Op-ed by D. Kenton Henry Editor, Broker 26 November 2021

In September, I learned Aetna and Unitedhealthcare would be reentering the Texas ACA Underage 65 health insurance market for the first time since 2015. Since then, BlueCross BlueShield has been the only “household name,” a large, financially sound insurance company in the southeast Texas market. This was most welcome news, and I was hopeful these additional peer companies would allow my clients and fellow Texans access to more doctors and hospitals. Finding my client’s preferred doctors and hospitals in a plan network has been my client’s and my greatest challenge since the departure of all PPO network options six years ago. Alas, the hoped-for provider expansion in 2022, at this point, has failed to materialize. From 2015 into 2021, the St. Lukes Hospital system has been the only major hospital system participating in most insurance companies’ HMO networks. Such will remain the case for 2022.

Additionally, the entry of Bright Insurance Company (for the first time) doesn’t even appear to do that. They will limit their policyholder’s access to hospitals will be limited to smaller HCA local community hospitals. At least for the time being.

Doctors have practicing privileges at one or more hospitals. Of course, it follows that when an insurance company has fewer hospitals in their network, they will have fewer participating doctors. And so it seems. Only one health insurance company in the southeast Texas ACA health insurance market allows its clients access to the three major hospital systems in the area. Those hospitals are St. Luke’s, Memorial Hermann, and Houston Methodist. And then, only if you acquire their more expensive Silver or Gold plans.

However, there is a bit of good news for all Americans in the “Individual and Family” health insurance market. The federal government’s American Rescue Plan has increased the amount of Advance Premium Tax Credit (subsidy) and Cost Sharing Reduction (reduction of deductibles, copays, and coinsurance) available to a household. It also expanded the eligibility for these subsidies. As the feature article below explains, this will qualify more people for both types of savings.

Furthermore, unemployment effects and increases your potential premium tax credit! The American Rescue Plan exempts up to $10,200 in UI benefits from federal income tax. People who receive UI benefits in 2020 will be able to reduce their adjusted gross income by up to that amount, and so reduce their federal income tax liability.

Please get in touch with me to learn the details on the aforementioned company providing the greatest access to providers and how the expanded subsidies and Cost-Sharing Reductions may improve your health insurance situation.

If you choose to be proactive and would like to do some reconnaissance before calling me for assistance and details, you may click on my quoting link immediately following. When the page opens, ignore the login button. You need not log in. Enter your information. I.e., birth date, zip code, etc. On the next page, click on the top box “SELECT ALL” to clear the selections. Then select “MEDICAL” only, to get started. Otherwise, you will be overwhelmed with options and information. You can always return for dental, etc.)

Click “YES” if you would like to estimate whether you qualify for a subsidy. If so, enter your estimated annual income in 2022 and click “CALCULATE”. It will estimate your subsidy. The estimates are usually accurate to within $3.00. From there, click “NEXT”. You will then see all your plan options and be able to LOOKUP PROVIDERS and see plan details. Or simply call me to do all this for you!

CLICK HERE TO SEE ALL YOUR ACA HEALTH INSURANCE OPTIONS (IF NECESSARY, COPY THE LINK IN YOUR BROWSER AND HIT ENTER):

https://allplanhealthinsurance.insxcloud.com/

MEDICARE RECIPIENTS:

