a New Opportunity to Change Your Medicare Supplement Plan Without Health Questions

By D. Kenton Henry – editor, agent, broker

Dear Hoosier Clients and Friends,

Beginning January 1 of this year, Indiana implemented a new consumer protection commonly called the Medicare Supplement Birthday Rule. This new law provides Medicare beneficiaries with an important opportunity each year to change their Medicare Supplement (Medigap) plan without medical underwriting.

For many people, this means you may now be able to replace your current Medicare Supplement policy with a similar or lower-benefit plan and be guaranteed acceptance, regardless of health conditions.

What the Indiana Birthday Rule Allows

Under the new rule, eligible Indiana residents may apply for a replacement Medicare Supplement policy each year around their birthday, and the insurance company must approve the application if the required conditions are met.

This protection is intended to give policyholders a way to review and potentially reduce premiums while maintaining Medicare Supplement coverage.

Key Requirements to Qualify

To take advantage of Indiana’s Birthday Rule, the following conditions must be met:

1. You Must Currently Have a Medicare Supplement Policy

The rule applies only to individuals who are already enrolled in a Medicare Supplement (Medigap) plan.

2. You Must Be Replacing Your Plan With the Same or Lower Benefits

You may switch to another Medicare Supplement plan that offers equal or lesser benefits than your current policy. For example:

Plan G → another company’s Plan G

Plan G → Plan N

Plan F → Plan G

However, you cannot move to a plan with richer benefits under the Birthday Rule.

3. You Must Apply at Least 60 Days Before Your Birthday

Under Indiana’s new rule, the application signed and received date must be within 60 days from the applicant’s birthday. And the effective date must be on the first day of the month that is at least thirty (30) days after the signature date.

The replacement policy will become effective on the first day of your birthday month.

Medical Underwriting Is Waived

If the above conditions are met, the insurance company cannot deny your application due to health conditions.

Why This Rule Matters

Before this rule took effect, Medicare Supplement policyholders often had to undergo medical underwriting to change plans. That meant individuals with health conditions could be:

Declined for coverage

Charged higher premiums

Unable to change carriers

The Birthday Rule now provides an annual opportunity to review your coverage and potentially reduce premiums without having to answer health questions.

Should You Review Your Plan?

Even if you are satisfied with your current Medicare Supplement coverage, it may still be worthwhile to review your options. Insurance companies frequently adjust their pricing, and another carrier may offer the same plan benefits at a lower monthly premium.

The Birthday Rule allows you to explore those options without risking your coverage.

I Am Here to Help

If your current agent has not informed you of this opportunity, ask yourself, “Why?”

If your birthday is approaching and you would like to review your Medicare Supplement options under Indiana’s new Birthday Rule, please contact our office. I can help determine whether changing plans could benefit you.

Thank you for allowing me to continue assisting you with your Medicare coverage.

Sincerely,

D. Kenton Henry Office: 281.367.6565 Text my cell 24/7 @ 713.907.7984 Email: Allplanhealthinsurance.com@gmail.com Https://HealthandMedicareInsurance.com

Congratulations! You’ve worked hard, and now you’re turning age 65! Navigating through the myriad of solicitations you are receiving and the choices you have to cover the expenses not paid by Medicare can be overwhelming.

The first thing is what not to do!

DO NOT CALL AN 800 NUMBER and talk to some anonymous employee of an insurance company. Not only are they restricted to limiting you exclusively to their company’s options—but your personal information will be instantly sold and shared. Your phone is going to begin ringing off the hook!

I’ve been specializing in Medicare-related insurance for over thirty years, right here in The Woodlands, Texas, USA! I represent every Medicare-related product, including Supplement, Advantage, and Part D Drug plans, from virtually every “A” rated company doing Medicare-related business in Texas. And I CHARGE NO FEE for my services! Deal with a local agent/broker who values your business enough not to share it with anyone!

D. Kenton Henry Editor, Agent, Broker Office: 281.367.6565 Text my cell 24/7 @713.907.7984 Email: Allplanhealthinsurance.com@gmail.com

Editor, Broker, Agent – D. Kenton Henry TheWoodlandsTXHealthInsurance.com; HealthandMedicareInsurance.com

Each year, our Medicare Part D Drug Plan and Medicare Advantage Plan owe us our Annual Notice of Change (ANOC). Your plan is obligated to have it to us by September 30th. Resist the temptation to ignore it, AS MAJOR CHANGES ARE COMING OUR WAY!Your ANOC will arrive by U.S. mail along with dozens of solicitations for our Medicare insurance business. So, watch for it and review it carefully.

These changes are credited to the Biden “Inflation Reduction Act.” On the surface, they will undoubtedly benefit many seniors using prescription drugs. What remains to be seen are the consequences beneath the surface. The first is … at what cost (premium)? Your current plan’s 2025 premium will be in your ANOC. But we will have to wait until October 1 to know what the alternative plans will cost. This begs the question—because of the additional cost of these mandated improvements in benefits—will all these 30 different plans and their companies even remain in the marketplace? And what if yours doesn’t?

Let’s address the upcoming changes in benefits: We will begin with what your Medicare Part B premium to Medicare for Out-Patient Care will go to: For those earning less than $105,000 your premium will go to $185.00 (up from $174.70) For those in the highest income bracket, earning greater than $500,000 your premium will go to $628.90 (from $594.00) For every income block in between, couples filing jointly, and what Part D premiums to Medicare will go to, please click on this link and scroll down: https://www.irmaacertifiedplanner.com/2025-irmaa-brackets/

