Please correct me if I am wrong, but I recall that ever since President Obama took office in 2009–in the midst of the housing crisis; failed savings and loans and with the legacy of Enron still looming fresh in the memories of stockholders everywhere– he has said more government regulation through stricter laws and scrutiny (among a host of other burdensome and expensive supposed remedies) was necessary to protect the consumer and public in general. Now–in a narrative of unabashed hypocrisy his administration speaks out and intervenes to prevent Texas’s Governor Rick Perry from doing that very thing.

Perry directed the Texas Department of Insurance to establish strict rules to regulate Navigators trained to help Texans purchase health insurance under the Affordable Care Act (ACA). (These rules are outlined in our feature article below.) Remember – when you go through one these Navigators to enroll in an ACA compliant health plan for an effect date of January 1 – you will be required to divulge your income; your birth date; social security number; address; credit card and checking account information. Do you really want just anyone taking this information? Do you really want the person taking it to not be subject to criminal and financial background checks? Insurance agents licensed in the State of Texas are subject to all these requirements. Why would the administration which always argues for more protection of the individual from the misfeasance, malfeasance and just plain greed of the big corporations, e.g., health insurance companies – now be opposed to such? Why is this regulation so suddenly a liability? Please weigh in and help me understand this. The arguments presented by the fed below do not.

Admin. – Kenton Henry

****************************************************

Feature Article

The Texas Tribune

Wednesday, September 18, 2013

Perry Directs TDI to Regulate Federal Navigator Program

Gov. Rick Perry has directed the Texas Department of Insurance to establish strict rules to regulate so-called navigators trained to help Texans purchase health coverage under Obamacare.

While the governor says the extra regulations will ensure that people handling Texans’ private financial and health information are properly trained and qualified, the rules could present a significant roadblock to organizations helping to implement the federal Affordable Care Act.

“This is blatant attempt to add cumbersome requirements to the navigator program and deter groups from working to inform Americans about their new health insurance options and help them enroll in coverage,” Fabien Levy, a spokesman for the U.S. Department of Health and Human Services, said in an email.