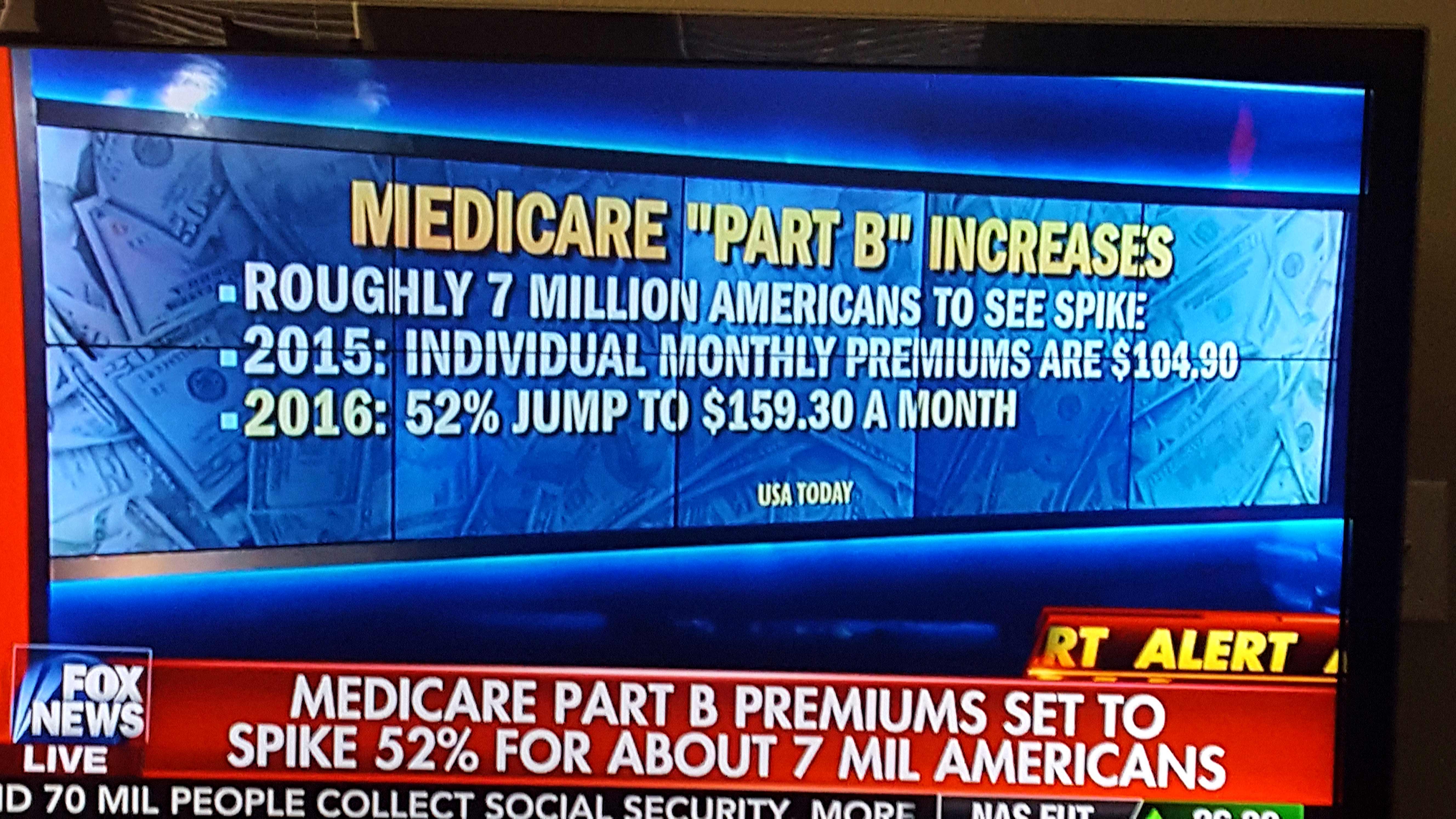

As the cost for everything, including medical treatment, is going up, so too are Medicare’s premiums and deductibles. As our second feature article below illustrates, the Medicare Part B (outpatient) basic premium is going from $148.50 to $170.10 and it’s calendar year deductible is going from $203.00 to $233.00! You can do the math, but, needless to say, so much for 5% inflation rate projected by the current administration which also does not appear to apply to our cost for gasoline, meat, and energy and food, in general! You’ve already spent the increase in your Social Security Benefit!

The details of how your Medicare Part B basic premium will may titrate upward relative to your income are clearly outlined in Feature Article 2, just published by the Centers For Medicare and Medicaid Services.

Lastly, if you are making the decision whether to go with a Medicare Advantage Prescription Drug Health Plan vs. a Medicare Supplement policy coupled with a Part D Prescription Drug Plan – please read Feature Article 3 (say it ain’t so, Joe!) below, and carefully weigh your decision.

Again, please contact me for guidance in how to minimize the impact of these changes and maximize your both your access to providers and quality health care. My 35 years specializing in the health and Medicare related insurance industry have provided me insights beyond that of the average agent/broker/generalist; and my clients access to a far greater number of products and solutions.

D. Kenton Henry TheWoodlandsTXHealthInsurance.com

Allplanhealthinsurance.com@gmail.com

Office: 281-367-6565

Text My Cell @ 713-907-7984

Https://TheWoodlandsTXHealthInsurance.com Https://Allplanhealthinsurance.com Https://HealthandMedicareInsurance.com

*********************************************************************************************************

FEATURE ARTICLE 1:

11.24.2021

Cost Sharing Reductions on Silver Plans

Two types of Marketplace subsidies:

Advanced Premium Tax Credits(APTC):Lowers the cost of premiums and can be used on any Marketplace plan except for catastrophic plans.

Cost Sharing Reductions(CSR):Lowers the cost of deductibles and can only be applied to Marketplace Silver plans.

This year, many people will qualify for both types of savings!