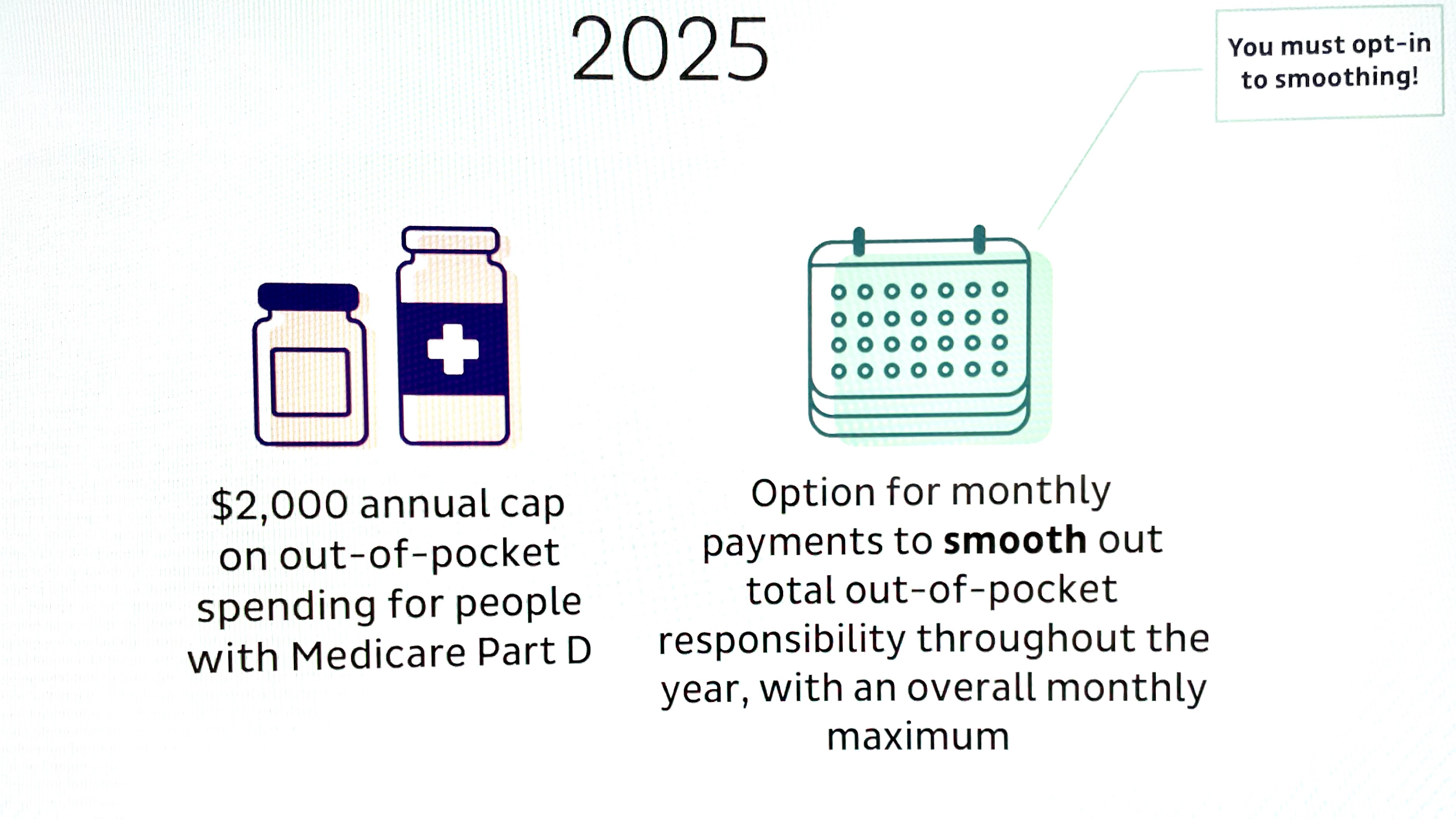

Relative to Medicare Part D Prescription Drug plans, as is the case in 2024, there is no beneficiary cost sharing above the annual OOP threshold. That will be $2,000 in 2025. That’s down from $8,000 in 2024!The coverage gap phase (also known as the “donut hole”) will be eliminated, which will result in standard Part D coverage consisting of a three-phase benefit: a deductible phase, an initial coverage phase, and a catastrophic phase. The annual Part D Drug Plan deductible caps at $590, up from $545 this year.

Here is how the changes take effect for the coming calendar years.

2025: The Inflation Reduction Act will lower out-of-pocket costs for Medicare Part D enrollees to a maximum of $2,000 per year. The Coverage Gap Discount Program will end and be replaced by the Manufacturer Discount Program. The standard Part D benefit design will also change to include three phases: deductible, initial coverage, and catastrophic coverage. The law will also require Part D plans to offer enrollees the option to pay for prescription drugs in capped monthly payments instead of all at once.

2027: Medicare will negotiate costs for 15 Part D drugs.

2028: Medicare will negotiate costs for 15 Part B and Part D drugs.

2029: Medicare will negotiate costs for 20 Part B and Part D drugs.

Every year after 2028: Medicare will negotiate costs for 20 Part B and Part D drugs.

IN REVIEW:

In 2025, Medicare Part D, the federal program that helps Medicare beneficiaries pay for prescription drugs, will undergo significant changes aimed at reducing out-of-pocket costs for seniors and improving access to necessary medications. These changes are part of the ongoing implementation of the Inflation Reduction Act (IRA) of 2022, which introduced sweeping reforms to the healthcare system, particularly in prescription drug pricing.

Key Changes in 2025

1. Introduction of a $2,000 Out-of-Pocket Cap

One of the most anticipated changes is the introduction of a $2,000 annual cap on out-of-pocket costs for prescription drugs under Medicare Part D. This cap will significantly ease the financial burden for many seniors who, in previous years, faced unlimited out-of-pocket expenses once they passed through the “donut hole” coverage gap.

This new cap means that once a beneficiary’s spending on covered drugs reaches $2,000 in a year, Medicare will cover the remaining costs, ensuring that seniors are not overwhelmed by high medication expenses.

2. Expanded Access to Low-Income Subsidies

Starting in 2025, eligibility for the Low-Income Subsidy (LIS), also known as “Extra Help,” will be expanded. Previously, this subsidy was available only to individuals with incomes up to 150% of the federal poverty level. In 2025, the threshold will be increased to 200% of the federal poverty level, allowing more seniors to qualify for additional financial assistance. This expansion is expected to help millions of low-income seniors reduce their prescription drug costs even further.

3. Price Negotiations for High-Cost Drugs

Another major change is the implementation of Medicare’s ability to negotiate drug prices directly with pharmaceutical companies. Starting in 2025, Medicare will begin negotiating the prices of 20 high-cost drugs that are covered under Part D. This is a historic shift in policy, as Medicare has previously been prohibited from negotiating drug prices.

The drugs selected for negotiation will be among the most expensive and widely used by Medicare beneficiaries. The goal is to bring down the cost of these medications, resulting in lower premiums and out-of-pocket costs for beneficiaries.

4. Elimination of the Coverage Gap (Donut Hole)

The infamous “donut hole” in Medicare Part D coverage will be fully eliminated in 2025. This gap in coverage previously required beneficiaries to pay a higher percentage of their drug costs after their spending reached a certain limit until they qualified for catastrophic coverage. With the donut hole’s elimination, seniors will no longer experience a sudden increase in out-of-pocket costs, making drug costs more predictable and manageable throughout the year.

5. Enhanced Catastrophic Coverage

In conjunction with the out-of-pocket cap, changes to catastrophic coverage will also take effect. Once a beneficiary’s drug spending surpasses the $2,000 threshold, they will enter catastrophic coverage, where Medicare will cover 100% of the drug costs for the remainder of the year. Previously, beneficiaries were still required to pay 5% of their drug costs even in the catastrophic phase.

Impact on Beneficiaries

These changes are expected to have a profound impact on Medicare beneficiaries, especially those with chronic conditions who rely on expensive medications. The $2,000 out-of-pocket cap, in particular, is seen as a game-changer, as it will provide financial relief to millions of seniors who previously faced unlimited costs for their medications.

The expansion of the Low-Income Subsidy will also bring much-needed assistance to a broader range of seniors, ensuring that those with limited financial resources can afford their prescriptions.

To further assist Medicare recipients with large prescription drug costs until such time as they have reached their $2,000 annual maximum out-of-pocket, Medicare is implementing the MEDICARE PRESCRIPTION PAYMENT PLAN (M3P), also known as the “Smoothing” because it allows Medicare Part D beneficiaries to pay their of Out-of-Pocket Prescription Drug Costs Over the course of the Year.”

Elements of M3P:

Monthly Installments: Starting in 2025, beneficiaries will have the option to spread out their out-of-pocket costs over the course of the year, rather than paying large sums at once when they fill prescriptions. This “smoothing” option is designed to make it easier for beneficiaries to manage their drug costs.

All Part D members will be eligible to opt into the program for 1/1/2025, regardless of low-income status.

Once opted into the program, members pay $0 at the pharmacy.

The drug plan will pay the pharmacy the cost of the drug in full along inclusive of the member’s cost share. The Medicare recipient will then pay their drug cost in monthly installments, billed by the plan, over the course of the year, using the Center for Medicare Services (CMS) prescribed payment methodology.

As alluded to previously, these improvements in benefits will not be without consequences. While the 2025 changes to Medicare Part D are widely welcomed, they are not without controversy. In addition to potential increases in Part D and Medicare Advantage Part D premiums, some critics argue that the drug price negotiation process could lead to reduced access to certain medications if pharmaceutical companies decide to withdraw drugs from the Medicare program rather than negotiate lower prices. There are also concerns about the long-term sustainability of these reforms and their potential impact on the pharmaceutical industry’s ability to innovate.

Conclusion:

As 2025 approaches, Medicare beneficiaries should begin to familiarize themselves with these upcoming changes and how they may affect their prescription drug coverage. The enhancements to Medicare Part D reflect a broader effort to make healthcare more affordable and accessible for seniors, addressing long-standing issues in the system. While the full impact of these reforms will unfold over time, the changes in 2025 mark a significant step forward in improving the financial security and well-being of millions of Medicare beneficiaries.

For changes in covered and non-covered drugs, see Feature Article 1 below.

Please contact me directly with any questions or concerns as the details of changes to your current plan become available. I can help you review all the 2025 options available to you in the marketplace and would welcome you as a client. Remember, we can enroll in a new Part D Drug Plan for 2025 beginning 10/15/2024.

Donald Kenton Henry, Jr

Office: 281-367-6565 Text my cell 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com Https://HealthandMedicareInsurance.com Https://Allplanhealthinsurance.com

FEATURE ARTICLE 1:

Study Finds Drug Coverage Changes in Medicare Part D Plans

Avalere’s Kylie Stengel talks about the regional shifts in formularies and utilization management in Medicare Part D prescription drug plans.

The number of both the standalone prescription drug plans (PDP) and the low-income subsidy (LIS) benchmark plans in Medicare Part D decreased between 2023 and 2024, according to a new review from Avalere.

Of the 801 prescription drug plans offered in 2023 across the United States, 95 were no longer offered in 2024, which is a decrease of 12%. Additionally, almost half of Medicare beneficiaries enrolled in the low-income benchmark plans were in plans that lost benchmark status, meaning enrollees had to choose a new plan or pay a premium in 2024.

