By D. Kenton Henry, Editor, Broker, Agent

Each year Medicare recipients and their agents and brokers prepare for upcoming changes in Medicare. This is because all changes have the potential to impact the member’s pocketbook. They may directly affect it or trickle down to the products they use to supplement Medicare.

Here is what we know is changing:

In 2017 you pay:

$1,288 Medicare deductible for each benefit period

• Days 1-60: $0 coinsurance for each benefit period

• Days 61-90: $322 coinsurance per day of each benefit period

• Days 91 and beyond: $644 coinsurance per each “lifetime reserve day” after day 90 for each benefit period (up to 60 days over your lifetime)

Beyond lifetime reserve days: all costs

In 2018 you will pay:

$1,316 Medicare deductible for each benefit period

• Days 1-60: $0 coinsurance for each benefit period

• Days 61-90: $329 coinsurance per day of each benefit period

• Days 91 and beyond: $658 coinsurance per each “lifetime reserve day” after day 90 for each benefit period (up to 60 days over your lifetime)

• Beyond lifetime reserve days: all costs

PART B DEDUCTIBLE:

The Medicare Part B deductible is $183 in 2017. It is expected to rise in 2018, but the Center For Medicaid and Medicare Services has not, and is not expected to, release that figure until closer to the end of this calendar year.

PART B PREMIUMS:

COST OF LIVING ADJUSTMENT (COLA), I.e., the Social Security Income Payment Adjustment, numbers for the coming year have not been released as of yet. But it’s widely expected that there will be a COLA of around 2 percent for 2018 (as opposed to 0.3 percent for 2017, and zero percent for 2016). CMS has not yet set Part B premiums for 2018, but it’s likely that premiums will level out for all enrollees (except those with high incomes, who always pay more). This because any necessary rate change will be covered by the COLA. In other words, the increase in Part B premiums will be offset by an increase in income payments for low-income recipients.

For high-income Part B enrollees (income over $85,000 for a single individual, or $170,000 for a married couple), premiums in 2017 range from $187.50/month to $428.60/month, depending on income. They will likely rise again for 2018, but there’s another change coming that will affect some high-income Part B enrollees in 2018. As part of the Medicare payment solution that Congress enacted in 2015 to solve the “doc fix” problem, new income brackets were created to determine Part B premiums for high-income Medicare enrollees, and they’ll take effect in 2018.

The high-income brackets start at $85,001 for a single individual and $170,001 for a married couple. Enrollees with income between $85,001 and $107,000 ($170,001 and $214,000 for a married couple) won’t see any changes to their bracket.

But enrollees with income above those limits might be bumped into a higher bracket in 2018, which means their premiums could jump considerably. The highest bracket (i.e., with the highest Part B premium) will now apply to those with income above $160,000 ($320,000 for a married couple), whereas the highest bracket didn’t apply in 2017 until an enrollee’s income reached $241,000 ($428,000 for a married couple). As with the deductible, Medicare Part B premiums for 2018 have not yet been set, but slightly less wealthy Medicare enrollees will begin paying the highest prices for Medicare Part B in 2018.

Here are Medicare Part B Premiums for 2017 (based on a 2-year look-back to 2015):

If your yearly income in 2015 (for what you pay in 2017) was You pay each month (in 2017)

File individual tax return File joint tax return Married Filing Separately

$85,000 or less $170,000 or less $85,000 or less = $134

above $85,000 up to $107,000 above $170,000 up to $214,000 N/A = $187.50

above $107,000 up to $160,000 above $214,000 up to $320,000 N/A = $267.90

above $160,000 up to $214,000 above $320,000 up to $428,000 N/A = $348.30

above $214,000 above $428,000 above $129,000 = $428.60

PART D PRESCRIPTION DRUG PLANS:

The Part D Annual Deductible is $405 in 2018, up from $400 in 2017

Premiums in the State of Texas, e.g., range from a low of $16.70 to a high of $197.10

* On the positive side, the Affordable Care Act is gradually closing the donut hole -technically known as the Gap – in Medicare Part D. In 2018, enrollees will pay just 35% of the plans cost for brand-name drugs while in the donut hole, and 44% of the cost of generic drugs.

2018 PART D COVERAGE GAP STAGE:

Begins after the total yearly drug cost (including what Your plan has paid and what you have paid) reaches $3,750. After you enter the coverage gap, you pay 35% of the drug cost for covered brand-name drugs and 44% of the drug cost for covered generic drugs until your out-of-pocket costs (not including your premiums) total $5,000, which is the end of the coverage gap. Not everyone will enter the coverage gap.

2018 Catastrophic Coverage Stage:

After your yearly out-of-pocket drug costs (including drugs purchased through your retail pharmacy and mail-order) reach $5,000, you pay the greater of:

• 5% of the cost, or

• $3.35 copay for generic drugs (including brand drugs treated as generic) and $8.35 copay for all other drugs.

