Op–Ed by D. Kenton Henry 01 October 2019 HealthandMedicare.com

VS.

VS.

I listened to the recent Democrat Presidential Primary Debates, as I listen to the daily sound bites in the media, as candidates try unabashedly to outdo each other. They do this in terms of the massive give-aways they promise us if elected in 2020. They promise these things not just to citizens, but everyone within the border of the United States. My incredulity, upon hearing such, exceeds even those bounds.

Their original promise is “free healthcare for all”. Healthcare free of premiums, deductibles, and copays. Medicare is the vehicle. To which I must ask myself, “Do these people even know the costs involved in Medicare?” “Do they really believe Medicare pays everything?” They would have you believe as much. They are counting on your naivety and lack of familiarity with the subject.

What makes Medicare a convenient and acceptable form of medical coverage for millions of people 65 and older (or disabled for 24 months or more) is it working in conjunction with private insurance plans. That, and thousands of licensed and “Certified” agents and brokers, helping to deliver comprehensive medical coverage at an affordable price. It is a hybrid package that provides as complete protection as available. The insurance plans would not exist without Medicare and, by itself, Medicare leaves the recipient/member exposed to significant liabilities.

Do these candidates, and the average voter know that in 2019:

A hospital admission requires the Medicare member to pay a $1,364 deductible each time they are admitted to the hospital as an inpatient for a separate medical condition, or the same medical condition separated by more than 60 days.

For days beyond 60, they pay $335 per day

Beyond day 90, they pay $682 per day

Eventually― say in the event of a stroke, paralysis, or being severely burned―they will pay all costs.

Part B Co-Insurance, Deductible and Premium

Relative to out-patient medical care, the Medicare member pays 20%, plus can be liable for excess charges above and beyond what Medicare deems “reasonable and customary”.

In addition, Medicare recipients pay an annual deductible of $185 for Medicare Part B (out-patient) medical care and a premium generally beginning at $135.50 per month and increasing to as high as $460.50. The latter depending on one’s adjusted gross income.

Perhaps most important, to take note of, in considering whether “Medicare For All” is even feasible, much less cost effective, is this. Medicare recipients have paid into the Medicare program their entire working careers via Medicare care taxes and payroll deductions. To qualify for Part A, (inpatient) coverage, they must have worked a minimum of 40 quarters or “buy in “with a premium as high as $422 per month.

So, you can see, Medicare is hardly free. And yet these candidates would have you believe it will be provided free of premiums, deductibles, and copays. (Now this is where even The Tooth Fairy raises her eyebrows!) It will be GIVEN, not to just those over 65, but to every man, woman, child, legal, and non-legal citizen or resident of the United States―whether they have paid a dime into the system or not.

Factor all that in and process this. Medicare now spends an average of about $13,600 a year per beneficiary, and in five years, the annual cost is expected to average more than $17,000, the report said.

According to CMS.gov (The Centers for Medicare & Medicaid Services ― refer to featured article 1 below*) The Medicare Board of Trustees predicts Medicare’s two trust funds, for Part A and Part B and D, respectively ― will go broke in 2026!

To put things in perspective, in 1960 there were about five workers for every Social Security beneficiary. The ratio of workers to beneficiaries fell to 3.3 in 2005 and then to 2.8 in 2016. It will decline further to about 2.2 by 2035, when most baby boomers will have retired, officials said.

The aging of the population is another factor in the growth of the two entitlement programs. The number of Medicare beneficiaries is expected to surge to 87 million in 2040, from 60 million this year, according to Medicare actuaries. And the number of people on Social Security is expected to climb to 90 million, from 62 million, in the same period.

The United States Treasury: U.S. Debt And Deficit Grow As Some See Government As The “Be–All and End–All”.

All this and the candidates would have you believe our government can provide free health care to everyone? When it can’t even provide it to our current citizens who have paid into the system their entire working lives! And who exactly is the government? “We The People”. We the tax payers. You and I. Even some of the candidates, admit the proposal will call for more taxes from the middle class. More? Really! One projected cost for Medicare For All is 39 trillion dollars over the first ten year period. The national debt is currently $22 trillion and took since the end of President Andrew Jackson’s administration (1837 and the last time the national debt was fully paid-off) to accumulate that! The combined wealth of all American households is less than $99 trillion. One can only conclude that “Medicare For All” would be a “Welfare System For All”. It would push our country into a socialist economic system to a depth from which it would be impossible to extricate itself.

As a new Medicare recipient, myself, I find the combination of the government program and private insurance working very well for myself and clients, from an insured standpoint. The program’s, and our nation’s, fiscal concerns are a more substantial matter and a topic for another time. With Medicare “Open Enrollment” a mere 15 days away, I can only say, “I hope whoever is President, and controls Congress, in future administrations―while providing a safety net for all American citizens―first and foremost, provides the capable, responsible, American taxpayer quality medical coverage―free of rationing of treatment and access to providers. At an affordable cost.”