“We did see a reduction in the number of PDP offerings in general, but this is really a significant decrease in specifically the LIS benchmark plan offerings,” Kylie Stengel, associate principal at Avalere said in an interview. “We do believe that is due to the changing market conditions under the Inflation Reduction Act, although not all of the IRA changes are in effect as of yet. These changes together have changed how plans thought about their offerings for 2024.”

The Inflation Reduction Act’s $35 cap on insulin out-of-pocket costs went into effect in January 2023. Next year will see two important elements of the Inflation Reduction Act being implemented: a $2,000 cap on out-of-pocket costs under Part D and the Prescription Payment Plan, sometimes called the “smoothing” program, where beneficiaries with Medicare Part D drug coverage will have the option to pay out-of-pocket costs in monthly payments spread out over the year.

Medicare Part D provides prescription drug coverage to supplement traditional Medicare or Medicare Advantage plans. In 2023, more than 50 million of the 65 million Medicare beneficiaries were enrolled in Part D plans.

Seniors with low incomes are eligible for prescription drug coverage from plans that meet a certain benchmark for no additional premium costs. The benchmark is the maximum premium that the Medicare program will pay for drug plan coverage.

“The benchmark is an enrollment weighted average in each region,” Stengel said. “CMS takes the average of all bids from both PDP and Medicare Advantage plans and sets a premium amount by region.”

In its analysis, Avalere assessed data from the Part D Public Use Files for 2023 and 2024 from the Centers for Medicare and Medicaid Services. This data contains information about formulary, cost sharing, and utilization management for Medicare prescription drug plans.

Avalere researchers looked at coverage changes and focused on 24 of the most used, single-source branded drugs in five therapeutic categories: anticoagulants; asthma/chronic obstructive pulmonary disease (COPD) autoimmune; multiple sclerosis and pulmonary hypertension. Avalere, however, is not releasing the names of the drugs they analyzed.

Researchers conducted two sets of comparisons. In the prescription drug plans, they looked at. Changes in formularies from 2023 and 2024 and the differences for plans that exited the market. They also assessed the low-income benchmark plans for whether they maintained benchmark status and the differences in formularies in plans that lost and plans that maintained benchmark status.

“When you look under the hood, when you look at specific therapeutic areas and regions, there is a lot of variability,” Stengel said. “When you’re looking across all drugs at a national level, you might not see a lot of change.”

One of the biggest areas to see change was the coverage of drugs to treat patients with pulmonary hypertension. In 2023, 39% of plans covered the drugs for pulmonary hypertension. In 2024, just 30% of plans did.

Avalere also found regional differences in coverage for some therapeutic areas. For example, coverage of drugs to treat patients with multiple sclerosis was lower among plans that remained in the market in 2024 in 11 regions but higher in 13 regions.

Avalere found that cost-sharing changes were limited for autoimmune, multiple sclerosis, and pulmonary hypertension drugs. However, use of coinsurance for anticoagulants and drugs that treat patients with asthma/COPD increased substantially for all prescription drug plan comparisons.

For the low income subsidy benchmark plans, there were regional differences on the utilization management used for the anticoagulant drugs. In five regions, there was a 20-percentage-point or more difference in utilization management among plans that lost benchmark status compared with plans that maintained benchmark status.

“It’s hard to know what factors are driving this; we didn’t do an assessment in terms of why there might have been a decrease in coverage for some of these therapeutic areas. But pulmonary hypertension is an area with a lot of higher cost drugs so we thought might expect there to more changes,” Stengel said. “Plans might be reacting to the elimination of patient cost-sharing to reduce their financial risk.”

But she said it may be too early to predict plan offerings for 2025. “I think we can expect potentially there to be less enhanced plans in the market just because the overall the basic benefit is a richer compared with previous years.”

In addition to owning the first insurance agency in The Woodlands, Texas, and most of the United States, to create a website (Allplaninsurance.com) in 1995, I was among the first to offer Medicare Advantage and Medicare Part D Prescription Drug Plans (MAPD plans) to Medicare recipients following their creation by the Medicare Modernization Act of 2003. Congress created them to provide a lower premium insurance product as an alternative to Medicare Supplement policies, which has been the standard insurance product to serve as secondary insurance covering medical expenses not paid by Original Medicare. And—with premiums as low as $0—they have certainly done that. Contrary to what may be the common perception of the public, every good agent has a little bit of social worker in them and wants to think they have really helped a person and improved their situation. As an agent (before the advent of Medicare Advantage plans), I would sit across coffee tables from prospective clients living in single-wide trailers and subsisting on social security income alone. I would watch tears come in their eyes as they told me they simply did not have another dime to spend on insurance, leaving me to drive off and them no better off for my visit. So, from that standpoint, they have been a source of great relief for me as well as my clients.

In addition to lower premiums, MAPD plans offer other advantages. Specifically, they are:

The convenience of combining medical coverage with prescription drug coverage under the cover of one policy. Effectively eliminating the necessity of paying a second premium for the latter.

The provision of “extra” benefits such as dental, vision, and hearing benefits

“Guaranteed Approval” during the Annual Election Period October 15th and December 7th and the option of changing your plan each January 1 as the plans and your needs change.

Premiums are not age-based and do not increase due to age as one gets older.

Seniors are inundated with seemingly endless television and radio commercials promoting Medicare Advantage plans ad infinitum. But while they drive home the advantages mentioned above, they virtually never mention the disadvantages or compromises that come with electing them over a Medicare Supplement policy. There are many reasons for this, but this is the one most relevant to you:

Medicare, like Social Security, is hemorrhaging dollars. Please don’t take it from me. Google it. Financial prognosticators project it will enter a default position by 2031. Medicare trustees say the Part A (Hospital and Skilled Nursing coverage) program will begin running deficits again in 2025, drawing down the trust fund until it depletes in 2031. After that date, the program will not bring in enough money to fully pay out Part A benefits. *(See Feature Article 2 below.)

Now, we all know our government will just tax us more, and our treasury will print enough more money to keep things going. But the bottom line is that Medicare is seeking any way of saving money and limiting its losses. The easiest way to do this is to lower its share of claims. The easiest way to lower its share of claims is to increase enrollment in Medicare Advantage plans relative to Medicare Supplement. And why is that?

Opposed to Supplement, Advantage plans . . .

1)Force the insured member to share in more expenses as the medical claims come in.

2) They influence the member to utilize a limited network of providers or pay a higher cost for not.

3) They subject the member to preauthorization of medical tests and procedures, often resulting in significant delays in treatment. *(See Feature Article 1, 2 and 3 below.)

4)Advantage plans that combine prescription drug coverage with medical coverage (MAPD plans) lock the member into a drug plan that may not provide the lowest total cost for drugs or cover them in the first place.

5)Once a member foregoes Medicare Supplement in favor of an Advantage plan beyond 12 months, they may find themselves locked into an Advantage plan—and out of a Medicare Supplement plan—due to preexisting medical conditions for the remainder of their lives.

One reason for these differences in how things are covered is that when a person elects Medicare Advantage, their benefits and administration are assigned to the insurance plan and company issuing it and away from Medicare. Medicare no longer plays a role in your coverage. As Advantage plans are allocated a limited amount of dollars per plan member, the companies will seek to limit expenditures. Recent adjustments in budgets for the plans will result in more of this. *(See Feature Articles below.)

And now, we learn that in addition to the increasing number of denials for tests and procedures by Advantage plans, Medicare is allocating less money to cover benefits, resulting in an actual reduction in benefits in 2025. Depending on the Medicare Supplement plan option (A-N) one elects, these compromises seldom, if ever, apply to their coverage.

All this being said, we get back to affordability and the reality that Medicare Supplement premiums will increase due to the member’s age as the member ages. This could bring me back to that coffee table where clients simply can no longer afford their premiums. While their costs for treatment may increase, some will need a lower premium to afford some type of coverage. Those people should know I offer Medicare Advantage plans from virtually every major carrier in one’s county or region. These include (among others) Aetna, Anthem, AARP Unitedhealthcare, BlueCross BlueShield, Cigna, Kelseycare Advantage, and Wellcare.

Regardless of your situation, I offer whatever product is appropriate and best suited to meet your Medicare-related insurance needs. When you work with me, I will be an advocate on your behalf. I represent you over the insurance company. Yes, I still have a little bit of social work in me.

Please get in touch with me. I am waiting to answer your questions and assist you with your coverage.

Hospitals’ Medicare Advantage problem hits an inflection point

Jakob Emerson – 5 April 2024

The tensions between hospitals and Medicare Advantage plans continue to grow. With the program hitting nearly 34 million enrollees in March, paired with recent policy moves by the federal government, the scene has been set for those relations to worsen.

