By D. Kenton Henry

Perhaps a storm would be a better analogy but 2016 will deliver something more than a mild tropical depression to the coast of the “Individual and Family” health insurance market. At the same―the Cat 3 (minimum) hurricane projected to slam the Senior market of Medicare recipients appears to have been diverted. For now.

As we enter the third year of enrollment in health insurance plans compliant with the Affordable Care Act (ACA) the “Affordable” aspect of care or―more accurately―the cost of protecting oneself from the cost of health care―seems elusive and more and more a case of misrepresentation. As I have said many times in the past, if you qualify for a subsidy of your health insurance premiums you may find your options affordable. However, depending on where you live, you will surely be upset with the increasing cost of health insurance. 70% of all Obamacare members are enrolled in a Silver Plan. The Department of Health and Human Services (DHS), which oversees enforces the Act and oversees the health insurance industry, has designated the second lowest cost Silver Plan of any insurance company to be the default plan one must select in order to maximize the benefit of any subsidy. This could include a reduction in not only one’s premium but their deductibles and co-pays. As Fox News and the Washington Post report (see featured article below) the cost of these plans will rise by a national average of 7.5%. States such as Oklahoma will see an increase of 37.5%!

In some states it is much worse.

To add insult to injury many insurance companies, such as BlueCross BlueShield of Texas, have taken such losses―in spite of skyrocketing premiums―they have announced they are eliminating the Preferred Provider Organization (PPO) network option for their plans and member benefit. The only option will be to select a Health Maintenance Organization (HMO) network option wherein the company can ration your providers and treatment. While the young or otherwise very healthy may find this option acceptable, those of us who are older or dealing with existing illnesses or injuries are certain to be upset by this development. The insurance companies seem to be in agreement on the viability of PPOs and explain any premium increase necessary to assure they even break even on a PPO policy would be beyond the increase limit set by Obamacare. As such, it would therefore not be approved by their state insurance commissioner. So the question remains: what will your personal network and benefit options be for 2016 and what will they cost?

Virtually all insurance companies are keeping the answers close to their vest until this Sunday, November 1, the first day of OPEN ENROLLMENT wherein one may choose a health insurance plan for 2016. Enrollment will remain open until January 31st. Those without a plan at that time will be locked out for the remainder of the year and will pay a penalty equal to the higher of two amounts:

2.5% of your yearly household income (Only the amount of income above the tax filing threshold, about $10,150 for an individual in 2014, is used to calculate the penalty.) The maximum penalty is the national average premium for a Bronze plan

$695 per person ($347.50 per child under 18) The maximum penalty per family using this method is $2,085.

A banner follows which, as of Sunday, November 1st, you may click on and by simply entering your birth date, zip code and tobacco usage, obtain ALL your health insurance options from each and every insurance company issuing 2016 coverage in your state. It will also allow you to calculate what subsidy, if any, and enable you (if you choose) to log directly into the federal marketplace to acquire it and your insurance plan. If you have questions, as you most surely will, do not hesitate to contact me via my contact information via the link or below.

CLICK ON THIS BANNER TO OBTAIN 2016 HEALTH INSURANCE QUOTES:

