By D Kenton Henry, editor of HealthandMedicareInsurance.com, agent, and Independent Insurance Broker

When most people compare Medicare Advantage plans, they focus on premiums, dental benefits, vision coverage, hearing aids, grocery cards, or over-the-counter allowances.

Those benefits certainly have value. However, after nearly four decades in the health insurance business, I have found that the biggest differences between Medicare Advantage and Medicare Supplement plans often become apparent only when a beneficiary actually needs medical care.

As Medicare Advantage enrollment continues to grow and healthcare costs continue to rise, provider networks and prior authorization requirements are becoming increasingly important issues for Medicare beneficiaries.

Provider Networks Continue to Change

One of the primary advantages of a Medicare Supplement policy is flexibility.

Generally speaking, a Medicare Supplement policyholder may receive treatment from any physician or hospital in the United States that accepts Medicare patients.

Medicare Advantage plans operate differently.

Most Medicare Advantage plans utilize provider networks. Those networks may change from year to year as insurance companies renegotiate contracts with physicians, specialists, hospitals, and healthcare systems.

A doctor who participates this year may not participate next year.

A hospital system that is in-network today could become out-of-network in the future.

For beneficiaries who travel frequently, maintain residences in multiple states, or simply want maximum freedom in choosing healthcare providers, network changes can sometimes create unexpected challenges.

Prior Authorization Remains a Concern

Another issue receiving increased attention is prior authorization.

Many Medicare Advantage plans require advance approval before certain services are performed. These may include:

MRI scans

CT scans

Physical therapy

Skilled nursing facility care

Certain surgical procedures

Some specialty medications

The concern is not always whether a service is ultimately approved.

Rather, the concern is that treatment may be delayed while additional documentation is gathered and reviewed.

Physicians across the country have frequently expressed frustration regarding the administrative burden associated with prior authorization requirements.

By contrast, beneficiaries covered under Original Medicare with a Medicare Supplement policy generally encounter fewer authorization hurdles because Medicare itself determines coverage.

An Aging Population Means More Healthcare Utilization

The first wave of Baby Boomers entered Medicare in 2011.

Every year, Medicare beneficiaries grow older, utilize more healthcare services, and gain access to increasingly sophisticated—and expensive—medical treatments.

Insurance companies face growing pressure to control costs while keeping premiums competitive.

Common tools used to manage those costs include:

Narrower provider networks

Increased care management programs

Expanded prior authorization requirements

More intensive utilization review

These trends are unlikely to disappear anytime soon.

Rural Beneficiaries May Face Additional Challenges

Provider access can be especially important for beneficiaries living outside major metropolitan areas.

While beneficiaries in cities such as Houston, Dallas, Austin, or San Antonio may have numerous participating providers available, individuals living in smaller communities may have fewer options.

When specialty care is needed, network limitations can sometimes require additional travel or create fewer choices regarding where treatment is received.

A Medicare Supplement policy largely eliminates those concerns because coverage follows Medicare rather than a specific provider network.

The Hidden Value of Medicare Supplement Coverage

Consumers naturally focus on premium.

Insurance professionals often focus on risk and long-term flexibility.

When affordable, Medicare Supplement plans provide several advantages:

Predictability

Generally lower out-of-pocket exposure

Fewer surprise medical bills

Greater budgeting certainty

Provider Freedom

No network restrictions

No referrals required

Coverage that travels with you throughout the United States

Administrative Simplicity

Fewer authorization requirements

Less paperwork

Fewer coverage-related obstacles when seeking care

Medicare Advantage Still Has an Important Role

None of this means Medicare Advantage is a poor choice.

For many beneficiaries:

Monthly budgets are limited.

Medicare Supplement premiums may be unaffordable.

Health conditions may make medical underwriting difficult or impossible.

In those situations, Medicare Advantage plans can provide valuable protection at little or no additional premium.

The key is understanding the tradeoff.

