Date: September 3, 2024

Editor, Broker, Agent – D. Kenton Henry TheWoodlandsTXHealthInsurance.com; HealthandMedicareInsurance.com

Each year, our Medicare Part D Drug Plan and Medicare Advantage Plan owe us our Annual Notice of Change (ANOC). Your plan is obligated to have it to us by September 30th. Resist the temptation to ignore it, AS MAJOR CHANGES ARE COMING OUR WAY! Your ANOC will arrive by U.S. mail along with dozens of solicitations for our Medicare insurance business. So, watch for it and review it carefully.

These changes are credited to the Biden “Inflation Reduction Act.” On the surface, they will undoubtedly benefit many seniors using prescription drugs. What remains to be seen are the consequences beneath the surface. The first is … at what cost (premium)? Your current plan’s 2025 premium will be in your ANOC. But we will have to wait until October 1 to know what the alternative plans will cost. This begs the question—because of the additional cost of these mandated improvements in benefits—will all these 30 different plans and their companies even remain in the marketplace? And what if yours doesn’t?

Let’s address the upcoming changes in benefits:

We will begin with what your Medicare Part B premium to Medicare for Out-Patient Care will go to:

For those earning less than $105,000 your premium will go to $185.00 (up from $174.70)

For those in the highest income bracket, earning greater than $500,000 your premium will go to $628.90 (from $594.00)

For every income block in between, couples filing jointly, and what Part D premiums to Medicare will go to, please click on this link and scroll down: https://www.irmaacertifiedplanner.com/2025-irmaa-brackets/