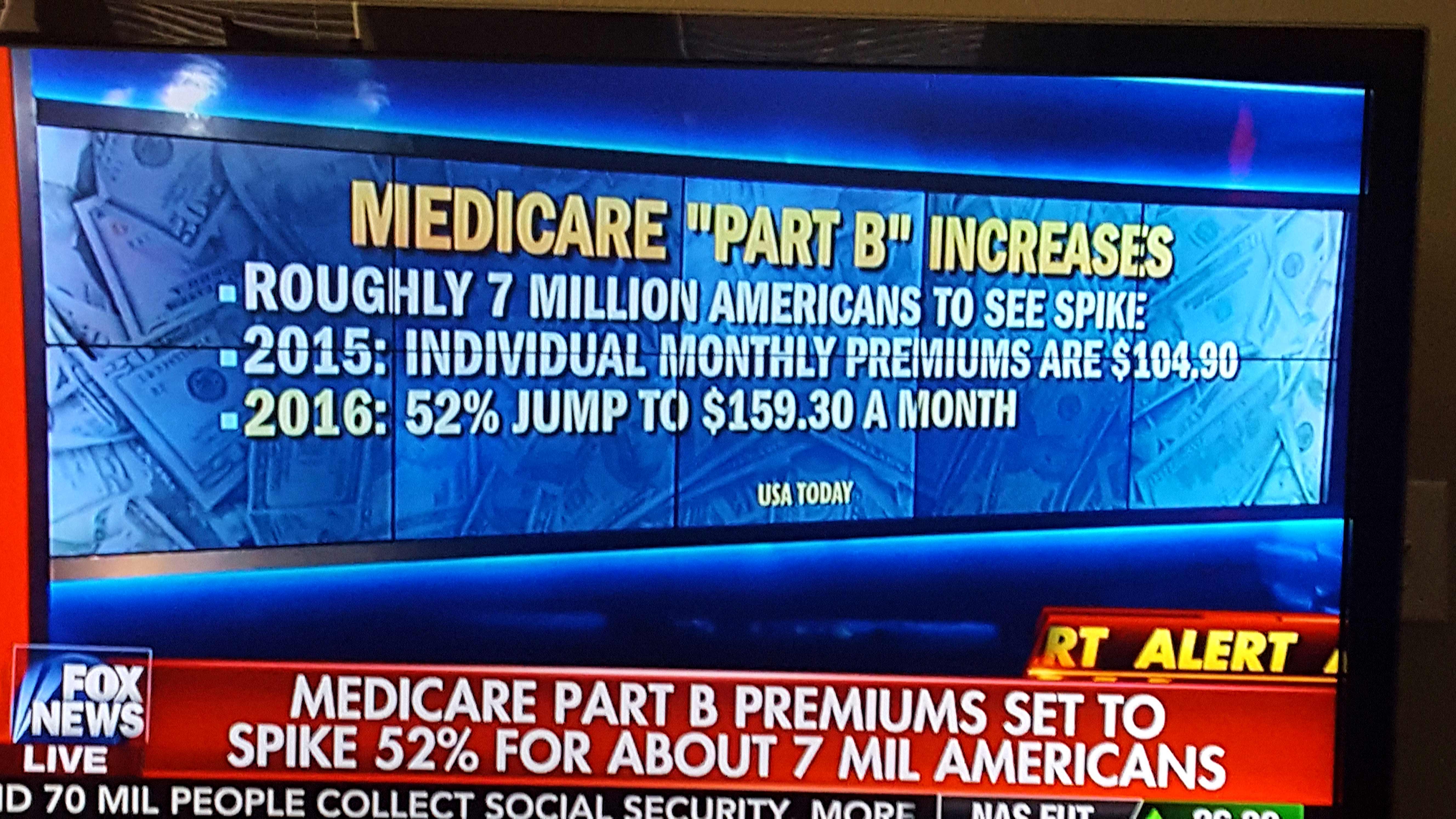

Relative to Medicare recipients, it would appear a planned increase in the 2016 Medicare Part B premium and deductible has been taken off the table for the time being. The increase would have resulted in a huge spike in what higher income recipients and new enrollees in Part B Out-Patient coverage would pay in premium. The proposed premium increase would have been as presented here:

Income Limits, Medicare Part B Premiums for 2016

| Single | Married | 2015 | 2016 Held Harmless | 2016 Not Held Harmless |

| $85,000 or less | $170,000 or less | $104.90 | $104.90 | $159.30 |

| $85,001 to $107,000 | $170,001 to $214,000 | $146.90 | $223.00 | |

| $107,001 to $160,000 | $214,001 to $320,000 | $209.80 | $318.60 | |

| $160,001 to $214,000 | $320,001 to $428,000 | $272.70 | $414.20 | |

| Above $214,000 | Above $428,000 | $335.70 | $509.80 |

The threat and legislation which averted this is described in detail in The Fiscal Times article below. As of today, it is still unclear to this editor whether the increase in the calendar year deductible has also been averted.

Editor, Broker, Agent ― D. Kenton Henry

Office: 281.367.6565

Cell (call or text): 713.907.7984

http://allplanhealthinsurance.com

http://thewoodlandstxhealthinsurance.com

Blog: http://healthandmedicareinsurance.com

*******************************************************************

FEATURED ARTICLES:

THE WASHINGTON POST

26 October 2015

2016 Affordable Care Act insurance rates are climbing

By Amy Goldstein October 26

The prices for a popular and important group of health plans sold through the federal insurance exchange will climb by an average of 7.5 percent for the coming year, a jump nearly four times bigger than a year ago, according to new government figures.

The rate increase for 2016 compares with average growth of 2 percent, from 2014 to this year, in the monthly premiums for a level of coverage that serves as the benchmark for federal subsidies that help most consumers buying coverage under the Affordable Care Act.

A “snapshot” of insurance rates, released Monday by the Department of Health and Human Services, also shows that the rate increases for next year vary substantially around the country. Although there are exceptions, more populous states and metropolitan areas tend to have more modest premium increases for the coming year than smaller areas.

The changes for next year have a wide range — from premium increases averaging 35 percent in Oklahoma and Montana to a decrease of nearly 13 percent in Indiana.

The analysis is based on hundreds of health plans sold in local markets within 37 states that use HealthCare.gov, the federal online insurance marketplace. It excludes plans in other states that have created separate ACA insurance marketplaces. The rates reflect the prices of the second-least expensive health plan in each market for 2016 in a tier of coverage known as silver. ACA health plans are divided into four tiers, all named for metals, depending on the amount of customers’ care that they cover. Silver plans have proven by far the most popular. Officials at HHS issued the analysis as less than a week remains before the start on Nov. 1 of a third open-enrollment season for Americans eligible to sign up for health plans under the insurance marketplaces created by the 2010 health-care law. The exchanges are intended for people who cannot get affordable health benefits through a job.

