Dental Insurance: Worth the Premium — or Just a Payment Plan?

“Is dental insurance really worth what I pay for it?”

That’s a question I hear often—and it’s usually followed by:

“Or am I just spreading the cost of my dental work over time?”

My answer? It depends—but it doesn’t have to be a losing proposition.

Employer vs. Individual Coverage

If you receive dental insurance through an employer, part (or all) of your premium is subsidized. That makes the value proposition much more favorable.

However, if you are:

Self-employed

Retired

Or purchasing coverage on your own

…then you’re paying the full premium—and the math becomes more important.

Without the right strategy, dental insurance can become nothing more than a time-payment plan. Worse yet, you could end up paying more in premiums than you ever receive in benefits.

The Reality of Dental Costs

Let’s be honest—dental work is expensive.

A single dental implant can cost anywhere from $3,500 to $7,000. And unlike medical insurance, dental plans come with strict limitations.

Before choosing a plan, there are three key concepts you need to understand:

1. “Reasonable and Customary” Limits

No insurance company pays unlimited fees.

Instead, they base payments on what is considered “reasonable and customary” for your geographic area.

A crown in Beverly Hills will cost more than one in Brenham, Texas

If a dentist charges above the accepted range, you pay the difference

Understanding this concept is critical to avoiding unexpected costs.

2. Network vs. Non-Network Plans

Dental plans fall into two categories:

Network Plans (Recommended)

PPO (DPPO): Flexibility to go out-of-network (at higher cost)

HMO (DHMO): Must stay in-network for coverage

These plans offer lower negotiated fees because dentists agree to discounted rates.

Non-Network Plans

“Any dentist” plans

Typically higher premiums

Often result in higher out-of-pocket costs

Why? Because dentists are free to charge above what the insurance company considers reasonable—and you’re responsible for the difference.

3. The Most Important Rule: Avoid Excess Charges

Here’s where many people get burned:

With a non-network plan, you can be billed above what insurance pays

With a network plan, dentists must write off excess charges

That means:

If your share is 20% or 50%—that’s all you pay. No surprises.

Finding the Right Dentist (and Plan)

As an individual, you don’t have the bargaining power of a large employer.

So how do you gain access to lower fees and quality care?

You choose an insurance company that:

Has a large, reputable network

Pays claims promptly and reliably

Attracts high-quality dentists

Then you select a dentist based on:

Credentials

Technology used

Patient reviews

Location and convenience

Understanding Benefit Limits

Dental insurance is not unlimited coverage.

Typical plans:

Cover $1,000–$1,500 per year

Higher-end plans may go up to $5,000 annually

Often include waiting periods for major work

A smarter strategy is to choose a plan that:

Starts affordable

Increases benefits over time

Aligns with your expected dental needs

A Real-World Strategy (From Experience)

After decades in the business—and personal experience with extensive dental work—I approached my own coverage strategically.

I selected:

A financially strong insurance company

A plan that started at $1,500, then increased to $2,500, and ultimately $5,000 annually

A highly qualified dentist within the network

This allowed me to:

Stage treatment over time

Maximize benefits

Avoid excessive out-of-pocket costs

Bottom Line: How to Make Dental Insurance Work

To get real value from dental insurance:

✔ Choose a network plan

✔ Match benefits to your expected needs

✔ Select a skilled, in-network dentist

✔ Work with a knowledgeable advisor

How I Can Help

With over 30 years of experience in health, Medicare, and dental insurance, I help clients:

Compare plans from top-rated carriers

Avoid costly mistakes

Maximize benefits relative to premium

I represent companies such as: Aetna, Ameritas, Anthem, Blue Cross Blue Shield, Cigna, Delta Dental, Humana, and UnitedHealthcare.

Let’s Talk

If you’re considering dental coverage—or wondering if your current plan is worth it—I’d be happy to help.

D.Kenton Henry

TheWoodlandsTXHealthInsurance.com 📞 281-367-6565 Text my cell 24/7 @ 713-907-7984

Final Thought

Dental insurance can either be:

A smart financial tool or

An expensive payment plan

The difference lies in how you choose—and how you use—it.

By D. Kenton Henry – editor, agent, broker 12 March 2026

Good news for Indiana Medicare Supplement policyholders.

A recent update to Indiana’s new Medicare Supplement Birthday Rule has expanded the period during which eligible individuals may change their Medigap coverage without medical underwriting.

This change may reopen opportunities for some individuals who believed they had already missed their window.

HOT OFF THE PRESS

What Changed?

Beginning March 15, 2026, the Birthday Rule now allows policyholders to apply for a replacement Medicare Supplement policy during a period that begins:

31 days before their birthday and continues through 31 days after their birthday.

This creates a 63-day annual window centered around a person’s birthday.

What This Means

If you currently have a Medicare Supplement (Medigap) policy, you may now apply during this window to switch to the same plan letter offered by a different insurance company.

The insurance company must approve the application regardless of health conditions, provided the rule’s requirements are met.

Example

If your birthday is March 4, your Birthday Rule window would run from approximately:

February 1 through April 4

This means individuals with March birthdays who thought they missed the opportunity earlier this year may still qualify to apply.

Important Requirements

To use Indiana’s Birthday Rule:

• You must currently have a Medicare Supplement policy • The new policy must be the same plan letter as your current coverage • The application must be submitted within the 31 days before or after your birthday • The new policy will take effect on the first day of the month following the application date

Your broker will also need documentation confirming your current plan letter.

Why This Matters

For many seniors, this rule creates an opportunity to:

— without answering health questions or risking denial of coverage.

Need Help Reviewing Your Options?

If your birthday falls within this window and you would like to see whether switching carriers might benefit you, I would be happy to help review your options.

D. Kenton Henry Office: 281-3676565 Text my cell 24/7 @713-907-7984 Email: Allplanhealthinsurance.com

D. Kenton Henry Editor, agent, broker 30 SEPTEMBER 2025

Medicare 2026: Welcome clients and prospective clients! Before reading this (if you have not already), you should go to your mail box and retrieve your 2026 Annual Notice of Change from Medicare. You were due to receive it no later than today per Center For Medicare Rules and Regulations. If will give you a good idea if you need to re-shop your Medicare Advantage or Part D Drug plan for the coming calendar year. If not, the following changes may.

10 changes to review before the Annual Election period, often referred to as the Open Enrollment (Oct 15–Dec 7)

If you’re on Medicare, 2026 brings important updates—especially to prescription drug coverage. The Part D out-of-pocket cap rises to $2,100, the standard deductible becomes $615, and Medicare’s first negotiated drug prices start on January 1, 2026. Medicare Advantage also gets new guardrails around prior authorization and appeals, and some supplemental “perks” are being narrowed. Check your Annual Notice of Change (ANOC) (it should arrive by Sept 30) and compare your plan options—small differences can mean big savings. If you’d like help, I’ll review your medications, doctors, and benefits to make sure you’re in the right fit for January 1.

Here is an itemized list of the 10 Key Changes:

Medicare changes your 2026 plan review should cover

1) Part D’s annual out-of-pocket cap rises to $2,100. Once a member’s 2026 Part D out-of-pocket spending reaches $2,100, they’ll pay $0 for covered Part D drugs for the rest of the calendar year.

2) The standard Part D deductible increases to $615. Plans can’t set a deductible higher than $615 in 2026 under the redesigned Part D rules.

3) Drug price negotiations start showing up at the counter. Medicare’s first set of negotiated Maximum Fair Prices (MFPs) for 10 widely used Part D drugs take effect January 1, 2026. Members should review their ANOC and plan formularies to determine how these prices impact their medications.

4) Insulin and adult vaccines: protections continue. Part D insulin remains capped and no-deductible; starting in 2026, the cap is the lesser of $35, 25% of the MFP, or 25% of the negotiated price. ACIP-recommended adult vaccines remain $0 under Part D.

5) “Pay-over-time” for prescriptions auto-renews. The Medicare Prescription Payment Plan (monthly billing instead of paying large amounts at the pharmacy) auto-renews in 2026 unless the member opts out. It smooths payments but doesn’t lower total costs—good to remind clients who tried it in 2025.

