By D. Kenton Henry, Editor / Agent / Broker — TheWoodlandsTXHealthInsurance.com, AllPlanHealthInsurance.com, HealthandMedicareInsurance.com 30 October 2025

Each November in Texas marks more than just the start of the new health insurance year—it’s your gateway to securing coverage for the year ahead. This time around, the 2026 individual and family health insurance market is undergoing noticeable changes. Here’s what you need to know—and how you can be ready.

1. Why 2026 matters

Open enrollment for 2026 policies begins November 1, 2025, and runs until January 15, 2026 for most Texas consumers. If you don’t act in this window, you could be locked out of making changes until next year unless a qualifying life event occurs. Given major shifts among carriers and plan options, early action is more important than ever.

2. Carrier changes you should track

One of the major headlines: Aetna will exit the Texas individual and family market beginning in 2026. That means if you currently have an Aetna plan, your policy will not renew for 2026. You’ll need to select a different carrier in the upcoming enrollment period.

Other carriers are repositioning their offerings, adjusting networks, benefits, and rates. Even if your carrier is staying, plan names and design may change. As your broker, I’ll review all available options from multiple carriers and ensure you’re not simply renewing by default.

3. What this means for you

No automatic renewal: If your carrier exits the market, your current plan will not carry over. You’ll receive a Notice of Change—or termination—and need to select a new plan.

Shop your options: Differences between plans are not only about monthly premiums. Review networks, cost-sharing, deductibles, out-of-pocket maximums, and whether benefits match your healthcare needs.

Subsidy changes: The federal subsidy rules continue to evolve. Even small changes in income, household, or eligibility can shift your subsidy level. I’ll help you analyse eligibility for Advance Premium Tax Credits (APTC) and other cost-saving tools.

Timing matters: Beginning November 1, I’ll be available to assist you through the selection process—not just on carriers and plans, but on ensuring accurate enrollment to avoid coverage gaps.

4. Why working with a broker matters

As an independent broker specializing in medical insurance since 1986, I work with virtually every major carrier licensed in Texas. My services to you are free of charge. My goal is to ensure you get the best plan that fits your health needs, budget, and preferences—especially in a year of significant market change. Rather than navigating dozens of plan names on your own, let me do the heavy lifting and help you make an informed choice.

5. What to do now

Gather your information – your current health plan, recent premium receipts, summary of benefits, and any health changes.

Schedule your review – open enrollment kicks off November 1. If you’d like early preparation, I’m available now to pre-review your situation so you’re ready to act.

Act during the window – November 1 through January 15 is your open period. Plans go into effect January 1, 2026, or, depending on carrier rules, as early as December 1, 2025.

Don’t wait – with carrier exits and plan redesigns in motion, the sooner you start the review, the better your chance of finding the optimal match.

Working together, we’ll turn these market shifts into an advantage—so instead of scrambling when notices arrive, you’ll move confidently into 2026 with coverage aligned to your needs.Let me handle the complexity so you can focus on your life, your health, and your goals.

If it’s after hours, or you simply prefer, you can do preliminary research before calling me by obtaining quotes from my quoting engine. You do NOT have to log in to obtain them but be certain to call me afterwards with questions, and assistance in finding your providers within the networks, as well as applying. CLICK HERE: https://allplaninsurance.insxcloud.com/get-a-quote

D. Kenton Henry Editor · Agent · Broker TheWoodlandsTXHealthInsurance.com * AllPlanHealthInsurance.com * HealthandMedicareInsurance.com

Ever since the passage of the Patient Protection and Affordable Care Act (ACA), commonly referred to as “Obamacare”, in 2010, the Department of Health and Human Services has dictated when and under what circumstances an individual and family can apply for and obtain health insurance. This period is known as the Open Enrollment Period, and it is upon us. Each year, between November 1st and December 15th, U.S. citizens and their families may apply for and obtain health insurance effective January 1st of the coming calendar year. From then until January 15th, they may apply for coverage effective February 1st. Beyond that date, they are locked out of any health insurance plan they were not enrolled in when the year ended. Only special circumstances such as losing “creditable” coverage through no fault of their own, moving out of a plan’s area, birth of a child, or death of a covered family member allow them to apply for coverage beyond the Open Enrollment Period. And only if they were insured when the special circumstance occurred and no more than 60 days have passed. Creditable coverage meets all the mandates of the Affordable Care Act, such as guaranteed coverage for pre-existing health conditions, including pregnancy and mental health disorders, along with no out-of-pocket for preventative medicine. All coverage is guaranteed so long as the above requirements are met.

If affordability of health insurance is an issue, Premium Tax Credits (subsidies) are available from the Department of Health and Human Services (DHS) to people or families whose income falls below a certain threshold.

WHO IS ELIGIBLE FOR THE PREMIUM TAX CREDIT?

To receive the premium tax credit for coverage starting in 2024, a Marketplace enrollee must meet the following criteria:

· Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2024 benefit year will be determined based on 2023 poverty guidelines

· Can not have access to affordable coverage through an employer (including a family member’s employer)

· Can not be eligible for coverage through Medicare, Medicaid, the Children’s Health Insurance Program (CHIP)

· Have U.S. citizenship or proof of legal residency (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements)

· If married, must file taxes jointly

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Your tax credit is based on the household income estimate you put on your Marketplace application.

Income between 100% and 400% FPL: If your income is in this range (in all states) you qualify for premium tax credits that lower your monthly premium for a Marketplace health insurance plan. The lower your income is as a percent of the FPL—the higher your subsidy.

