By D. Kenton Henry, Editor / Agent / Broker — TheWoodlandsTXHealthInsurance.com, AllPlanHealthInsurance.com, HealthandMedicareInsurance.com 30 October 2025

Each November in Texas marks more than just the start of the new health insurance year—it’s your gateway to securing coverage for the year ahead. This time around, the 2026 individual and family health insurance market is undergoing noticeable changes. Here’s what you need to know—and how you can be ready.

1. Why 2026 matters

Open enrollment for 2026 policies begins November 1, 2025, and runs until January 15, 2026 for most Texas consumers. If you don’t act in this window, you could be locked out of making changes until next year unless a qualifying life event occurs. Given major shifts among carriers and plan options, early action is more important than ever.

2. Carrier changes you should track

One of the major headlines: Aetna will exit the Texas individual and family market beginning in 2026. That means if you currently have an Aetna plan, your policy will not renew for 2026. You’ll need to select a different carrier in the upcoming enrollment period.

Other carriers are repositioning their offerings, adjusting networks, benefits, and rates. Even if your carrier is staying, plan names and design may change. As your broker, I’ll review all available options from multiple carriers and ensure you’re not simply renewing by default.

3. What this means for you

No automatic renewal: If your carrier exits the market, your current plan will not carry over. You’ll receive a Notice of Change—or termination—and need to select a new plan.

Shop your options: Differences between plans are not only about monthly premiums. Review networks, cost-sharing, deductibles, out-of-pocket maximums, and whether benefits match your healthcare needs.

Subsidy changes: The federal subsidy rules continue to evolve. Even small changes in income, household, or eligibility can shift your subsidy level. I’ll help you analyse eligibility for Advance Premium Tax Credits (APTC) and other cost-saving tools.

Timing matters: Beginning November 1, I’ll be available to assist you through the selection process—not just on carriers and plans, but on ensuring accurate enrollment to avoid coverage gaps.

4. Why working with a broker matters

As an independent broker specializing in medical insurance since 1986, I work with virtually every major carrier licensed in Texas. My services to you are free of charge. My goal is to ensure you get the best plan that fits your health needs, budget, and preferences—especially in a year of significant market change. Rather than navigating dozens of plan names on your own, let me do the heavy lifting and help you make an informed choice.

5. What to do now

Gather your information – your current health plan, recent premium receipts, summary of benefits, and any health changes.

Schedule your review – open enrollment kicks off November 1. If you’d like early preparation, I’m available now to pre-review your situation so you’re ready to act.

Act during the window – November 1 through January 15 is your open period. Plans go into effect January 1, 2026, or, depending on carrier rules, as early as December 1, 2025.

Don’t wait – with carrier exits and plan redesigns in motion, the sooner you start the review, the better your chance of finding the optimal match.

Working together, we’ll turn these market shifts into an advantage—so instead of scrambling when notices arrive, you’ll move confidently into 2026 with coverage aligned to your needs.Let me handle the complexity so you can focus on your life, your health, and your goals.

If it’s after hours, or you simply prefer, you can do preliminary research before calling me by obtaining quotes from my quoting engine. You do NOT have to log in to obtain them but be certain to call me afterwards with questions, and assistance in finding your providers within the networks, as well as applying. CLICK HERE: https://allplaninsurance.insxcloud.com/get-a-quote

D. Kenton Henry Editor · Agent · Broker TheWoodlandsTXHealthInsurance.com * AllPlanHealthInsurance.com * HealthandMedicareInsurance.com

By D. Kenton Henry Editor, Agent, Broker HealthandMedicareInsurance.com 11 September 2024

Welcome, fellow boomers and others blessed to have lived long enough to find yourself here. I believe you recognize that the information in my blog posts can contribute to this leg of our journey being the longest and most rewarding. I’m right here with you and doing my best to make it so for all of us. Coming changes in 2025 Medicare plans are significant, so please read this and feel free to take notes. They could impact you and probably will.

We will begin with what your Medicare Part B premium to Medicare for Out-Patient Care will go to: For those earning less than $105,000 your premium will go to $185.00 (up from $174.70) For those in the highest income bracket, earning greater than $500,000 your premium will go to $628.90 (from $594.00) For every income block in between, couples filing jointly, and what Part D premiums to Medicare will go to, please click on this link and scroll down: https://www.irmaacertifiedplanner.com/2025-irmaa-brackets/

An Annual Notice of Change (AOC) from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan is due you. It will arrive in the United States mail and, per Medicare rules, by September 30th. So, like the pretty woman in the image above, open it and read it. It outlines how much your premiums, deductibles, and co-pays will differ in the coming year. Will your drugs be covered, and will your current drug plan even be available? We don’t yet know. Mutual of Omaha notified agents and brokers that it is withdrawing altogether from the Part Drug plan market beginning January 1. If you are currently with them or have any other plan that is exiting the marketplace, follow the instructions in the next paragraph.

According to eHealth, a mere 36% of those surveyed claim the AOC to be “readily understandable.” The author of the attached article recommends you spend at least 30 minutes reviewing it. However, if you finish this article, you can cut that time considerably. If you have finished all and still feel you are among the remaining (up to) 64%—please call me @ 281-367-6565.

This article is a follow-up to my last blog post on September 3rd. “MAJOR CHANGES IN MEDICARE PART D DRUG PLANS ARE COMING OUR WAY (what we know. and one thing we don’t know).” To read it, please click on this link. (if necessary, copy and paste it in your browser’s URLbox and hit enter):

Well, now we know more of the potential compromises mentioned or alluded to in that article. All of these are covered in detail in Feature Article 1 below.

The changes addressed here are largely because of the new $2,000 per year limit on Medicare Part D drug costs in 2025 (versus $8,000, plus 5% thereafter, in 2024). That leaves Medicare Part D insurance companies looking for ways to compensate for the additional costs shifting from you to them. Come January, you will meet a new deductible of up to $590 (from $545) for applicable drugs. Typically, your plan will apply this to brand-name drugs and not Tier 1 or Tier 2 generics.

Beyond that, the Gap, commonly referred to as the “donut hole” (in which you were previously responsible for 25% of your drug costs), has been eliminated entirely. You will have entered the “Initial Coverage” phase in which your elected drug plan will pay 65% of your applicable drug costs, and you will pay 25%. The Manufacturer (pharmaceutical company) will discount the remaining 10%. When you hit your maximum Out-of-Pocket (OOP) threshold of $2,000, you enter “Catastrophic Coverage”. At that point, your plan will pay 60%. Reinsurance (CMS, the Center for Medicare Services, i.e., the government) will pay 20%, and the Manufacturer will pay the remaining 20%. You will pay $0.

This, of course, sounds very well and good! And for those utilizing large quantities of drugs, or expensive drugs, this will indeed be of great benefit. But in what ways may the drug plans “compensate” for the additional costs they will bear? Much of such was referenced or alluded to above. However, please permit me to drill down on potential measures drug plans may take to offset their increased share of your drug cost. *(I am a Medicare Insurance product broker and not a C.P.A. As such, I will not address the impact on the taxpayer of their increased share of Medicare drug costs in this forum. wink. wink 😉

The drill down:

In addition to the higher deductible, higher premiums may be in store. But it could have been a lot worse. CMS did health insurance companies a favor with a “premium-stabilization” plan. In 2025, they will give them a subsidy in exchange for not “slapping members with exorbitant premium hikes. So, “what might have been a 40%, 50%, or higher premium increase may only be as high as 25%. Either way, it will be a sticker shock when some see how their premiums changed.” *(a paraphrase a quote in Feature Article 1)

The Kaiser Family Foundation says the average cost of a stand-alone Part D drug plan is $43. I have seen previews of premiums which will be $0, but others, have risen. In addition to your premium, co-pays for your drugs could go substantially higher. If your drug plan is obligated to charge you less for (or cover more of) a particular drug, are they simply going to charge you more for others?

And what about “Value Added Benefits” (VAB) available in some Medicare Advantage Plans? These include vision, hearing, and dental services. Other examples include acupuncture, bathroom safety devices, and wigs for hair loss. And what about your gym membership? Embedded dental insurance has been dramatically cut back or removed completely.

VAB are not covered by Original Medicare. Medicare Advantage has been able (often along with a $0 premium) to offer these things as an additional incentive to encourage enrollment in their plans. However, because you left Original Medicare and “assigned” the administration of your benefits and claims to the Advantage company when you enrolled, your plan can choose to provide these ancillary benefits that Original Medicare does not. Or they can choose to cover them no longer. This discretion is on their part because the provision of VAB benefits is not codified in law or per CMS regulation. Resultingly, they are not guaranteed. They are optional benefits that the plans have the right to withdraw at any time. I hope you can continue to “workout” at the gym, at your plan’s expense, in 2025 and beyond. But be prepared to purchase a home gym kit if you learn your membership is downgraded or your Advantage plan disappears entirely.