Why are subsidies more generous this year:

The American Rescue Plan Act increased the amount of APTC and CSR available to a household, and it also expanded the eligibility for these subsidies.

Silver plans vs. other metal levels:

All Marketplace health insurance plans are broken into five types: Platinum, Gold, Silver, Bronze and Catastrophic. You can expect the same level of care fromall metal levels. The difference is how your healthcare costs will be split between you and the insurance company. Metal levels Premium Platinum Highest Gold Silver Bronze Catastrophic Deductible Higher Middle Lower Lowest Lower Middle Higher Highest. If you are eligible for a CSR, you must choose a Silver plan!

*********************************************************************************************************

FEATURE ARTICLE 2:

Key Points:

Part B premium for 2022 is $170.10, up $21.60 from 2021.

The annual deductible for all Medicare Part B beneficiaries is $233 in 2022, an increase of $30 from the annual deductible of $203 in 2021.

Follow the link below for more information and the 2022 Medicare Part B Income-Related Monthly Adjustment Amounts

OR SIMPLY READ THE ARTICLE IMMEDIATELY BELOW

Centers for Medicare & Medicaid Services

Nov 12, 2021

Fact sheet

2022 Medicare Parts A & B Premiums and Deductibles/2022 Medicare Part D Income-Related Monthly Adjustment Amounts

Nov 12, 2021

Share

opens in new window opens in new window opens in new window

On November 12, 2021, the Centers for Medicare & Medicaid Services (CMS) released the 2022 premiums, deductibles, and coinsurance amounts for the Medicare Part A and Part B programs, and the 2022 Medicare Part D income-related monthly adjustment amounts.

Medicare Part B Premium and Deductible

Medicare Part B covers physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A.

Each year the Medicare Part B premium, deductible, and coinsurance rates are determined according to the Social Security Act. The standard monthly premium for Medicare Part B enrollees will be $170.10 for 2022, an increase of $21.60 from $148.50 in 2021. The annual deductible for all Medicare Part B beneficiaries is $233 in 2022, an increase of $30 from the annual deductible of $203 in 2021.

The increases in the 2022 Medicare Part B premium and deductible are due to:

- Rising prices and utilization across the health care system that drive higher premiums year-over-year alongside anticipated increases in the intensity of care provided.

- Congressional action to significantly lower the increase in the 2021 Medicare Part B premium, which resulted in the $3.00 per beneficiary per month increase in the Medicare Part B premium (that would have ended in 2021) being continued through 2025.

- Additional contingency reserves due to the uncertainty regarding the potential use of the Alzheimer’s drug, Aduhelm™, by people with Medicare. In July 2021, CMS began a National Coverage Determination analysis process to determine whether and how Medicare will cover Aduhelm™ and similar drugs used to treat Alzheimer’s disease. As that process is still underway, there is uncertainty regarding the coverage and use of such drugs by Medicare beneficiaries in 2022. While the outcome of the coverage determination is unknown, our projection in no way implies what the coverage determination will be, however, we must plan for the possibility of coverage for this high cost Alzheimer’s drug which could, if covered, result in significantly higher expenditures for the Medicare program.

Medicare Open Enrollment and Medicare Savings Programs

Medicare Open Enrollment for 2022 began on October 15, 2021, and ends on December 7, 2021. During this time, people eligible for Medicare can compare 2022 coverage options between Original Medicare, and Medicare Advantage, and Part D prescription drug plans. In addition to the recently released premiums and cost sharing information for 2022 Medicare Advantage and Part D plans, the Fee-for-Service Medicare premiums and cost sharing information released today will enable people with Medicare to understand all their Medicare coverage options for the year ahead. Medicare health and drug plan costs and covered benefits can change from year to year, so people with Medicare should look at their coverage choices annually and decide on the options that best meet their health needs.

To help with their Medicare costs, low-income seniors and adults with disabilities may qualify to receive financial assistance from the Medicare Savings Programs (MSPs). The MSPs help millions of Americans access high-quality health care at a reduced cost, yet only about half of eligible people are enrolled. The MSPs help pay Medicare premiums and may also pay Medicare deductibles, coinsurance, and copayments for those who meet the conditions of eligibility. Enrolling in an MSP offers relief from these Medicare costs, allowing people to spend that money on other vital needs, including food, housing, or transportation. People with Medicare interested in learning more can visit: https://www.medicare.gov/your-medicare-costs/get-help-paying-costs/medicare-savings-programs.