Medicare Supplement

Higher monthly premium

Broad provider access

Minimal prior authorization concerns

Predictable healthcare costs With certain Medicare Supplement Plans (F and G) out-of-pocket costs–with the exception of RX drugs at the pharmacy counter–can be a little as $0 to Medicare’s current Part B out-patient calendare year deductible of $282

Medicare Advantage

Lower monthly premium

Network restrictions may apply

Prior authorization requirements are more common

Cost-sharing occurs as healthcare services are utilized If using an MAPD PPO and going both in and outside the network in 2026 your out-of-pocket maximum expenses can be over $13,000 with certain plans

Final Thoughts

As healthcare continues to evolve, I believe annual reviews are becoming more important than ever.

The Medicare Advantage plan that works well today may not be identical next year. Networks change. Benefits change. Drug formularies change.

For beneficiaries who can comfortably afford the premium and qualify for coverage, Medicare Supplement insurance continues to offer the broadest provider access, the greatest flexibility, and the fewest obstacles to receiving care.

As always, each individual’s circumstances are different. If you have questions about your Medicare coverage options, I encourage you to contact me for a personalized review.

D Kenton Henry Independent Medicare Insurance Broker Since 1986

By D. Kenton Henry Editor, Agent, Broker HealthandMedicareInsurance.com 11 September 2024

Welcome, fellow boomers and others blessed to have lived long enough to find yourself here. I believe you recognize that the information in my blog posts can contribute to this leg of our journey being the longest and most rewarding. I’m right here with you and doing my best to make it so for all of us. Coming changes in 2025 Medicare plans are significant, so please read this and feel free to take notes. They could impact you and probably will.

We will begin with what your Medicare Part B premium to Medicare for Out-Patient Care will go to: For those earning less than $105,000 your premium will go to $185.00 (up from $174.70) For those in the highest income bracket, earning greater than $500,000 your premium will go to $628.90 (from $594.00) For every income block in between, couples filing jointly, and what Part D premiums to Medicare will go to, please click on this link and scroll down: https://www.irmaacertifiedplanner.com/2025-irmaa-brackets/

An Annual Notice of Change (AOC) from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan is due you. It will arrive in the United States mail and, per Medicare rules, by September 30th. So, like the pretty woman in the image above, open it and read it. It outlines how much your premiums, deductibles, and co-pays will differ in the coming year. Will your drugs be covered, and will your current drug plan even be available? We don’t yet know. Mutual of Omaha notified agents and brokers that it is withdrawing altogether from the Part Drug plan market beginning January 1. If you are currently with them or have any other plan that is exiting the marketplace, follow the instructions in the next paragraph.

According to eHealth, a mere 36% of those surveyed claim the AOC to be “readily understandable.” The author of the attached article recommends you spend at least 30 minutes reviewing it. However, if you finish this article, you can cut that time considerably. If you have finished all and still feel you are among the remaining (up to) 64%—please call me @ 281-367-6565.

This article is a follow-up to my last blog post on September 3rd. “MAJOR CHANGES IN MEDICARE PART D DRUG PLANS ARE COMING OUR WAY (what we know. and one thing we don’t know).” To read it, please click on this link. (if necessary, copy and paste it in your browser’s URLbox and hit enter):

Well, now we know more of the potential compromises mentioned or alluded to in that article. All of these are covered in detail in Feature Article 1 below.