The easiest way to determine whether and for how much you qualify is to call me. You will estimate your 2024 household’s adjusted gross income and my subsidy calculator will tell us (based on the number of people in your household) how much your subsidy will be. If we give the DHS the same information you give me, my calculations are usually accurate to within $3.00 of what you will actually receive. We then apply that subsidy against the premium of the plan you wish to acquire and arrive at your net premium.

The number of people who qualify for subsidies continues to grow. For details on this, please refer to this chart and my feature article 2 below.

As to how much retail (gross) premiums are expected to grow from 2023 to 2024, estimates put the national average at 6%. (For the details on this, please refer to Feature Article 1 below.) Given the rate of core and real inflation, this should not come as a surprise. Acquisition of a subsidy will certainly offset ever-increasing premiums.

As always, the greatest challenge to the consumer and their agent/broker is affordability or obtaining the desired benefits. Instead, it is finding their doctors in the networks of a health plan. In 2024, as it was this year, there will be over 100 different plans available from six to eight different companies, depending on where one resides. Dealing with this myriad of options is where my three decades specializing in health insurance in the Houston area is invaluable. I know which hospitals are in which plan networks, and my provider search tools scan all plans without you having to go from company to company for results. Because I represent every company doing business in Texas, you can acquire information on all of them with one call to me.

Again, Open Enrollment begins November 1st, and for coverage during the entirety of 2024, it ends December 15th. Unlike going to the marketplace (Healthcare.gov) you will get me each time you call my local office with questions and for assistance and service–as opposed to an 800 number where you will get a different individual each time you call. My service is much more personalized and detailed than that of an hourly worker at the end of that toll-free number. If I don’t provide you with the level of service you deserve, I don’t have a client. And if I don’t have a client, I don’t earn a living. And it costs you no more to go through me than directly to the company whose policy you ultimately acquire.

I look forward to working with you and providing the best of service. Please call me.

D. Kenton Henry

Office: 281-367-6565 Text me 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

This analysis of insurers’ preliminary rate filings shows that ACA Marketplace insurers are requesting a median premium increase of 6% for 2024. Insurers cite price increases for medical care and prescription drugs as a key driver of premium growth in 2024, In addition to inflation’s impact on medical costs, insurers point to growth in the utilization of health care, which fell in 2020 but has since returned to more normal levels.

Insurers’ proposed rate changes – most of which fall between 2% and 10% – may change during the review process. Although most Marketplace enrollees receive subsidies and are not expected to face these added costs, premium increases could result in higher federal spending on subsidies.

The analysis can be found on the Peterson-KFF Health System Tracker, an information hub dedicated to monitoring and assessing the performance of the U.S. health system.