In their analysis, federal officials contend that the health plans sold through the exchanges will be affordable to people willing to shop for the best rates. The cost to consumers, HHS officials emphasize, is cushioned by the fact that nearly nine in 10 are eligible for tax credits.

Taking the subsidies into account, nearly four in five people who already have gotten insurance through these marketplaces will have access for 2016 to a health plan for which they could pay no more than $100 in monthly premiums, the analysis found. The analysis does not address other costs to consumers, such as co-payments and deductibles, which tend to be more expensive in ACA health plans than in employer-based health benefits.

The figures in the analysis reinforce a theme that Obama administration officials introduced last year and have revived as the third sign-up period approaches: the usefulness of researching the best and most affordable coverage, even if it means switching insurance from year to year. “If consumers come back to the Marketplace and shop, they may be able to find a plan that saves them money and meets their health needs,” Kevin Counihan, the HHS official who oversees the health exchanges, said in a statement.

The new figures show that existing customers who went back last fall to HealthCare.gov and picked a different plan at the same level of coverage saved an average of nearly $400 in premiums over the course of this year. Slightly fewer than one-third of those who bought such coverage for a second time switched health plans, according to the analysis. During this open enrollment, Obama administration officials are striving both to attract existing customers again and to ferret out Americans eligible for the exchanges who remain uninsured even though the law requires them to have coverage. Although many consumers can be largely shielded from rate jumps through subsidies and shopping around, the increases ratchet up the government’s expenditures on the tax credits that the law provides, health policy analysts point out.

Analysts have expected that premiums for the coming year would grow more rapidly than they did for 2015. “This is the first year that insurers actually have a full year of experience with how much care people use,” said Larry Levitt, senior vice president of the Kaiser Family Foundation, a health policy organization. “In the first two years of the program, insurers were essentially guessing.” In addition, Caroline Pearson, senior vice president at Avalere, a health-care consulting firm, said that, as some health plans have attracted a significant share of customers, “the need to price really low diminishes a little bit.” Clare Krusing, a spokeswoman for America’s Health Insurance Plans, the industry’s main trade group, said that “averages don’t tell the whole story” and that insurance rates hinge on “location and the cost of providing care to individuals in particular markets.” In particular, Krusing said, last year was “a record-breaking year for prescription drug prices. That trend is likely to continue.”

***********************************

Seniors Exhale as Congress Blocks Huge Medicare Increase

By Eric Pianin October 27, 2015 3:17 PM

Responding to pressure from seniors’ and labor groups as the 2016 campaign season heats up, congressional leaders and the White House have blocked a huge, 50 percent increase in the Medicare Part B premium for nearly one third of the 50 million elderly Americans who depend on the program for health services.

The bipartisan solution will block all but a tiny fraction of the premium increase. It is contained in the two-year budget and debt ceiling bill negotiated by House Speaker John Boehner (R-OH), House Minority Leader Nancy Pelosi (D-CA) and the White House and that awaits ratification by the two chambers – likely by the end of this week.

Related: Millions Facing a Hefty Increase in Medicare Premiums in 2016

The threatened sharp premium increase – reported back in August by The Fiscal Times – was triggered by a quirk in federal law that penalizes wealthier Medicare beneficiaries, newcomers to the program and lower income Americans with complicated chronic health problems. It kick in any time the Social Security Administration fails to approve an annual cost-of-living adjustment – as will be the case next year.

Medicare Part B and the Social Security trust fund are interconnected, and most seniors on Medicare have their monthly premiums deducted from their Social Security checks. Because the federal law “holds harmless” about 70 percent of Medicare recipients from premium increases to cover unexpected increases in healthcare costs, the remaining 30 percent of Medicare Part B beneficiaries suffer the consequences by being made to pay higher premiums.

Without intervention by Congress, roughly 15 million seniors and chronically ill people currently claiming both Medicare and Medicaid coverage would have seen their premiums increase from $104.90 per month to $159.30 for individuals, according to Medicare actuaries. The actuaries also predicted an increase in the annual deductible for Part B of Medicare, from $147 in 2015 to $223 next year.

Related: Social Security Ruling Drives Up Medicare Costs for Millions

Estimates of the cost of legislation to blunt or block a premium increase have ranged from $7.5 billion to $10 billion. Under the budget agreement unveiled late last night, that cost will be covered by a loan of general revenue from the U.S. Treasury to the Supplemental Medical Insurance Trust Fund.

In order to repay that loan, the 15 million people who are not subject to the “hold harmless” protection will be required to pay an additional $3 a month in premiums – a token amount — until the loan is repaid years from now, according to a House budget document describing the deal. Medicare beneficiaries who currently pay higher income-related premiums would pay more than $3, based on their income levels.

If there is no Social Security cost of living adjustment increase for 2017, this provision will apply again.