6) Medicare Advantage prior-auth and appeals guardrails tighten. For 2026, CMS says MA plans must honor previously approved inpatient admissions (can only reopen for obvious error or fraud), and CMS closes appeals loopholes so members and providers receive required notices and can appeal adverse coverage decisions. Expect fewer mid-stay reversals. Centers for Medicare & Medicaid Services

7) Limits on certain “extra perks” in MA (SSBCI) take effect. CMS codified non-allowable Special Supplemental Benefits for the Chronically Ill—examples include non-healthy food, alcohol, tobacco, and life insurance. Some plans may rebalance extras as a result.

8) Star Ratings update: new/returning measures. 2026 Stars add or reintroduce measures like Kidney Health Evaluation for Patients with Diabetes plus Improving/Maintaining Physical and Mental Health (weight = 1). Tougher cut points in 2026 may shift plan bonuses and benefit richness—worth watching locally.

9) Part D benefit design shifts behind the scenes. Liability shares change across phases (plans, manufacturers, CMS), and there’s a new subsidy for selected (negotiated) drugs. Members may see formulary/tier adjustments—another reason to compare plans.

10) ANOC timing: what to tell clients. Remind everyone: Annual Notice of Change (ANOC) letters arrive by September 30 each year; if they didn’t see one, call the plan. Open Enrollment runs Oct 15 – Dec 7 for Jan 1 effective dates.

Check your Annual Notice of Change (ANOC) (it should arrive by Sept 30) and compare your plan options—small differences can mean big savings. If you’d like help, I’ll review your medications, doctors, and benefits to make sure you’re in the right fit for January 1.

Other Developments

Some Medicare Advantage supplemental benefits (i.e. nutrition support, OTC medicine) may be reduced in favor of core services.

In six states, prior authorizations for certain Original Medicare services will be tested.

Part B and Part D premiums and deductibles are both set to increase—Part B premium up ~11.6%, and Part D premium by about 6%.

Who Am I?

In addition to being the editor of this blog I have has been helping individuals and families navigate the health and Medicare insurance landscape since 1986. With nearly four decades of experience, he specializes in Medicare Supplement, Medicare Advantage, and Medicare Part D prescription drug plans.

As an independent broker, I am appointed with virtually every competitive, A-rated Medicare insurance company in Texas, Indiana, Ohio, and Michigan. This broad access allows him to recommend the plan that truly best fits each client’s needs.

Above all, I work for my clients—not the insurance companies. You will never pay more by enrolling through me than you would if you purchased an insurance product directly from the carrier. My mission is to provide clear guidance, personalized recommendations, and ongoing support to ensure my clients get the coverage and peace of mind they deserve.

If you have any questions about 2026 Medicare Part D prescription drug plans, Medicare Advantage, or Medicare Supplement (Medi-Gap) policies, please give me a call.

Average premiums, benefits and plan choices for Medicare Advantage and the Medicare Part D prescription drug program should remain relatively stable next year, CMS said in a Sept. 26 news release. But MA enrollment is projected to decrease 900,000 in 2026.

Despite a slight dip in available MA plans nationally, over 99% of Medicare beneficiaries will still be able to access an MA plan.

The agency estimates the premiums for MA plans to drop from $16.40 to $14.00. On average, the total premium for standalone Part D is estimated to fall $3.81. CMS’ July forecast predicted elevated Medicare Part D base premium increases in the neighborhood of 6%.

Congratulations! You’ve worked hard, and now you’re turning age 65! Navigating through the myriad of solicitations you are receiving and the choices you have to cover the expenses not paid by Medicare can be overwhelming.

The first thing is what not to do!

DO NOT CALL AN 800 NUMBER and talk to some anonymous employee of an insurance company. Not only are they restricted to limiting you exclusively to their company’s options—but your personal information will be instantly sold and shared. Your phone is going to begin ringing off the hook!

I’ve been specializing in Medicare-related insurance for over thirty years, right here in The Woodlands, Texas, USA! I represent every Medicare-related product, including Supplement, Advantage, and Part D Drug plans, from virtually every “A” rated company doing Medicare-related business in Texas. And I CHARGE NO FEE for my services! Deal with a local agent/broker who values your business enough not to share it with anyone!

D. Kenton Henry Editor, Agent, Broker Office: 281.367.6565 Text my cell 24/7 @713.907.7984 Email: Allplanhealthinsurance.com@gmail.com

By D. Kenton Henry Editor, Agent, Broker HealthandMedicareInsurance.com 11 September 2024

Welcome, fellow boomers and others blessed to have lived long enough to find yourself here. I believe you recognize that the information in my blog posts can contribute to this leg of our journey being the longest and most rewarding. I’m right here with you and doing my best to make it so for all of us. Coming changes in 2025 Medicare plans are significant, so please read this and feel free to take notes. They could impact you and probably will.

We will begin with what your Medicare Part B premium to Medicare for Out-Patient Care will go to: For those earning less than $105,000 your premium will go to $185.00 (up from $174.70) For those in the highest income bracket, earning greater than $500,000 your premium will go to $628.90 (from $594.00) For every income block in between, couples filing jointly, and what Part D premiums to Medicare will go to, please click on this link and scroll down: https://www.irmaacertifiedplanner.com/2025-irmaa-brackets/

An Annual Notice of Change (AOC) from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan is due you. It will arrive in the United States mail and, per Medicare rules, by September 30th. So, like the pretty woman in the image above, open it and read it. It outlines how much your premiums, deductibles, and co-pays will differ in the coming year. Will your drugs be covered, and will your current drug plan even be available? We don’t yet know. Mutual of Omaha notified agents and brokers that it is withdrawing altogether from the Part Drug plan market beginning January 1. If you are currently with them or have any other plan that is exiting the marketplace, follow the instructions in the next paragraph.

According to eHealth, a mere 36% of those surveyed claim the AOC to be “readily understandable.” The author of the attached article recommends you spend at least 30 minutes reviewing it. However, if you finish this article, you can cut that time considerably. If you have finished all and still feel you are among the remaining (up to) 64%—please call me @ 281-367-6565.

This article is a follow-up to my last blog post on September 3rd. “MAJOR CHANGES IN MEDICARE PART D DRUG PLANS ARE COMING OUR WAY (what we know. and one thing we don’t know).” To read it, please click on this link. (if necessary, copy and paste it in your browser’s URLbox and hit enter):

Well, now we know more of the potential compromises mentioned or alluded to in that article. All of these are covered in detail in Feature Article 1 below.

The changes addressed here are largely because of the new $2,000 per year limit on Medicare Part D drug costs in 2025 (versus $8,000, plus 5% thereafter, in 2024). That leaves Medicare Part D insurance companies looking for ways to compensate for the additional costs shifting from you to them. Come January, you will meet a new deductible of up to $590 (from $545) for applicable drugs. Typically, your plan will apply this to brand-name drugs and not Tier 1 or Tier 2 generics.

Beyond that, the Gap, commonly referred to as the “donut hole” (in which you were previously responsible for 25% of your drug costs), has been eliminated entirely. You will have entered the “Initial Coverage” phase in which your elected drug plan will pay 65% of your applicable drug costs, and you will pay 25%. The Manufacturer (pharmaceutical company) will discount the remaining 10%. When you hit your maximum Out-of-Pocket (OOP) threshold of $2,000, you enter “Catastrophic Coverage”. At that point, your plan will pay 60%. Reinsurance (CMS, the Center for Medicare Services, i.e., the government) will pay 20%, and the Manufacturer will pay the remaining 20%. You will pay $0.

This, of course, sounds very well and good! And for those utilizing large quantities of drugs, or expensive drugs, this will indeed be of great benefit. But in what ways may the drug plans “compensate” for the additional costs they will bear? Much of such was referenced or alluded to above. However, please permit me to drill down on potential measures drug plans may take to offset their increased share of your drug cost. *(I am a Medicare Insurance product broker and not a C.P.A. As such, I will not address the impact on the taxpayer of their increased share of Medicare drug costs in this forum. wink. wink 😉

The drill down:

In addition to the higher deductible, higher premiums may be in store. But it could have been a lot worse. CMS did health insurance companies a favor with a “premium-stabilization” plan. In 2025, they will give them a subsidy in exchange for not “slapping members with exorbitant premium hikes. So, “what might have been a 40%, 50%, or higher premium increase may only be as high as 25%. Either way, it will be a sticker shock when some see how their premiums changed.” *(a paraphrase a quote in Feature Article 1)

The Kaiser Family Foundation says the average cost of a stand-alone Part D drug plan is $43. I have seen previews of premiums which will be $0, but others, have risen. In addition to your premium, co-pays for your drugs could go substantially higher. If your drug plan is obligated to charge you less for (or cover more of) a particular drug, are they simply going to charge you more for others?