D. Kenton Henry, editor HealthandMedicareInsurance.com, Agent, Broker

Email: Allplanhealthinsurance.com@gmail.com https://TheWoodlandsTXHealthInsurance.com https://Allplanhealthinsurance.com https://HealthandMedicareInsurance.com

************************************************************************************Featured article:

Centers for Medicare & Medicaid Services

Press release

Medicare Trustees Report shows Hospital Insurance Trust Fund will deplete in 7 years

Apr 22, 2019

Medicare Trustees Report shows Hospital Insurance Trust Fund will deplete in 7 years

Today, the Medicare Board of Trustees released their annual report for Medicare’s two separate trust funds — the Hospital Insurance (HI) Trust Fund, which funds Medicare Part A, and the Supplementary Medical Insurance (SMI) Trust Fund, which funds Medicare Part B and D.

The report found that the HI Trust Fund will be able to pay full benefits until 2026, the same as last year’s report.For the 75-year projection period, the HI actuarial deficit has increased to 0.91 percent of taxable payroll from 0.82 percent in last year’s report. The change in the actuarial deficit is due to several factors, most notably lower assumed productivity growth, as well as effects from slower projected growth in the utilization of skilled nursing facility services, higher costs and lower income in 2018 than expected, lower real discount rates, and a shift in the valuation period.

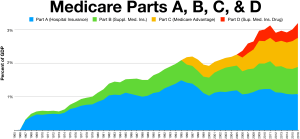

The Trustees project that total Medicare costs (including both HI and SMI expenditures) will grow from approximately 3.7 percent of GDP in 2018 to 5.9 percent of GDP by 2038, and then increase gradually thereafter to about 6.5 percent of GDP by 2093. The faster rate of growth in Medicare spending as compared to growth in GDP is attributable to faster Medicare population growth and increases in the volume and intensity of healthcare services.

The SMI Trust Fund, which covers Medicare Part B and D, had $104 billion in assets at the end of 2018. Part B helps pay for physician, outpatient hospital, home health, and other services for the aged and disabled who voluntarily enroll. It is expected to be adequately financed in all years because premium income and general revenue income are reset annually to cover expected costs and ensure a reserve for Part B costs. However, the aging population and rising health care costs are causing SMI projected costs to grow steadily from 2.1 percent of GDP in 2018 to approximately 3.7 percent of GDP in 2038. Part D provides subsidized access to drug insurance coverage on a voluntary basis for all beneficiaries, as well as premium and cost-sharing subsidies for low-income enrollees. Findings revealed that Part D drug spending projections are lower than in last year’s report because of slower price growth and a continuing trend of higher manufacturer rebates.

President Donald J. Trump’s Fiscal Year 2020 Budget, if enacted, would continue to strengthen the fiscal integrity of the Medicare program and extend its solvency. Under President Trump’s leadership, CMS has already introduced a number of initiatives to strengthen and protect Medicare and proposed and finalized a number of rules that advance CMS’ priority of creating a patient-driven healthcare system through competition. In particular, CMS is strengthening Medicare through increasing choice in Medicare Advantage and adding supplemental benefits to the program; offering more care options for people with diabetes; providing new telehealth services; and lowering prescription drug costs for seniors. CMS is also continuing work to advance policies to increase price transparency and help beneficiaries compare costs across different providers.

The Medicare Trustees are: Health and Human Services Secretary, Alex M. Azar; Treasury Secretary and Managing Trustee, Steven Mnuchin; Labor Secretary, Alexander Acosta; and Acting Social Security Commissioner, Nancy A. Berryhill. CMS Administrator Seema Verma is the secretary of the board.

The report is available at https://www.cms.gov/Research-Statistics-Data-and-Systems/Statistics-Trends-and-Reports/ReportsTrustFunds/index.html.

***************************************************************************************************

*Featured Article #2

Politics

Health insurers ramp up lobbying battle against Medicare-for-all

By Ana Radelat

The CT Mirror |

Aug 12, 2019 | 6:00 AM

Health insurers have joined forces with their longtime foe, the pharmaceutical industry, as well as partnering with the American Medical Association and the Federation of American Hospitals, to form a coalition to fight Medicare-for-all proposals and other Democratic plans to alter the nation’s health care.

As Democratic presidential candidates embrace changes to the nation’s health care system that could threaten Connecticut’s health insurers, the industry is hitting back.