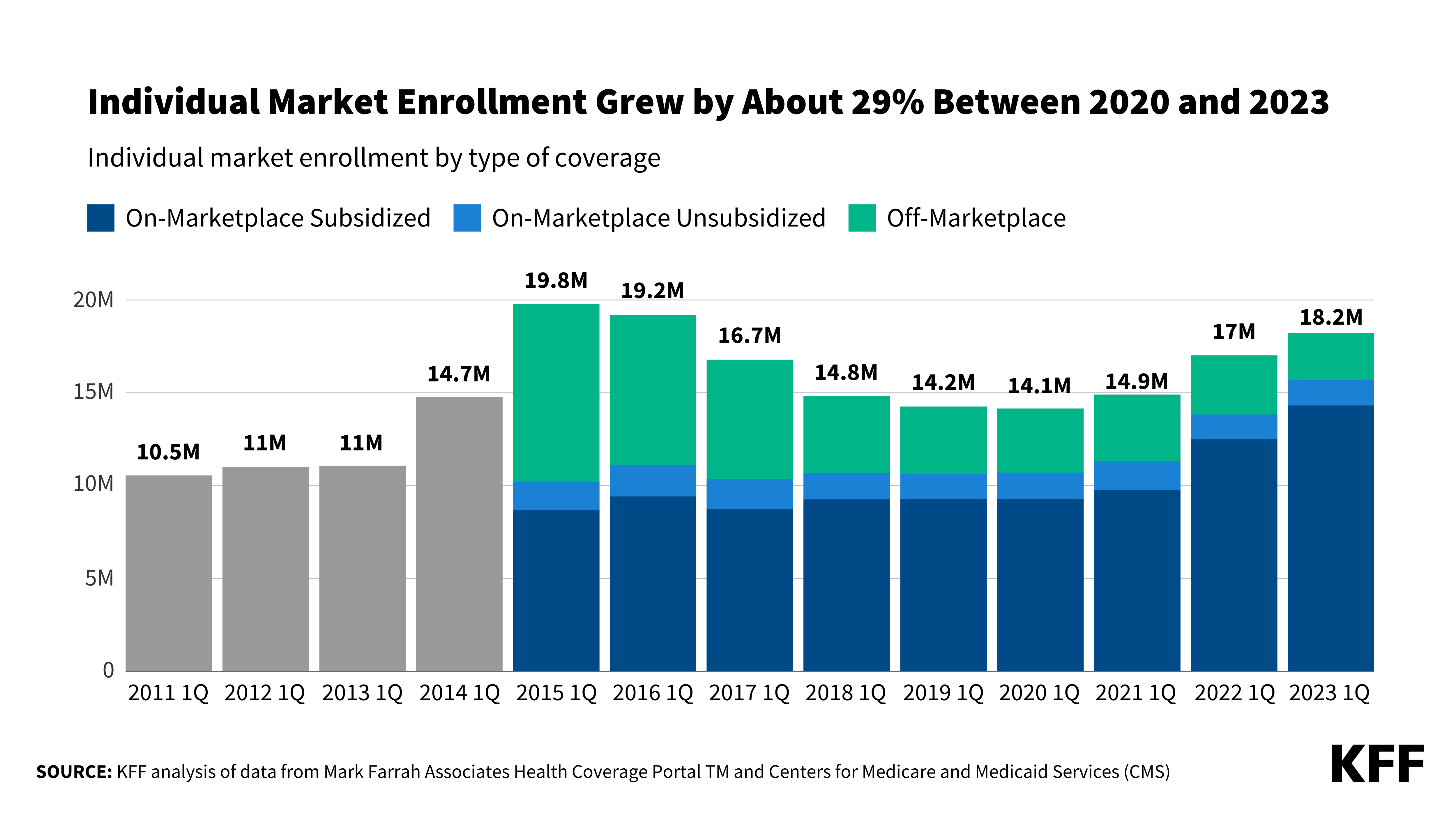

Enhanced Marketplace subsidies have continued to drive up enrollment in the individual market, and the loss of Medicaid coverage by millions of people could contribute to this trend, according to a new KFF analysis. Meanwhile, enrollment in non-ACA-compliant plans is at a record low.

As of early 2023, an estimated 18.2 million people have individual market coverage, the highest since 2016. Individual market enrollment grew by about 29% between early 2020 and early 2023 — a result of enhanced subsidies introduced by the Inflation Reduction Act, increased outreach, and an extended enrollment period.

This enrollment growth could continue in 2023 as states resume Medicaid disenrollments amid the unwinding of the continuous enrollment provision. Some of the people losing Medicaid coverage may be eligible for subsidies on the ACA Marketplaces.

Due in part to the enhanced subsidies, about 4 in 5 individual market enrollees have subsidized coverage — the highest share since the ACA was implemented.

The number of people in non-compliant plans has fallen each year and could decrease further due to the Biden Administration’s proposed rule that would reverse the expansion of short-term plans. An estimated 1.2 million people were in non-ACA-compliant plans in mid-2022, compared to 5.7 million in mid-2015. These short-term plans often do not include certain benefits or coverage for pre-existing conditions and can impose a dollar limit on insurance coverage.

If unsubsidized premiums rise in 2024 due to higher health care prices and utilization, enhanced subsidies could shield most individual market enrollees from increases in their monthly payments.

(AETNA AND UNITEDHEALTHCARE RE-ENTER THE ACA INDIVIDUAL AND FAMILY HEALTH INSURANCE MARKET)

By Editor, Agent, Broker

D. Kenton Henry

It is that time of year and, once more, we find ourselves on the cusp of the “Annual Election Period” for Medicare Advantage and Part D Prescription Drug Plans. This is the period when any Medicare recipient may enroll or change their Advantage and / or drug plans for a January 1 effective date. The period runs from October 15th through December 7th.

As if this was not a busy enough time for Medicare insurance product brokers, many of us (like myself) must do “double duty”, during the holidays. This is because the “Open Enrollment Period” for those “Under the Age Of 65“, in need of Individual and Family health insurance, begins November 1 and runs through January 15th. This a one month extension from previous years. However, those wishing to have new coverage effective by January 1 must still enroll by December 15th.

In addition to the extension of the ACA enrollment period, an interesting and positive turn is that Aetna and Unitedhealthcare are re-entering the marketplace in SE Texas for 2022 after a six year hiatus! This brings welcome competition to a market which was vacated by every major carrier – other than BlueCross BlueShield – in January of 2016. While we will not have insight into the details of their health plan options until just before November 1, their names and reputation should garner a lot of attention, not only from consumers but medical providers. It is my hope that more high quality doctors and hospitals will elect to participate in the insurance companies’ provider networks. With Preferred Provider Organization (PPO) network plans eliminated, Health Maintenance Organization (HMO) network plans have been the consumer’s only option since 2016. And with the expansion in the availability of the Advance Premium Tax Credit and Cost Share Reductions, for many, their greatest challenge is no longer being able to afford health insurance but finding their providers in an insurance plan’s network.

And it is the same for me. As an agent / broker with 34 years in medical insurance, my greatest challenge isn’t finding a plan the consumer can afford or the benefits they’re seeking. It’s finding my client’s, and prospective client’s, medical providers participating in a network. While this isn’t a major issue to those new to the area, those of us who have resided here for years, have long established relationships with providers we are reluctant to part with.

I would be extremely pleased if some of the companies in the marketplace elect to offer PPO plans in 2022. But make no mistake, I in no way expect this to happen. The problem for a company considering offering PPO coverage is that if all their peers do not also, they “adversely select” against themselves. In other words, if they are the “only game in town” when it comes to PPO plans, they are going to attract, and garner, an inordinate number of “bad risks”. In other words, insured members with serious pre-existing conditions who need access to a greater number of providers will flock to them vs the insurance company offering access to an HMO network only. They will submit higher and more frequent claims, thereby compounding the potential for “loss” to the insurance company. This is why insurance companies ceased, in unison, offering PPO coverage, in most regions of the United States, in 2016. They want to limit your access to providers, and thereby limit your access to what is likely to be more expensive treatment. Enrolling people in HMO plans is the easiest way to do this. Regardless, my duty, as your agent, is to do my best to find your providers participating in the network of a plan whose benefits meet your needs.

The good news is – two new major carriers will uncertainly increase the number of options available to the consumer in terms of premiums, benefits, and providers. Additionally, several of the insurance companies are lowering copays and deductibles and the Department of Health and Human Services, which oversees the sale of all ACA health insurance, has made it much easier to qualify for a “subsidy” to reduce the policyholder’s share of the premium due, especially for anyone who claimed unemployment benefits any time during 2021.