And what about “Value Added Benefits” (VAB) available in some Medicare Advantage Plans? These include vision, hearing, and dental services. Other examples include acupuncture, bathroom safety devices, and wigs for hair loss. And what about your gym membership? Embedded dental insurance has been dramatically cut back or removed completely.

VAB are not covered by Original Medicare. Medicare Advantage has been able (often along with a $0 premium) to offer these things as an additional incentive to encourage enrollment in their plans. However, because you left Original Medicare and “assigned” the administration of your benefits and claims to the Advantage company when you enrolled, your plan can choose to provide these ancillary benefits that Original Medicare does not. Or they can choose to cover them no longer. This discretion is on their part because the provision of VAB benefits is not codified in law or per CMS regulation. Resultingly, they are not guaranteed. They are optional benefits that the plans have the right to withdraw at any time. I hope you can continue to “workout” at the gym, at your plan’s expense, in 2025 and beyond. But be prepared to purchase a home gym kit if you learn your membership is downgraded or your Advantage plan disappears entirely.

With no obligation, please feel free to contact me for clarification of these relevant issues and additional guidance in navigating the Medicare system and the changes referred to here. I’m in Medicare with you. I am a “Boomer” who has spent the better part of his life in the medical insurance market. For years, I have assisted individuals, families, and businesses in identifying and enrolling in health insurance plans that came as close as I could get them to fully meeting their medical insurance wants and needs.

To sum things up, I work for my clients. I work for you. Not the insurance company. I study, take their tests, and “certify” to represent their products each calendar year. I just completed certifying with approximately 14 companies in preparation for marketing their products in 2025. They do not pay to renew my licenses or my Errors and Omissions insurance, nor do they cover my office insurance and expenses. Neither they, nor anyone else, pay me wages or a salary. And that is great! I knew and understood those terms when I went out on my own. And that is precisely why I did it. I did not want to be beholden to the insurance company.

After becoming independent, the list of companies I was contracted with grew to over 40 during the 1990s. That number has changed as many of those companies went the way of the steam engine with “Obamacare” and all the red tape and regulations that come with it and remaining in the industry. But I persist. I remain positioned to provide you with virtually every available Medicare and health insurance product in your region.

In conclusion:

If you’re reading this, chances are you remember Jim Rockford (a private detective, portrayed by the actor the late James Garner) in his TV show, The Rockford Files (you can hear the opening music now, can’t you?). In the prelude to each episode, you see his cassette recording answering machine and hear the message, “This is Jim Rockford. At the tone, leave a message …”.

Should you get mine, please do the same. Or you may simply text me.

FORTUNE Richard Eisenberg Updated Mon, Aug 26, 2024

Why this year’s Medicare Annual Notice of Change will be vital reading for beneficiaries

In this article:

If you’re on Medicare, you’ll be getting one or two Annual Notice of Change letters in your mail or email this September about your 2025 coverage and costs. You may be tempted to ignore what looks like junk, as nearly a third of recipients do, according to an eHealth survey.

Don’t.

“So often, a person who is quite happy with their plan and doesn’t bother to look at their Annual Notice of Change then gets a nasty surprise in January” when the plan’s new costs and coverage kick in, says Danielle Roberts, author of 10 Costly Medicare Mistakes You Can’t Afford to Make and founding partner of Boomer Benefits, which sells Medicare policies.

What is an Annual Notice of Change?

An Annual Notice of Change from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan lays out how much your premiums, deductibles, and co-pays will differ in the year ahead and whether the plan will even be offered. (Medigap plans don’t send these notices because they don’t change much year to year.)

An Annual Notice of Change from your Part D plan also says whether your prescriptions will be covered and, if so, how much you’ll pay. A Medicare Advantage Notice of Change will tell you if your doctors and hospitals will remain in the plan’s network.

While this information is always essential to make smart choices during Medicare’s eight-week open enrollment period (Oct. 15 – Dec. 7), experts say reading your Annual Notice of Change is especially important in 2024.

“There is an excellent chance that something is changing on your plan,” says Roberts. “This year, more than ever, we can expect big changes in the plans.”

Surprising effect of the $2,000 prescription drug cap

That’s largely due to a major Medicare change coming in 2025: the new $2,000 cap on out-of-pocket costs for prescriptions covered by a Part D plan.

Since Part D health insurers will be on the hook for more prescription costs due to the cap, they’ll be looking for ways to compensate.

That could mean higher premiums (currently $43 a month for stand-alone plans, on average, according to KFF), deductibles, and co-pays—possibly substantially higher than in 2024.

“I have been very, very concerned about what the $2,000 cap was going to do to Part D premiums,” says Roberts.

The prescription drug change in 2025 could also lead to your Part D plan no longer covering certain medications you take or raising prices of ones it will.

Medicare Advantage plans—some facing profit squeezes currently—often include Part D coverage, so they may respond to the $2,000 cap by trimming or eliminating benefits to keep their popular $0 premiums intact, experts expect.

As a result, your Medicare Advantage benefits that original Medicare can’t offer—such as dental, vision, hearing, and gym memberships—could be less attractive than in 2024, or possibly gone entirely.

“It really will be important to understand what’s changing in the coming year in my current plan and does the plan still fit?” says eHealth CEO Fran Soistman. “Does it still provide the value that it did when I elected to go in it in the first place?”

Reading and understanding the Notice of Change

Your Annual Notice of Change will tell you—if you can understand it.

Only 36% of Medicare beneficiaries surveyed by eHealth said their Annual Notice of Change letter is “readily understandable.”

Figure on spending about 30 minutes closely reading your Annual Notice of Change to see exactly what will be different in 2025 and whether you’ll want to switch plans or coverage next year as a result.

During open enrollment, you can switch from your current Part D plan to another, from your Medicare Advantage plan to another, from Medicare Advantage to original Medicare as well as from original Medicare to a Medicare Advantage plan.

But don’t feel compelled to switch plans just because your Annual Notice of Change says your premium will go up a little or a benefit will be trimmed slightly.

“If there’s a modest benefit decrease or premium increase, but they’re satisfied with what the carrier is providing, people shouldn’t make a change,” Soistman says.

However, he added, if a medication you take will no longer be covered or your physician or hospital won’t be in network, that’s an important change that may persuade you to switch coverage.

The Medicare Plan Finder on Medicare’s site will let you compare Part D and Medicare Advantage plans for 2025.

And, as Philip Moeller writes in the forthcoming revised edition of his book, Get What’s Yours for Medicare, if your Medicare Advantage plan won’t include your favorite doctor or hospital in its network in the year ahead, it’s legally obligated to work with you to identify other physicians or hospitals in its network that you’d like.

A new program to help avoid big premium hikes

To help prevent drastic Part D premium increases, the government’s Centers for Medicare and Medicaid Services recently threw a bone to health insurers with a premium-stabilization plan.

Medicare will provide a special subsidy to those insurers for 2025 in exchange for avoiding slapping members with exorbitant premium hikes.

“It should take what might have been a 40%, 50%, or higher premium increase down to probably 25%,” says Soistman. “It’s still going to be a bit of sticker shock when some people see how their premiums changed.”

Roberts says, “I’m still somewhat concerned about premiums, but I feel a little better after the stabilization program announcement.”

Getting help if your Medicare plan will change

After reading your Annual Notice of Change, you may want to get help deciding on the right Medicare plans for 2025 and to understand the implications of coming changes to your plans.

You can ask a Medicare broker or agent for assistance; there’s a directory at the National Association of Benefits and Insurance Professionals site. The sooner you do, the better, since agents and brokers will be swamped near the end of open enrollment.

“At Boomer Benefits, we have to stop taking new requests after Thanksgiving,” says Roberts.

If one of your prescriptions won’t be covered by your Part D plan in 2025, call your doctor to see if another covered medication would be okay or if you should find a new plan that includes it, Roberts advises.

For information about Part D and Medicare Advantage plans without purchase recommendations, try yourState Health Insurance Assistance Program or visit Medicare’s site or call Medicare’s toll-free number.

More time for open enrollment?

Soistman believes all the changes coming to Part D and Medicare Advantage plans for 2025 will push back the arrival of the Annual Notice of Change documents to the last two weeks of September.

If so, this will give people with the plans less time than normal to read the notices before open enrollment.