With no obligation, please feel free to contact me for clarification of these relevant issues and additional guidance in navigating the Medicare system and the changes referred to here. I’m in Medicare with you. I am a “Boomer” who has spent the better part of his life in the medical insurance market. For years, I have assisted individuals, families, and businesses in identifying and enrolling in health insurance plans that came as close as I could get them to fully meeting their medical insurance wants and needs.

To sum things up, I work for my clients. I work for you. Not the insurance company. I study, take their tests, and “certify” to represent their products each calendar year. I just completed certifying with approximately 14 companies in preparation for marketing their products in 2025. They do not pay to renew my licenses or my Errors and Omissions insurance, nor do they cover my office insurance and expenses. Neither they, nor anyone else, pay me wages or a salary. And that is great! I knew and understood those terms when I went out on my own. And that is precisely why I did it. I did not want to be beholden to the insurance company.

After becoming independent, the list of companies I was contracted with grew to over 40 during the 1990s. That number has changed as many of those companies went the way of the steam engine with “Obamacare” and all the red tape and regulations that come with it and remaining in the industry. But I persist. I remain positioned to provide you with virtually every available Medicare and health insurance product in your region.

In conclusion:

If you’re reading this, chances are you remember Jim Rockford (a private detective, portrayed by the actor the late James Garner) in his TV show, The Rockford Files (you can hear the opening music now, can’t you?). In the prelude to each episode, you see his cassette recording answering machine and hear the message, “This is Jim Rockford. At the tone, leave a message …”.

Should you get mine, please do the same. Or you may simply text me.

FORTUNE Richard Eisenberg Updated Mon, Aug 26, 2024

Why this year’s Medicare Annual Notice of Change will be vital reading for beneficiaries

In this article:

If you’re on Medicare, you’ll be getting one or two Annual Notice of Change letters in your mail or email this September about your 2025 coverage and costs. You may be tempted to ignore what looks like junk, as nearly a third of recipients do, according to an eHealth survey.

Don’t.

“So often, a person who is quite happy with their plan and doesn’t bother to look at their Annual Notice of Change then gets a nasty surprise in January” when the plan’s new costs and coverage kick in, says Danielle Roberts, author of 10 Costly Medicare Mistakes You Can’t Afford to Make and founding partner of Boomer Benefits, which sells Medicare policies.

What is an Annual Notice of Change?

An Annual Notice of Change from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan lays out how much your premiums, deductibles, and co-pays will differ in the year ahead and whether the plan will even be offered. (Medigap plans don’t send these notices because they don’t change much year to year.)

An Annual Notice of Change from your Part D plan also says whether your prescriptions will be covered and, if so, how much you’ll pay. A Medicare Advantage Notice of Change will tell you if your doctors and hospitals will remain in the plan’s network.

While this information is always essential to make smart choices during Medicare’s eight-week open enrollment period (Oct. 15 – Dec. 7), experts say reading your Annual Notice of Change is especially important in 2024.

“There is an excellent chance that something is changing on your plan,” says Roberts. “This year, more than ever, we can expect big changes in the plans.”

Surprising effect of the $2,000 prescription drug cap

That’s largely due to a major Medicare change coming in 2025: the new $2,000 cap on out-of-pocket costs for prescriptions covered by a Part D plan.

Since Part D health insurers will be on the hook for more prescription costs due to the cap, they’ll be looking for ways to compensate.

That could mean higher premiums (currently $43 a month for stand-alone plans, on average, according to KFF), deductibles, and co-pays—possibly substantially higher than in 2024.

“I have been very, very concerned about what the $2,000 cap was going to do to Part D premiums,” says Roberts.

The prescription drug change in 2025 could also lead to your Part D plan no longer covering certain medications you take or raising prices of ones it will.

Medicare Advantage plans—some facing profit squeezes currently—often include Part D coverage, so they may respond to the $2,000 cap by trimming or eliminating benefits to keep their popular $0 premiums intact, experts expect.

As a result, your Medicare Advantage benefits that original Medicare can’t offer—such as dental, vision, hearing, and gym memberships—could be less attractive than in 2024, or possibly gone entirely.

“It really will be important to understand what’s changing in the coming year in my current plan and does the plan still fit?” says eHealth CEO Fran Soistman. “Does it still provide the value that it did when I elected to go in it in the first place?”

Reading and understanding the Notice of Change

Your Annual Notice of Change will tell you—if you can understand it.

Only 36% of Medicare beneficiaries surveyed by eHealth said their Annual Notice of Change letter is “readily understandable.”

Figure on spending about 30 minutes closely reading your Annual Notice of Change to see exactly what will be different in 2025 and whether you’ll want to switch plans or coverage next year as a result.

During open enrollment, you can switch from your current Part D plan to another, from your Medicare Advantage plan to another, from Medicare Advantage to original Medicare as well as from original Medicare to a Medicare Advantage plan.

But don’t feel compelled to switch plans just because your Annual Notice of Change says your premium will go up a little or a benefit will be trimmed slightly.

“If there’s a modest benefit decrease or premium increase, but they’re satisfied with what the carrier is providing, people shouldn’t make a change,” Soistman says.

However, he added, if a medication you take will no longer be covered or your physician or hospital won’t be in network, that’s an important change that may persuade you to switch coverage.

The Medicare Plan Finder on Medicare’s site will let you compare Part D and Medicare Advantage plans for 2025.

And, as Philip Moeller writes in the forthcoming revised edition of his book, Get What’s Yours for Medicare, if your Medicare Advantage plan won’t include your favorite doctor or hospital in its network in the year ahead, it’s legally obligated to work with you to identify other physicians or hospitals in its network that you’d like.

A new program to help avoid big premium hikes

To help prevent drastic Part D premium increases, the government’s Centers for Medicare and Medicaid Services recently threw a bone to health insurers with a premium-stabilization plan.

Medicare will provide a special subsidy to those insurers for 2025 in exchange for avoiding slapping members with exorbitant premium hikes.

“It should take what might have been a 40%, 50%, or higher premium increase down to probably 25%,” says Soistman. “It’s still going to be a bit of sticker shock when some people see how their premiums changed.”

Roberts says, “I’m still somewhat concerned about premiums, but I feel a little better after the stabilization program announcement.”

Getting help if your Medicare plan will change

After reading your Annual Notice of Change, you may want to get help deciding on the right Medicare plans for 2025 and to understand the implications of coming changes to your plans.

You can ask a Medicare broker or agent for assistance; there’s a directory at the National Association of Benefits and Insurance Professionals site. The sooner you do, the better, since agents and brokers will be swamped near the end of open enrollment.

“At Boomer Benefits, we have to stop taking new requests after Thanksgiving,” says Roberts.

If one of your prescriptions won’t be covered by your Part D plan in 2025, call your doctor to see if another covered medication would be okay or if you should find a new plan that includes it, Roberts advises.

For information about Part D and Medicare Advantage plans without purchase recommendations, try yourState Health Insurance Assistance Program or visit Medicare’s site or call Medicare’s toll-free number.

More time for open enrollment?

Soistman believes all the changes coming to Part D and Medicare Advantage plans for 2025 will push back the arrival of the Annual Notice of Change documents to the last two weeks of September.

If so, this will give people with the plans less time than normal to read the notices before open enrollment.

The eHealth agency has asked the Centers for Medicare and Medicaid Services to extend open enrollment by about five days to give beneficiaries, insurers, and Medicare brokers more time. Boomer Benefits favors the extension, too.

So far, the government hasn’t responded to eHealth’s proposal.

Could the 2025 open enrollment become Medicare’s equivalent of the Department of Education’s FAFSA financial-aid form fiasco of chaos and confusion?

“I don’t think it will be quite as drastic. I think it is going to be a year of change, though,” says Soistman. “And change is hard for people.” ********* Please follow me follow D. Kenton Henry @Https://HealthandMedicareInsurance.com

Ever since the passage of the Patient Protection and Affordable Care Act (ACA), commonly referred to as “Obamacare”, in 2010, the Department of Health and Human Services has dictated when and under what circumstances an individual and family can apply for and obtain health insurance. This period is known as the Open Enrollment Period, and it is upon us. Each year, between November 1st and December 15th, U.S. citizens and their families may apply for and obtain health insurance effective January 1st of the coming calendar year. From then until January 15th, they may apply for coverage effective February 1st. Beyond that date, they are locked out of any health insurance plan they were not enrolled in when the year ended. Only special circumstances such as losing “creditable” coverage through no fault of their own, moving out of a plan’s area, birth of a child, or death of a covered family member allow them to apply for coverage beyond the Open Enrollment Period. And only if they were insured when the special circumstance occurred and no more than 60 days have passed. Creditable coverage meets all the mandates of the Affordable Care Act, such as guaranteed coverage for pre-existing health conditions, including pregnancy and mental health disorders, along with no out-of-pocket for preventative medicine. All coverage is guaranteed so long as the above requirements are met.