In the Medicare related insurance market, increases in variables for 2022 are estimated to be higher than in recent years. Some were not definite as of the end of September. The Part A In-patient deductible is projected to increase but, as of this date, I have no definitive cost. The Part B Out-patient deductible is estimated to be going from $203 to $217 per calendar year and it’s premium is projected to go from $148.50 to $158.50 per month.

There are currently 30 different Part D Drug plans for Texans to choose from. Each covers some drugs but not others. The plan which is best for you is entirely dependent on the drugs you use. Not the drugs your spouse, neighbor, or I use – but the ones you use. The Part D deductible is going from $445 to $480 for the calendar year. A drug plan may choose to have deductible ranging from $0 all the way to$480 before your drugs become available for a copay. With many plans, the deductible will not apply to Tier 1 and Tier 2 generic drugs. The threshold for entering the “GAP” will occur when the member and plan have paid $4,430. During this time, the member will pay 25% of the cost of their drugs. They will cross over into “CATASTROPHIC COVERAGE” if, and when, the member has personally expended $7,050. At this point, a member will pay $3.95 for a generic drug and $9.85 or 5% of the cost of a brand name drug – whichever is higher.

As a broker for my clients, and prospective clients, my goal is to identify the Medicare Plan, whether Medicare Supplement, Advantage or Part D Drug Plan which is most likely to result in their lowest total out of pocket cost for the calendar year while providing them access to all their providers. The “total cost” is the sum of their premium, any applicable deductible or deductibles, and copays or coinsurance. Our objective is the lowest sum and that plan, or plans, will usually be my recommendation.

To this end, I encourage anyone interested in enlisting my help, to contact me. If you would like me to identify your lowest total cost drug plan for 2022, based on your current or anticipated drug use, email me a list of your Rx drugs and, preferably, the dosages. The latter can make a difference. If you know you want Medicare Advantage, send me a list of doctors and hospitals you feel you must have access to. Please recall that with Medicare Supplement coverage you may obtain treatment from any doctor, hospital, lab, or medical provider, that sees Medicare patients. There are no networks with which to concern yourself. However, with Supplement, unlike most Medicare Advantage plans, you will have to acquire a Part D Prescription Drug Plan to accompany it. For those using little or only low cost generic drugs, the lowest premium plan for Texans in 2022 will be $6.90 per month.

*(READ FEATURED ARTICLE BELOW ON WASHINGTON’S EFFORTS TO LOWER RX DRUG COST FOR MEDICARE RECIPIENTS)

The name of my insurance agency I opened in 1991, after being in the medical and life insurance industry since 1986, is All Plan Med Quote. It is located in The Woodlands, Texas. In 1995, I created one of the first websites in the country to market health insurance via the internet. It still exists as Allplanhealthinsurance.com. In 2015, I expanded my web presence with TheWoodlandsTXHealthInsurance.com. The primary objective in naming the first two was to convey that (while I work, for the consumer) I am appointed (contracted) with virtually every “A” rated, major and minor insurance company doing business in your geographic region. But the insurance companies do not pay me a guaranteed wage or salary. They compensate me fairly if, and only if, you elect to go through me to acquire their products. But, without my clients, I have no income. So certainly my clients are my priority. Not the insurance companies. And, as my client, you are charged no more by going through me to obtain their product then if you walked through their front door and acquired it directly from them.

Here is a partial list of the companies whose products may, or may not, be appropriate for you, I may introduce to you:

AARP Unitedhealthcare

Aetna

Ambetter

Anthem

BlueCross BlueShield of Texas

Caresource

Cigna

Community Health Choice

Friday

Humana

KelseyCare Advantage

Molina

Mutual of Omaha

Oscar

Scott and White

Unitedhealthcare

Wellcare

D. Kenton Henry Office: 281-367-6565 Text my cell 24/7: 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

Democrats’ signature legislation to lower drug prices was defeated in a House committee on Wednesday as three moderate Democrats voted against their party.

Reps. Kurt Schrader (D-Ore.), Scott Peters (D-Calif.), and Kathleen Rice (D-N.Y.) voted against the measure to allow the secretary of Health and Human Services to negotiate lower drug prices, a long-held goal of Democrats.

The vote is a striking setback for Democrats’ $3.5 trillion package. Drug pricing is intended to be a key way to pay for the package. Leadership can still add a version of the provision back later in the process, but the move shows the depth of some moderate concerns.

The three moderates said they worried the measure would harm innovation from drug companies and pushed a scaled-back rival measure. The pharmaceutical industry has also attacked Democratic leaders’ measure, known as H.R. 3, as harming innovation.

The three lawmakers had long signaled their concerns with the drug pricing measure, but actually voting it down in the House Energy and Commerce Committee is an escalation.

A separate committee, the House Ways and Means Committee, did advance the drug pricing measures on Wednesday, keeping the provisions in play for later in the process.

Energy and Commerce Committee Chairman Frank Pallone Jr. (D-N.J.) had implored the three lawmakers to vote in favor of the measure to at least keep the process going.

“Vote to move forward today,” he said to the moderates in his party. “Vote to continue the conversation.”

Still, Pallone said he is confident that some form of measure to lower drug prices will make it into the final package. The House legislation was already expected to change before the final version, given moderate Democratic concerns in the Senate as well. Senate Democrats are working on their own bill, which is not yet finalized but is expected to be less far-reaching.

“I know it is going to have drug pricing reform,” Pallone said of the final bill, noting that negotiations with the Senate would continue over the coming weeks.

Still, the move on Wednesday is a show of force from the moderates.

Henry Connelly, a spokesman for Speaker Nancy Pelosi (D-Calif.), said Democrats were not giving up on including drug pricing measures.