“The relationship between hospitals and managed care is strained at best right now,” Chip Kahn, president and CEO of the Federation of American Hospitals, told Becker’s. “[Insurers] are finding every way to not pay for the care that Medicare beneficiaries should receive. I don’t know how the issue gets worse — we’re at a critical stage, and I think CMS is sending those signals.”

On April 1, CMS finalized a slight decrease in MA benchmark payments for 2025. The agency has also issued more strict prior authorization rules this year and cracked down on when MA plans must cover inpatient care.

The health insurance industry has said the new rates will “put even more pressure on the benefits and premiums” of MA beneficiaries, a warning that individual insurers have also issued in recent months.

“Payers know that they’re going to have to cut supplemental benefits, and premiums may even have to go up, but I wouldn’t want to be the first one to do it,” Scott Ellsworth, founder and president at Ellsworth Consulting, told Becker’s. Mr. Ellsworth is a former insurance executive, overseeing entire divisions at Centene, Optum and a BCBS plan throughout his career.

“Seniors have seen their benefits get better every year, but now we’re at an inflection point and the free lunch is over,” he said. “There is going to be a sharing of the pain. Providers have disproportionately shared the pain and now you’re seeing many of them say ‘enough is enough, we’re out.'”

In 2023, Becker’sreported on at least 15 hospitals and health systems nationwide that dropped some or all of their Medicare Advantage contracts. Among the most commonly cited reasons are excessive prior authorization denial rates and slow payments from insurers. Some systems have noted that most MA carriers have faced allegations of billing fraud from the federal government and are being probed by lawmakers over their high denial rates.

“It’s become a game of delay, deny and not pay,” Chris Van Gorder, president and CEO of San Diego-based Scripps Health, told Becker’s in September. “Providers are going to have to get out of full-risk capitation because it just doesn’t work — we’re the bottom of the food chain, and the food chain is not being fed.”

Scripps terminated MA contracts in January for its integrated medical groups, citing an annual loss of $75 million on its contracts with insurers.

In March, Bristol (Conn.) Health announced it was eliminating 60 positions, 21 of which are occupied and will result in layoffs. Its CEO, Kurt Barwis, laid blame on Medicare Advantage saying, “All the nice-to-haves are being taken out by the lack of insurance payment and the lack of reimbursement.”

In January, the Healthcare Financial Management Association released a survey of 135 health system CFOs, which found that 16% of systems are planning to stop accepting one or more MA plans in the next two years. Another 45% said they are considering the same but have not made a final decision. The report also found that 62% of CFOs believe collecting from MA is “significantly more difficult” than it was two years ago.

“Medicare Advantage net reimbursement right now is terrible for hospitals — our clients average about 85 cents on the dollar, and it’s only getting worse,” Mr. Ellsworth said. “MA is a race to the bottom, and I would argue that we’ve hit that bottom. Payers are going to struggle with this too, but no one wants to be the first to blink.”

Medicare Advantage denials increased almost 56% for the average hospital from January 2022 to July 2023, according to data from a joint American Hospital Association and Syntellis report. The denials and inconsistent reimbursement led to a 28% drop in hospital cash reserves.

Both Mr. Ellsworth and Mr. Kahn noted that it isn’t feasible for most health systems to completely walk away from Medicare Advantage, given that it now makes up more than half of the Medicare population. Instead, many hospitals are paring down contracts and looking for payer partners that align best with their financial objectives. Some systems are even exploring launching their own MA plan built in tandem with one insurer. Others have partnered with grocers or other health systems.

“We will ultimately pick a couple of partners going forward, and I think a lot of health systems are going to do this,” Will Bryant, CFO of Chapel Hill, N.C.-based UNC Health, told Becker’s in November. “They’re going to be the partners who act like partners and not who deny care in order to bolster their billions of dollars of quarterly earnings.”

Sachin Jain, MD, CEO of SCAN Group — one of the nation’s largest nonprofit Medicare Advantage companies — cautioned hospitals that dropping MA plans is a short-term trend that is “going to backfire in a big way for these large health systems.”

“You’re a nonprofit system saying you’re no longer going to accept the insurance that low-income people actually have,” he said. “We’ll see how that works out for you.”

Dr. Jain said any public policy program is going to create unintended consequences, adding, “What I would say to anybody who’s critical about the program is that you’re right, but let’s fix that.”

Former CMS Administrator Don Berwick, MD, toldBecker’s in February that the battle between hospitals and Medicare Advantage is a “manifestation of an underlying broken system in which everyone that gives care wants to give more, and everyone that pays for care wants to pay less.”

“To me, the untold story yet is about the physicians and nurses who don’t feel directly tied to ongoing Medicare Advantage trends, but they are certainly immersed in a changing financial landscape,” Dr. Berwick said. “As venture capital, private equity and ownership of healthcare by private interests increases, it changes their worlds, what it’s like to practice, their feelings about themselves, and the degrees of freedom they have to care for their patients. That chicken is going to come home to roost.”

Despite the tensions with hospitals, the MA program has bipartisan support in Congress and a 95% quality satisfaction rating among enrolled members in 2023. There are about 4,000 MA plans being offered this year nationwide, and MA members spend an average of $2,434 less on out-of-pocket costs and premiums per year compared to traditional Medicare enrollees.

“Medicare Advantage is very important, especially for low-income seniors,” Mr. Ellsworth said. “Hospitals need to acknowledge the reimbursement problem and proactively address their relationships [with payers] head-on.”

The fund covering Medicare‘s hospital-insurance benefits is now projected to run out of money in 2031, according to a new report by Medicare trustees.

This new insolvency date gives policymakers three more years than previously estimated to address impending financial setbacks that are facing the social safety net program, which provides health care benefits to tens of millions of Americans.

The ultimate insolvency date will likely change, the trustees say, due to difficulties in accurately projecting program expenditures. That leaves the exact timeline unclear for lawmakers to hash out a plan to mend Medicare’s finances, which could require an increase in taxes, a cut in benefits or a combination of both to keep benefits paying out in full.

What the report says

In a report released Friday, Medicare’s Board of Trustees provided the latest snapshot of the program’s finances. On the whole, Medicare is on sounder financial footing than indicated in last year’s trustee report, though financial shortfalls still loom.

Medicare hospital insurance benefits, aka Medicare Part A, are expected to fully pay out until 2031, a three-year improvement from the last trustee report.

Medicare Part B and Part D do not face insolvency, the report said, because they are funded separately — partially by premiums and general revenue from the U.S. Department of the Treasury. These benefits help cover typical health-insurance and prescription-drug expenses, respectively.

By contrast, Medicare Part A, which generally covers inpatient hospital care, skilled-nursing facility care, home-health care and hospice care, uses a separate reserve that’s funded by a 2.9% Medicare payroll tax. This is the trust fund at risk of insolvency.

In 2022, Medicare’s balance sheet looked better than previous years, the report shows. The hospital-insurance trust fund had a surplus of $54 billion, and Medicare overall brought in about $84 billion more than it paid out.

Nearly every year since 2008, the Part A trust fund has run a deficit, the report notes, with the exception of 2021 and 2022. The fund ran a steep shortfall in 2020 of more than $60 billion, largely because Medicare began making loans to health care providers to increase their cash flow as they grappled with the COVID-19 crisis. Then in 2021, providers began to repay Medicare, leading to the current surpluses.

The surpluses aren’t expected to last, however. Medicare trustees say the Part A program will begin running deficits again in 2025, drawing down the trust fund until it depletes in 2031. After that date, the program would not be bringing in enough money to fully pay out Part A benefits.

Key context

Medicare covered 65 million Americans last year. The vast majority of those people, about 88%, were 65 or older, though the program also provides health coverage to millions of disabled Americans.

Medicare — particularly Part A — has long faced financial issues. The nation’s changing demographic makeup is a big reason why. Because Medicare Part A relies on payroll taxes, it is more susceptible to insolvency when a growing share of the population is older, ultimately changing the worker-to-beneficiary ratio. In other words: less money coming in and more money going out. These demographic changes are also leading to insolvency issues for Social Security.

Compared to Social Security, projections for Medicare’s insolvency are less certain because it’s difficult for the trustees to accurately predict future health care expenditures. This can lead to some larger swings in the predicted insolvency date. By contrast to the trustee’s estimate, the Congressional Budget Office estimates the fund will remain solvent until 2033.

According to the nonprofit Center on Budget and Policy Priorities (CBPP), if Medicare Part A went insolvent, it would still be able to pay out almost all benefits. This leads some experts to call for tempered reactions to the newly projected insolvency date.