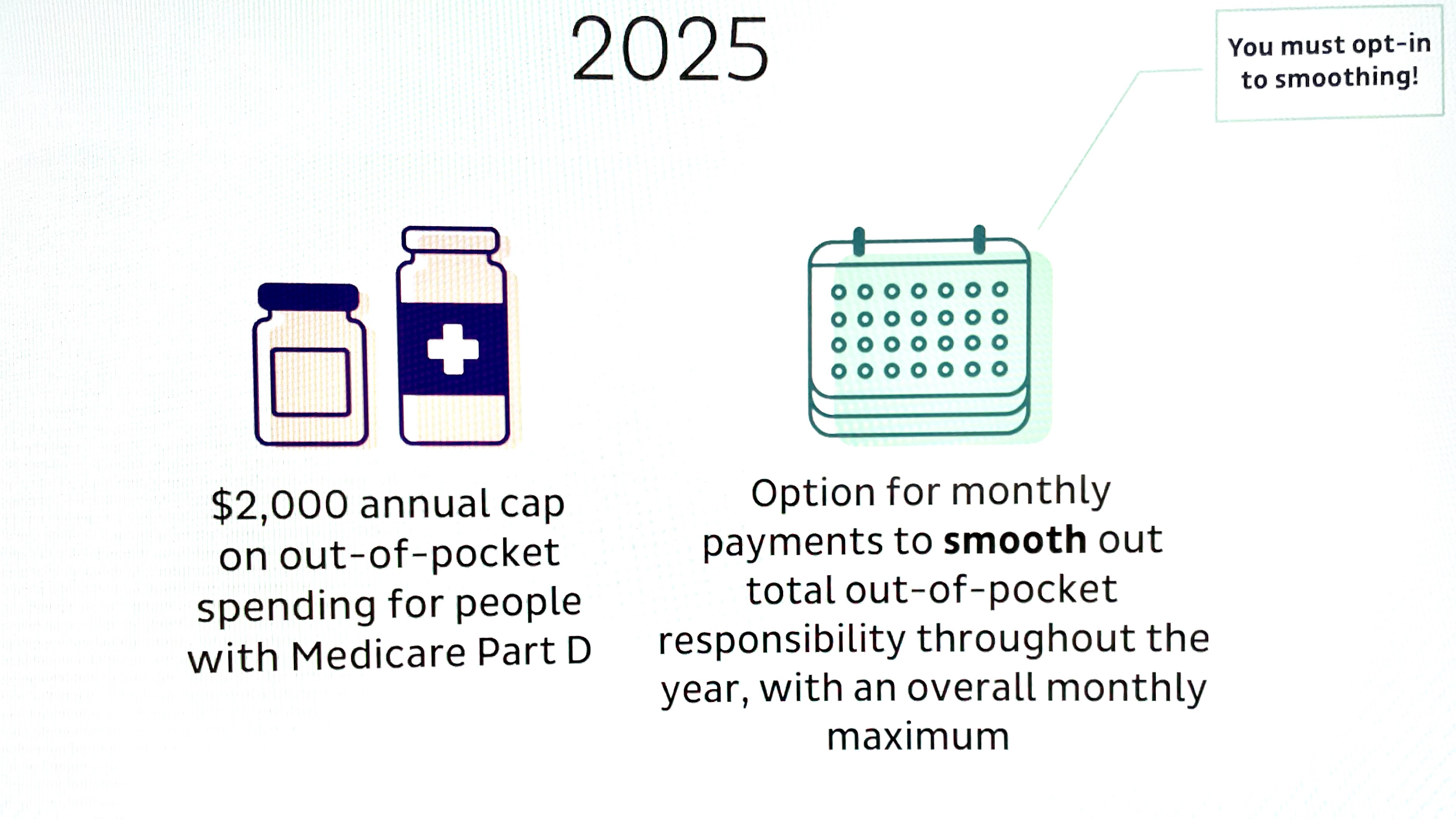

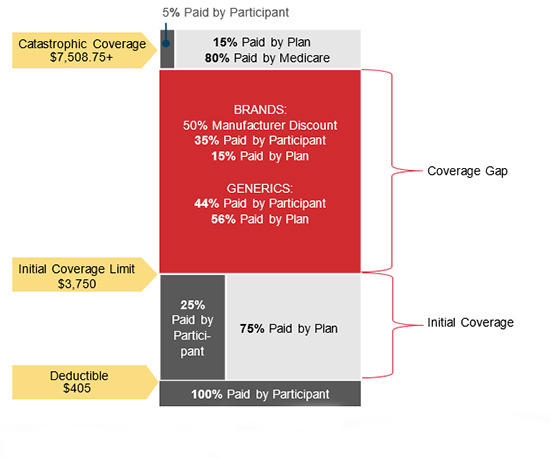

Relative to Medicare Part D Prescription Drug plans, as is the case in 2024, there is no beneficiary cost sharing above the annual OOP threshold. That will be $2,000 in 2025. That’s down from $8,000 in 2024! The coverage gap phase (also known as the “donut hole”) will be eliminated, which will result in standard Part D coverage consisting of a three-phase benefit: a deductible phase, an initial coverage phase, and a catastrophic phase. The annual Part D Drug Plan deductible caps at $590, up from $545 this year.

Here is how the changes take effect for the coming calendar years.

- 2025: The Inflation Reduction Act will lower out-of-pocket costs for Medicare Part D enrollees to a maximum of $2,000 per year. The Coverage Gap Discount Program will end and be replaced by the Manufacturer Discount Program. The standard Part D benefit design will also change to include three phases: deductible, initial coverage, and catastrophic coverage. The law will also require Part D plans to offer enrollees the option to pay for prescription drugs in capped monthly payments instead of all at once.

- 2027: Medicare will negotiate costs for 15 Part D drugs.

- 2028: Medicare will negotiate costs for 15 Part B and Part D drugs.

- 2029: Medicare will negotiate costs for 20 Part B and Part D drugs.

- Every year after 2028: Medicare will negotiate costs for 20 Part B and Part D drugs.

IN REVIEW:

In 2025, Medicare Part D, the federal program that helps Medicare beneficiaries pay for prescription drugs, will undergo significant changes aimed at reducing out-of-pocket costs for seniors and improving access to necessary medications. These changes are part of the ongoing implementation of the Inflation Reduction Act (IRA) of 2022, which introduced sweeping reforms to the healthcare system, particularly in prescription drug pricing.

Key Changes in 2025

1. Introduction of a $2,000 Out-of-Pocket Cap

One of the most anticipated changes is the introduction of a $2,000 annual cap on out-of-pocket costs for prescription drugs under Medicare Part D. This cap will significantly ease the financial burden for many seniors who, in previous years, faced unlimited out-of-pocket expenses once they passed through the “donut hole” coverage gap.

This new cap means that once a beneficiary’s spending on covered drugs reaches $2,000 in a year, Medicare will cover the remaining costs, ensuring that seniors are not overwhelmed by high medication expenses.

2. Expanded Access to Low-Income Subsidies

Starting in 2025, eligibility for the Low-Income Subsidy (LIS), also known as “Extra Help,” will be expanded. Previously, this subsidy was available only to individuals with incomes up to 150% of the federal poverty level. In 2025, the threshold will be increased to 200% of the federal poverty level, allowing more seniors to qualify for additional financial assistance. This expansion is expected to help millions of low-income seniors reduce their prescription drug costs even further.