“Polling consistently shows immense bipartisan support for Democrats’ drug price negotiation legislation, including overwhelming majorities of Republicans and independents who are fed up with Big Pharma charging Americans so much more than they charge for the same medicines overseas,” he said in a statement after the vote. “Delivering lower drug costs is a top priority of the American people and will remain a cornerstone of the Build Back Better Act as work continues between the House, Senate and White House on the final bill.”

Peters and Schrader both cited concerns about harming drug companies’ ability to develop new drugs, citing the industry’s record during the COVID-19 crisis.

Peters warned that “government-dictated prices” under the bill would cause harm to the “private investment” that backs drug development.

Schrader said the bill would mean “killing jobs and innovation that drives cures for these rare diseases.”

Advocates said the lawmakers were simply beholden to the pharmaceutical industry.

“Reps. Peters, Rice, and Schrader are prioritizing drug company profits over lower drug prices for the American people, particularly for patients with chronic conditions such as diabetes and multiple sclerosis,” said Patrick Gaspard, president of the left-leaning Center for American Progress. “To the contrary of what they contend, their opposition to the drugs proposal threatens the entirety of President Joe Biden’s Build Back Better agenda, which Democrats have campaigned on for years and that they previously voted for.”

Savings from the drug pricing provisions are a key way of paying for other health care priorities in the $3.5 trillion package, including expanding Medicaid in the 12 GOP-led states that have so far refused, expanding financial assistance under ObamaCare, and adding dental, vision, and hearing benefits to Medicare.

The Congressional Budget Office found that H.R. 3 would save about $500 billion over 10 years. Depending on what Senate Democrats can find agreement on, the final drug pricing legislation is expected to be less far-reaching, meaning it will result in fewer savings, though how much less is unclear.

The Senate bill would still allow Medicare to negotiate lower drug prices, but it is expected not to include another provision that would cap drug prices based on the lower prices paid in other wealthy countries. That provision has drawn particular pushback from some moderate Democrats.

Allowing Medicare to negotiate drug prices is extremely popular with voters, with almost 90 percent support in a Kaiser Family Foundation poll earlier this year. Many vulnerable House Democrats support the idea.

“Is dental insurance really worth the premium I pay?” is one question I am asked frequently. It is often followed, almost instantly, by―”Or am I simply paying for my dental work on a time a payment plan?”

My answer to both questions is a definitive, “Maybe.”

If you, as the majority do, have dental insurance through your employer, that employer is subsidizing all or part of your premium. This convenience makes for a solution to the equation, more favorable to you. In contrast―if you are self-employed, retired, or otherwise personally have to pay the full amount of a dental insurance premium―the opposite may be true. That is unless you take some straightforward advice, I am about to provide. If you do not, you most likely will only be spreading your cost for dental work over time. Even worse, dental insurance could prove to be a “loss item” in that you will have paid more in premiums than you will ever receive in benefits.

Short of taking a long drive and crossing the Rio Grande into Mexico to obtain your dental work, what can you do to offset the cost of say, a dental implant, which, on this side of the border, is going to run from $3,500 to $7,000?

Let me preface this by with a premise or three:

#1) With no insurance company is “the sky the limit”. I’m referring to the fee they are going to pay a dentist for a particular dental procedure. For example, no insurance company is going to accept a fee of $10,000 for a single porcelain crown. Not even their share of that cost, which is typically 50%. So what is the limit of a fee the insurance company will cover? That limit must be contractually defined, and the limit most insurance companies abide by is, “reasonable and customary” or “reasonable, usual, and customary”. These are empirical standards an insurance company uses to determine whether to pay a fee. Or how much of a fee to pay. If the dentist charges the general prevailing rate in your geographical area, they are going to pay the portion for which they are contractually obligated. Basically, it’s the average charged in your neighborhood. You will be charged more in Beverly Hills, California and less in Brenham, Texas “where the cows think it’s heaven”. Additionally, if “usual” is part of the definition, the fee has to be in line with what this particular dentist charges for a particular procedure. If fee is disproportionate either, or, both, ways―the maximum amount paid by the insurance company will be the limit set in their fee schedule.

#2) A dental insurance plan is either a provider network plan or a non-network plan. If it is a network plan, it is usually either a Dental Preferred Provider Organization (DPPO) Plan or a Dental Health Maintenance Organization (DHMO) Plan. If it is the first, you may go outside the network of dentists with which the insurance company has contracted but will most likely pay a higher cost for doing so. With the latter, you must remain within the network of dentists or, you have no insurance coverage whatsoever. For either of these options, you pay a lower premium than if you purchase a non-network or “any dentist” plan. The reason is that you agree to utilize or, at least, consider utilizing a dentist with whom the insurance company has contracted to charge you a lower fee than they would without the contract. This limits the insurance companies losses and brings increased traffic to the dentist.

#3) This is perhaps the most important part. If you purchase a non-network dental insurance plan, you can, almost, be assured you will be charged more than the insurance company deems acceptable. Additionally, you will be responsible for any dollar amount above their “reasonable and customary” rate. However, if you purchase a network plan, and go within the network of dentists, you will not be held responsible for any “excess” charges. Any charges above the reasonable and customary rate, the dentist will be forced to “write off”. In this situation, you will never have to worry about a surprise bill or claim. If a policy says your share of the bill is 20% or 50%, it will be that and not 20% or 50% plus any excess charges.

Assuming you accept you must acquire a network plan, in order to limit you own losses and surprise dental bills, the challenge becomes, “How do you find a quality dentist willing to accept a lower fee for treating you?” The typical HMO dental provider is typically someone straight out of dental school or who otherwise needs to build their patient base. In return for sending patients their way, the dentist is willing to accept a meaningfully lower fee. If the dentist is a PPO provider, they may have been in business longer, have more experience, and perhaps a reputation for having better skills. But they are willing to accept a somewhat lower fee in return from the many employees a large company may send their way. The dentist who isn’t willing to participate in any network apparently feels they have all the clients they need. That or their reputation is so great it will draw all the traffic they require.