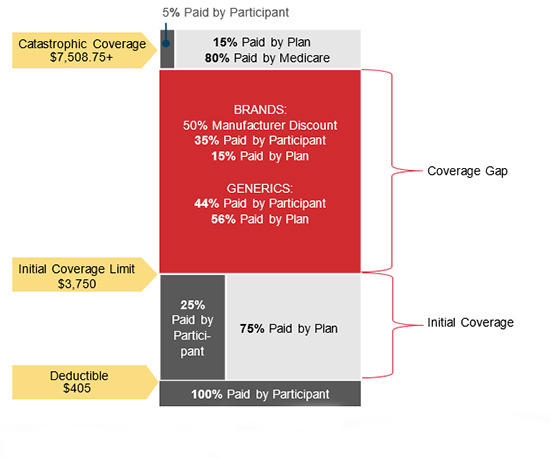

The changes addressed here are largely because of the new $2,000 per year limit on Medicare Part D drug costs in 2025 (versus $8,000, plus 5% thereafter, in 2024). That leaves Medicare Part D insurance companies looking for ways to compensate for the additional costs shifting from you to them. Come January, you will meet a new deductible of up to $590 (from $545) for applicable drugs. Typically, your plan will apply this to brand-name drugs and not Tier 1 or Tier 2 generics.

Beyond that, the Gap, commonly referred to as the “donut hole” (in which you were previously responsible for 25% of your drug costs), has been eliminated entirely. You will have entered the “Initial Coverage” phase in which your elected drug plan will pay 65% of your applicable drug costs, and you will pay 25%. The Manufacturer (pharmaceutical company) will discount the remaining 10%. When you hit your maximum Out-of-Pocket (OOP) threshold of $2,000, you enter “Catastrophic Coverage”. At that point, your plan will pay 60%. Reinsurance (CMS, the Center for Medicare Services, i.e., the government) will pay 20%, and the Manufacturer will pay the remaining 20%. You will pay $0.

This, of course, sounds very well and good! And for those utilizing large quantities of drugs, or expensive drugs, this will indeed be of great benefit. But in what ways may the drug plans “compensate” for the additional costs they will bear? Much of such was referenced or alluded to above. However, please permit me to drill down on potential measures drug plans may take to offset their increased share of your drug cost. *(I am a Medicare Insurance product broker and not a C.P.A. As such, I will not address the impact on the taxpayer of their increased share of Medicare drug costs in this forum. wink. wink 😉

The drill down:

In addition to the higher deductible, higher premiums may be in store. But it could have been a lot worse. CMS did health insurance companies a favor with a “premium-stabilization” plan. In 2025, they will give them a subsidy in exchange for not “slapping members with exorbitant premium hikes. So, “what might have been a 40%, 50%, or higher premium increase may only be as high as 25%. Either way, it will be a sticker shock when some see how their premiums changed.” *(a paraphrase a quote in Feature Article 1)

The Kaiser Family Foundation says the average cost of a stand-alone Part D drug plan is $43. I have seen previews of premiums which will be $0, but others, have risen. In addition to your premium, co-pays for your drugs could go substantially higher. If your drug plan is obligated to charge you less for (or cover more of) a particular drug, are they simply going to charge you more for others?

And what about “Value Added Benefits” (VAB) available in some Medicare Advantage Plans? These include vision, hearing, and dental services. Other examples include acupuncture, bathroom safety devices, and wigs for hair loss. And what about your gym membership? Embedded dental insurance has been dramatically cut back or removed completely.

VAB are not covered by Original Medicare. Medicare Advantage has been able (often along with a $0 premium) to offer these things as an additional incentive to encourage enrollment in their plans. However, because you left Original Medicare and “assigned” the administration of your benefits and claims to the Advantage company when you enrolled, your plan can choose to provide these ancillary benefits that Original Medicare does not. Or they can choose to cover them no longer. This discretion is on their part because the provision of VAB benefits is not codified in law or per CMS regulation. Resultingly, they are not guaranteed. They are optional benefits that the plans have the right to withdraw at any time. I hope you can continue to “workout” at the gym, at your plan’s expense, in 2025 and beyond. But be prepared to purchase a home gym kit if you learn your membership is downgraded or your Advantage plan disappears entirely.