*Tip of the 2018 Part D Open Enrollment Period:

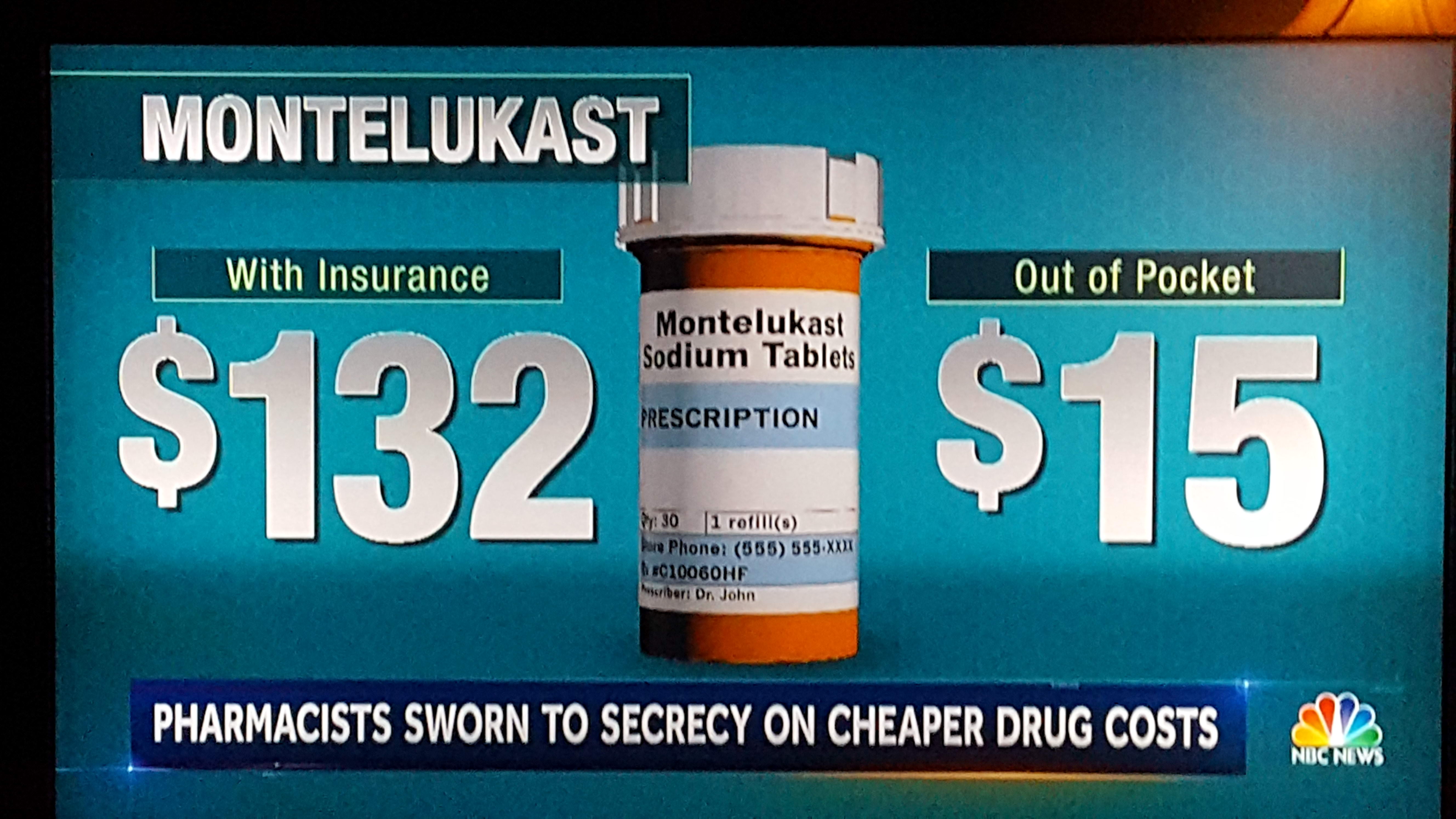

When purchasing your prescription drugs at the pharmacy counter, always ask your pharmacist for the lowest possible cost for your drug through their pharmacy. NBC Today Show did a segment today (10.17.17) in which they revealed that many times your copay for the drug, through your insurance, is higher than the lowest cost from the pharmacy. As the photo at the top of this article depicts, sometimes the difference is quite significant. A pharmacist in Magnolia, Texas, explained that a contractual “Gag” order exists between the pharmacy and the pharmacist (or employee) which prevents the latter from disclosing this to the customer. However, once questioned, the pharmacist or employee must disclose accurate information. If the cash price is lower, by all means, pay the cash price and do not let the purchase go through your insurance.

I will keep followers of my blog apprised of, as yet, unannounced changes in Medicare as they become available. In the meantime, to those of you who are my current clients, I would like to extend a sincere thank you for your business and the confidence you have placed in me.

ASSISTANCE IN IDENTIFYING YOUR LOWEST TOTAL COST PART D DRUG PLAN:

You, and those who would consider my services may email or―for those who feel it a more secure method―may fax a list of your prescription drugs and dosages to my secure fax. (I am the only one with access to it.) I will submit your drug regimen to the quoting system which will identify the plan which covers all your drugs at the lowest total cost for the coming calendar year. The lowest-total-cost is the sum of the plan premium, any applicable deductible, and your drug costs. Whether you elect to go through me to acquire it, is at your discretion.

Please email Kenton at:

allplanhealthinsurance.com@gmail.com

or

Fax to my secure fax at:

281.367.4772

I am processing quote requests in the order received.

Thank you so much for taking the time to stay abreast of these relevant changes affecting, and so important to, Medicare recipients. I know many of you are living on fixed incomes, and keeping your costs for protecting yourself from increases in medical care, and insurance, is of vital importance to you.

http://TheWoodlandsTXHealthInsurance.com https://HealthandMedicareInsurance.com