3. Price Negotiations for High-Cost Drugs

Another major change is the implementation of Medicare’s ability to negotiate drug prices directly with pharmaceutical companies. Starting in 2025, Medicare will begin negotiating the prices of 20 high-cost drugs that are covered under Part D. This is a historic shift in policy, as Medicare has previously been prohibited from negotiating drug prices.

The drugs selected for negotiation will be among the most expensive and widely used by Medicare beneficiaries. The goal is to bring down the cost of these medications, resulting in lower premiums and out-of-pocket costs for beneficiaries.

4. Elimination of the Coverage Gap (Donut Hole)

The infamous “donut hole” in Medicare Part D coverage will be fully eliminated in 2025. This gap in coverage previously required beneficiaries to pay a higher percentage of their drug costs after their spending reached a certain limit until they qualified for catastrophic coverage. With the donut hole’s elimination, seniors will no longer experience a sudden increase in out-of-pocket costs, making drug costs more predictable and manageable throughout the year.

5. Enhanced Catastrophic Coverage

In conjunction with the out-of-pocket cap, changes to catastrophic coverage will also take effect. Once a beneficiary’s drug spending surpasses the $2,000 threshold, they will enter catastrophic coverage, where Medicare will cover 100% of the drug costs for the remainder of the year. Previously, beneficiaries were still required to pay 5% of their drug costs even in the catastrophic phase.

Impact on Beneficiaries

These changes are expected to have a profound impact on Medicare beneficiaries, especially those with chronic conditions who rely on expensive medications. The $2,000 out-of-pocket cap, in particular, is seen as a game-changer, as it will provide financial relief to millions of seniors who previously faced unlimited costs for their medications.

The expansion of the Low-Income Subsidy will also bring much-needed assistance to a broader range of seniors, ensuring that those with limited financial resources can afford their prescriptions.

To further assist Medicare recipients with large prescription drug costs until such time as they have reached their $2,000 annual maximum out-of-pocket, Medicare is implementing the MEDICARE PRESCRIPTION PAYMENT PLAN (M3P), also known as the “Smoothing” because it allows Medicare Part D beneficiaries to pay their of Out-of-Pocket Prescription Drug Costs Over the course of the Year.”

Elements of M3P:

- Monthly Installments: Starting in 2025, beneficiaries will have the option to spread out their out-of-pocket costs over the course of the year, rather than paying large sums at once when they fill prescriptions. This “smoothing” option is designed to make it easier for beneficiaries to manage their drug costs.

- All Part D members will be eligible to opt into the program for 1/1/2025, regardless of low-income status.

- Once opted into the program, members pay $0 at the pharmacy.

- The drug plan will pay the pharmacy the cost of the drug in full along inclusive of the member’s cost share. The Medicare recipient will then pay their drug cost in monthly installments, billed by the plan, over the course of the year, using the Center for Medicare Services (CMS) prescribed payment methodology.

As alluded to previously, these improvements in benefits will not be without consequences. While the 2025 changes to Medicare Part D are widely welcomed, they are not without controversy. In addition to potential increases in Part D and Medicare Advantage Part D premiums, some critics argue that the drug price negotiation process could lead to reduced access to certain medications if pharmaceutical companies decide to withdraw drugs from the Medicare program rather than negotiate lower prices. There are also concerns about the long-term sustainability of these reforms and their potential impact on the pharmaceutical industry’s ability to innovate.

Conclusion:

As 2025 approaches, Medicare beneficiaries should begin to familiarize themselves with these upcoming changes and how they may affect their prescription drug coverage. The enhancements to Medicare Part D reflect a broader effort to make healthcare more affordable and accessible for seniors, addressing long-standing issues in the system. While the full impact of these reforms will unfold over time, the changes in 2025 mark a significant step forward in improving the financial security and well-being of millions of Medicare beneficiaries.

For changes in covered and non-covered drugs, see Feature Article 1 below.

Please contact me directly with any questions or concerns as the details of changes to your current plan become available. I can help you review all the 2025 options available to you in the marketplace and would welcome you as a client. Remember, we can enroll in a new Part D Drug Plan for 2025 beginning 10/15/2024.

Donald Kenton Henry, Jr

Office: 281-367-6565

Text my cell 24/7 @ 713-907-7984

Email: Allplanhealthinsurance.com@gmail.com

Https://HealthandMedicareInsurance.com

Https://Allplanhealthinsurance.com

FEATURE ARTICLE 1:

Study Finds Drug Coverage Changes in Medicare Part D Plans

August 22, 2024

Avalere’s Kylie Stengel talks about the regional shifts in formularies and utilization management in Medicare Part D prescription drug plans.