“Medicare does not face a financing ‘crisis’ and is not ‘bankrupt,’ as some critics charge,” tweeted Paul Van de Water, a senior fellow at the CBPP who specializes in Medicare. “Even if policymakers took no further action … tax revenues would still cover 89 percent of scheduled benefits” after the insolvency date.

Avoiding Medicare insolvency

Policymakers have several options to avoid impending insolvency headed for Medicare Part A. The trustees note two options that could immediately solve the issue:

The standard 2.9% payroll tax could be immediately raised to 3.52%, which would be enough to plug any financial shortfalls over the next 75 years.

In lieu of a tax increase, expenditures (read: benefits) would need to be reduced immediately by 13%, the trustees say.

Realistically, a combination of the two could work and the benefits cuts and/or tax increases could be implemented over a longer period of time.

Additionally, President Joe Biden released a plan last month to push the insolvency date back by 25 years.

The central change under the president’s plan would be a Medicare payroll tax increase on Americans earning more than $400,000.

Currently, earnings over $200,000 for individuals are taxed at 3.8% (while income under that amount is taxed at the standard 2.9% rate). These rates are split 50-50 between employees and employers.

The president’s plan introduces a new tier for income over $400,000, a tax rate of 5%.

The president’s Medicare proposal — part of a larger 2024 budget plan — is not expected to make it through the Republican-controlled House of Representatives.

Dozens of health systems ask CMS to crack down on Medicare Advantage Denials

Becker’s Hospital CFO Report

Rylee Wilson – Friday, March 22nd, 2024

Over 100 hospitals, health systems and providers signed on to a call for CMS to do more on Medicare Advantage denials.

Members of Premier, a healthcare services company, penned a letter to CMS administrator Chiquita Brooks-LaSure on March 21, requesting CMS collect more data on claims denied by Medicare Advantage plans and take enforcement action against plans not following the coverage rules set out by Medicare.

A survey of Premier’s member hospitals and health systems found 15% of claims to private payers are denied. A slightly higher portion of Medicare Advantage claims, 15.7%, are denied, according to the survey.

On average, hospitals spend $47.77 in administrative costs to appeal a denied Medicare Advantage claim, according to the Premier survey.

In the letter, the health systems asked CMS to monitor how much MA plans spent on direct patient care to address “potentially dire impacts on Medicare beneficiaries and providers.”

“It is imperative that CMS leverage its full authority to ensure that MA plans’ medical loss ratio (MLR) requirements for revenue used for patient care are satisfied in alignment with the benefits to which Medicare beneficiaries are entitled,” the providers wrote.

Dozens of health systems signed the letter, including CommonSpirit Health, Ascension, Advocate Health, AdventHealth and Providence.

The providers also asked CMS to bar MA plans from delaying or denying claims approved through electronic prior authorization and weight patient experience more heavily in its ratings of MA plans.

A growing number of hospital executives have criticized Medicare Advantage, often citing excessive prior authorization hurdles and delayed payments. A handful of systems have moved to drop the program entirely.

FEATURE ARTICLE 3

Nearly 15% of claims submitted to private payers are initially denied

Nearly 15% of medical claims submitted to private payers for reimbursement are initially denied, according to new survey data released Thursday.

Denied claims are more prevalent for high-cost treatments, with the average rejected charges at $14,000 and up, Premier Inc. reported. Medicare Advantage and other private payers eventually overturned more than half (54%) of denials, with the claims paid, but only after “multiple, costly rounds of provider appeals.”

The findings are from a national survey of hospitals, health systems and post-acute providers, conducted by the Charlotte-based healthcare improvement company.

“To address these potentially dire impacts on Medicare beneficiaries and providers, we urge CMS to stringently monitor MA plans’ reporting of expenditures on direct patient care,” Premier and 118 member organizations wrote in a March 21 letter to the head of the Centers for Medicare & Medicaid Services. “It is imperative that CMS leverage its full authority to ensure that MA plans’ medical loss ratio requirements for revenue used for patient care are satisfied in alignment with the benefits to which Medicare beneficiaries are entitled.”

Premier partnered with member hospitals to conduct the survey from October to December 2023. A total of 516 hospitals across 36 states, representing 52,123 acute care beds responded. Answers were based on claims submitted to private payers in 2022.

On average, hospitals and other providers incurred a cost of $43.84 per claim to fight denials. With insurers processing about 3 billion claims per year, this equates to $19.7 billion per year in expenses for these reviews. An average of about 3% of all claims denied included those that were already preapproved via prior authorization, Premier noted.

The continued burden from these delays and denials has impacted hospital finances. During the past year, average days of cash on hand at hospitals declined by 44 days or 17%. Meanwhile, days of cash on hand increased among insurers such as UnitedHealth Group (up 25.5% on average since 2019) and Cigna (24.4% on average).

The letter writers—who included numerous large health systems and other provider organizations—want CMS to take enforcement action against MA plans that “fail to abide by the coverage rules of Medicare.”

“Additionally, we note that CMS has moved away from holding MA plans accountable for [Consumer Assessment of Healthcare Providers and Systems] and other patient experience measures in recent rulemaking by reducing the weighting of patient experience and access measures in the Star Ratings program. We recommend that CMS return to its past policy of weighting patient experience and access measures more heavily in the MA Star Ratings methodology, empowering beneficiaries to hold their health plans financially accountable,” the letter stated.

The analysis does not specifically mention radiology services, but it mirrors ongoing problems imaging providers have had with prior authorization and the No Surprises Act (links to previous coverage below).

*(IF YOU WATCH TV, YOU HAVE SEEN THE HIGH-PROFILE COMMERCIALS FOR THESE DRUGS. IF YOU’VE BEEN PRESCRIBED ANY OF THEM, YOU KNOW HOW HIGH THE COST CAN BE. FOR MANY, PROHIBITIVELY SO. FOR DETAILS ON HOW RELIEF MAY BE COMING, PLEASE READ THE FEATURE ARTICLE AT THE BOTTOM OF MY OWN JUST BELOW.)

IT’S ALMOST TIME TO RE-SHOP YOUR MEDICARE ADVANTAGE AND DRUG PLAN FOR 2024

By D. Kenton Henry, editor, broker, agent

6 September 2023

With the Labor Day holiday behind us, summer is virtually over. And, the coming of fall brings Medicare’s Annual Election Period (AEP). For those new to Medicare, and as a reminder to those recipients who are not, this period runs from each fall. Beginning October 1, we can preview the new Medicare Advantage and Part D drug plans to determine which, if any, is superior to our current plan, and from October 15 to December 7, enroll in it. Our new plan selection will go into effect on January 1. Of course, if your current plan remains your best option, you need not do a thing, and it will roll right over into the new year. Simply continue to pay your premium.

But how will you know if a superior Medicare Advantage or Part D Drug plan exists for you in the coming year? First, your current drug plan owes you an Annual Notice Of Change (AOC). It must come in your U.S. mail by September 30. If they do not send it, they violate Medicare regulations. So be sure to watch your mail closely. I know we are all being inundated with advertisements this time of year in a frenzied attempt to garner our business, but sort through it long enough to find your AOC!

Then, please review it carefully. While it may remain virtually the same in the coming year, something inevitably changes. Be it the premium, the copays, the out-of-pocket maximum, the doctors and hospitals, or the drugs. Once you are aware of any changes, you must compare your plan to all the new plans in the new year. Or – you may simply call me. I have been in the medical insurance industry since 1986, specializing in Medicare-related insurance and Under Age 65 Individual and Family health insurance. As I and my clientele have grown older, I have focused even more on assisting Medicare recipients.

Researching and identifying a plan that is in my client’s best interest and making my recommendation is an annual service I provide them. While some can do it independently, my familiarity with all the options and the mechanisms for exploring and enrolling in them is so great that many find it easier to sit back and let me do the research for them. Then, if they agree with my recommendation, I am happy to enroll them, making the process go as quickly and smoothly as possible. There is no obligation to take my recommendation, nor is there any fee charged by me whether one does or doesn’t. Should you enroll through me, you will be charged no more for the product than if you walked through the front door and acquired it directly from the insurance company offering it. So I believe you get the benefit of my 37 years of experience in the market at no cost to you. While Medicare requires that I inform you, no one agent can represent every company and plan in the market, I do represent most. I have diligently researched which plans I believe will be most competitive for most people’s purposes and have studied and certified (tested) to be able to insure you with them. And more importantly, I have reviewed all of them relative to your needs before making my recommendation. On the rare occasion I am not appointed (contracted) with a company in your best interest, I will recommend them just the same and encourage you to enroll with them and advise you how to go about that. I do so in the hopes that it will begin a relationship with you and that – next year – I may be appointed with the company with which you wish to enroll.