The eHealth agency has asked the Centers for Medicare and Medicaid Services to extend open enrollment by about five days to give beneficiaries, insurers, and Medicare brokers more time. Boomer Benefits favors the extension, too.

So far, the government hasn’t responded to eHealth’s proposal.

Could the 2025 open enrollment become Medicare’s equivalent of the Department of Education’s FAFSA financial-aid form fiasco of chaos and confusion?

“I don’t think it will be quite as drastic. I think it is going to be a year of change, though,” says Soistman. “And change is hard for people.” ********* Please follow me follow D. Kenton Henry @Https://HealthandMedicareInsurance.com

MEDICARE ADVANTAGE PPO PLAN WITH $0 OUT-OF-POCKET FOR ALL MEDICAL EXPENSES IN OR OUT OF NETWORK WITH THE EXCEPTION OF RX DRUGS

Clients and Friends,

Medicare’s Annual Enrollment Period and Open Enrollment ends December 7th. If you are in a Medicare Supplement policy it is probably because you want to maintain access to as many doctors, hospitals, and providers as possible. And you know that you may see any medical provider that sees Medicare patients. It is also true that if you have been with your supplement policy a number of years, you have also experienced a premium increase—probably every year on your policy anniversary. And if you are beyond 70 years of age, there’s a good possibility your premiums are $300 or more per month. If you’ve remained with your current policy through continued premium increases it must be because you have one or more medical conditions which have precluded you from moving to a lower cost Medicare Supplement policy with a significantly lower premium. Well, this new option may just provide the solution to your ever increasing costs without compromising your access to medical providers. And it is a Medicare Advantage plan which—if you apply by December 7th (the last day of Open Enrollment)—you will not have to answer any health questions and your approval is guaranteed for a January 1 effective date.

Think about it. No Medicare Part B deductible which is going to $240 in 2024. No cost for any minor or major medical care during the year. A $0 copay for Tier 1 generic drugs. No cost for anything other than Tier 2-5 prescription drugs and no premium for a stand-alone Part D Drug plan to accompany your Medicare Supplement policy! All with no risk of being declined for medical reasons and pre-existing medical conditions covered from day 1.

The greatest challenge in finding the optimal Medicare Advantage Plan is not finding the best benefits or lowest premium and prescription drug costs. It is in finding one’s doctors and hospitals in the provider network of a plan. With this plan you may go in or out of the PPO network and experience $0 out-of-pocket for everything with the exception of Rx drugs beyond Tier 1 Preferred Generics which are still available for a $0 copay!

2024 MEDICARE ADVANTAGE PPO PLAN WITH $0 OUT-OF-POCKET IN OR OUT OF NETWORK WITH THE EXCEPTION OF RX DRUGS

The additional good news is that this plan, utilizing a PPO network, means that—although you should rarely find it necessary to go outside their network of providers—should it be—you may do so at $0 out-of pocket! I believe you will find the benefits and drug costs to be excellent. (see below)

I am recommending you go with this Medicare Advantage Flex (PPO) MAPD for 2024. For proprietary and Medicare compliance regulations, I will not be identifying this plan by name or insurance company. (You must contact me for that.) But HERE ARE THE HIGHLIGHTS:I) MEDICARE ADVANTAGE PPO PLAN

(Premiums and copays based on your residence in Texas)

Monthly Plan Premium = $238

Health Deductible = $0

Drug Deductible = $545 ($0 deductible for Tier 1 and Tier 2 generic drugs)

“Preferred” Pharmacies which include: CVS, HEB, KROGER, WALMART

Drug Copays:

Tier 1 (Preferred Generic) = $0.00

Tier 2 (Non-Preferred Generic) = $8.00

Tier 3 (Preferred Brand Name) = $47.00

Tier 4 (Non-Preferred Brand Name) = $100.00

Tier 5 Specialty Drugs = 25%

D. Kenton Henry

Agent / Broker @ TheWoodlandsTXHealthInsurance.com and Allplanhealthinsurance.com

Office: 281.367.6565

Toll Free: 800.856.6556

Text my cell 24/7 @ 713.907.7984

https://TheWoodlandsTXHealthInsurance.com

FOR THE LATEST IN HEALTH AND MEDICARE RELATED NEW, FOLLOW MY BLOG @ Https://HealthandMedicareInsurance.com

Ever since the passage of the Patient Protection and Affordable Care Act (ACA), commonly referred to as “Obamacare”, in 2010, the Department of Health and Human Services has dictated when and under what circumstances an individual and family can apply for and obtain health insurance. This period is known as the Open Enrollment Period, and it is upon us. Each year, between November 1st and December 15th, U.S. citizens and their families may apply for and obtain health insurance effective January 1st of the coming calendar year. From then until January 15th, they may apply for coverage effective February 1st. Beyond that date, they are locked out of any health insurance plan they were not enrolled in when the year ended. Only special circumstances such as losing “creditable” coverage through no fault of their own, moving out of a plan’s area, birth of a child, or death of a covered family member allow them to apply for coverage beyond the Open Enrollment Period. And only if they were insured when the special circumstance occurred and no more than 60 days have passed. Creditable coverage meets all the mandates of the Affordable Care Act, such as guaranteed coverage for pre-existing health conditions, including pregnancy and mental health disorders, along with no out-of-pocket for preventative medicine. All coverage is guaranteed so long as the above requirements are met.

If affordability of health insurance is an issue, Premium Tax Credits (subsidies) are available from the Department of Health and Human Services (DHS) to people or families whose income falls below a certain threshold.

WHO IS ELIGIBLE FOR THE PREMIUM TAX CREDIT?

To receive the premium tax credit for coverage starting in 2024, a Marketplace enrollee must meet the following criteria:

· Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2024 benefit year will be determined based on 2023 poverty guidelines

· Can not have access to affordable coverage through an employer (including a family member’s employer)

· Can not be eligible for coverage through Medicare, Medicaid, the Children’s Health Insurance Program (CHIP)

· Have U.S. citizenship or proof of legal residency (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements)

· If married, must file taxes jointly

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Your tax credit is based on the household income estimate you put on your Marketplace application.

Income between 100% and 400% FPL: If your income is in this range (in all states) you qualify for premium tax credits that lower your monthly premium for a Marketplace health insurance plan. The lower your income is as a percent of the FPL—the higher your subsidy.

The easiest way to determine whether and for how much you qualify is to call me. You will estimate your 2024 household’s adjusted gross income and my subsidy calculator will tell us (based on the number of people in your household) how much your subsidy will be. If we give the DHS the same information you give me, my calculations are usually accurate to within $3.00 of what you will actually receive. We then apply that subsidy against the premium of the plan you wish to acquire and arrive at your net premium.

The number of people who qualify for subsidies continues to grow. For details on this, please refer to this chart and my feature article 2 below.

As to how much retail (gross) premiums are expected to grow from 2023 to 2024, estimates put the national average at 6%. (For the details on this, please refer to Feature Article 1 below.) Given the rate of core and real inflation, this should not come as a surprise. Acquisition of a subsidy will certainly offset ever-increasing premiums.

As always, the greatest challenge to the consumer and their agent/broker is affordability or obtaining the desired benefits. Instead, it is finding their doctors in the networks of a health plan. In 2024, as it was this year, there will be over 100 different plans available from six to eight different companies, depending on where one resides. Dealing with this myriad of options is where my three decades specializing in health insurance in the Houston area is invaluable. I know which hospitals are in which plan networks, and my provider search tools scan all plans without you having to go from company to company for results. Because I represent every company doing business in Texas, you can acquire information on all of them with one call to me.

Again, Open Enrollment begins November 1st, and for coverage during the entirety of 2024, it ends December 15th. Unlike going to the marketplace (Healthcare.gov) you will get me each time you call my local office with questions and for assistance and service–as opposed to an 800 number where you will get a different individual each time you call. My service is much more personalized and detailed than that of an hourly worker at the end of that toll-free number. If I don’t provide you with the level of service you deserve, I don’t have a client. And if I don’t have a client, I don’t earn a living. And it costs you no more to go through me than directly to the company whose policy you ultimately acquire.

I look forward to working with you and providing the best of service. Please call me.

D. Kenton Henry

Office: 281-367-6565 Text me 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

This analysis of insurers’ preliminary rate filings shows that ACA Marketplace insurers are requesting a median premium increase of 6% for 2024. Insurers cite price increases for medical care and prescription drugs as a key driver of premium growth in 2024, In addition to inflation’s impact on medical costs, insurers point to growth in the utilization of health care, which fell in 2020 but has since returned to more normal levels.