The problem is, unlike a large oil company, as an individual, or family, you don’t bring enough “volume” to the table to bargain for a lower dental fee. At least not by yourself. Therefore, you have to identify and purchase your dental insurance from an insurance company which has the reputation of insuring a large number of employees of that oil company. As well as having a reputation for paying their claims in a timely and efficient manner. A manner such that the dentist wants to be contracted with them. From your standpoint, you want that insurance company to have a reputation for the same when it comes to you and not have to worry about claim disputes.

Another challenge is, at $6,000 for a dental implant, your dental benefit may not go too far. Secondly, does your insurance plan cover implants in the first place? Again, the sky is not the limit. The average dental plan covers a maximum of $1,000 of dental treatment per year. You can pay a higher premium for incremental benefits up to a maximum of $5,000. But a policy which pays that much in year one would cost a fortune and there is typically a twelve-month wait for major dental work to be covered. As such, you may want to find a plan which increases to that limit with each passing year and is available at what you consider a reasonable cost.

How do you find a dental policy which does not subject you to “excess” costs; allows you to see a highly skilled dentist, utilizing the latest technology and performing the most advanced form of treatment; all at a competitive premium? And this from a company which pays the claims they are contractually obligated to pay while doing so in a timely fashion?

This is where I, and my thirty-three years experience in the medical and dental insurance business, come in. My experience as a patient and consumer is even longer. After being in braces for eight years, I had all my front teeth knocked out in an auto accident when they impacted the steering wheel. I was wearing a seat belt, which saved my life, but not a shoulder strap. I’ve had to have the dental work replaced on three occasions since that senior year of high school. This year, I proceeded with what will be one double crown and, ultimately, two implants. (Ouch, is right!) I was not willing to accept this type of work from a mediocre dentist―and certainly did not care to pay cash for it! So I found a policy, issued by a large, financially sound insurance company, with a reputation for excellent customer and claim service. Then I found a policy which ultimately pays the maximum $5,000 annual benefit. In order for it to be affordable to me, it started, December 1 of 2018, at a calendar year benefit of $1,500―immediately went to $2,500 January 1, of this year―and will go to a $5,000 benefit this coming January. So I only paid for a $1,500 benefit for one month before it jumped to a $2,500 benefit! During this year I acquired the double porcelain crown and the bone graft and post for one dental implant. In 2020, I will have the crown for the implant post attached, when my calendar year benefit is $5,000. The second implant is optional, and I will probably have that work done in 2021 when my benefit remains $5K.

Once I knew what company to go with, the final step in selecting my dental insurance policy required finding the right dentist. I reviewed the insurance company’s list of network providers and researched the dentist’s reputation via credentials and reviews. I won’t belabor that but, suffice it to say, I found a dentist who met my requirements. He is very conveniently located relative to any resident of The Woodlands or Spring and, in my opinion, is well worth going to if you reside anywhere in Montgomery County or Northwest Harris County. He utilizes the latest technology, has a great and skilled staff, and a decent, very professional, if not overly effusive, chairside manner.*

In summation, in order to make dental insurance worth your while, you need to:

1) accept you need to acquire a “network provider” dental plan

2) find a policy which pays a reasonable benefit based on your foreseeable need, at an affordable premium and

3) allows you to go to a skilled dentist convenient to you

I have done all the homework for you. For over three decades, I have specialized in medical, Medicare-related, and dental insurance. I provide objective quotes from established “A” rated companies and quality customer service. Among the companies I represent are Aetna, Ameritas, Anthem, BlueCross BlueShield, Cigna, Delta Dental, Humana, and UnitedHealthcare. I am located in the heart of The Woodlands and am accessible from my websites Allplanhealthinsurance.com and TheWoodlandsTXHealthInsurance.com. You may also feel free to contact me at my numbers below.

I look forward to working with and assisting you in acquiring any of the above referenced products.

*(Neither I nor my agency and websites are affiliated in any way with a particular dentist or dental office. Neither do we receive compensation from the same for any recommendation we may make.)

In a surprise announcement today the Center For Medicare and Medicaid Services gave notice they are reversing planned cuts to Medicare Advantage Plans for 2015. But after all variables are factored in will the end result be an increase or decrease in reimbursements for Medicare approved procedures next year?

If implemented the cuts would have resulted in 2% lower payments to Medicare providers on top of the 6% cuts for 2014. Instead, the agency says, payments will instead be increased 0.4%. Still, with all variables in play, Aetna anticipates payment reductions and Humana estimates a funding decline of 3%. (See feature article from Reuters below.)

What is the end result of all this? 2014 reductions already saw the termination of thousands of providers from HMO and PPO Medicare Advantage networks. Further reductions are likely to result in more of the same along with probable increases in premiums and copays for medical procedures. And–if not now–certainly when they are ultimately implemented as mandated by the Affordable Care Act (ACA). Which begs the question: If all these cuts to Medicare Advantage were for the purpose of financing the ACA, what is the long-term impact of delaying them on the financial solvency of the Act? Or was the latter really ever a concern of the administration? Or is it simply the case that concern over the effect of cuts on this fall’s election over-rides the need for the Act to be financially feasible? (In case you were naïve enough to believe feasibility was realistic in the first place.) In light of all the approximately 38 delays and changes in the law since its passage, it is apparent to this author that political expediency rules the day in Washington. In other words, “business as usual”.