If affordability of health insurance is an issue, Premium Tax Credits (subsidies) are available from the Department of Health and Human Services (DHS) to people or families whose income falls below a certain threshold.

WHO IS ELIGIBLE FOR THE PREMIUM TAX CREDIT?

To receive the premium tax credit for coverage starting in 2024, a Marketplace enrollee must meet the following criteria:

· Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2024 benefit year will be determined based on 2023 poverty guidelines

· Can not have access to affordable coverage through an employer (including a family member’s employer)

· Can not be eligible for coverage through Medicare, Medicaid, the Children’s Health Insurance Program (CHIP)

· Have U.S. citizenship or proof of legal residency (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements)

· If married, must file taxes jointly

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Your tax credit is based on the household income estimate you put on your Marketplace application.

Income between 100% and 400% FPL: If your income is in this range (in all states) you qualify for premium tax credits that lower your monthly premium for a Marketplace health insurance plan. The lower your income is as a percent of the FPL—the higher your subsidy.

The easiest way to determine whether and for how much you qualify is to call me. You will estimate your 2024 household’s adjusted gross income and my subsidy calculator will tell us (based on the number of people in your household) how much your subsidy will be. If we give the DHS the same information you give me, my calculations are usually accurate to within $3.00 of what you will actually receive. We then apply that subsidy against the premium of the plan you wish to acquire and arrive at your net premium.

The number of people who qualify for subsidies continues to grow. For details on this, please refer to this chart and my feature article 2 below.

As to how much retail (gross) premiums are expected to grow from 2023 to 2024, estimates put the national average at 6%. (For the details on this, please refer to Feature Article 1 below.) Given the rate of core and real inflation, this should not come as a surprise. Acquisition of a subsidy will certainly offset ever-increasing premiums.

As always, the greatest challenge to the consumer and their agent/broker is affordability or obtaining the desired benefits. Instead, it is finding their doctors in the networks of a health plan. In 2024, as it was this year, there will be over 100 different plans available from six to eight different companies, depending on where one resides. Dealing with this myriad of options is where my three decades specializing in health insurance in the Houston area is invaluable. I know which hospitals are in which plan networks, and my provider search tools scan all plans without you having to go from company to company for results. Because I represent every company doing business in Texas, you can acquire information on all of them with one call to me.

Again, Open Enrollment begins November 1st, and for coverage during the entirety of 2024, it ends December 15th. Unlike going to the marketplace (Healthcare.gov) you will get me each time you call my local office with questions and for assistance and service–as opposed to an 800 number where you will get a different individual each time you call. My service is much more personalized and detailed than that of an hourly worker at the end of that toll-free number. If I don’t provide you with the level of service you deserve, I don’t have a client. And if I don’t have a client, I don’t earn a living. And it costs you no more to go through me than directly to the company whose policy you ultimately acquire.

I look forward to working with you and providing the best of service. Please call me.

D. Kenton Henry

Office: 281-367-6565 Text me 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

This analysis of insurers’ preliminary rate filings shows that ACA Marketplace insurers are requesting a median premium increase of 6% for 2024. Insurers cite price increases for medical care and prescription drugs as a key driver of premium growth in 2024, In addition to inflation’s impact on medical costs, insurers point to growth in the utilization of health care, which fell in 2020 but has since returned to more normal levels.

Insurers’ proposed rate changes – most of which fall between 2% and 10% – may change during the review process. Although most Marketplace enrollees receive subsidies and are not expected to face these added costs, premium increases could result in higher federal spending on subsidies.

The analysis can be found on the Peterson-KFF Health System Tracker, an information hub dedicated to monitoring and assessing the performance of the U.S. health system.

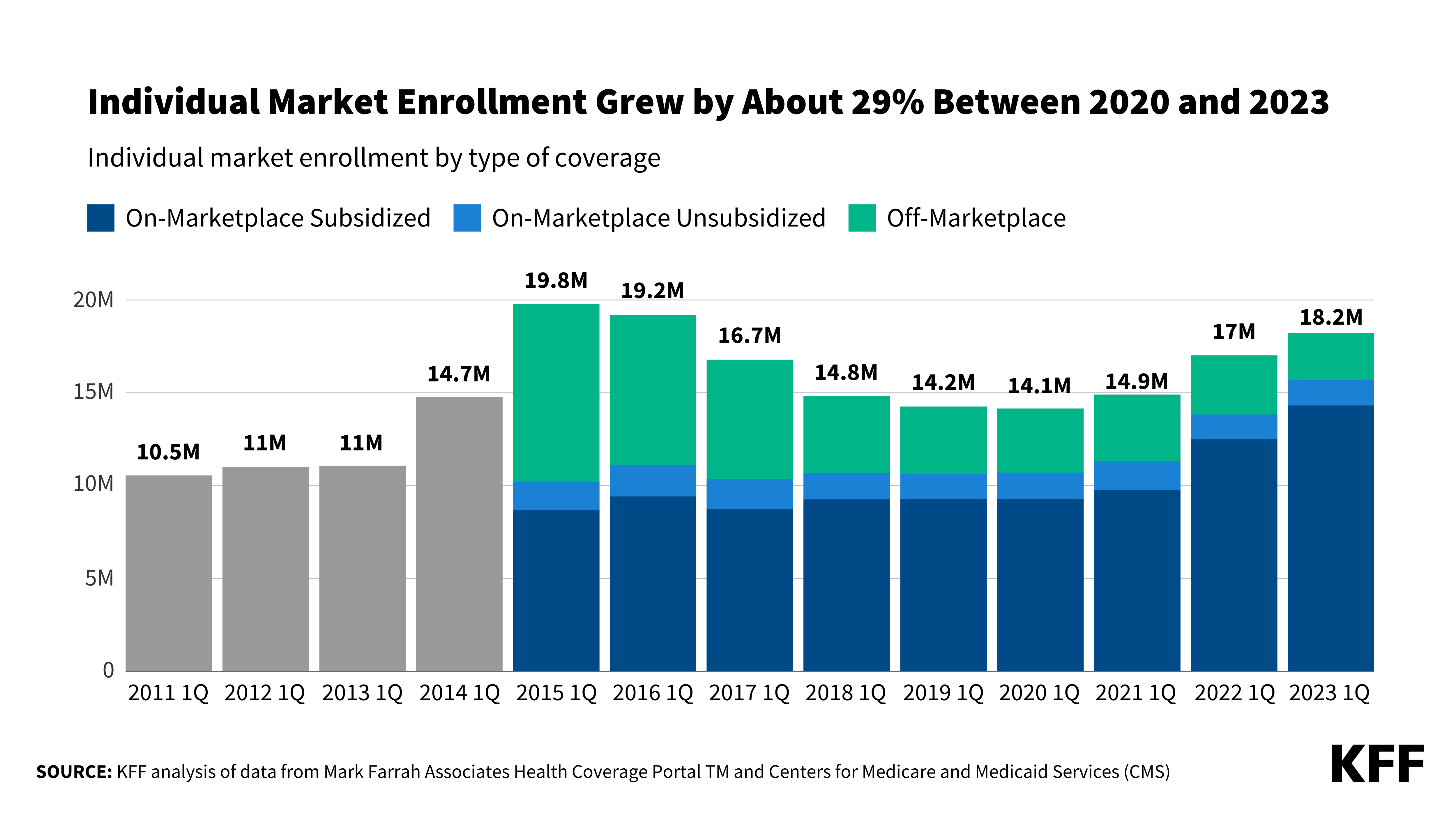

Enhanced Marketplace subsidies have continued to drive up enrollment in the individual market, and the loss of Medicaid coverage by millions of people could contribute to this trend, according to a new KFF analysis. Meanwhile, enrollment in non-ACA-compliant plans is at a record low.

As of early 2023, an estimated 18.2 million people have individual market coverage, the highest since 2016. Individual market enrollment grew by about 29% between early 2020 and early 2023 — a result of enhanced subsidies introduced by the Inflation Reduction Act, increased outreach, and an extended enrollment period.

This enrollment growth could continue in 2023 as states resume Medicaid disenrollments amid the unwinding of the continuous enrollment provision. Some of the people losing Medicaid coverage may be eligible for subsidies on the ACA Marketplaces.

Due in part to the enhanced subsidies, about 4 in 5 individual market enrollees have subsidized coverage — the highest share since the ACA was implemented.