Insurers’ proposed rate changes – most of which fall between 2% and 10% – may change during the review process. Although most Marketplace enrollees receive subsidies and are not expected to face these added costs, premium increases could result in higher federal spending on subsidies.

The analysis can be found on the Peterson-KFF Health System Tracker, an information hub dedicated to monitoring and assessing the performance of the U.S. health system.

Enhanced Marketplace subsidies have continued to drive up enrollment in the individual market, and the loss of Medicaid coverage by millions of people could contribute to this trend, according to a new KFF analysis. Meanwhile, enrollment in non-ACA-compliant plans is at a record low.

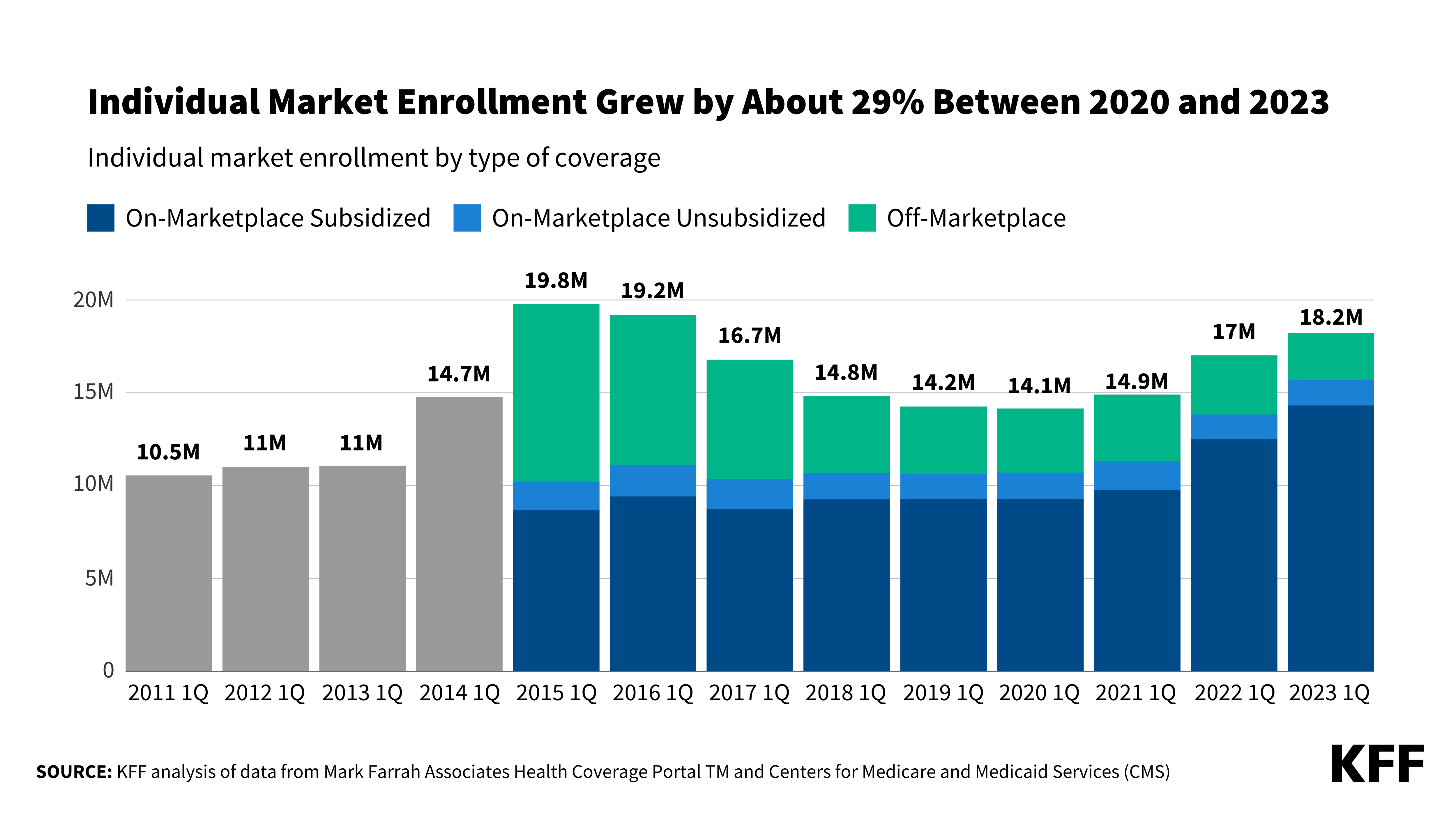

As of early 2023, an estimated 18.2 million people have individual market coverage, the highest since 2016. Individual market enrollment grew by about 29% between early 2020 and early 2023 — a result of enhanced subsidies introduced by the Inflation Reduction Act, increased outreach, and an extended enrollment period.

This enrollment growth could continue in 2023 as states resume Medicaid disenrollments amid the unwinding of the continuous enrollment provision. Some of the people losing Medicaid coverage may be eligible for subsidies on the ACA Marketplaces.

Due in part to the enhanced subsidies, about 4 in 5 individual market enrollees have subsidized coverage — the highest share since the ACA was implemented.

The number of people in non-compliant plans has fallen each year and could decrease further due to the Biden Administration’s proposed rule that would reverse the expansion of short-term plans. An estimated 1.2 million people were in non-ACA-compliant plans in mid-2022, compared to 5.7 million in mid-2015. These short-term plans often do not include certain benefits or coverage for pre-existing conditions and can impose a dollar limit on insurance coverage.

If unsubsidized premiums rise in 2024 due to higher health care prices and utilization, enhanced subsidies could shield most individual market enrollees from increases in their monthly payments.

As is the case each year, it behooves those in need of “Individual and Family” Affordable Care Act (ACA) compliant health insurance to re-shop their health insurance. This, because the premiums and benefits of your existing plan, and all others, will most certainly change in some respect. If for no other reason than in this circumstance:

If you receive a premium tax credit (subsidy) and the benchmark (second lowest cost Silver plan) premium in your area goes up, subsidy amounts will also go up. Conversely, if the benchmark premium goes down, subsidy amounts will also go down. This is independent of what your own plan’s price does.

Regardless of whether you receive a subsidy, premiums across most states will increase by an average of 7.7%, according to ACA Signups. As described in my feature article below, “That’s a little larger than the overall average rate increases we’ve seen for the last few years (3.5% for 2022, less than 1% for 2021, and a slight decrease for 2020). But an overall average rate change only gives us a big picture; it doesn’t tell you how much your own plan’s premium will change or how much your net premium will change, and it also doesn’t account for the new plans that will be offered for 2023.”

What we do know, is that two insurance companies are exiting the Texas health insurance market to one degree or another. Bright health insurance is exiting altogether, and Friday will cease offering “on-exchange” plans. In other words, plans that are available through the Federal marketplace, Healthcare.gov, for a subsidized premium. They will still offer “off-exchange” plans. What that means is, if you are currently insured by one of these companies and plans exiting Texas, you most certainly want to research and make an informed decision as to what replacement plan is in your best interest. Relative to insurance company expansion in the Texas market, Cigna will begin offering Individual and Family coverage beginning January 1. However, it will be limited to the Dallas-Fort Worth region for the time being.

The feature article does such a fine job of providing a comprehensive summation of the overall 2023 health insurance market that I will not it repeat here. Rather, I implore you, to read it in full. What I provide is local expertise that a national broker or quoting website cannot. Specifically, that is an insight into how each plan compares competitively in features and benefits and quality of local provider networks. I am intimately familiar with the local public’s preference for hospitals and medical providers as well as which health plans give them the greatest access to those, and which do not. My general impression, after 31 years in the Houston health insurance market, is that my client’s access to their doctors and hospitals is more important than premium. Particularly in Montgomery and the counties surrounding the city, as opposed to the city where the younger populace is more concerned with the latter. This is something, national marketers often fail to appreciate.

As you begin to ferret through the myriad of health insurance plan options available to you in 2023, please feel free to contact me for objective, no-fee, no-obligation guidance. I represent all insurance companies that will be issuing policies in southeast Texas and most in the remainder of the state. You may contact me via the email and phone numbers below. In the meantime, you may go to my quoting link where, in the next few days, you may enter your gender, age, and zip code, and conduct your preliminary research before calling me for details and insights. I look forward to working with you and having you as a client.