The number of both the standalone prescription drug plans (PDP) and the low-income subsidy (LIS) benchmark plans in Medicare Part D decreased between 2023 and 2024, according to a new review from Avalere.

Of the 801 prescription drug plans offered in 2023 across the United States, 95 were no longer offered in 2024, which is a decrease of 12%. Additionally, almost half of Medicare beneficiaries enrolled in the low-income benchmark plans were in plans that lost benchmark status, meaning enrollees had to choose a new plan or pay a premium in 2024.

“We did see a reduction in the number of PDP offerings in general, but this is really a significant decrease in specifically the LIS benchmark plan offerings,” Kylie Stengel, associate principal at Avalere said in an interview. “We do believe that is due to the changing market conditions under the Inflation Reduction Act, although not all of the IRA changes are in effect as of yet. These changes together have changed how plans thought about their offerings for 2024.”

The Inflation Reduction Act’s $35 cap on insulin out-of-pocket costs went into effect in January 2023. Next year will see two important elements of the Inflation Reduction Act being implemented: a $2,000 cap on out-of-pocket costs under Part D and the Prescription Payment Plan, sometimes called the “smoothing” program, where beneficiaries with Medicare Part D drug coverage will have the option to pay out-of-pocket costs in monthly payments spread out over the year.

Medicare Part D provides prescription drug coverage to supplement traditional Medicare or Medicare Advantage plans. In 2023, more than 50 million of the 65 million Medicare beneficiaries were enrolled in Part D plans.

Seniors with low incomes are eligible for prescription drug coverage from plans that meet a certain benchmark for no additional premium costs. The benchmark is the maximum premium that the Medicare program will pay for drug plan coverage.

“The benchmark is an enrollment weighted average in each region,” Stengel said. “CMS takes the average of all bids from both PDP and Medicare Advantage plans and sets a premium amount by region.”

In its analysis, Avalere assessed data from the Part D Public Use Files for 2023 and 2024 from the Centers for Medicare and Medicaid Services. This data contains information about formulary, cost sharing, and utilization management for Medicare prescription drug plans.

Avalere researchers looked at coverage changes and focused on 24 of the most used, single-source branded drugs in five therapeutic categories: anticoagulants; asthma/chronic obstructive pulmonary disease (COPD) autoimmune; multiple sclerosis and pulmonary hypertension. Avalere, however, is not releasing the names of the drugs they analyzed.

Researchers conducted two sets of comparisons. In the prescription drug plans, they looked at. Changes in formularies from 2023 and 2024 and the differences for plans that exited the market. They also assessed the low-income benchmark plans for whether they maintained benchmark status and the differences in formularies in plans that lost and plans that maintained benchmark status.

“When you look under the hood, when you look at specific therapeutic areas and regions, there is a lot of variability,” Stengel said. “When you’re looking across all drugs at a national level, you might not see a lot of change.”

One of the biggest areas to see change was the coverage of drugs to treat patients with pulmonary hypertension. In 2023, 39% of plans covered the drugs for pulmonary hypertension. In 2024, just 30% of plans did.

Avalere also found regional differences in coverage for some therapeutic areas. For example, coverage of drugs to treat patients with multiple sclerosis was lower among plans that remained in the market in 2024 in 11 regions but higher in 13 regions.

Avalere found that cost-sharing changes were limited for autoimmune, multiple sclerosis, and pulmonary hypertension drugs. However, use of coinsurance for anticoagulants and drugs that treat patients with asthma/COPD increased substantially for all prescription drug plan comparisons.

For the low income subsidy benchmark plans, there were regional differences on the utilization management used for the anticoagulant drugs. In five regions, there was a 20-percentage-point or more difference in utilization management among plans that lost benchmark status compared with plans that maintained benchmark status.

“It’s hard to know what factors are driving this; we didn’t do an assessment in terms of why there might have been a decrease in coverage for some of these therapeutic areas. But pulmonary hypertension is an area with a lot of higher cost drugs so we thought might expect there to more changes,” Stengel said. “Plans might be reacting to the elimination of patient cost-sharing to reduce their financial risk.”

But she said it may be too early to predict plan offerings for 2025. “I think we can expect potentially there to be less enhanced plans in the market just because the overall the basic benefit is a richer compared with previous years.”

Leave a comment