So, while the leaves don’t fall much around here in October, they do turn brown. And Joe Willy Namath and J.J. Walker will soon be annoying you with their incessant and infernal commercials. Let these things remind you to call me for the answers to your Medicare-related questions and any guidance you would like. Remember, there is no cost to you for such, and, at the very least, you’ll know you are doing everything right and make another friend in the process.

Oh – again! Please read my feature article, which appears directly below this. The current administration is attempting to lower drug costs for Medicare recipients by allowing Medicare to negotiate lower drug prices, for the first time, with pharmaceutical companies. The article identifies 10 of the most expensive drugs they target for lower costs. If you, like me, have been exposed to the never-ending drug commercials accompanying your television programs, you probably can already guess what some of them are. Obviously, advertising works, and the companies must pay for it somehow!

Drugs Up for Medicare Price Cuts Fuel Drugmakers’ Legal Strategy

Ian Lopez: Senior Reporter

Nyah Phengsitthy: Reporter

Drugmakers are poised to change their lawsuits and bring new ones against the Biden administration now that the list of the first 10 drugs subject to Medicare price negotiations is out.

Bristol-Myers Squibb Co., Johnson & Johnson, and other companies with drugs up for negotiation are likely to amend their lawsuits against the price talks under the Inflation Reduction Act to better their chances at taking down the program, legal analysts say.

Amending complaints could bolster the plaintiffs’ chances at overcoming government arguments that they lack standing to sue and allow them to later move for summary judgment or request a preliminary injunction.

Companies like Amgen Inc. and Novo Nordisk that have drugs on the list but haven’t sued yet may do so, or join suits already filed, attorneys say, contributing to a pharmaceutical industry legal strategy geared toward getting the US Supreme Court to intervene.

“Now that the list is announced, we’ll definitely see movement in the lawsuits, because beforehand it was a little more of a theoretical harm,” said Carmel Shachar, a professor at Harvard Law School. “I think we’ll see a big flurry of action when the prices are announced as well, with attempts to hold it up with injunctions and summary judgment.”

Drugmakers and industry groups that sued before the release of Medicare’s list issued statements afterward that they remain steadfast in their position that the price negotiation program is unconstitutional. Eight lawsuits were filed before the list announcement. Another company with a drug on the list, Novartis AG, sued after.

“The IRA’s price control provisions will constrain medical innovation, limit patient access and choice, and negatively impact overall quality of care,” J&J said. “The IRA’s policies put an artificial deadline on innovation, threatening intellectual property protections and shortening the timeframe to deepen our understanding of patients’ unmet medical needs. At the same time, seniors could face bureaucratic barriers to access and potentially higher out of pocket costs even with the IRA’s out-of-pocket cost limits for Part D drugs.”

Attorneys note that some of the lawsuits may be scaled back with the list out, while others are expanded to encompass new claims. Some judges may try and consolidate the litigation, the attorneys say.

They also note that more drugmakers may push courts for a preliminary injunction against the program to buy time while the litigation inches its way to the highest court.

“They’re not going to give this up quietly,” said Yaniv Heled, a professor at Georgia State University College of Law. “You can expect to see lawsuits, and then appeals, and then more lawsuits and then more appeals.”

‘Fight to the Bitter End’

The 10 drugs selected for pricing negotiations are Bristol-Myers and Pfizer Inc.‘s Eliquis, J&J’s Xarelto, Boehringer Ingelheim and Eli Lilly & Co.‘s Jardiance, Merck & Co. Inc.‘s Januvia, AstraZeneca PLC’s Farxiga, Novartis’ Entresto, Amgen’s Enbrel, AbbVie Inc. and J&J’s Imbruvica, J&J’s Stelara, and Novo Nordisk’s Fiasp and NovoLog insulin products.

Pfizer said it wouldn’t be leading negotiations over Eliquis’ list price and that the task would fall to Bristol-Myers. Eli Lilly similarly said the company “will not have any role in whatever price is set” by Medicare for Jardiance.

Novo Nordisk said it “will explore all options that allow us to drive change for people that need it and strive to continue to bring innovative medicines to the market while helping increase access for those that need them,” though it took issue with the government’s approach. Likewise, AstraZeneca said it would “evaluate our next steps over the coming weeks.”

Merck filed the first lawsuit to block the negotiations in June, followed by suits by other drugmakers and their allies, arguing the program was unconstitutional or violated procedural requirements for implementation.

They’re awaiting a decision from Judge Michael J. Newman of the US District Court for the Southern District of Ohio on the U.S. Chamber of Commerce’s request for a preliminary injunction—an ask that could halt the program before negotiations even begin.

The Chamber asked the court to rule before the Oct. 1 deadline when drugmakers must decide if they will enter negotiations. The group said the Biden administration didn’t do its “homework” to understand price control schemes and is rushing for implementation.

“They had a year to research these basic questions,” Neil Bradley, the Chamber’s executive vice president and chief policy officer, said in a press call.

Drugmakers who’ve already filed lawsuits will “fight to the bitter end,” Heled said.

“I can’t imagine that the litigations are going to end before these prices are supposed to take hold or go into force,” Heled said.

Drug manufacturers on the list will also “definitely” want to amend their complaints, said Laura Dolbow, a fellow at the University of Pennsylvania Law School who specializes in administrative law.

Companies may also amend their complaints to include additional causes of actions, said Andrew Twinamatsiko, associate director of the Health Policy and the Law Initiative at Georgetown University’s O’Neill Institute. For example, plaintiffs arguing the program violates the First, Fifth, and Eighth Amendments of the Constitution may consider raising Administrative Procedure Act claims like those in recent lawsuits from AstraZeneca and Boehringer Ingelheim.

Drugmakers “could find a creative way of going around” the drug pricing law’s preclusion of judicial review of prices, he said.

More constitutional claims could emerge, and the courts could have a “remarkably large number of potential avenues to consider,” said Robin Feldman, a law professor at the University of California, San Francisco.

“What are they not claiming?” Feldman said. And “lawsuits already filed have named more constitutional provisions than most people knew existed.”

‘No Standing’

Astellas Pharma Inc., which filed a suit July 14, ended up with none of its products on the list. Legal experts expect Astellas’s case to be dismissed.

The drugmaker said in a statement that no decisions have been made regarding its lawsuit, but it remains confident in its stance that the program “would result in lower costs for the government, but not necessarily reduce out-of-pocket costs for patients.”

The case brought by trade group Pharmaceutical Research and Manufacturers of America also faces possible dismissal.

The Biden administration filed a motion to dismiss the PhRMA suit in the US District Court for the Western District of Texas a day before the list came out, specifically asking that the National Infusion Center Association be dismissed because it lacks standing and failed to allege that the federal program will cause any of its members an injury.

The actions drugmakers with products on the list take now could affect what other manufacturers will do in the future, said Nicholas Bagley, a law professor at the University of Michigan. The experiences of the drugmakers in the first round of negotiations could set the precedent for price talks in later rounds.

“If you’re a manufacturer who doesn’t have a drug listed, you’re likely to sit back and watch these other litigants,” Bagley said.

Everyone with Medicare Supplement knows the value and convenience it provides in allowing the policyholder to seek medical attention from any medical provider that sees Medicare patients. All hospitals see Medicare patients, so, heaven forbid, should we get cancer and want to go to MD Anderson Hospital in Houston—we may go directly there. And, depending on which Medicare Supplement plan we elect, we can be out of virtually nothing for our medical care.

The only real disadvantage to a Medicare Supplement plan is the premium. And it's not the first-year premium upon entering Medicare at age 65, but rather the premium in the ensuing years. This occurs because, as we age, each year, on our policy anniversary, the premium is usually increased to account for the additional risk an insurance company assumes to cover us as we age. The older we are, the more likely we are to generate medical insurance claims, and larger ones at that. Hence, the older we get, the more burdensome our premiums will become.

The only solution to that (while remaining insured)—other than to switch to a Medicare Advantage plan—is to re-shop our supplement plan. Typically, it does not behoove us to do this every year. Assuming our insurance company is ethical and competitive, the savings involved in moving to a more competitive plan won't be large enough to warrant the effort. But by the time we have experienced a second or third annual increase—it will be. In only a few states, is a Medicare Supplement policyholder allowed the right to move to a lower-cost plan and be guaranteed approval. This transition will be accomplished during that state's Open Enrollment Period. Texas has no Open Enrollment Period for Medicare Supplements. In Texas, Open Enrollment only applies to Medicare Advantage and Part D Drug Plans. In Texas, a Medicare recipient can apply for a new Medicare Supplement policy 365 days per year. Still, they must qualify based on their current health and health history. If their health is good, or their medical conditions are well controlled, they may be approved for the new and lower-cost plan. And this can be accomplished while maintaining equal benefits or even upgrading to superior benefits, if available.