Thank you so much, D. Kenton Henry

Https://TheWoodlandsTXHealthInsurance.com Https://Allplanhealthinsurance.com Https://HealthandMedicareInsurance.com Office: 281-367-6565 Text my cell 24/7 @ 713-907-7984

For the latest in health and Medicare related insurance go to: https://HealthandMedicareInsurance.com

Open enrollment for 2023 ACA coverage: what to expect

Record-high enrollment in ACA-compliant plans is likely to continue this year – thanks to an extension of the American Rescue Plan’s affordability provisions

The tenth annual open enrollment for ACA-compliant individual/family health coverage is just around the corner. It starts November 1, and will continue through January 15 in most states.

Millions of Americans will enroll or renew their coverage for 2023 during open enrollment. Some have been buying their own health insurance for years, while others are fairly new to the process. And some are currently uninsured or have been covered by plans that aren’t ACA-compliant – such asa healthcare sharing ministry plan or short-term health insurance.

This article will give you an overview of what to expect during the open enrollment period. For even more information about open enrollment, check out our comprehensive guide to open enrollment.

ACA open enrollment will look mostly familiar this fall

In general, this year’s open enrollment period will be fairly similar to last year’s, but with some changes that we’ll address in more detail below:

The Inflation Reduction Act has extended the American Rescue Plan’s subsidy enhancements through 2025, so the subsidy rules that were in effect for 2022 will continue to be in effect for 2023. (There’s no “subsidy cliff” and the percentage of income that you have to pay for the benchmark plan is lower than it used to be.)

Because the subsidy enhancements have been extended, the record-high enrollment we saw this year is likely to continue, and the improved affordability that the American Rescue Plan created will also continue. But that doesn’t mean your premium will stay the same — more on this below.

Brokers and Navigators will continue to provide assistance with enrollment. And Navigator funding is higher than ever before, in an effort to increase outreach and enrollment assistance.

The insurers offering health plans through the exchanges (and outside the exchanges) will generally be the same insurers that offered plans for 2022. But there are several insurers joining the exchange or expanding their coverage area for 2023, and some insurers that are shrinking their coverage areas.

The IRS has proposed a fix for the “family glitch” which will make some families newly eligible for premium subsidies in the marketplace.

Standardized plans are returning to HealthCare.gov. Standardized plans were optional for insurers to offer in 2017 and 2018, but the federal government no longer created standardized plan designs as of 2019. For 2023, standardized plans will once again be available through HealthCare.gov. And they’re no longer optional; insurers are required to offer them.

Open enrollment dates and deadlines for 2023 plans

By now, most people are accustomed to the fact that individual/family health coverage is no longer available for purchase year-round, and instead uses open enrollment and special enrollment periods, similar to those used for employer-sponsored plans. The same open enrollment schedules apply to plans purchased through the exchange/marketplace and to plans purchased from insurance companies through private channels (ie, “off-exchange”).

Open enrollment begins November 1, and in nearly every state, it will continue through at least January 15. (Note that Idaho is an exception: Open enrollment in Idaho starts and ends earlier, running from October 15 to December 15. Idaho is the only state where open enrollment for 2023 coverage will end before the start of the year.)

So in most states, the enrollment schedule will follow the same timeframe that was used last year. And in most states, you’ll need to enroll by December 15 in order to have your coverage take effect on January 1. Enrolling after December 15 will generally result in a February 1 effective date.

One caveat to keep in mind: If your current health plan is terminating at the end of 2022 and not available for renewal, you can select a new plan as late as December 31 and still have it take effect January 1.

Although open enrollment continues through at least mid-January in most states, it’s generally in your best interest to finalize your plan selection in time to have the coverage in force on January 1. We’ve explained this in much more detail here.

In most states, that means you’ll need to enroll or make a plan change by December 15. In terms of the effective date of your coverage, there’s no difference between enrolling on November 1 versus December 15. But waiting until the last minute might feel a bit more stressful, and you might have trouble finding an enrollment assister who can help you at that point. You don’t need to be the first person in line, but it’s good to give yourself a bit of wiggle room in case you run into glitches with the enrollment process or find that you’d like assistance with some or all of it.

Rest assured, however, that open enrollment continues until at least mid-January in most states. So if there’s no way for you to get signed up in the earlier part of the enrollment window, you can most likely complete the process after the start of the year and have coverage in effect as of February.

Insurers entering and leaving individual and family markets

As is always the case, there will be some fluctuation in terms of which insurers offer individual/family health coverage for 2023. For the last several years, the general trend has been toward increased insurer participation in the exchanges. Here’s more about what we saw in 2020, 2021, and 2022.)

That trend is continuing in 2023, with new insurers joining (or rejoining) the exchanges in many states. But there are also some significant insurer exits that existing enrollees need to be aware of.

Several insurers are joining exchanges in the following states for 2023:

Bright Health (Exiting the individual/family market in all 17 states where they currently offer these plans, resulting in approximately a million exchange enrollees needing to select new plans; previously, Bright has planned to exit six states and remain in 11 other states, but that changed as of October 2022, when they announced a full exit from the individual market. Anyone with an individual/family plan from Bright Health — in any state — will need to switch to a different insurer for 2023. It’s possible, however, that Bright Health might continue to offer “an immaterial amount” of individual market plans in some states.)

WPS Health Plan Inc. is exiting the on-exchange market in Wisconsin, but will continue to offer off-exchange plans.

Friday Health Plans is exiting the on-exchange market in Texas, but will continue to offer off-exchange plans in Texas. Friday has not announced any exits in the other states where they offer plans in the exchange.

Even in states where the participating 2023 insurers will be the same ones that offered coverage in 2022, there may be service area changes in some states. This could result in an insurer’s plans becoming newly available in some areas, or no longer available in some areas.

The main takeaway point is that it’s important to actively compare your available plan options, as opposed to just letting your existing plan auto-renew. One of the new plans (or another existing plan) might end up being a better fit for your needs. But it’s also possible that the benchmark plan’s pricing could change significantly, affecting the amount of your subsidy. If the price of your current plan shoots up, a comparable plan will likely be available for about what you paid this year (if your income and family size haven’t changed).

It’s also worth keeping in mind that the insurer’s estimate of what you’re likely to pay in the coming year, provided in a letter this fall, may be inaccurate – again, because of a shift in its pricing relationship to this year’s benchmark plan. You’ll get a separate letter from the exchange with details about your subsidy amount for 2023 and the amount you’ll pay if you let your current plan renew. But it’s also essential to log onto the exchange, update your information, and learn what your current plan and alternative plans will cost in 2023.

Ever since ACA-compliant plans debuted in the fall of 2013, people have been ineligible for subsidies if they’re eligible for an employer-sponsored health plan that’s considered affordable. And the affordability determination has always been based on the cost of employee-only coverage, without taking into account the cost to add family members to the plan. But if the employer-sponsored plan was deemed affordable, the entire family was ineligible for subsidies in the marketplace, as long as they were eligible to be added to the employer’s plan. This is known as the “family glitch,” and it has put affordable health coverage out of reach for millions of Americans over the years.

Earlier this year, the IRS proposed a long-awaited fix for the family glitch, which is expected to be in place by the time open enrollment gets underway. Under the proposed rule change, the marketplace will do two separate affordability determinations when a family has access to an employer’s plan: one for the employee, and one for total family coverage. If the employee’s coverage is considered affordable but the family’s is not, the rest of the family will potentially be eligible for subsidies in the marketplace.

Some families will still find that they prefer to use the employer’s plan, despite the cost. But some will find that it’s beneficial to put some or all of the family members on a marketplace plan, even while the employee continues to have employer-sponsored coverage.

The main point to keep in mind here is that it’s important to double check your marketplace options this fall – even if you looked in the past and weren’t eligible for subsidies due to an offer of employer-sponsored coverage.

The only way to know for sure what your 2023 premium will be is to watch for correspondence from your insurer and exchange. They will notify you this fall about changes to your plan for 2023, including the new premium (and subsidy amount if you’re subsidy-eligible; most people are).