The number of people in non-compliant plans has fallen each year and could decrease further due to the Biden Administration’s proposed rule that would reverse the expansion of short-term plans. An estimated 1.2 million people were in non-ACA-compliant plans in mid-2022, compared to 5.7 million in mid-2015. These short-term plans often do not include certain benefits or coverage for pre-existing conditions and can impose a dollar limit on insurance coverage.

If unsubsidized premiums rise in 2024 due to higher health care prices and utilization, enhanced subsidies could shield most individual market enrollees from increases in their monthly payments.

TIME IS RUNNING OUT FOR A JANUARY 1 EFFECTIVE DATE!

Op-ed by D. Kenton Henry Editor, Broker 26 November 2021

In September, I learned Aetna and Unitedhealthcare would be reentering the Texas ACA Underage 65 health insurance market for the first time since 2015. Since then, BlueCross BlueShield has been the only “household name,” a large, financially sound insurance company in the southeast Texas market. This was most welcome news, and I was hopeful these additional peer companies would allow my clients and fellow Texans access to more doctors and hospitals. Finding my client’s preferred doctors and hospitals in a plan network has been my client’s and my greatest challenge since the departure of all PPO network options six years ago. Alas, the hoped-for provider expansion in 2022, at this point, has failed to materialize. From 2015 into 2021, the St. Lukes Hospital system has been the only major hospital system participating in most insurance companies’ HMO networks. Such will remain the case for 2022.

Additionally, the entry of Bright Insurance Company (for the first time) doesn’t even appear to do that. They will limit their policyholder’s access to hospitals will be limited to smaller HCA local community hospitals. At least for the time being.

Doctors have practicing privileges at one or more hospitals. Of course, it follows that when an insurance company has fewer hospitals in their network, they will have fewer participating doctors. And so it seems. Only one health insurance company in the southeast Texas ACA health insurance market allows its clients access to the three major hospital systems in the area. Those hospitals are St. Luke’s, Memorial Hermann, and Houston Methodist. And then, only if you acquire their more expensive Silver or Gold plans.

However, there is a bit of good news for all Americans in the “Individual and Family” health insurance market. The federal government’s American Rescue Plan has increased the amount of Advance Premium Tax Credit (subsidy) and Cost Sharing Reduction (reduction of deductibles, copays, and coinsurance) available to a household. It also expanded the eligibility for these subsidies. As the feature article below explains, this will qualify more people for both types of savings.

Furthermore, unemployment effects and increases your potential premium tax credit! The American Rescue Plan exempts up to $10,200 in UI benefits from federal income tax. People who receive UI benefits in 2020 will be able to reduce their adjusted gross income by up to that amount, and so reduce their federal income tax liability.

Please get in touch with me to learn the details on the aforementioned company providing the greatest access to providers and how the expanded subsidies and Cost-Sharing Reductions may improve your health insurance situation.

If you choose to be proactive and would like to do some reconnaissance before calling me for assistance and details, you may click on my quoting link immediately following. When the page opens, ignore the login button. You need not log in. Enter your information. I.e., birth date, zip code, etc. On the next page, click on the top box “SELECT ALL” to clear the selections. Then select “MEDICAL” only, to get started. Otherwise, you will be overwhelmed with options and information. You can always return for dental, etc.)

Click “YES” if you would like to estimate whether you qualify for a subsidy. If so, enter your estimated annual income in 2022 and click “CALCULATE”. It will estimate your subsidy. The estimates are usually accurate to within $3.00. From there, click “NEXT”. You will then see all your plan options and be able to LOOKUP PROVIDERS and see plan details. Or simply call me to do all this for you!

CLICK HERE TO SEE ALL YOUR ACA HEALTH INSURANCE OPTIONS (IF NECESSARY, COPY THE LINK IN YOUR BROWSER AND HIT ENTER):

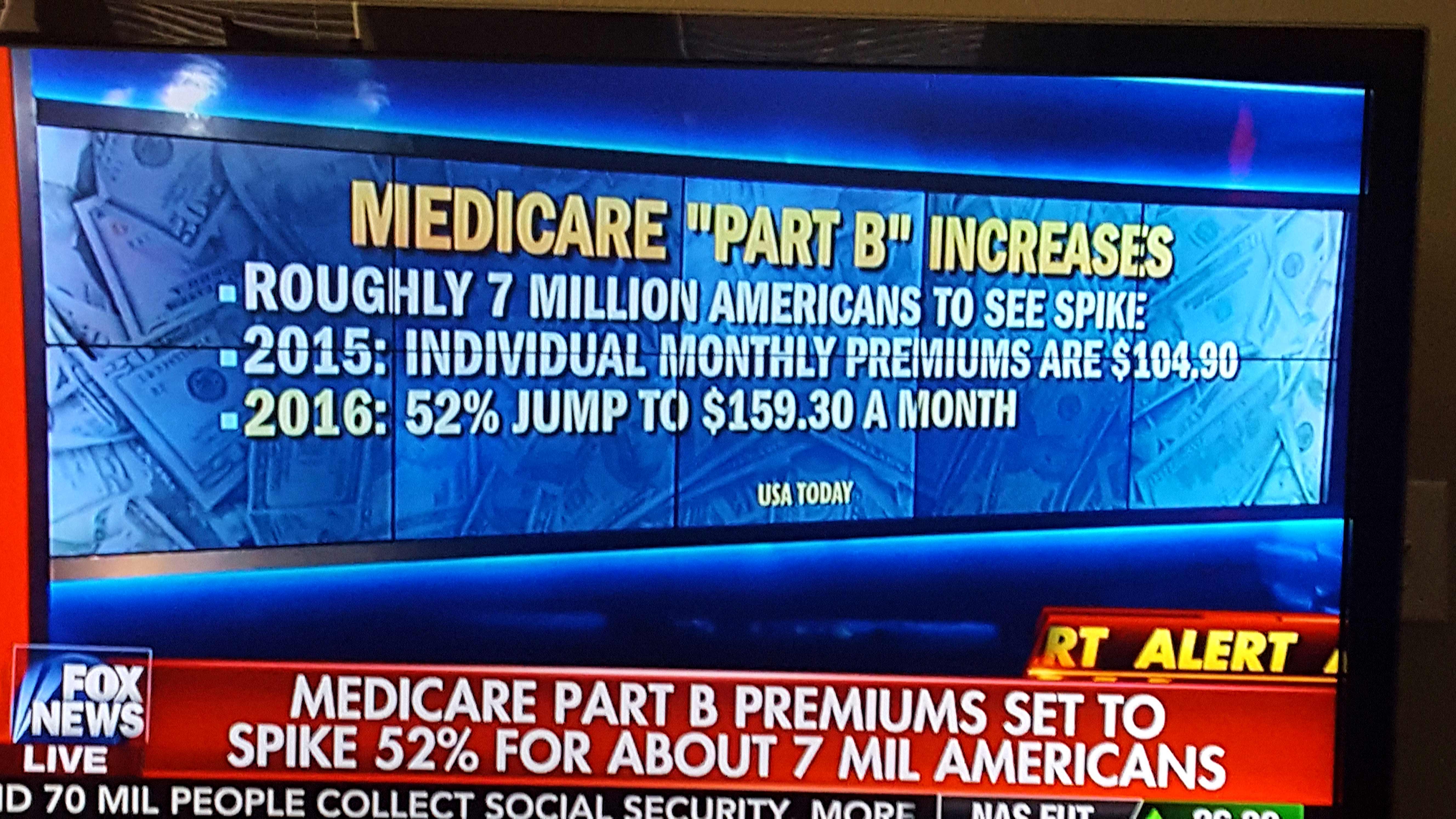

As the cost for everything, including medical treatment, is going up, so too are Medicare’s premiums and deductibles. As our second feature article below illustrates, the Medicare Part B (outpatient) basic premium is going from $148.50 to $170.10 and it’s calendar year deductible is going from $203.00 to $233.00! You can do the math, but, needless to say, so much for 5% inflation rate projected by the current administration which also does not appear to apply to our cost for gasoline, meat, and energy and food, in general! You’ve already spent the increase in your Social Security Benefit!

The details of how your Medicare Part B basic premium will may titrate upward relative to your income are clearly outlined in Feature Article 2, just published by the Centers For Medicare and Medicaid Services.

Lastly, if you are making the decision whether to go with a Medicare Advantage Prescription Drug Health Plan vs. a Medicare Supplement policy coupled with a Part D Prescription Drug Plan – please read Feature Article 3 (say it ain’t so, Joe!) below, and carefully weigh your decision.

Again, please contact me for guidance in how to minimize the impact of these changes and maximize your both your access to providers and quality health care. My 35 years specializing in the health and Medicare related insurance industry have provided me insights beyond that of the average agent/broker/generalist; and my clients access to a far greater number of products and solutions.