If you are wondering if lower-cost Medicare coverage is available and considering applying for such—now is the time to do so. Brokers and agents, like myself, are currently in our slow period. This is because the government (Medicare) dictates when Medicare recipients may apply for a Medicare Advantage or Part D Drug Plan. That is each year between October 15 and December 7—the Open Enrollment Period for those products. Plans applied for during that period are guaranteed approval with a January 1 effective date. Brokers and agents who specialize in Medicare-related insurance products, like myself, begin studying and testing for national tests, which must be passed each fall in order to represent these plans in the coming calendar year, along with certifying (testing) with each insurance company whose product we want to represent. So from September, when most of us study and test, to the end of December, we are inundated with identifying our client's best plan options for the coming year and enrolling them in that product. Even with the best of staff, our market feels as though we are surrounded by "sharks in a feeding frenzy." Especially if we also assist Under Age 65 clients in obtaining Individual and Family health insurance with an overlapping Open Enrollment Period!

So—if you are at all considering obtaining a lower-cost Medicare Supplement plan—now—and the next three months—is the time to do so. I can scan the market to identify equal or superior benefits at meaningful premium savings. Sometimes a very meaningful 30% or more! Once I have done that, I will make the application process go as quickly and smoothly as possible. I charge no fee for my service, and you will be charged no more for the insurance plan than if you acquire it directly from the insurance company itself. You will not cancel your current coverage until we know you have been approved for all pre-existing conditions.

Please email or give me a call. I have been in the industry for 37 years and am not going anywhere. I enjoy what I do, and that is helping others find their best medical coverage at the lowest possible cost.

*(Please see feature article 1 below on prescription drug shortages and feature article 2 on Medicare Advantage Claim Denials.)

D. Kenton Henry

Office: 281-367-6565 Text my cell 24/7: 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

**********************************************************************

FEATURE ARTICLE 1

Drug price caps in Inflation Reduction Act exacerbating shortages, Gottlieb says . . .THE HILL

BY JULIA SHAPERO - 05/21/23 4:58 PM ET

Former Food and Drug Administration (FDA) Commissioner Scott Gottlieb

Former Food and Drug Administration (FDA) Commissioner Scott Gottlieb said on Sunday that drug price caps in the Inflation Reduction Act are exacerbating drug shortages.

"The features under the Inflation Reduction Act will exacerbate this problem, because it'll prevent these generic manufacturers from being able to take price increases," Gottlieb, who now serves on the board of Pfizer, told CBS' "Face the Nation."

"For example, if they enter a market for the first time, or they spend a lot of money upgrading a facility to be compliant with state-of-the-art regulations, they're not gonna be able to take a price increase to recoup some of those costs," he added. "So, it's going to come out of their own pocket."

Gottlieb said that sterile injectable drugs are particularly susceptible to shortages, suggesting that they should be carved out of the Inflation Reduction Act.

"The reimbursement for these drugs under government programs has been driven down very low, something above the marginal cost of manufacturing the drugs, and that's fine when it comes to a pill form drug where there's not a lot that can go wrong."

"But when it comes to an injectable drug, you need to leave a margin in so people can reinvest in manufacturing facilities, make sure they're high quality," he added. "They haven't done that, and things go wrong, and it results in shortages."

A March report from the Senate Committee on Homeland Security and Governmental Affairs found that there were more than 295 active drug shortages at the end of 2022, marking a five-year high.

**********************************************************************

FEATURE ARTICLE 2

SENATORS PRESS MEDICARE ADVANTAGE INSURERS OVER CLAIMS DENIALS

FIERCE HEALTHCARE MAY 19, 2023

By Paige Minemyer

There were no insurers represented on the hearing panel, and the senators instead heard from multiple policy experts, the Office of Inspector General and the widow of a patient who was harmed by care denials and delays. (Getty Images/designer491)

Pharmacy benefit managers weren't the only ones on the hot seat in Congress this week.

The Senate's Permanent Subcommittee on Investigations put Medicare Advantage (MA) plans on notice Wednesday, demanding answers for claims denials. Chairman Richard Blumenthal, D-Connecticut, said in an opening statement during the hearing that the committee sent letters to the three largest MA plans—UnitedHealthcare, Humana and Aetna—seeking documentation on how they make decisions around claims denials.

Blumenthal said these coverage denials have become commonplace for many MA enrollees.

"These denials have become so routine that some patients can predict the day on which they will come," he said.

He added that "there is growing evidence" pointing to MA plans using artificial intelligence and data algorithms in making denials, rather than relying on feedback from physicians or other clinical experts. A recent investigation from Stat found that these tools are taking on an increasing role in coverage decisions, though there is limited oversight and transparency

Blumenthal said the Department of Health and Human Services Office of Inspector General (OIG) has also identified a "large number of cases" where MA insurers refused to authorize services that met coverage requirements under Medicare. For example, a cancer patient seeking a routine scan to determine whether the disease had spread was held up by their insurer for a month, and another payer refused to cover a walker for a patient as they had already received a cane.

"In each of these cases, the insurer's decision overlooked the treating physician's assessment of what their patient needed," Blumenthal said.

There were no insurers represented on the hearing panel, and the senators instead heard from multiple policy experts, OIG and the widow of a patient who was harmed by care denials and delays. Megan Tinker, chief of staff at OIG, said in her submitted statement that in 2018, MA plans denied 1.5 million prior authorization requests, about 5% of the total. In addition, they rejected 56.2 million payment requests, or 9.5%.

Tinker said that between 2014 and 2016, MA plans overturned their own coverage denials 75% of the time when a member or provider appealed the decision. OIG also found that 13% of coverage denials were for services that met Medicare's coverage rules.

Tinker noted in her opening remarks that the program has grown rapidly over the past several years, and enrollment in MA now accounts for more than 50% of total Medicare enrollment.

"Fast growth has increased vulnerabilities and the need for robust program integrity measures," she said. "OIG work has demonstrated that the risk of waste, fraud and abuse in managed care are significant."

Jean Fuglesten Biniek, Ph.D., associate director of the Program on Medicare Policy at KFF, noted in her submitted remarks that the way payments work in MA may create financial incentives for insurers to deny care. It costs MA plans 83% of what it costs traditional Medicare to cover key services, while they are paid 106% of what the Centers for Medicare & Medicaid Services pays in fee-for-service Medicare, according to data from the Medicare Payment and Advisory Commission.

This means plans retain $2,300 above the cost of paying for a member's care, she said.

She added that there are also significant gaps in the data around prior authorization in MA; for example, there is no information about what services are denied or whether there are certain beneficiaries who are denied care more often. There is also a dearth of detail on how long it takes MA plans to respond to these requests.

"As a result, policymakers don't have the information they need to conduct oversight," she said.

By D. Kenton Henry editor, agent, broker 12 October 2022

In a year in which the annual inflation rate is over 9%, and the core inflation rate over 6%, there is some good news relative to Medicare Part D 2023 Drugs and Plan costs. And it comes just in time as the approximately 64 million Americans on Medicare will be electing their drug coverage during the “Annual Election Period” from October 15th through December 7th, for coverage to begin January 1.

While Medicare Part A (hospital and skilled nursing facility) coverage has been paid for during the working careers of most Americans or their spouses, Part B (out-patient coverage) has not. Medicare accesses an income-adjusted monthly premium based on a “two-year look-back at one’s income tax return. (for details refer to Chart 1, and Feature Article 1, below)

The base premium for individuals earning $97,000 or less, and couples filing jointly earning $194,00 or less, will be down $5.20 per month from $170.10 to $164.90.The Medicare Part B out-patient deductible will be down $7.00 from $233.00 to $226.00 in 2023. Although these decreases are nominal, to say the least, they are a move in the right direction.