There’s a lot of variation from one plan to another in terms of pricing changes, and your net (after-subsidy) premium will also depend on how much your subsidy changes for 2023. But here’s a general overview of what to keep in mind:

Across most of the states, the preliminary average rate change for 2023 amounts to a 7.7% increase, according to ACA Signups. Final rates aren’t yet available in many states, but we’re generally seeing final rates that tend to be a bit lower than the insurers proposed. (This is partly due to the Inflation Reduction Act — which was enacted after insurers filed their rates and which will result in slightly smaller-than-proposed rate increases for some plans — and partly due to state regulators’ actions to reduce rates during the review process).

That’s a little larger than the overall average rate increases we’ve seen for the last few years (3.5% for 2022, less than 1% for 2021, and a slight decrease for 2020). But an overall average rate change only gives us a big picture; it doesn’t tell you how much your own plan’s premium will change or how much your net premium will change, and it also doesn’t account for the new plans that will be offered for 2023.

If the benchmark (second-lowest-cost Silver plan) premium in your area goes up, subsidy amounts will also go up. Conversely, if the benchmark premium goes down, subsidy amounts will also go down. This is independent of what your own plan’s price does. It can be possible, for example, for your plan’s premium to go up while the benchmark premium goes down (perhaps because a new insurer takes over the benchmark spot), resulting in a more significant increase in the actual amount you pay each month. This is why it’s so important to pay close attention to the information you receive from your insurer and the exchange, and to carefully consider all of your options during open enrollment.

You can start doing your plan shopping research now

If you already have marketplace coverage, keep an eye out for correspondence from the marketplace and your insurer. If you currently have off-exchange coverage, be sure to check your eligibility for subsidies in the marketplace; you might find that you can get a much better value by switching to a plan offered through the marketplace.

And if you’re currently uninsured or enrolled in non-ACA-compliant coverage, you’ll definitely want to look at the plan options that are available to you during open enrollment, and check your eligibility for subsidies. You might be surprised to see how affordable your coverage can be. The average enrollee is paying $133/month this year, and more than a quarter of enrollees are paying less than $10/month. Although specific plan prices change from one year to the next, this same overall level of affordability will continue in 2023.

Op-Ed by D. Kenton Henry Editor, agent, broker 10 May 2022

As a Medicare recipient, each fall during Medicare’s Annual Election Period (AEP) – from October 15th to December 7th – you are allowed to select a new Part D Drug Plan for the coming calendar year.

Did you research which of the approximately 30 Part D Drug Plans available to you would result in your lowest total costs in 2022? Did you select a plan because it quoted the lowest price and coinsurance for your drugs? Midyear, to your surprise, you have been informed the cost of your drug(s) is now much higher!

If you did, you are not alone. As a Medicare recipient, and an agent/broker working on behalf of Medicare clients, I am not only frustrated but somewhat embarrassed by this phenomenon. The reason for the latter is because one of the primary services I provide clients is to, during the AEP, quote the price of each of their prescription drugs and their lowest total cost drug plan for the coming new year. Clients rely on me for accurate information and base their drug plan selection on my research and quotes. When suddenly they are notified that their drugs’ actual price is higher or will be increasing midyear, it reflects poorly on me. Even though the information I provided them was accurate at the time and price discrepancies are beyond my control.

As my feature news article from Kaiser Health (below) explains, “As early as three weeks after Medicare’s drug plan enrollment period ends on December 7th, insurance plans can change what they charge members for drugs – and they can do it repeatedly.”

Please read the article for full disclosure about how this is allowed to happen. Suffice it to say, many Medicare recipients are living on a fixed income, and this practice makes it very difficult for them to budget appropriately and pay their drug and remaining bills. As a consumer, my opinion is that this practice is unconscionable and inexcusable. It seems if a pharmaceutical company wants a particular drug company to include its drug in their plan’s formulary, they should quote a price and be contractually committed to, and obligated to, providing that drug at that price for the entire coming calendar year. As with a fixed mortgage or purchase agreement, the terms should be locked in for the life of the contract. Again, in my opinion, anything less assumes the character of a “bait and switch” transaction.

Feature Article 2 highlights the pushback on brand name drug coverage by Medicare while pointing out the preferred treatment in lower drug costs for Medicaid recipients. Their savings are provided by discounts and coupons vs the drug cost for those in Medicare who do not receive those.

In terms of working with me as a professional, I will continue to provide my clients the most accurate price and dispensing information for Rx drugs and the Part D Drug plans available to them. This will be the case for purposes of the AEP; because they are new to Medicare; or because they need to change plans due to a residential move and plan availability. I do not charge a fee for this service.

In the meantime, do not hesitate to contact me with any questions or assistance you might require. Not only as they relate to Medicare but for you or family members who might not yet be eligible for Medicare. My services and terms apply to Under Age 65 health insurance, as well.

Drug plan prices touted during Medicare open enrollment can rise within a month

May 3, 20225:00 AM ET

SUSAN JAFFE

Retiree Donna Weiner shows some of the daily prescription medications for which she pays more than $6,000 per year through a Medicare prescription drug plan. She supports giving Medicare authority to negotiate drug prices.

Phelan M. Ebenhack/AP

Something strange happened between the time Linda Griffith signed up for a new Medicare prescription drug plan during last fall’s enrollment period and when she tried to fill her first prescription in January.

She picked a Humana drug plan for its low prices, with help from her longtime insurance agent and the Medicare Plan Finder, an online pricing tool for comparing a dizzying array of options. But instead of the $70.09 she expected to pay for her dextroamphetamine, used to treat attention-deficit/hyperactivity disorder, her pharmacist told her she owed $275.90.

“I didn’t pick it up because I thought something was wrong,” said Griffith, 73, a retired construction company accountant who lives in the Northern California town of Weaverville.

“To me, when you purchase a plan, you have an implied contract,” she said. “I say I will pay the premium on time for this plan. And they’re going to make sure I get the drug for a certain amount.”

But it often doesn’t work that way. As early as three weeks after Medicare’s drug plan enrollment period ends on Dec. 7, insurance plans can change what they charge members for drugs — and they can do it repeatedly. Griffith’s prescription out-of-pocket cost has varied each month, and through March, she has already paid $433 more than she expected to.

A recent analysis by AARP, which is lobbying Congress to pass legislation to control drug prices, compared drugmakers’ list prices between the end of December 2021 — shortly after the Dec. 7 sign-up deadline — and the end of January 2022, just a month after new Medicare drug plans began. Researchers found that the list prices for the 75 brand-name drugs most frequently prescribed to Medicare beneficiaries had risen as much as 8%.

Sponsor Message

Medicare officials acknowledge that manufacturers’ prices and the out-of-pocket costs charged by an insurer can fluctuate. “Your plan may raise the copayment or coinsurance you pay for a particular drug when the manufacturer raises their price, or when a plan starts to offer a generic form of a drug,” the Medicare website warns.

But no matter how high the prices go, most plan members can’t switch to cheaper plans after Jan. 1, said Fred Riccardi, president of the Medicare Rights Center, which helps seniors access Medicare benefits.

Drug manufacturers usually change the list price for drugs in January and occasionally again in July, “but they can increase prices more often,” said Stacie Dusetzina, an associate professor of health policy at Vanderbilt University and a member of the Medicare Payment Advisory Commission. That’s true for any health insurance policy, not just Medicare drug plans.

Like a car’s sticker price, a drug’s list price is the starting point for negotiating discounts — in this case, between insurers or their pharmacy benefit managers and drug manufacturers. If the list price goes up, the amount the plan member pays may go up, too, she said.

The discounts that insurers or their pharmacy benefit managers receive “don’t typically translate into lower prices at the pharmacy counter,” she said. “Instead, these savings are used to reduce premiums or slow premium growth for all beneficiaries.”

Medicare’s prescription drug benefit, which began in 2006, was supposed to take the surprise out of filling a prescription. But even when seniors have insurance coverage for drugs, advocates said, many still can’t afford them.

“We hear consistently from people who just have absolute sticker shock when they see not only the full cost of the drug, but their cost sharing,” said Riccardi.

The potential for surprises is growing. More insurers have eliminated copayments — a set dollar amount for a prescription — and instead charge members a percentage of the drug price, or coinsurance, Chiquita Brooks-LaSure, the top official at the Centers for Medicare & Medicaid Services, said in a recent interview with KHN. The drug benefit is designed to give insurers the “flexibility” to make such changes. “And that is one of the reasons why we’re asking Congress to give us authority to negotiate drug prices,” she said.

CMS also is looking at ways to make drugs more affordable without waiting for Congress to act. “We are always trying to consider where it makes sense to be able to allow people to change plans,” said Dr. Meena Seshamani, CMS deputy administrator and director of the Center for Medicare, who joined Brooks-LaSure during the interview.