Advanced Premium Tax Credits(APTC):Lowers the cost of premiums and can be used on any Marketplace plan except for catastrophic plans.

Cost Sharing Reductions(CSR):Lowers the cost of deductibles and can only be applied to Marketplace Silver plans.

This year, many people will qualify for both types of savings!

Why are subsidies more generous this year:

The American Rescue Plan Act increased the amount of APTC and CSR available to a household, and it also expanded the eligibility for these subsidies.

Silver plans vs. other metal levels:

All Marketplace health insurance plans are broken into five types: Platinum, Gold, Silver, Bronze and Catastrophic. You can expect the same level of care fromall metal levels. The difference is how your healthcare costs will be split between you and the insurance company. Metal levels Premium Platinum Highest Gold Silver Bronze Catastrophic Deductible Higher Middle Lower Lowest Lower Middle Higher Highest. If you are eligible for a CSR, you must choose a Silver plan!

On November 12, 2021, the Centers for Medicare & Medicaid Services (CMS) released the 2022 premiums, deductibles, and coinsurance amounts for the Medicare Part A and Part B programs, and the 2022 Medicare Part D income-related monthly adjustment amounts.

Medicare Part B Premium and Deductible

Medicare Part B covers physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A.

Each year the Medicare Part B premium, deductible, and coinsurance rates are determined according to the Social Security Act. The standard monthly premium for Medicare Part B enrollees will be $170.10 for 2022, an increase of $21.60 from $148.50 in 2021. The annual deductible for all Medicare Part B beneficiaries is $233 in 2022, an increase of $30 from the annual deductible of $203 in 2021.

The increases in the 2022 Medicare Part B premium and deductible are due to:

Rising prices and utilization across the health care system that drive higher premiums year-over-year alongside anticipated increases in the intensity of care provided.

Congressional action to significantly lower the increase in the 2021 Medicare Part B premium, which resulted in the $3.00 per beneficiary per month increase in the Medicare Part B premium (that would have ended in 2021) being continued through 2025.

Additional contingency reserves due to the uncertainty regarding the potential use of the Alzheimer’s drug, Aduhelm™, by people with Medicare. In July 2021, CMS began a National Coverage Determination analysis process to determine whether and how Medicare will cover Aduhelm™ and similar drugs used to treat Alzheimer’s disease. As that process is still underway, there is uncertainty regarding the coverage and use of such drugs by Medicare beneficiaries in 2022. While the outcome of the coverage determination is unknown, our projection in no way implies what the coverage determination will be, however, we must plan for the possibility of coverage for this high cost Alzheimer’s drug which could, if covered, result in significantly higher expenditures for the Medicare program.

Medicare Open Enrollment and Medicare Savings Programs

Medicare Open Enrollment for 2022 began on October 15, 2021, and ends on December 7, 2021. During this time, people eligible for Medicare can compare 2022 coverage options between Original Medicare, and Medicare Advantage, and Part D prescription drug plans. In addition to the recently released premiums and cost sharing information for 2022 Medicare Advantage and Part D plans, the Fee-for-Service Medicare premiums and cost sharing information released today will enable people with Medicare to understand all their Medicare coverage options for the year ahead. Medicare health and drug plan costs and covered benefits can change from year to year, so people with Medicare should look at their coverage choices annually and decide on the options that best meet their health needs.

To help with their Medicare costs, low-income seniors and adults with disabilities may qualify to receive financial assistance from the Medicare Savings Programs (MSPs). The MSPs help millions of Americans access high-quality health care at a reduced cost, yet only about half of eligible people are enrolled. The MSPs help pay Medicare premiums and may also pay Medicare deductibles, coinsurance, and copayments for those who meet the conditions of eligibility. Enrolling in an MSP offers relief from these Medicare costs, allowing people to spend that money on other vital needs, including food, housing, or transportation. People with Medicare interested in learning more can visit: https://www.medicare.gov/your-medicare-costs/get-help-paying-costs/medicare-savings-programs.

Medicare Part B Income-Related Monthly Adjustment Amounts

Since 2007, a beneficiary’s Part B monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 7 percent of people with Medicare Part B. The 2022 Part B total premiums for high-income beneficiaries are shown in the following table:

Beneficiaries who file individual tax returns with modified adjusted gross income:

Beneficiaries who file joint tax returns with modified adjusted gross income:

Income-related monthly adjustment amount

Total monthly premium amount

Less than or equal to $91,000

Less than or equal to $182,000

$0.00

$170.10

Greater than $91,000 and less than or equal to $114,000

Greater than $182,000 and less than or equal to $228,000

68.00

238.10

Greater than $114,000 and less than or equal to $142,000

Greater than $228,000 and less than or equal to $284,000

170.10

340.20

Greater than $142,000 and less than or equal to $170,000

Greater than $284,000 and less than or equal to $340,000

272.20

442.30

Greater than $170,000 and less than $500,000

Greater than $340,000 and less than $750,000

374.20

544.30

Greater than or equal to $500,000

Greater than or equal to $750,000

408.20

578.30

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

Beneficiaries who are married and lived with their spouses at any time during the year, but who file separate tax returns from their spouses, with modified adjusted gross income:

Income-related monthly adjustment amount

Total monthly premium amount

Less than or equal to $91,000

$0.00

$170.10

Greater than $91,000 and less than $409,000

374.20

544.30

Greater than or equal to $409,000

408.20

578.30

Medicare Part A Premium and Deductible

Medicare Part A covers inpatient hospital, skilled nursing facility, hospice, inpatient rehabilitation, and some home health care services. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

The Medicare Part A inpatient hospital deductible that beneficiaries pay if admitted to the hospital will be $1,556 in 2022, an increase of $72 from $1,484 in 2021. The Part A inpatient hospital deductible covers beneficiaries’ share of costs for the first 60 days of Medicare-covered inpatient hospital care in a benefit period. In 2022, beneficiaries must pay a coinsurance amount of $389 per day for the 61st through 90th day of a hospitalization ($371 in 2021) in a benefit period and $778 per day for lifetime reserve days ($742 in 2021). For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $194.50 in 2022 ($185.50 in 2021).

Part A Deductible and Coinsurance Amounts for Calendar Years 2021 and 2022 by Type of Cost Sharing

2021

2022

Inpatient hospital deductible

$1,484

$1,556

Daily coinsurance for 61st-90th Day

$371

$389

Daily coinsurance for lifetime reserve days

$742

$778

Skilled Nursing Facility coinsurance

$185.50

$194.50

Enrollees age 65 and over who have fewer than 40 quarters of coverage and certain persons with disabilities pay a monthly premium in order to voluntarily enroll in Medicare Part A. Individuals who had at least 30 quarters of coverage or were married to someone with at least 30 quarters of coverage may buy into Part A at a reduced monthly premium rate, which will be $274 in 2022, a $15 increase from 2021. Certain uninsured aged individuals who have less than 30 quarters of coverage and certain individuals with disabilities who have exhausted other entitlement will pay the full premium, which will be $499 a month in 2022, a $28 increase from 2021.

Medicare Part D Income-Related Monthly Adjustment Amounts

Since 2011, a beneficiary’s Part D monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 8 percent of people with Medicare Part D. These individuals will pay the income-related monthly adjustment amount in addition to their Part D premium. Part D premiums vary from plan to plan and roughly two-thirds are paid directly to the plan, with the remaining deducted from Social Security benefit checks. The Part D income-related monthly adjustment amounts are all deducted from Social Security benefit checks. The 2022 Part D income-related monthly adjustment amounts for high-income beneficiaries are shown in the following table:

Beneficiaries who file individual tax returns with modified adjusted gross income:

Beneficiaries who file joint tax returns with modified adjusted gross income:

Income-related monthly adjustment amount

Less than or equal to $91,000

Less than or equal to $182,000

$0.00

Greater than $91,000 and less than or equal to $114,000

Greater than $182,000 and less than or equal to $228,000

12.40

Greater than $114,000 and less than or equal to $142,000

Greater than $228,000 and less than or equal to $284,000

32.10

Greater than $142,000 and less than or equal to $170,000

Greater than $284,000 and less than or equal to $340,000

51.70

Greater than $170,000 and less than $500,000

Greater than $340,000 and less than $750,000

71.30

Greater than or equal to $500,000

Greater than or equal to $750,000

77.90

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

Beneficiaries who are married and lived with their spouses at any time during the year, but file separate tax returns from their spouses, with modified adjusted gross income:

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

He’s one of a slew of pitchmen and women selling Medicare Advantage plans to the more than 54 million Americans 65 or over eligible for Medicare. That includes more than 100,000 of us in Orange, Ulster and Sullivan counties.