With no obligation, please feel free to contact me for clarification of these relevant issues and additional guidance in navigating the Medicare system and the changes referred to here. I’m in Medicare with you. I am a “Boomer” who has spent the better part of his life in the medical insurance market. For years, I have assisted individuals, families, and businesses in identifying and enrolling in health insurance plans that came as close as I could get them to fully meeting their medical insurance wants and needs.

To sum things up, I work for my clients. I work for you. Not the insurance company. I study, take their tests, and “certify” to represent their products each calendar year. I just completed certifying with approximately 14 companies in preparation for marketing their products in 2025. They do not pay to renew my licenses or my Errors and Omissions insurance, nor do they cover my office insurance and expenses. Neither they, nor anyone else, pay me wages or a salary. And that is great! I knew and understood those terms when I went out on my own. And that is precisely why I did it. I did not want to be beholden to the insurance company.

After becoming independent, the list of companies I was contracted with grew to over 40 during the 1990s. That number has changed as many of those companies went the way of the steam engine with “Obamacare” and all the red tape and regulations that come with it and remaining in the industry. But I persist. I remain positioned to provide you with virtually every available Medicare and health insurance product in your region.

In conclusion:

If you’re reading this, chances are you remember Jim Rockford (a private detective, portrayed by the actor the late James Garner) in his TV show, The Rockford Files (you can hear the opening music now, can’t you?). In the prelude to each episode, you see his cassette recording answering machine and hear the message, “This is Jim Rockford. At the tone, leave a message …”.

Should you get mine, please do the same. Or you may simply text me.

FORTUNE Richard Eisenberg Updated Mon, Aug 26, 2024

Why this year’s Medicare Annual Notice of Change will be vital reading for beneficiaries

In this article:

If you’re on Medicare, you’ll be getting one or two Annual Notice of Change letters in your mail or email this September about your 2025 coverage and costs. You may be tempted to ignore what looks like junk, as nearly a third of recipients do, according to an eHealth survey.

Don’t.

“So often, a person who is quite happy with their plan and doesn’t bother to look at their Annual Notice of Change then gets a nasty surprise in January” when the plan’s new costs and coverage kick in, says Danielle Roberts, author of 10 Costly Medicare Mistakes You Can’t Afford to Make and founding partner of Boomer Benefits, which sells Medicare policies.

What is an Annual Notice of Change?

An Annual Notice of Change from your Medicare Part D prescription drug plan or a private insurer’s Medicare Advantage plan lays out how much your premiums, deductibles, and co-pays will differ in the year ahead and whether the plan will even be offered. (Medigap plans don’t send these notices because they don’t change much year to year.)

An Annual Notice of Change from your Part D plan also says whether your prescriptions will be covered and, if so, how much you’ll pay. A Medicare Advantage Notice of Change will tell you if your doctors and hospitals will remain in the plan’s network.

While this information is always essential to make smart choices during Medicare’s eight-week open enrollment period (Oct. 15 – Dec. 7), experts say reading your Annual Notice of Change is especially important in 2024.

“There is an excellent chance that something is changing on your plan,” says Roberts. “This year, more than ever, we can expect big changes in the plans.”

Surprising effect of the $2,000 prescription drug cap

That’s largely due to a major Medicare change coming in 2025: the new $2,000 cap on out-of-pocket costs for prescriptions covered by a Part D plan.

Since Part D health insurers will be on the hook for more prescription costs due to the cap, they’ll be looking for ways to compensate.

That could mean higher premiums (currently $43 a month for stand-alone plans, on average, according to KFF), deductibles, and co-pays—possibly substantially higher than in 2024.

“I have been very, very concerned about what the $2,000 cap was going to do to Part D premiums,” says Roberts.

The prescription drug change in 2025 could also lead to your Part D plan no longer covering certain medications you take or raising prices of ones it will.

Medicare Advantage plans—some facing profit squeezes currently—often include Part D coverage, so they may respond to the $2,000 cap by trimming or eliminating benefits to keep their popular $0 premiums intact, experts expect.