On April 22, CMS unveiled a proposal to streamline access to the Medicare Savings Program, which helps 10 million low-income enrollees pay Medicare premiums and reduce cost sharing. Enrollees also receive drug coverage with reduced premiums and out-of-pocket costs.

The subsidies make a difference. Low-income beneficiaries who have separate drug coverage plans and receive subsidies are nearly twice as likely to take their medications as those without financial assistance, according to a study Dusetzina co-authored for Health Affairs in April.

When CMS approves plans to be sold to beneficiaries, the only part of drug pricing it approves is the cost-sharing amount — or tier — applied to each drug. Some plans have as many as six drug tiers.

In addition to the drug tier, what patients pay can also depend on the pharmacy, their deductible, their copayment or coinsurance — and whether they opt to abandon their insurance and pay cash.

After Linda Griffith left the pharmacy without her medication, she spent a week making phone calls to her drug plan, pharmacy, Social Security and Medicare but still couldn’t find out why the cost was so high. “I finally just had to give in and pay it because I need the meds — I can’t function without them,” she said.

But she didn’t give up. She appealed to her insurance company for a tier reduction, which was denied. The plan denied two more requests for price adjustments, despite assistance from Pam Smith, program manager for five California counties served by the Health Insurance Counseling and Advocacy Program. They are now appealing directly to CMS.

“It’s important to us to work with our members who have questions about any out-of-pocket costs that are higher than the member would expect,” said Lisa Dimond, a Humana spokesperson. She could not comment about Griffith’s situation because of privacy rules.

However, Griffith said she received a call from a Humana executive who said the company had received an inquiry from the media. After they discussed the problem, Griffith said, the woman told her, “The [Medicare] Plan Finder is an outside source and therefore not reliable information,” but assured Griffith that she would find out where the Plan Finder information had come from.

She won’t have to look far: CMS requires insurers to update their prices every two weeks.

“I want my money back, and I want to be charged the amount I agreed to pay for the drug,” said Griffith. “I think this needs to be fixed because other people are going to be cheated.”

KHN (Kaiser Health News) is a national newsroom that produces in-depth journalism about health issues. It is an editorially independent operating program of KFF (Kaiser Family Foundation).

Beauty may be in the eye of the beholder, but drug price trends are in the way you crunch the numbers.

Beauty may be in the eye of the beholder, but drug price trends are in the way you crunch the numbers.

In a piece posted on the Health Affairs Forefront blog last month, Anna Anderson-Cook, Ph.D., and her colleagues at Arnold Ventures argued that analyses by IQVIA and others that show relatively level or even decreased net drug prices in recent years may be misleading. Arnold Ventures, formerly The Laura and John Arnold Foundation, is a philanthropic organization that supports a variety of criminal justice, education and healthcare projects. In healthcare, it has been one of the main supporters of Civica Rx, a nonprofit drug manufacturer, and the Institute for Clinical and Economic Review, a cost-effectiveness research organization in Boston.

One of the interesting points raised by Anderson-Cook and her colleagues is that overall trends “do not apply to the commercial market or to Medicare Part D, where net prices are both significantly higher and growing more rapidly” than they are for other payers. They cite Medicaid as an example of a payer that skews overall results. Medicaid plans have considerably lower net drug costs (costs after rebates and other discounts) than Part D plans because of Medicaid-specific rebates rules that result in larger rebates for Medicaid programs.

The Arnold Ventures researchers also made the case that year-over-year comparisons of net prices for drugs that are already on the market paint an incomplete picture because of the number and expense of new drugs.

Citing a Congressional Budget Office report, Anderson-Cook and her colleagues noted that in 2017 drugs launched after 2015 cost 12 times as much as drugs already on the market in 2015. What’s more, new drugs tend to do well, sales wise, once they are approved and on the market. The Arnold Ventures researchers pointed to a Part D dashboard maintained by CMS that shows that 30 brand-name drugs launched after 2015 were top sellers in Part D by 2019.

So far the cost of these new brand-name drugs has been offset by the shift from brand-name products to generics among the older drugs. The migration to generics has kept increases in net spending per beneficiary in Part D plans on a relatively even keel, meaning it hasn’t surpassed inflation.

The researchers also noted that at 90% the generic dispensing rate may have reached its upper limit. If brand-name drug costs continue to escalate while the generic market stays at 90%, there will be upward pressure on Part D spending, notwithstanding the level-to-moderate spending in the recent past. They cited a 2021 Medicare Trustees Report that projects that the cost of the Part D program will grow by 6.1% annually over the next five years. Biosimilars to the brand-name biologics may have their intended effect, tugging down prices of the biologics, but so far they haven’t had the same effect on prices that generics have had on small-molecule drugs, say the authors.

Without comprehensive reform, Anderson-Cook and her colleagues concluded, the cost of brand-name drugs will “grow aggressively,” straining the Medicare budget and the resources of the program’s beneficiaries.

Op-ed by D. Kenton Henry Editor, Broker 21 March 2022

Greetings from TheWoodlandsTXHealthInsurance.com, deep in the heart of The Woodlands, Texas, for 31 years now!

The “Annual Election Period” (AEP), when Medicare Recipients can change their Part D Drug Plans or enroll in a Medicare Advantage Plan, has closed for 2022. As always, it will reopen October 15th and run through December 7th, for a January 1 effective date. So (minus extenuating circumstances), people are locked into their existing drug and Medicare Advantage Plans for the remainder of the calendar year.

During these AEP’s – when I am inundated with clients who instruct me to shop for their best plan for the coming calendar year – I am also asked, by many, to reshop their Medicare Supplement Plan. This in spite of the fact that I can reshop their Medicare Supplement Plan 365 days of the year! I suppose it’s a combination of not knowing this about Supplement plans and their simply being “out of sight … out of mind” until the AEP when every TV and radio ad is telling them to call for the Medicare benefits “they’re entitled to”!

The first reality is – all Medicare Supplement premiums increase as we age. Couple this with cost increases within Medicare itself – which are inevitably passed on to premiums – and it behooves us to reshop our Medicare plans periodically. I recommend every two to three years.

The second reality is – outside the AEP – January 1 until October 15th – I am in a much better position to give the proper and utmost attention to my clients, and prospective clients, and ensure I am getting them approved for a Medicare Supplement plan for which:

1) they can realistically be fully approved without a rate-up in premium

2) which provides them benefits equal to or appropriate for their needs and

3) saves them significant premium dollars

Things which might provide further incentive to apply for replacement coverage are:

1) they are now eligible for a “household discount” (typically 7%)

2) they are now in Medicare Supplement Plan F and realize conversion to Plan G will save them such significant premium savings it easily offsets the liability for the Part B calendar year out-patient deductible they will have to meet. Or . . .

3) they wish to save even more and apply for Plan N

Before proceeding to take an application, I make it abundantly clear to a prospective applicant that, now that they are more than six months past their date of enrollment in Medicare Part B – they no longer qualify for “Guaranteed Issue.” This means every applicant must qualify based on their health history. The process entails answering health-related questions and providing physician and prescription drug medications. The thing that most often results in an application being declined for issue is a pending or anticipated surgery or hospital stay. Absent these, if a person’s health issues are relatively controlled with medication, or otherwise – and their weight is relatively proportionate to their height – they stand a good chance of being approved. In which case, I would encourage them to apply for replacement coverage. At that point, the only thing at risk is the time it takes to complete an application. The worst case is a declination, which doesn’t preclude you from being approved at a later date. It is not like a derogatory remark on a credit report!

In conclusion (for those of you old enough to remember and – if you are on Medicare – you are!) now is a time when I am a bit like the “Maytag Repairman”. In other words, with the exception tending to my prospects just turning age 65 and aging into Medicare, I am sitting around waiting for the phone to ring. (smiling emoji)

I hope to hear from you, so please refer to my contact information just below. Aside from this, please read my feature article which follows immediately. It is relevant to all Medicare recipients but especially to those currently enrolled in Medicare Advantage primarily for the purpose of consolidating supplement coverage – such as dental and vision – with their medical insurance. Changes could well be coming.

D. Kenton Henry Office: 281.367.6565 Text my cell 24/7: 713.907.7984 Email: Allplanhealthinsurance.com@gmail.com

Medicare Watchdog Warns of $12 Billion in Excess Payments