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

Those pitches, which also flood our mailboxes during this enrollment period that ends Dec. 7, complicate what can be a mind-boggling array of insurance choices.

First, some basic facts:

Medicare Advantage is the all-in-one alternative to original Medicare health insurance. Original Medicare includes coverage for hospitalization (Part A), medical visits and procedures (Part B) and, at additional cost, prescription drugs (Part D). Before you enroll in Advantage plans, you must have original Medicare, and you still must pay the Part B premium of $148.50 (in 2021). While Medicare Advantage plans include medical, hospital and drug coverage, they can also feature extra benefits not offered by traditional Medicare, such as dental, hearing and vision coverage with no additional premium.

Especially in those pitches from celebrities like Namath, William Shatner and Jimmie Walker, they can also promise everything from free meal delivery to money deposited in your Social Security account.

But …

“Buyer beware,” says Erinn Braun, Orange County Office for the Aging’s Health Insurance Counseling and Assistance Program coordinator. She provided much information for this column.

Pitches like Namath’s can be misleading or downright deceptive, starting with the red, white and blue colors that insinuate the ads are from the government, as do the state logos on some mailers. While the plans themselves are perfectly legal and may be great for many of the 27 million Americans enrolled in them, they often don’t deliver everything those pitches seem to promise. Plus, those pitches don’t come close to telling the full story of the benefits of those plans – many of which aren’t even offered in your area.

For instance:

Unlike original Medicare, which is accepted by virtually all doctors and hospitals, Medicare Advantage plans include a network of doctors and hospitals you must visit to be insured. So if you hear about a great gastroenterologist in New York City and she isn’t in your Advantage plan’s network, your insurance may not cover your visit. Plus, unlike original Medicare, you may need prior approval for coverage of a medical procedure or equipment such as insulin pumps.

And while the dental and vision coverage of Medicare Advantage plans sounds great, some plans in your area may only include routine visits, not more expensive items like dental implants and eyeglasses. Plus, the average yearly coverage limit of Advantage dental plans ranges from about $1,000 to $1,300, according to the Kaiser Family Foundation. The dentists and eye doctors you visit must also be in the plan’s networks – meaning your eye doctor or dentist may not accept your plan.

Steve Israel

As for those meals and money Joe Willie is pitching?

Again, buyer beware.

A few Advantage plans may offer meal delivery for the qualified but only one or two plans in your county may offer those benefits. And your doctors or hospital may not accept those plans. Same thing goes for that money Namath says could go into your Social Security account. Not only does that money go toward the required payment for Part B of original Medicare, very few plans – if any – in your area may feature that benefit, and those plans may not include your doctors.

Finally, when you call the number provided by Namath and other pitch folks, you’ll reach a salesperson who’s in business to … you guessed it … sell you a Medicare Advantage plan.

For help selecting the right Medicare plan for you, contact your county’s Office of the Aging. Orange: 845-615-3710, Sullivan: 845-807-0241, Ulster: 845-340-3456. A trusted health insurance agent can also help. Medicare.gov and 1-800-Medicare provide a wealth of information.

By D. Kenton Henry Editor, Agent, Broker 29 October 2018

The media is proffering all manner of good news when it comes to the Open Enrollment Period for purchasing 2019 individual and family health insurance, just three days away. The doors open this Thursday, November 1st and will remain so through December 15th. During this time you, the consumer, will be able to review your options and make a decision to renew your existing policy or select a new one to become effective January 1. Whichever, that policy will cover you the coming calendar year.

The feature article appearing below, states there will be ” . . . fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.” To wit, it cites, the budget for insurance counselors, known as navigators, has been cut by 80%, leaving over one-third of navigators in 2,400 counties served by Healthcare.gov, unfunded. Thank you very much, New York Times. Somehow, they neglected to consult with me and my agency, ALL PLAN MED QUOTE. Reading the article in full, one can infer they feel the only meaningful assistance can come from the government (at taxpayers’ expense) and fail to credit the private industry, which has provided counsel and enrollment assistance within the domestic insurance industry some two hundred years plus. One token sentence in the article acknowledges the private industry’s presence to assist the consumer with procuring health insurance. In my estimation, this reflects the media’s general opinion and thesis that the government is the end-all solution to every conceivable personal financial issue. Which, again, in the mind of this editor, is precisely the philosophy, the perpetuation of which got us into this fix in the first place. Moreover, what exactly is that fix?

Current pre-midterm election media coverage informs us premiums have stabilized and are, in many cases, going down in 2019. While that may be true in some localities, the recently released premiums in southeast Texas reflect increases of 20% or more. If you obtain a subsidy, wherein you get a tax credit for a portion of your premium, the subsidy itself may be larger, but the balance may be as well. Also, for those not obtaining a subsidy (the vast majority of us) the increase will be born entirely by ourselves. The situation has made healthcare the number one concern of Americans heading into next week’s midterm elections according to a Fox News Poll.

For the record, ALL PLAN MED QUOTE and I have never been subsidized by taxpayer dollars. As an independent, self-employed broker/agent I am compensated when I successfully enroll someone in health insurance. I am not compensated when I fail at such. That is fine by me. In spite of continual cuts in agent compensation. I prefer autonomy to bureaucracy. My advice and guidance are objective. My goal is to succeed it getting you enrolled in a policy which makes sure you have access to the care and treatment you need, when you need it and are not financially devastated in the process. All this for the lowest possible premium. I do not care which insurance company you contract with, as long as you are satisfied you have obtained the best coverage for your given situation and needs. Ideally, it would also provide you access to all the doctors and medical providers you choose to utilize. Regrettably, that latter objective has become my biggest challenge and is one every insurance agent and counselor faces. To say it can be overcome in every instance would be misleading but I do my best. All 2019 individual and family options are Health Maintenance Organizations (HMO) policies, and this has been so since 2016. The HMO networks are narrow in comparison to what one may typically have experienced with employer-based HMO coverage. However, there are a very few plans (3 in my primary region) which operate very similar to a traditional Exclusive Provider Organization (EPO) policy in that they do cover treatment at a provider outside the network. Benefits are paid up to a limited percentage, and there is no cap on your maximum annual out-of-pocket but―for someone who wants to be assured they can obtain coverage from the provider of their choice―it is better than no coverage whatsoever. If you feel you must learn more about this option, please contact me.

To assist me in these ends, I am appointed with every company providing Patient Protection and Affordable Care Act-compliant health insurance company doing business in Montgomery, Harris, Fort Bend, and Galveston counties. BlueCross BlueShield of Texas (to my knowledge) does business in every corner of Texas, and I have been appointed with them twenty-seven years. In addition to Texas, I am licensed in Indiana, Michigan, and Ohio.

I offer short-term health insurance for those who do not get a subsidy and those who, whether they do or not, cannot afford credible health insurance. However, I do not represent it as covering pre-existing health conditions, as it does not. Nor do I represent it as a substitute for credible, compliant coverage. It is a short-term bridge to a long-term solution.

As always, the Open Enrollment Period will be a very busy and hectic time for anyone in my profession. To make things proceed more smoothly, I would appreciate you visit my quoting site to obtain spreadsheet comparison of your options from all the health insurance companies offering coverage in your county. Attempt to narrow your selection down to those plans you feel most closely approximate the coverage you need. You can search for in-network providers from the search button directly next to the premium quoted. If you are so confident a plan is right for you, please feel free to apply straight from the quote. However, many of you will have questions or appreciate my insight and experience with the plan details and application process. Those in need of a subsidy will find my assistance especially helpful. If this is you, please do not hesitate to contact me.

Again, for quotes and applications, you may go to my website at Http://TheWoodlandsTXHealthInsurance.com and click on “Health” in the top menu.

Alternatively, you may go directly to my spreadsheet quotes and an application by clicking on this link: https://allplanhealthinsurance.insxcloud.com

*(it is not necessary to log in or register to obtain quotes or apply)

**(if these links do not function from this text, please copy and paste or type in your browser and hit enter)

If you apply for coverage through these links, I will be your agent and available to assist and commit to providing the best of service throughout the year. I bring my entire thirty-two years in medical insurance to bear for this purpose. I look forward to hearing from you and assisting you. Regardless, I hope you succeed in obtaining health insurance which suffices until Congress puts their heads together and provides us with more reasonable options.

D. Kenton Henry All Plan Med Quote Office: 281.367.6565 Text my cell @ 713.907.7984 Email: Allplanhealthinsurance.com For the latest in health and Medicare-related insurance, news go to Https://HealthandMedicareInsurance.com

************************************************************************************************ FEATURED ARTICLE

The New York Times By Robert Pear Oct. 27, 2018

Shopping for Insurance? Don’t Expect Much Help Navigating Plans

Affordable Care Act navigators helping patients during an enrollment event in 2016 at Southwest General Hospital in San Antonio.CreditCreditEric Gay/Associated Press

WASHINGTON — When the annual open enrollment period begins in a few days, consumers across the country will have more choices under the Affordable Care Act, but fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.