As a result, your Medicare Advantage benefits that original Medicare can’t offer—such as dental, vision, hearing, and gym memberships—could be less attractive than in 2024, or possibly gone entirely.

“It really will be important to understand what’s changing in the coming year in my current plan and does the plan still fit?” says eHealth CEO Fran Soistman. “Does it still provide the value that it did when I elected to go in it in the first place?”

Reading and understanding the Notice of Change

Your Annual Notice of Change will tell you—if you can understand it.

Only 36% of Medicare beneficiaries surveyed by eHealth said their Annual Notice of Change letter is “readily understandable.”

Figure on spending about 30 minutes closely reading your Annual Notice of Change to see exactly what will be different in 2025 and whether you’ll want to switch plans or coverage next year as a result.

During open enrollment, you can switch from your current Part D plan to another, from your Medicare Advantage plan to another, from Medicare Advantage to original Medicare as well as from original Medicare to a Medicare Advantage plan.

But don’t feel compelled to switch plans just because your Annual Notice of Change says your premium will go up a little or a benefit will be trimmed slightly.

“If there’s a modest benefit decrease or premium increase, but they’re satisfied with what the carrier is providing, people shouldn’t make a change,” Soistman says.

However, he added, if a medication you take will no longer be covered or your physician or hospital won’t be in network, that’s an important change that may persuade you to switch coverage.

The Medicare Plan Finder on Medicare’s site will let you compare Part D and Medicare Advantage plans for 2025.

And, as Philip Moeller writes in the forthcoming revised edition of his book, Get What’s Yours for Medicare, if your Medicare Advantage plan won’t include your favorite doctor or hospital in its network in the year ahead, it’s legally obligated to work with you to identify other physicians or hospitals in its network that you’d like.

A new program to help avoid big premium hikes

To help prevent drastic Part D premium increases, the government’s Centers for Medicare and Medicaid Services recently threw a bone to health insurers with a premium-stabilization plan.

Medicare will provide a special subsidy to those insurers for 2025 in exchange for avoiding slapping members with exorbitant premium hikes.

“It should take what might have been a 40%, 50%, or higher premium increase down to probably 25%,” says Soistman. “It’s still going to be a bit of sticker shock when some people see how their premiums changed.”

Roberts says, “I’m still somewhat concerned about premiums, but I feel a little better after the stabilization program announcement.”

Getting help if your Medicare plan will change

After reading your Annual Notice of Change, you may want to get help deciding on the right Medicare plans for 2025 and to understand the implications of coming changes to your plans.

You can ask a Medicare broker or agent for assistance; there’s a directory at the National Association of Benefits and Insurance Professionals site. The sooner you do, the better, since agents and brokers will be swamped near the end of open enrollment.

“At Boomer Benefits, we have to stop taking new requests after Thanksgiving,” says Roberts.

If one of your prescriptions won’t be covered by your Part D plan in 2025, call your doctor to see if another covered medication would be okay or if you should find a new plan that includes it, Roberts advises.

For information about Part D and Medicare Advantage plans without purchase recommendations, try yourState Health Insurance Assistance Program or visit Medicare’s site or call Medicare’s toll-free number.

More time for open enrollment?

Soistman believes all the changes coming to Part D and Medicare Advantage plans for 2025 will push back the arrival of the Annual Notice of Change documents to the last two weeks of September.

If so, this will give people with the plans less time than normal to read the notices before open enrollment.

The eHealth agency has asked the Centers for Medicare and Medicaid Services to extend open enrollment by about five days to give beneficiaries, insurers, and Medicare brokers more time. Boomer Benefits favors the extension, too.

So far, the government hasn’t responded to eHealth’s proposal.

Could the 2025 open enrollment become Medicare’s equivalent of the Department of Education’s FAFSA financial-aid form fiasco of chaos and confusion?

