the details of the options you see and I can submit your application for you. I the meantime (as of this moment), if you know―or believe―you qualify for a subsidy of your premium, you may go to my second quoting site where you may calculate the subsidy you qualify for or the penalty for not purchasing health insurance in 2017. You mag go on to obtain your quote and, if applying, log directly into healthcare.gov and apply. If doing so, when asked if you are working with anyone else on your coverage, select Agent or Broker and list my agent (legal) name, Donald Kenton Henry, and my National Producer Number (NPN) 387509. If you do this, I will be able to assist with any incomplete applications or outstanding requirements. If you become my client, in most cases, I can handle service related issues throughout the year without you having to deal with the personnel at healthcare.gov or an insurance company. The important thing I would like for you to appreciate is – you are charged not one penny more in premium by going through me for your health insurance than if you were to go directly through the front door of the insurance company whose product you wish to acquire and purchased it directly. And I charge no fee for my service. I only hope that, if I introduce you to a product you wish to utilize or a strategy, you wish to employ, you will acquire the product through me as your agent.

Click on this link to calculate penalties, subsidies and preview the plans available Tuesday, November 1: https://allplanhealthinsurance.insxcloud.com/my-quote/individual-info

I look forward to working with you and to, if becoming your agent, providing you the best of insurance service throughout the year. Again, please call me at 281–367–6565.

(Donald) Kenton Henry ― editor, broker

*******************************************************************

FEATURE ARTICLE

The New York Times

Health Law Tax Penalty? I’ll Take It, Millions Say

By ROBERT PEAR OCT. 26, 2016

The decision by many healthy people not to sign up under the Affordable Care Act, even if it means a tax penalty, is undermining the plan. CreditKaren Bleier/Agence France-Presse — Getty Images

WASHINGTON — The architects of the Affordable Care Act thought they had a blunt instrument to force people — even young and healthy ones — to buy insurance through the law’s online marketplaces: a tax penalty for those who remain uninsured.

It has not worked all that well, and that is at least partly to blame for soaring premiums next year on some of the health law’s insurance exchanges.

The full weight of the penalty will not be felt until April, when those who have avoided buying insurance will face penalties of around $700 a person or more. But even then that might not be enough: For the young and healthy who are badly needed to make the exchanges work, it is sometimes cheaper to pay the Internal Revenue Service than an insurance company charging large premiums, with huge deductibles.

“In my experience, the penalty has not been large enough to motivate people to sign up for insurance,” said Christine Speidel, a tax lawyer at Vermont Legal Aid.

Some people do sign up, especially those with low incomes who receive the most generous subsidies, Ms. Speidel said. But others, she said, find that they cannot afford insurance, even with subsidies, so “they grudgingly take the penalty.”

The I.R.S. says that 8.1 million returns included penalty payments for people who went without insurance in 2014, the first year in which most people were required to have coverage. A preliminary report on the latest tax-filing season, tabulating data through April, said that 5.6 million returns included penalties averaging $442 a return for people uninsured in 2015.

With the health law’s fourth open-enrollment season beginning Tuesday, consumers are anxiously weighing their options.

William H. Weber, 51, a business consultant in Atlanta, said he paid $1,400 a month this year for a Humana health plan that covered him and his wife and two children. Premiums will increase 60 percent next year, Mr. Weber said, and he does not see alternative policies that would be less expensive. So he said he was seriously considering dropping insurance and paying the penalty.

“We may roll the dice next year, go without insurance and hope we have no major medical emergencies,” Mr. Weber said. “The penalty would be less than two months of premiums.” (He said that he did not qualify for a subsidy because his income was too high, but that his son, a 20-year-old barista in New York City, had a great plan with a subsidy.)

Iris I. Burnell, the manager of a Jackson Hewitt Tax Service office on Capitol Hill, said she met this week with a client in his late 50s who has several part-time jobs and wants to buy insurance on the exchanges. But, she said, “he’s finding that the costs are prohibitive on a monthly basis, so he has resigned himself to the fact that he will have to suffer the penalty.”

When Congress was writing the Affordable Care Act in 2009 and 2010, lawmakers tried to balance carrots and sticks: subsidies to induce people to buy insurance and tax penalties “to ensure compliance,” in the words of the Senate Finance Committee.

But the requirement for people to carry insurance is one of the most unpopular provisions of the health law, and the Obama administration has been cautious in enforcing it. The I.R.S. portrays the decision to go without insurance as a permissible option, not as a violation of federal law.

The law “requires you and each member of your family to have qualifying health care coverage (called minimum essential coverage), qualify for a coverage exemption, or make an individual shared responsibility payment when you file your federal income tax return,” the tax agency says on its website.

Some consumers who buy insurance on the exchanges still feel vulnerable. Deductibles are so high, they say, that the insurance seems useless. So some think that whether they send hundreds of dollars to the I.R.S. or thousands to an insurance company, they are essentially paying something for nothing.

Obama administration officials say that perception is wrong. Even people with high deductibles have protection against catastrophic costs, they say, and many insurance plans cover common health care services before consumers meet their deductibles. In addition, even when consumers pay most or all of a hospital bill, they often get the benefit of discounts negotiated by their insurers.

The health law authorized certain exemptions from the coverage requirement, and the Obama administration has expanded that list through rules and policy directives. More than 12 million taxpayers claimed one or more coverage exemptions last year because, for instance, they were homeless, had received a shut-off notice from a utility company or were experiencing other hardships.

“The penalty for violating the individual mandate has not been very effective,” said Joseph J. Thorndike, the director of the tax history project at Tax Analysts, a nonprofit publisher of tax information. “If it were effective, we would have higher enrollment, and the population buying policies in the insurance exchange would be healthier and younger.”

Americans have decades of experience with tax deductions and other tax breaks aimed at encouraging various types of behavior, as well as “sin taxes” intended to discourage other kinds of behavior, Mr. Thorndike said. But, he said: “It is highly unusual for the federal government to use tax penalties to encourage affirmative behavior. That’s a hard sell.”

The maximum penalty has been increasing gradually since 2014. Federal officials and insurance counselors who advise consumers have been speaking more explicitly about the penalties, so they could still prove effective.

Many health policy experts say the penalties would be more effective if they were tougher. That argument alarms consumer advocates.

“If you make the penalties tougher, you need to make financial assistance broader and deeper,” said Michael Miller, the policy director of Community Catalyst, a consumer group seeking health care for all.

http://www.nytimes.com/2016/10/27/us/obamacare-affordable-care-act-tax-penalties.html?smid=fb-share&_r=0

http://thewoodlandstxhealthinsurance.com

http://allplanhealthinsurance.com

https://allplanhealthinsurance.insxcloud.com/my-quote/individual-info