The Trump administration has opened the door to aggressive marketing of short-term insurance plans, which are not required to cover pre-existing medical conditions. Insurers are entering or returning to the Affordable Care Act marketplace, expanding their service areas and offering new products. But the budget for the insurance counselors known as navigators has been cut more than 80 percent, and in nearly one-third of the 2,400 counties served by HealthCare.gov, no navigators have been funded by the federal government.

“There is likely to be a lot of consumer confusion about the various plan options that may be available this year,” said Sabrina Corlette, a research professor at Georgetown University’s Health Policy Institute. “It will be a bit of a Wild West — buyer beware!”

“Obamacare health plans,” short-term plans and “Christian health sharing plans” are all displayed on the same page of some shopping sites like Affordable-Health-Insurance-Plans.org, which describes itself as a free referral service for insurance shoppers.

ADVERTISEMENT

Consumers may have difficulty sorting through their options after the administration sliced the budget last summer for insurance navigators to $10 million this year, from $36 million in 2017 and nearly $63 million in 2016.

“Navigators play a vital role in helping consumers prepare applications to establish eligibility and enroll in coverage through the marketplaces,” the Department of Health and Human Services says on its website.

But 797 counties served by HealthCare.gov will not have any navigators this year, according to a tabulation of federal data by the Kaiser Family Foundation. That is a sharp increase from 2016, when 127 counties lacked such assistance.

“If you are confused and you want somebody’s help to try to figure out what’s right for you — what’s junk and what is legitimate — there will be fewer people to help you in most states,” Ms. Corlette said.

Federal officials said they were not providing funds for navigators in Iowa, Montana or New Hampshire because no organizations had applied for the money in those states.

Cleveland, Dallas and large areas of Michigan and other states will also be without navigators.

Texas will be hit hard. The state has the largest number and the highest percentage of people who are uninsured, with 4.8 million people, or 17 percent of residents, lacking coverage, according to the Census Bureau.

“North Texas remains one of the most uninsured areas in the country,” said the chief executive of Dallas County, Judge Clay Lewis Jenkins. “The administration’s decision to defund all navigators across North Texas will hurt our ability to enroll individuals in health insurance and result in some working families losing coverage. Only 45 of Texas’ 254 counties have any navigator coverage.”

Seema Verma, the administrator of the Centers for Medicare and Medicaid Services, defended the cuts.

After five years, she said, “the public is more aware of the options for private coverage” available through the marketplace, so “it is appropriate to scale down the navigator program.” In addition, she said, information and assistance are available from other sources, including insurance agents and brokers.

Consumers can sign up for health insurance under the Affordable Care Act starting Thursday. Last year, 8.7 million people enrolled at HealthCare.gov, and three million more selected plans on insurance exchanges run by states.

Consumers can go without insurance next year without fear of a penalty, as Congress repealed the unpopular tax surcharge imposed on people who lack coverage.

Many health policy experts say that federal financial assistance is more important than the individual mandate in inducing people to buy insurance. Those subsidies will still be available to low- and moderate-income people for insurance that complies with the Affordable Care Act and is purchased through the public marketplace. The subsidies cannot be used for short-term policies.

The vast majority of the people we serve, over 90 percent, are motivated to have insurance because they want coverage for their family and themselves,” said Matthew Slonaker, the executive director of the Utah Health Policy Project, a nonprofit. “It’s not because they otherwise would have to pay a penalty.”

Average premiums for the most popular types of insurance purchased by individuals and families will be relatively stable next year and, in some states, will actually decline, the administration says.

Under new standards issued by the administration, navigators this year are encouraged to inform consumers of the full range of coverage options, including short-term plans that do not provide all of the benefits and consumer protections required by the Affordable Care Act.

President Trump has promoted the short-term policies as an inexpensive alternative to the Affordable Care Act, and he said those plans would be “much more widely available” as a result of an executive order he signed last year to overturn restrictions imposed by President Barack Obama.

Democrats have made health care a major theme in midterm election campaigns, and they say the short-term policies show how the Trump administration threatens protections for people with pre-existing conditions.

Short-term policies, which can extend up to 364 days and then be renewed for two additional years, often provide no coverage for pre-existing conditions, prescription drugs, pregnancy, maternity care or the treatment of mental disorders and drug abuse.

Indeed, Mr. Trump said, the short-term plans are cheaper because they are “not subject to any very expansive and expensive Obamacare coverage mandates and rules.”

ADVERTISEMENT

But, said Kirsten A. Sloan, a vice president of the American Cancer Society Cancer Action Network: “People may be attracted to short-term plans without understanding that the lower premiums come with less coverage. These plans may not cover the doctors and hospitals and drugs you need if you get sick.”

In another challenge this year, consumers may be deluged with robocalls offering cheap insurance.

Alex Quilici, the chief executive of YouMail, a company that offers software to combat robocalls, said he was seeing a huge increase in health insurance scams.

“Callers say ‘it’s open enrollment’ or ‘we can get you a better deal by looking at all the health insurance plans,’” Mr. Quilici said. “Callers ask for lots of personal information, and the unwitting consumer often gives their birth date, Social Security number and information for everybody in the family, in order to get a great deal. In reality, it’s identity theft or payment theft or both.”

Mr. Quilici’s company has recorded hundreds of robocalls. A typical call says that, with enrollment just “around the corner,” Mr. Trump has created short-term coverage options lasting up to three years, “so you and your family can get a great insurance plan at the price you can afford.”

It is difficult to identify the source of the robocalls, Mr. Quilici said, because callers often falsify information displayed on caller ID.

(A version of this article appears in print on Oct. 27, 2018, on Page A25 of the New York edition with the headline: Shopping for Health Insurance: Many Options but Little Guidance. Order Reprints | Today’s Paper | Subscribe)

Shortly after 1:30 a.m. Friday, July 28th, the U.S. Senate voted 49-51 to reject the Health Care Freedom Act (HCFA), a “skinny repeal” of the ACA. The pared-down version was attempted after previous efforts to pass a more sweeping repeal of the law have failed. Senate Majority Leader Mitch McConnell (R-KY) began floating the idea early in the week before ultimately releasing the text of the bill at 10 p.m. Thursday, just two hours before the vote. Republican Senators Susan Collins (ME), Lisa Murkowski (AK), and John McCain (AZ) joined all Democrats in voting no, while all other Republicans voted in favor. With the failure of this vote, congressional Republicans will no longer be able to use the budget reconciliation process to repeal provisions of the ACA until the next fiscal year and will instead have to move legislation under regular order that would require 60 votes for passage in the Senate. ― NAHU 7/28 (washingtonupdate@nahu.org)

Anyone who tells you they know what the next few months before health insurance OPEN ENROLLMENT (OE)―the period during which individuals and families may apply for and obtain coverage for the coming calendar year―will produce definitively, is deluding themselves. OE is scheduled to begin November 1 and run through December 7th. At this point, the only safe prediction is the preservation of the status quo. In other words, premiums will increase another 15 to 25% minimum; there will be fewer options regarding carriers and plans and fewer in-network medical providers from which to choose. In some parts of the country, it will be even worse, with only one carrier to choose from and―in some cases ― none. Whether that will be the case in Texas remains to be seen.

Here is what we do know:

1) Premiums will increase significantly in most areas

2) In the area of Houston, one more carrier―Memorial Hermann Health Plan―has announced they are withdrawing from the market. All of their current policyholders must find replacement coverage for 2018.

3) Humana has canceled all their current individual and family plans effective July 1 and will not participate in the market in 2018. This is in addition to Aetna, Cigna’s and Unitedhealthcare’s withdrawal from the market in 2017.

4) Residents of Harris, Fort Bend, and Montgomery Counties will (hopefully) have only plans from BlueCross BlueShield of Texas, Community Health Choice, and Molina Healthcare from which to choose.

5) The only remaining network option available from the above-referenced carriers will be Health Maintenance Organization (HMO) plans where the insured individual must seek treatment within the network or have no coverage whatsoever.

Here is an important change this editor (who is also a health insurance broker) recently learned. Married couples who are small business owners seeking Preferred Provider Organization (PPO) coverage as a way of having access to providers and treatment―will no longer be eligible for coverage with most (if not all) small group carriers unless they had a minimum average of one W-2 employee in the previous calendar year. This new stipulation would have prevented many of my business owner clients from obtaining the group PPO health insurance they now have, had it been in effect before January 1 of 2017. A prospective client of mine whose family coverage was canceled by Humana, July 1―in the midst of cancer treatment―now finds himself denied covered access to his oncologist and hospital. It appears all ongoing medical treatment from those providers, at least through the remainder of the year, will be self-funded. If you are a small business owner considering moving to group insurance in 2108, bear this in mind and begin paying at least one employee W-2, full time, through the remainder of 2017.