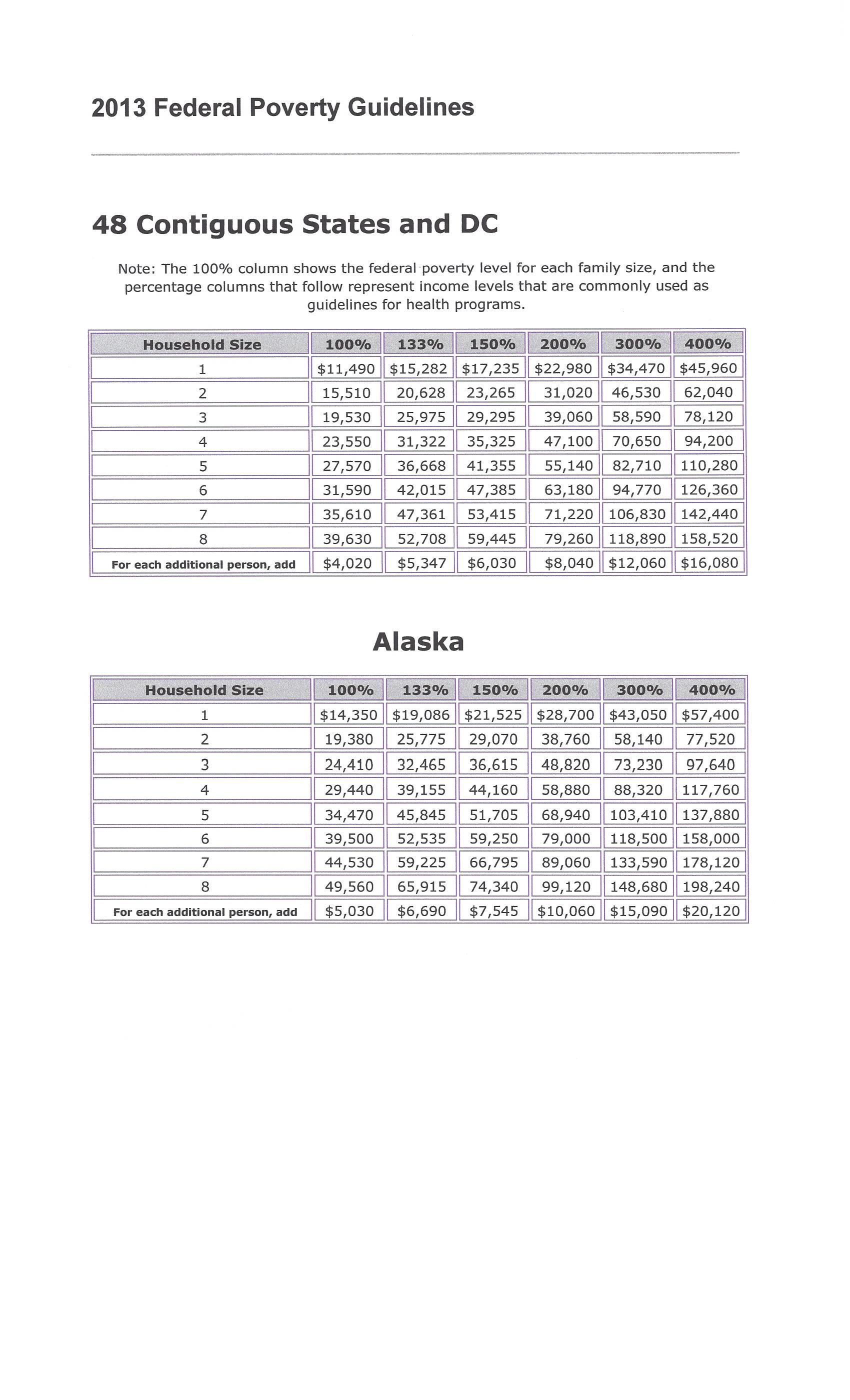

Along with many other provisions in President Obama’s signature health reform law, the individual mandate to purchase health insurance is set to take effect on Jan. 1. Texas’ Republican majority, which vehemently opposes the federal health law, declined to establish a state-based insurance marketplace. The federal government is doing it instead, launching an Orbitz-like online insurance exchange starting Oct. 1. That exchange will require individuals to input sensitive tax information, including their Social Security numbers and estimated annual income, to determine whether they qualify for tax credits to purchase coverage.

To help uninsured Texans use the complicated new system, the federal government awarded nearly $11 million in August to local organizations charged with hiring and training navigators, who will help consumers input their financial information and pick a health plan through in the exchange, must undergo 20 to 30 hours of training, pass a certification test and renew their certification annually, according to the U.S. Department of Health and Human Services.

For Perry, those ground rules are not enough.

“The U.S. Department of Health and Human Services has repeatedly delayed explaining how its navigators were going to be created, how they were going to operate and how they were going to be regulated,” Perry wrote in a letter to Insurance Commissioner Julia Rathgeber. “Because of the nature of navigators’ work and because they will be collecting confidential information, including birth dates, social security numbers and financial information, it is imperative that Texas train navigators on the collection and security of such data.”

In the letter, Perry specifically directed TDI to establish rules that require navigators to complete at minimum of 40 hours of state training in addition to the federal training requirements. He also demanded that navigators pass a rigorous exam based on that training, refrain from influencing a consumer’s insurance choice by recommending a specific plan or comparing benefits offered by different plans, and submit to periodic background and regulatory checks and show state identification while on the job.

He also directed TDI to maintain a database of registered navigators, including background checks and fingerprints; set limits on when and where navigators can enroll people in the exchange; charge fees to provide navigator training and registration; and establish the department’s authority to suspend or revoke navigators’ registration for failing to comply with state requirements.