(Reuters) – U.S. health insurers said on Tuesday they still expected cuts in government reimbursements for privately managed Medicare health plans for the elderly next year even after the Obama administration rolled back the steepest reductions.

The government agency that oversees Medicare said late on Monday that on average, reimbursements to insurers for private Medicare plans would rise 0.4 percent, reversing what it said was a proposed cut of 1.9 percent.

The insurance industry and advocates for the elderly had lobbied against the cuts, which were first proposed in February, saying they would reduce benefits for older people.

Republican and Democratic lawmakers had broadly opposed further cuts as well, adding pressure on the administration at a time when President Barack Obama’s healthcare law was also under attack.

After analyzing the final rate notice from the Centers for Medicare and Medicaid Services (CMS) and comparing it with their own models, health insurers said on Tuesday that the 2015 Medicare Advantage payment rates represented a cut to payments from 2014 levels.

Humana Inc, which derives two-thirds of its revenue from administering Medicare Advantage plans, said it expected a funding decline of about 3 percent for 2015 plans from 2014, according to a filing with the Securities and Exchange Commission.

This is slightly better than Humana’s initial forecast for a drop of 3.5 percent to 4 percent in those rates, based on the proposal issued on February 21.

Aetna Inc, which also provides Medicare Advantage plans, said it also anticipated a decline.

“Despite CMS’s actions, Medicare Advantage plans will still face rate decreases for 2015,” Aetna spokeswoman Kendall Marcocci said in a statement. The company is still evaluating the impact, she added.

CMS officials were not immediately available for comment on the insurers’ or analysts’ analyses.

Humana shares fell 1.7 percent on Tuesday. Aetna was little changed, and UnitedHealth Group Inc slipped 0.4 percent.

APPLES-TO-ORANGES

The comments from individual insurers echoed that of industry trade group America’s Health Insurance Plans, which said it was concerned about how the policy will affect the 15 million people who receive privately managed benefits. The balance of the more than 50 million older and disabled people who use Medicare are in a different program run by the government.

“The changes CMS included in the final rate notice will help mitigate the impact on seniors, but the Medicare Advantage program is still facing a reduction in payment rates next year on top of the 6 percent cut to payments in 2014,” AHIP President Karen Ignagni said in a statement.

Wall Street analysts saw an improvement of 2 to 3 percentage points in the government’s funding proposal, but they estimated about a 3 percent cut overall, not an increase of 0.4 percent.

They described an apples-and-oranges comparison between how they calculate the total impact of Medicare reimbursement rates versus how the government does so.

One difference may be that the government analysis did not reflect the 1 percent insurance tax that funds Obama’s Patient Protection and Affordable Care Act, while some analysts included it.

Another factor, some said, is that CMS adjusted its estimates to reflect the worsening health of some Medicare members, while analysts did not.

Analyst Sheryl Skolnick of CRT Capital described the final funding announcement as being “less worse” than anticipated.

“The market was assuming that the final rate would be better than the proposal, and that’s what it got,” Skolnick wrote in a note.

Each year, the government releases its formulas for determining how it will reimburse the insurers for plan members’ procedures and doctor visits. Insurers use this information to decide on the markets where they will offer plans and what benefits they can provide.

(Reporting by Caroline Humer; Editing by Michele Gershberg, Lisa Von Ahn)

Currently we have over 800,000 veterans awaiting decisions on their disability claims. The back log is so great–according to the most recent numbers available–the average wait time for a veteran is 15 months in Chicago, 16 months in New York and a year and a half in Los Angeles. Social Security’s disability program, which helps support 11 million Americans, will run through its trust fund in 2016, two years earlier than predicted. Couple this with the prediction Social Security, the fund that finances benefits for 44 million senior citizens and their survivors, will be exhausted by 2035 and Medicare, the health care program for those age 65 and over, will be have depleted its funds by 2024. Now consider a law has been passed which mandates health coverage for every American. Its objectives are largely, and initially, funded via subsidies from the federal government (you the tax payer). Can you possibly believe this is feasible given their track record? Given a federal debt of almost 17 trillion dollars? How long do you believe it will take before all private insurance companies are forced to withdraw from participation to be replaced by a single payer federally administrated program which can’t possibly be any more financially feasible than our government’s disability program, Social Security or Medicare?

House Votes To Target ACA Individual, Employer Mandates.

Coverage of the Obama Administration’s decision to delay the Affordable Care Act’s employer mandate continues Wednesday, the same day the House is set to vote to further capitalize on the weak position they believe the move has put Democrats in. Most reports, some national in scope, focus on the House votes to delay both the employer and individual mandates, while others focus on the implications of both of these provisions.

McClatchy (7/17, Kumar) reports that on Wednesday, the Republican-ruled House is expected to vote to delay key parts of the Affordable Care Act, a move that “is the latest in a sweeping legislative and political campaign to weaken the 2010 law and raise even more opposition in the eyes of an already skeptical nation, especially as it heads into 2014 elections that will decide control of the Congress and set the stage for the 2016 campaign for the White House.” The back-to-back votes will determine “whether to delay insurance mandates for both employers and individuals.”

(7/16, Howell) reports that “President Obama has threatened to veto” the bills. Meanwhile, “the votes will force Democrats to align with the president or distance themselves from the overhaul in the wake of its recent stumbles.” In addition, it has put the “Office of Management and Budget in the awkward position of threatening, in the case of the employer mandate, to kill a bill that would reflect the White House’s own decision-making.”

(7/16, Walsh) reports that “most House Democrats are expected to oppose two House Republican bills on Wednesday that would delay key provisions of Obamacare,” according to House Democratic Whip Steny Hoyer (D-MD).

(7/17, Baker) “Healthwatch” blog reports that the bill to delay the individual mandate “would cut the deficit, but would cause insurance premiums to rise,” according to the Congressional Budget Office.