Small business owners considering a move to small group coverage who can meet this eligibility requirement, please contact me for assistance in making the transition.

For individuals and families who do not have a business, or employer sponsored health insurance, I will have whatever health insurance options are available to residents of your county and will soon begin testing and certifying (as I must each fall) to market these plans for the coming calendar year. I will be able to assist you whether you qualify for a subsidy of your health insurance premium or do not. If you do, I believe it will be much easier to obtain your subsidy and health insurance through me than by dealing with the marketplace, Healthcare.gov. If you do not qualify for a one, I have a strategy for minimizing your premium while giving you access to the provider of your choice. It is not appropriate for everyone, but it has worked for many of my clients.

Please contact me at 281-367-6565; text me at 713-907-7984, or email me at allplanhealthinsurance.com@gmail.com

Though I see little reason to be optimistic for a solution to the aforementioned problems until the Patient Protection and Affordable Care Act (Obamacare) implodes entirely, and Congress is forced to unite to provide a workable solution, let’s hope enough reasonable minds prevail before it comes to that. In the meantime, I am here to assist in acquiring the best available option, as I have for the past 26 years.

Senate Republican leaders signaled Monday that they intend to move on from health care to other legislative priorities, even as President Trump continued to pressure lawmakers to repeal and replace the Affordable Care Act.

The discord comes amid uncertainty in the insurance industry and on Capitol Hill about what will come next after last week’s dramatic collapse of the GOP’s effort to scrap the seven-year-old landmark law. Trump on Monday threatened to end subsidies to insurers and also took aim at coverage for members of Congress.

But the White House insistence appears to have done little to convince congressional GOP leaders to keep trying. One after another on Monday, top GOP senators said that with no evidence of a plan that could get 50 votes, they were looking for other victories.

“We’ve had our vote, and we’re moving on to tax reform,” said Sen. John Thune (S.D.), one of Senate Majority Leader Mitch McConnell’s top lieutenants, speaking of the next big GOP legislative priority.

Sen. Roy Blunt (Mo.), another member of the Republican Senate leadership, put it this way: “I think it’s time to move on to something else. Come back to health care when we’ve had more time to get beyond the moment we’re in — see if we can’t put some wins on the board.”

McConnell did not address health care in his remarks opening Senate business on Monday afternoon. His top deputy, Sen. John Cornyn (Tex.), brushed back comments White House budget director Mick Mulvaney made on CNN on Sunday urging Republicans not to vote on anything else until voting on health care again.

“I don’t think [Mulvaney’s] got much experience in the Senate, as I recall,” said Cornyn as he made his way into the Senate chamber. “And he’s got a big job. He ought to do that job and let us do our job.”

Mulvaney was echoing what Trump tweeted Saturday: “Unless the Republican Senators are total quitters, Repeal & Replace is not dead! Demand another vote before voting on any other bill!”

On Monday, Trump tweeted: “If Obamacare is hurting people, & it is, why shouldn’t it hurt the insurance companies & why should Congress not be paying what public pays?” He was referencing subsidies that members of Congress receive to help offset their coverage costs purchased through the District’s exchanges, as required under the Affordable Care Act.

Sen. Rand Paul (R-Ky.) said Monday that based on a conversation he had with Trump, the president is considering taking executive action on health care, Reuters reported. A Paul spokesman did not immediately respond to a request for comment, and it was not clear what such an action could be. Health and Human Services Secretary Tom Price indicated over the weekend that he was considering using his regulatory authority to waive the Affordable Care Act’s mandate that all Americans buy coverage or pay a tax.

Some rank-and-file Republican lawmakers have used the collapse of repeal-and-replace to offer new fixes and improvements to health care, but there was no sign their leaders were engaged. On Monday, Price met with fellow physician Sen. Bill Cassidy (R-La.), who has proposed restructuring how federal money is distributed under the Affordable Care Act. Separately, a bipartisan group of 43 House members released details of their own plan.

“We had a productive meeting. All involved want a path forward,” said Cassidy in a statement after his White House meeting, also attended by several governors. In addition to turning over federal funds to the states, Cassidy and Sens. Lindsey O. Graham (R-S.C.) and Dean Heller (R-Nev.) have proposed repealing key mandates and a tax under the law.

But there are no signs that plan will be put to a vote any time soon. It has not been scored by the nonpartisan Congressional Budget Office. It’s unclear how many Republicans would vote for it. And McConnell is working on confirming Trump’s nominees this week.

A growing number of Republican lawmakers have raised the prospect of working with Democrats on health care. The collection of centrist House Republicans and Democrats unveiled a proposal Monday calling for revisions they said would help stabilize the individual insurance market.

Rep. Tom Reed (R-N.Y.), a co-chair of the centrist Republican and Democratic “Problem Solvers Caucus,” which released the plan, said he and his colleagues have been working on a draft for about three weeks, as they saw “the writing on the wall” that the Senate bill was likely to fail.

House Speaker Paul D. Ryan (R-Wis.) did not champion the plan. AshLee Strong, his press secretary, said in an email: “While the speaker appreciates members coming together to promote ideas, he remains focused on repealing and replacing Obamacare.”

Strong did not respond to a follow-up question about how that ought to happen. The House passed a sweeping rewrite of the Affordable Care Act this year, with only Republicans voting for it.

The Senate tried to pass its own version but was unable to reach an accord, even on a more modest bill that was meant to keep the talks alive in both chambers. That bill was rejected Friday when Sen. John McCain (R-Ariz.) joined two other Republicans to sink the legislation in a tension-filled vote that happened while most of the country was asleep.

In their outline, Reed and his colleagues said federal cost-sharing subsidies should be placed under congressional oversight and that mandatory funding should be assured. Now such disbursements are up to the Trump administration, which has been paying them monthly but has threatened to withhold them.

Top Democrats and Republicans warned against that.

“Right now, as insurers prepare to lock in their rates and plans for 2018, the Trump administration is dangling a massive sword of Damocles over the heads of millions of Americans — threatening to end payments the administration is supposed to make that would lower deductibles and out-of-pocket costs for so many Americans,” said Senate Minority Leader Charles E. Schumer (D-N.Y.) on the Senate floor.

Thune said he was “hopeful” the administration would keep making the payments.

After Friday’s vote, some Democrats have felt more empowered to talk about changes to the Affordable Care Act. The centrist House lawmakers want to repeal the 2.3 percent tax on medical device manufacturers and loosen the employer mandate under the Affordable Care Act. The law says companies with 50 or more full-time employees must offer coverage. They want to raise the threshold to 500.

They also said they want to create a state stability fund to reduce premiums and spur more innovation at the state level.

Getting health-care legislation backed only by Republicans to Trump’s desk by the end of August is all but impossible, even if they suddenly put aside their disagreements. The House is in recess until September. The Senate is scheduled to be in session the first two weeks of August.

The prospects of a bipartisan deal were just as doubtful, amid fierce partisanship that has gripped the Capitol in the Trump era, which has shown no signs of abating. Even those pushing for one were tempering expectations.

“We’re not stupid,” Reed said. “Those partisan swords — they’re going to be out there.”

Paige Winfield Cunningham contributed to this report

Perhaps a storm would be a better analogy but 2016 will deliver something more than a mild tropical depression to the coast of the “Individual and Family” health insurance market. At the same―the Cat 3 (minimum) hurricane projected to slam the Senior market of Medicare recipients appears to have been diverted. For now.

As we enter the third year of enrollment in health insurance plans compliant with the Affordable Care Act (ACA) the “Affordable” aspect of care or―more accurately―the cost of protecting oneself from the cost of health care―seems elusive and more and more a case of misrepresentation. As I have said many times in the past, if you qualify for a subsidy of your health insurance premiums you may find your options affordable. However, depending on where you live, you will surely be upset with the increasing cost of health insurance. 70% of all Obamacare members are enrolled in a Silver Plan. The Department of Health and Human Services (DHS), which oversees enforces the Act and oversees the health insurance industry, has designated the second lowest cost Silver Plan of any insurance company to be the default plan one must select in order to maximize the benefit of any subsidy. This could include a reduction in not only one’s premium but their deductibles and co-pays. As Fox News and the Washington Post report (see featured article below) the cost of these plans will rise by a national average of 7.5%. States such as Oklahoma will see an increase of 37.5%!

In some states it is much worse.