“TDI agrees that the navigators in Texas have to be well trained and competent in what they’re doing,” said Ben Gonzalez, an agency spokesman. “Our goal is for them to be accountable and be conscientious about the confidential information that they’re going to be collecting.”

Federal officials said some of the rules Perry ordered the state insurance department to implement are forbidden under U.S. law. For example, navigators are not allowed to retain or report information on consumers who sign up for coverage through the exchange; therefore, they could not submit that information to TDI, as Perry has requested. The federal agency also emphasized that navigators are not allowed to access consumers’ information after it has been submitted to the exchange.

Levy said the U.S. government has similar programs already set up to help counsel people applying for Medicare, and that those have “never faced this kind of bullying from Texas.”

“This is clearly an ideologically-driven attempt to prevent the uninsured from gaining health coverage,” Levy said. “But despite the state’s attempts, we are confident that navigators will still be able to help Texans enroll in quality, affordable health coverage when open enrollment begins on Oct. 1.”

Given the governor’s directive, the department will begin putting together the rules with some urgency, Gonzalez added. The rule-making process can take several weeks, as the state is required to hold public meetings and solicit stakeholder input before the rules are drafted. After a draft is approved, the rules must be posted on the Texas Register to receive official comment before they can be codified.

“It’s our expectation the rules and training be in place by Jan. 1, when insurance can be purchased through the exchange,” Rich Parsons, a spokesman for the governor’s office, said via email.

The federal health exchange has a six-month open enrollment period — from Oct. 1 to March 31 — in which navigators can help the uninsured find health coverage to comply with the insurance mandate. Individuals who do not purchase insurance during the open enrollment period could be subject to federal tax penalties. If the state’s regulations take effect on Jan. 1, the navigators will be required to undergo additional training during the open enrollment period, which could present significant challenges.

To address the privacy concerns raised about the navigator program, some grant recipients are already requiring navigators to undergo additional training on privacy protection. United Way of Tarrant County, in collaboration with 17 other organizations, received $5.8 million, the largest federal navigator grant in Texas. Tim McKinney, the organization’s chief executive officer, said the organization is requiring navigators to undergo an additional hour-and-a-half of training on how to comply with the federal privacy law HIPAA.

Lawmakers signed off on Perry’s call for greater regulation of the navigator program in the last legislative session when they passed Senate Bill 1795, which authorizes TDI “to regulate navigators if it determined that federal standards did not ensure they were qualified to perform their duties or avoid conflicts of interest,” according to a legislative report. The new state law allows the department to enact rules that protect patient privacy and prohibit navigators from accepting payments from health insurance companies or posing as an insurance agent. At least 16 other states have also enacted or are considering laws to regulate navigators, according to a USA Today report.

Texas Attorney General Greg Abbott and 12 other state attorneys general have also raised concerns that the federal navigator program could pose risks to patients’ privacy. In a letter sent to U.S. Health and Human Services Secretary Kathleen Sebelius in August, the attorneys general asserted that the federal government’s screening process does not require uniform background or fingerprint checks, meaning convicted criminals or identity thieves could become navigators. They also expressed concerns that navigators would not undergo sufficient training.

Some medical professionals and advocates have objected to the privacy concerns raised by conservatives, suggesting they are politically motivated. For example, navigators must already comply with state and federal laws governing the privacy of sensitive medical information. If they do not adhere to strict security and privacy standards, including how to handle and safeguard consumers’ Social Security numbers and identifiable information, they are subject to criminal and civil penalties at both the federal and state level. The federal government imposes up to a $25,000 civil penalty for violating its privacy and security standards.

This story was produced in partnership with Kaiser Health News, an editorially independent program of the Henry J. Kaiser Family Foundation, a nonprofit, nonpartisan health policy research and communication organization not affiliated with Kaiser Permanente.

http://allplaninsurance.com