Implications Of Employer Mandate Delay Still Unclear. The AP

(7/17, Alonso-Zaldivar) reports on the “domino effect” that is currently “undercutting” the Affordable Care Act: the Obama Administration’s delaying of the law’s employer mandate could “weaken” the individual mandate, because the requirement that companies report health insurance details for employers has also been pushed back. As the article explains, “without employers validating who’s covered, a scofflaw could lie, and the government would have no easy way to check.” The piece calls this yet “another incentive for uninsured people to ignore a new government requirement that for many will cost hundreds of dollars.”

As more insurers decide to pack up and leave certain states as health exchanges start to take form, experts say consumers are going to be left feeling the pain.

Over the last few weeks, several departure announcements have sent a ripple through the health insurance industry, as companies weigh whether or not they want to play ball under Obamacare. So far, California has experienced the biggest migration with Aetna (AET), UnitedHealthcare (UNH) and Cigna (CI) leaving the state’s exchange, Covered California.

Aetna also reportedly sent out a note to select customers last week, warning that the Patient Protection and Affordable Care Act is “changing health insurance.” Recipients were customers across the country with non-grandfathered health plans, meaning their plan was not in effect on March 23, 2010 and wouldn’t carry over under new state and federal exchange regulations under ACA.

“This includes adding preventative care and essential health benefits. The ACA also ends medical underwriting. Due to these and other changes, many people will pay more for their health insurance coverage in 2014 than they do today,” the letter stated according to the carrier.

Wellmark Blue Cross/Blue Shield also decided not to list on the individual exchange in Iowa for 2014, due to a lack of information available in the state, according to a spokesperson for the Iowa Insurance Division.

Fifteen states and the District of Colombia are in the process of creating their insurance exchanges before the 2014 deadline; when individuals must purchase insurance or face a fine for failing for comply with the individual mandate. The employer mandate has been pushed back to 2015, and some in the GOP including House Majority Leader Eric Cantor, (R-VA), are calling for the individual mandate to be rolled back as well.

More or Less Competition for Consumers?

Some experts say the recent departures hint consumers will have limited health-insurance choices thanks to the regulatory burdens of the law. Basic supply and demand dictates that with fewer insurers to choose from, consumers will have limited options and potentially higher prices, says Michael Cannon, director of Health Policy Studies at the CATO Institute.

A similar “exodus” occurred within the first six months of the implementation of the Affordable Care Act, Cannon says, when child-only care was enacted. Seventeen major insurers dropped child-only coverage, in an attempt to skirt the law’s new regulations and increased costs. The same may begin to take shape in the individual market.

“The program says you can’t charge higher premiums to the sick, so you have a situation where only low-risk consumers would be charged a premium much higher than their regular costs, so only people who buy it would be those who really needed it,” he says.

The employer mandate rollback is also a factor in the situation, says Grace-Marie Turner, founder of the Galen Institute, a health and tax policy research organization, as employers will now be incentivized to drop coverage and push their employees into the exchanges until 2015.

“It’s using employers to push more people into the exchanges,” Turner says.

Fewer insurers in state exchanges mean less competition, bottom line, she adds. “The whole point is we want more players, and more competition.”

Why California Matters

What happens in California is a big deal for the future of the Affordable Care Act, says Taylor Burke, associate professor and program director, MPH in Health Policy, at George Washington University.

“It’s an exit out the individual market, but [the insurers] only represent 8% of the individual market companies in the state,” Burke says. “California has the 7th largest economy on the globe, so whatever happens in California is a big deal for the stand up of the state exchanges.”

He points to two main reasons insurers leave a state: they don’t like the price points being offered in the exchanges nor the coverage they would have to offer under Obamacare’s 10 essential health benefits.

“In California, you can make the argument that there would be less choice, but if they stay in the market, their prices would be off the charts,” he says. “It would be a thing on the shelf, a high-ticket item that you couldn’t afford anyway.”

And if insurers take too long to make the decision, that may impact them negatively as well, he says.

“No one will want to buy their product. There’s a lot of hemming and hawing, but if the price point is too high, no one will buy it.”

But can consumers blame the insurer for higher prices? Turner says no, it’s the nature of the law’s regulations.

“Insurers can’t help the demands on the benefits they will have to cover—it will absolutely be more expensive,” she says. “It’s like going to buy a car with every accessory in the books—heated seats, fancy wheels, satellite radio, and saying you can’t charge more for it.”

What Insurers are Deciding

Robert Zirkenbach, spokesman for America’s Health Insurance Plans (AHIP), says each individual company will have to make their own decisions about which states to participate in as exchange bids come in.

“It will be based on a variety of reasons, but plans are offering coverage on the exchange, some will be outside the exchange—there will be options for consumers,” Zirkenbach says. “It will depend on the state and regulatory environment.”

He says the AHIP wants competition among insurers to keep consumer prices in check. “Choice and competition is a good thing—when states have been setting up their exchanges, we are trying to encourage this,” he says.

The National Association of Insurance Commissioners says insurers who are leaving these markets are likely doing so because they have core businesses in other segments, including the large group market.

“The carriers we have seen exiting the individual market are not major players in that market segment, and therefore we don’t anticipate a major disruption of coverage for a large portion of the market,” a spokesperson said in an email statement. “Each insurance company is making decisions regarding its participation in exchanges based upon a number of factors. Some are opting to participate in the exchanges, while others are not; however, nearly all of the requirements that apply to policies sold on the exchange also apply to policies sold outside the exchange, so insurers will not be avoiding a lot of requirements by opting out of the exchanges.”

{kind=link}

Leave a comment