Health insurers have joined forces with their longtime foe, the pharmaceutical industry, as well as partnering with the American Medical Association and the Federation of American Hospitals, to form a coalition to fight Medicare-for-all proposals and other Democratic plans to alter the nation’s health care.

The Partnership for America’s Health Care Future, funded by the insurance industry and its allies, is running digital and television ads aimed at undermining support for Medicare-for-all proposals and plans for a “public option,” a government-run health plan that would compete with private insurance plans.

The partnership was formed a little more than a year ago to protect the nation’s current health care programs, mainly the Affordable Care Act, Medicare and Medicaid.

[Politics] Returning home, Connecticut House members defend their support of impeachment inquiry »

The organization’s executive director, Lauren Crawford Shaver, said diverse groups in the coalition found a common cause in 2017 — opposing an attempt by congressional Republicans to repeal the Affordable Care Act.

“We came together to protect the law of the land,” she said.

That battle was won. Coalition members determined they should continue to band together to ward off other political dangers.

“There’s a lot of things we might fight about, but there’s a lot we can agree on,” Crawford Shaver said.

Sens. Bernie Sanders of Vermont and Elizabeth Warren of Massachusetts have called for a Medicare-for-all through a single-payer system, in which all Americans would be enrolled automatically in a government plan.

[Politics] Capitol Watch Podcast: As an older worker in Connecticut, what’s it like trying to find a new job? Here’s what we learned. »

Warren was among several candidates during the most recent Democratic debates who took aim at health insurers.

“These insurance companies do not have a God-given right to make $23 billion in profits and suck it out of our health care system,” she said.

Other candidates prefer a more modest approach, offering a “public option” or Medicare buy-in plan that would allow Americans to purchase government-run coverage, but unlike Medicare-for-all would not eliminate the role of private insurers.

That split among Democrats also runs through Connecticut’s congressional delegation, with Sen. Richard Blumenthal, D-Conn., and Rep. Jahana Hayes, D-5th District, endorsing Medicare-for-all plans and the other lawmakers supporting Medicare buy-in or public option plans.

The nation’s health insurers oppose all of the Democratic proposals discussed during the two nights of debates.

[Politics] Ghost gun ban, higher minimum wage and 9 other laws that go into effect Oct. 1 »

The insurers’ message is simple: The Affordable Care Act is working reasonably well and should be improved, not repealed by Republicans or replaced by Democrats with a big new public program. Further, they say, more than 155 million Americans have employer-sponsored health coverage and should be allowed to keep it.

Insurers also say that public option and Medicare buy-in plans would lead the nation down the path of a one-size-fits-all health care system run by bureaucrats in Washington D.C.

Advertisement

They say offering a public option or a Medicare buy-in would prompt employers to drop coverage for their workers and starve hospitals, especially those in rural areas, since government-run health plans usually reimburse doctors and hospitals less for medical services than private insurers. They also say Medicare-for-all and other Democratic proposals will lead to huge tax increases to pay for the plans.

“Whether it’s called Medicare for all, Medicare buy-in or the public option, the results will be the same: Americans will be forced to pay more and wait longer for worse care,” said Crawford Shaver.

The Partnership for America’s Health Care Future ran its first television ad on CNN just before and after the cable channel ran last week’s debates.

[Politics] Quinnipiac Poll shows growing support for impeaching Trump as news of whistleblower’s complaint sinks in »

The commercial showed several “ordinary Americans” at home and work decrying “one-size fits-all” health plans and “bureaucrats and politicians” determining care.

“We need to fix what’s broken, not start over,” the final speaker says.

Members of the Partnership for America’s Health Care Future have a lot of money and influence to wield on Capitol Hill. They spent a combined $143 million lobbying in 2018 alone, according to data from the Center for Responsive Politics.

And coalition members appear eager to spend even more lobbying money this year.

In the first six months of this year, America’s Health Insurance Plan, a health insurer industry group and member of the partnership, spent more than $5 million on lobbying expenses, and is on the way to surpassing the $6.7 million it spent in lobbying last year.

To underscore the health insurance industries’ importance to local economies, AHIP releases a state-by-state data book each year that details coverage, employment and taxes paid.

In Connecticut, the industry employs 12,296 workers directly and generates another 13,586 jobs indirectly, AHIP says. The payroll for both these groups of workers totals over $3.8 billion a year, AHIP says, and the average annual salary in the business is $112,770. The Connecticut Association of Health Plans puts the number higher, saying Connecticut has 25,000 direct jobs related to the health insurance industry, and another 24,000 indirect jobs.

AHIP also estimates that Connecticut collects nearly $200 million a year in premium taxes on health care policies sold in the state.

Connecticut’s reliance on health insurers – and their continuing influence – was on full display during the last legislative session when the insurance companies, led by Bloomfield-based Cigna, derailed

Leave a comment