The “not as good news” is that Part A Inpatient hospital costs to the beneficiary will be increasing. The inpatient hospital deductible is going to $1,600 for each admission – due to a different medical condition – or the same medical condition separated by 60 days or more.And the daily coinsurance for days 61-90 is going to $400 and for lifetime reserve days to $800. It is easy to see that most can ill afford to be liable for the cost of an extended hospital stay without supplemental coverage, such as Medicare Supplement or Medicare Advantage, to pay these expenses. (for details, refer to Chart 2 below)

Relative to Medicare Part D Prescription Drug Plans, the headline subject of this article, the best news is probably not that premiums are actually decreasing for many of the approximately 30 plan options available. Surveys show that Americans are more concerned about the price of their drugs than their plan premiums. So, more good news is that the cost of insulin – which has historically created something of a hardship for dependent diabetic patients – will be limited to a $35.00 monthly cap on insulin copays for Part D enrollees. In addition, all vaccines recommended for adults by the CDC will be available at no cost.

If not reversed, even greater cost savings are scheduled for 2024 and beyond. Here are some of the highlights:

2024

i) Part D enrollees entering the “catastrophic” phase of coverage will not owe any additional copays for the year. In other words, they will have 100% coverage.

ii) Part D premiums will be capped at a maximum price increase of 6% annually through 2029. Additionally, the government will expand eligibility for financial assistance.

2025

i) Out-of-pocket Medicare drug costs will be capped at $2,000 each year.

ii) Additionally, Part D enrollees will be able to spread out copay costs over the entire year, preventing hardship created by extremely high one-time bills.

2026

This will be the first year Medicare will be permitted to negotiate the cost of drugs. This will be limited to 10 drugs in 2026, increasing to 60 drugs by 2029.

These proposed changes all sound encouraging. Let us hope they survive to fruition. In the meantime, it is my job to assist my clients, and prospective clients, in identifying their lowest “total” cost Part D Drug plan for each calendar year. While people get fixated with monthly premium, one’s lowest total cost is the sum of their plan’s premium + any deductible due before their drugs become available for copays or coinsurance + their copays or coinsurance. We are seeking the lowest sum. It can be a tedious and confusing task for many and I assume that task for any client or prospective client requesting assistance.

For 2023 plan marketing, Medicare mandates I post the following disclaimer:

While I offer most, “I do not offer every plan available in your area. Please contact Medicare.gov or call 1-800-MEDICARE to get information on all your options.”

That being dispensed with, permit me to add – When someone requests I research the market for their lowest “total” cost drug or Medicare Advantage Plan, I not only employ proprietary software, but I utilize Medicare’s own data to make my recommendation. So rest assured, I have thoroughly reviewed all their options in the market before making my recommendation.

I do not charge a fee for my services. If you do not take advantage of my recommendation, you are out of nothing but the time we have spent together in arriving at it. However, if I introduce you to an insurance product, and you elect to apply for it, I only hope you will go through me to do so. You are not obligated to. Then, and only then, will I be compensated directly by the insurance company whose product you elect. The key to you is – you will pay no more premium for that product than if you were to walk in the front door of that company and purchase it directly from them. All companies in the Medicare Part D and Medicare Advantage market pay me the same so my objectivity is assured. Therefore, I like to think, you gain all the expertise my 36 years in the industry has to offer you at no additional charge. This is as opposed to a different person each time at the end of a toll-free number. I encourage you to take advantage of my offer and I look forward to establishing a working relationship with you.

D. Kenton Henry

All Plan Med Quote

Https://TheWoodlandsTXHealthInsurance.com Https://Allplanhealthinsurance.com Https://HealthandMedicareInsurance.com Office: 281-367-6565 Text my cell 24/7 @ 713-907-7984

CMS: Medicare Part B Premiums, Deductibles Will Decrease in 2023

Monthly Medicare Part B premiums will fall to $164.90 in 2023, marking a $5.20 decrease from this year, while Part A premiums are set to increase by $4 to $7.

September 27, 2022 – Medicare Part B premiums and deductibles will decrease in 2023, while Part A costs will rise, according to a fact sheet released by CMS.

Medicare Part B offers coverage for physician services, outpatient hospital services, certain home healthcare services, durable medical equipment (DME), and other medical services not covered by Medicare Part A.

The standard monthly premium for Part B enrollees will be $164.90 compared to $170.10 in 2022. The annual deductible will be $226, decreasing $7 from $233 in 2022.

Individuals with Medicare who take insulin through a pump supplied through the Part B DME benefit will not have to pay a deductible starting on July 1, 2023. In addition, cost-sharing will be capped at $35 for a one-month supply of covered insulin.

In 2023, Medicare beneficiaries who are 36 months post-kidney transplant can choose to continue Part B coverage of immunosuppressive drugs despite no longer being eligible for full Medicare coverage. These individuals will have to pay a monthly premium of $97.10 for immunosuppressive drug coverage.

Medicare beneficiaries with incomes greater than $97,000 will have higher Part B premiums. For example, monthly premiums will range from $230.80 to $560.50 for high-income beneficiaries. Similarly, monthly immunosuppressive drug coverage premiums will vary from $161.80 to $485.50 for high-income beneficiaries.

The While Part B costs will decrease in 2023, Part A costs are set to increase.

Medicare Part A offers coverage for inpatient hospital services, skilled nursing facility care, hospice care, inpatient rehab, and home healthcare services.

The Medicare Part A inpatient hospital deductible for beneficiaries admitted to the hospital will be $1,600 in 2023, rising from $1,556 in 2022. This deductible covers beneficiaries’ share of costs for the first 60 days of inpatient hospital care.

For days 61 through 90 of hospitalization, beneficiaries will have to pay a coinsurance amount of $400 per day, up from $389 in 2022. Past 90 days, the coinsurance will rise to $800 per day. The daily coinsurance for individuals in skilled nursing facilities will be $200 for days 21 through 100 of extended care services, up from $194.50 in 2022.

The majority of Medicare beneficiaries do not have to pay a Part A premium because they have worked at least 40 quarters in their life, the fact sheet noted. However, for those who have not, 2023 premiums are increasing.

Individuals who have at least 30 quarters of coverage or were married to someone with at least 30 quarters of coverage will have a Part A monthly premium of $278 in 2023, compared to $274 in 2022.

Individuals with less than 30 quarters and those with disabilities will have to pay the full 2023 premium of $506 per month, which is $7 higher than in 2022.

The fact sheet also shared 2023 information on Medicare Part D costs. Premiums for Medicare Part D, which offers drug coverage, vary from plan to plan. Around two-thirds of beneficiaries pay premiums directly to their plan, while the other third have their premiums deducted from their Social Security benefit checks.

Beneficiaries with incomes above $97,000 must also pay an income-related monthly adjustment amount in addition to their Part D premium. The amounts will range from $12.20 to $76.40 for high-income beneficiaries.

September 02, 2021 – The Alliance of Community Health Plans (ACHP) is urging the federal government to take action and lower prescription drug prices with a set of recommended actions.

The costs of prescription drugs continue to rise each year, but policymakers have done little to address it. ACHP’s list of suggestions ranges from increasing drug pricing transparency to expanding the use of biosimilars.

Catastrophic Medicare Part D prescription drug spending has been on the rise for over a decade. Seniors do not have an out-of-pocket cap for Medicare Part D, which can leave them with high costs in the catastrophic phase.

ACHP’s first recommendation is to redesign the Medicare Part D benefit including creating an out-of-pocket healthcare spending cap for seniors and to ensure that consumers will not owe anything during the catastrophic phase. Drug companies should also have to assume financial responsibility for each Part D phase and take some of the pressure off of Medicare.

Medicare should also receive resources to allow the program to negotiate lower drug prices for their beneficiaries, ACHP suggested.

ACHP’s next recommendation was for the federal government to allow the US Department of Health and Human Services (HHS) to negotiate prices for expensive prescription drugs that have no generic or biosimilar competition. These drugs were responsible for 60 percent of Part D spending in 2019, the fact sheet noted.

Currently, HHS has no power over competitive drug pricing.

Policymakers should also extend price negotiation to the commercial market to keep drug companies from shifting costs to non-Medicare consumers.

High-cost drugs that face no competition should also have an International Pricing Index applied that will limit the price to no more than 120 percent of its average international market price. The previous administration supported a similar approach through its Most Favored Nation model, but the Biden administration has proposed to rescind that model.

ACHP also urged the federal government to increase the use of biosimilars by informing clinicians and patients of the products and by persuading the Federal Trade Commission to increase biosimilar presence on the drug market. There are 29 FDA-approved biosimilars that are more affordable than other prescription drugs, but less than 12 are available on the market.

Increasing reimbursement rates for biosimilars could also improve utilization, the fact sheet stated.

ACHP’s suggestions also targeted drug companies’ unjustifiable raising of drug prices. At the beginning of 2021, 735 drugs prices increased up to 10 percent without reason.