Medicare Part B Income-Related Monthly Adjustment Amounts

Since 2007, a beneficiary’s Part B monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 7 percent of people with Medicare Part B. The 2022 Part B total premiums for high-income beneficiaries are shown in the following table:

| Beneficiaries who file individual tax returns with modified adjusted gross income: | Beneficiaries who file joint tax returns with modified adjusted gross income: | Income-related monthly adjustment amount | Total monthly premium amount |

| Less than or equal to $91,000 | Less than or equal to $182,000 | $0.00 | $170.10 |

| Greater than $91,000 and less than or equal to $114,000 | Greater than $182,000 and less than or equal to $228,000 | 68.00 | 238.10 |

| Greater than $114,000 and less than or equal to $142,000 | Greater than $228,000 and less than or equal to $284,000 | 170.10 | 340.20 |

| Greater than $142,000 and less than or equal to $170,000 | Greater than $284,000 and less than or equal to $340,000 | 272.20 | 442.30 |

| Greater than $170,000 and less than $500,000 | Greater than $340,000 and less than $750,000 | 374.20 | 544.30 |

| Greater than or equal to $500,000 | Greater than or equal to $750,000 | 408.20 | 578.30 |

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

| Beneficiaries who are married and lived with their spouses at any time during the year, but who file separate tax returns from their spouses, with modified adjusted gross income: | Income-related monthly adjustment amount | Total monthly premium amount |

| Less than or equal to $91,000 | $0.00 | $170.10 |

| Greater than $91,000 and less than $409,000 | 374.20 | 544.30 |

| Greater than or equal to $409,000 | 408.20 | 578.30 |

Medicare Part A Premium and Deductible

Medicare Part A covers inpatient hospital, skilled nursing facility, hospice, inpatient rehabilitation, and some home health care services. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

The Medicare Part A inpatient hospital deductible that beneficiaries pay if admitted to the hospital will be $1,556 in 2022, an increase of $72 from $1,484 in 2021. The Part A inpatient hospital deductible covers beneficiaries’ share of costs for the first 60 days of Medicare-covered inpatient hospital care in a benefit period. In 2022, beneficiaries must pay a coinsurance amount of $389 per day for the 61st through 90th day of a hospitalization ($371 in 2021) in a benefit period and $778 per day for lifetime reserve days ($742 in 2021). For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $194.50 in 2022 ($185.50 in 2021).

| Part A Deductible and Coinsurance Amounts for Calendar Years 2021 and 2022 by Type of Cost Sharing | ||

| 2021 | 2022 | |

| Inpatient hospital deductible | $1,484 | $1,556 |

| Daily coinsurance for 61st-90th Day | $371 | $389 |

| Daily coinsurance for lifetime reserve days | $742 | $778 |

| Skilled Nursing Facility coinsurance | $185.50 | $194.50 |

Enrollees age 65 and over who have fewer than 40 quarters of coverage and certain persons with disabilities pay a monthly premium in order to voluntarily enroll in Medicare Part A. Individuals who had at least 30 quarters of coverage or were married to someone with at least 30 quarters of coverage may buy into Part A at a reduced monthly premium rate, which will be $274 in 2022, a $15 increase from 2021. Certain uninsured aged individuals who have less than 30 quarters of coverage and certain individuals with disabilities who have exhausted other entitlement will pay the full premium, which will be $499 a month in 2022, a $28 increase from 2021.

For more information on the 2022 Medicare Parts A and B premiums and deductibles (CMS-8077-N, CMS-8078-N, CMS-8079-N), please visit https://www.federalregister.gov/public-inspection.

Medicare Part D Income-Related Monthly Adjustment Amounts

Since 2011, a beneficiary’s Part D monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 8 percent of people with Medicare Part D. These individuals will pay the income-related monthly adjustment amount in addition to their Part D premium. Part D premiums vary from plan to plan and roughly two-thirds are paid directly to the plan, with the remaining deducted from Social Security benefit checks. The Part D income-related monthly adjustment amounts are all deducted from Social Security benefit checks. The 2022 Part D income-related monthly adjustment amounts for high-income beneficiaries are shown in the following table:

| Beneficiaries who file individual tax returns with modified adjusted gross income: | Beneficiaries who file joint tax returns with modified adjusted gross income: | Income-related monthly adjustment amount |

| Less than or equal to $91,000 | Less than or equal to $182,000 | $0.00 |

| Greater than $91,000 and less than or equal to $114,000 | Greater than $182,000 and less than or equal to $228,000 | 12.40 |

| Greater than $114,000 and less than or equal to $142,000 | Greater than $228,000 and less than or equal to $284,000 | 32.10 |

| Greater than $142,000 and less than or equal to $170,000 | Greater than $284,000 and less than or equal to $340,000 | 51.70 |

| Greater than $170,000 and less than $500,000 | Greater than $340,000 and less than $750,000 | 71.30 |

| Greater than or equal to $500,000 | Greater than or equal to $750,000 | 77.90 |

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

| Beneficiaries who are married and lived with their spouses at any time during the year, but file separate tax returns from their spouses, with modified adjusted gross income: | Income-related monthly adjustment amount |

| Less than or equal to $91,000 | $0.00 |

| Greater than $91,000 and less than $409,000 | 71.30 |

| Greater than or equal to $409,000 | 77.90 |

Related Releases

Oct 21, 2021

Oct 15, 2021

Oct 15, 2021

Oct 08, 2021

Sep 30, 2021

Contact us

CMS News and Media Group

Catherine Howden, Director

Jason Tross, Deputy Director

Media Inquiries Form

202-690-6145

*********************************************************************************************************

FEATURE ARTICLE 3:

11.08.2021

Medicare plans: Be wary of Joe Namath, other celebrity pitchmen | Steve Israel

Steve Israel for the Times Herald-Record

Mon, November 8, 2021, 7:24 AM·3 min read

In this article:

American football player

Explore the topics mentioned in this article

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

He’s one of a slew of pitchmen and women selling Medicare Advantage plans to the more than 54 million Americans 65 or over eligible for Medicare. That includes more than 100,000 of us in Orange, Ulster and Sullivan counties.

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

Those pitches, which also flood our mailboxes during this enrollment period that ends Dec. 7, complicate what can be a mind-boggling array of insurance choices.

First, some basic facts:

Medicare Advantage is the all-in-one alternative to original Medicare health insurance. Original Medicare includes coverage for hospitalization (Part A), medical visits and procedures (Part B) and, at additional cost, prescription drugs (Part D). Before you enroll in Advantage plans, you must have original Medicare, and you still must pay the Part B premium of $148.50 (in 2021). While Medicare Advantage plans include medical, hospital and drug coverage, they can also feature extra benefits not offered by traditional Medicare, such as dental, hearing and vision coverage with no additional premium.

Especially in those pitches from celebrities like Namath, William Shatner and Jimmie Walker, they can also promise everything from free meal delivery to money deposited in your Social Security account.

But …

“Buyer beware,” says Erinn Braun, Orange County Office for the Aging’s Health Insurance Counseling and Assistance Program coordinator. She provided much information for this column.

Pitches like Namath’s can be misleading or downright deceptive, starting with the red, white and blue colors that insinuate the ads are from the government, as do the state logos on some mailers. While the plans themselves are perfectly legal and may be great for many of the 27 million Americans enrolled in them, they often don’t deliver everything those pitches seem to promise. Plus, those pitches don’t come close to telling the full story of the benefits of those plans – many of which aren’t even offered in your area.

For instance:

Unlike original Medicare, which is accepted by virtually all doctors and hospitals, Medicare Advantage plans include a network of doctors and hospitals you must visit to be insured. So if you hear about a great gastroenterologist in New York City and she isn’t in your Advantage plan’s network, your insurance may not cover your visit. Plus, unlike original Medicare, you may need prior approval for coverage of a medical procedure or equipment such as insulin pumps.

And while the dental and vision coverage of Medicare Advantage plans sounds great, some plans in your area may only include routine visits, not more expensive items like dental implants and eyeglasses. Plus, the average yearly coverage limit of Advantage dental plans ranges from about $1,000 to $1,300, according to the Kaiser Family Foundation. The dentists and eye doctors you visit must also be in the plan’s networks – meaning your eye doctor or dentist may not accept your plan.

Steve Israel

As for those meals and money Joe Willie is pitching?

Again, buyer beware.

A few Advantage plans may offer meal delivery for the qualified but only one or two plans in your county may offer those benefits. And your doctors or hospital may not accept those plans. Same thing goes for that money Namath says could go into your Social Security account. Not only does that money go toward the required payment for Part B of original Medicare, very few plans – if any – in your area may feature that benefit, and those plans may not include your doctors.

Finally, when you call the number provided by Namath and other pitch folks, you’ll reach a salesperson who’s in business to … you guessed it … sell you a Medicare Advantage plan.

For help selecting the right Medicare plan for you, contact your county’s Office of the Aging. Orange: 845-615-3710, Sullivan: 845-807-0241, Ulster: 845-340-3456. A trusted health insurance agent can also help. Medicare.gov and 1-800-Medicare provide a wealth of information.

steveisrael53@outlook.com

This article originally appeared on Times Herald-Record: Medicare pitches: Joe Namath, other celebrities don’t have best advice