“I don’t think it will be quite as drastic. I think it is going to be a year of change, though,” says Soistman. “And change is hard for people.” ********* Please follow me follow D. Kenton Henry @Https://HealthandMedicareInsurance.com

Ever since the passage of the Patient Protection and Affordable Care Act (ACA), commonly referred to as “Obamacare”, in 2010, the Department of Health and Human Services has dictated when and under what circumstances an individual and family can apply for and obtain health insurance. This period is known as the Open Enrollment Period, and it is upon us. Each year, between November 1st and December 15th, U.S. citizens and their families may apply for and obtain health insurance effective January 1st of the coming calendar year. From then until January 15th, they may apply for coverage effective February 1st. Beyond that date, they are locked out of any health insurance plan they were not enrolled in when the year ended. Only special circumstances such as losing “creditable” coverage through no fault of their own, moving out of a plan’s area, birth of a child, or death of a covered family member allow them to apply for coverage beyond the Open Enrollment Period. And only if they were insured when the special circumstance occurred and no more than 60 days have passed. Creditable coverage meets all the mandates of the Affordable Care Act, such as guaranteed coverage for pre-existing health conditions, including pregnancy and mental health disorders, along with no out-of-pocket for preventative medicine. All coverage is guaranteed so long as the above requirements are met.

If affordability of health insurance is an issue, Premium Tax Credits (subsidies) are available from the Department of Health and Human Services (DHS) to people or families whose income falls below a certain threshold.

WHO IS ELIGIBLE FOR THE PREMIUM TAX CREDIT?

To receive the premium tax credit for coverage starting in 2024, a Marketplace enrollee must meet the following criteria:

· Have a household income at least equal to the Federal Poverty Level (FPL), which for the 2024 benefit year will be determined based on 2023 poverty guidelines

· Can not have access to affordable coverage through an employer (including a family member’s employer)

· Can not be eligible for coverage through Medicare, Medicaid, the Children’s Health Insurance Program (CHIP)

· Have U.S. citizenship or proof of legal residency (Lawfully present immigrants whose household income is below 100 percent FPL can also be eligible for tax subsidies through the Marketplace if they meet all other eligibility requirements)

· If married, must file taxes jointly

Income: For the purposes of the premium tax credit, household income is defined as the Modified Adjusted Gross Income (MAGI) of the taxpayer, spouse, and dependents. The MAGI calculation includes income sources such as wages, salary, foreign income, interest, dividends, and Social Security.

Your tax credit is based on the household income estimate you put on your Marketplace application.

Income between 100% and 400% FPL: If your income is in this range (in all states) you qualify for premium tax credits that lower your monthly premium for a Marketplace health insurance plan. The lower your income is as a percent of the FPL—the higher your subsidy.

The easiest way to determine whether and for how much you qualify is to call me. You will estimate your 2024 household’s adjusted gross income and my subsidy calculator will tell us (based on the number of people in your household) how much your subsidy will be. If we give the DHS the same information you give me, my calculations are usually accurate to within $3.00 of what you will actually receive. We then apply that subsidy against the premium of the plan you wish to acquire and arrive at your net premium.

The number of people who qualify for subsidies continues to grow. For details on this, please refer to this chart and my feature article 2 below.

As to how much retail (gross) premiums are expected to grow from 2023 to 2024, estimates put the national average at 6%. (For the details on this, please refer to Feature Article 1 below.) Given the rate of core and real inflation, this should not come as a surprise. Acquisition of a subsidy will certainly offset ever-increasing premiums.

As always, the greatest challenge to the consumer and their agent/broker is affordability or obtaining the desired benefits. Instead, it is finding their doctors in the networks of a health plan. In 2024, as it was this year, there will be over 100 different plans available from six to eight different companies, depending on where one resides. Dealing with this myriad of options is where my three decades specializing in health insurance in the Houston area is invaluable. I know which hospitals are in which plan networks, and my provider search tools scan all plans without you having to go from company to company for results. Because I represent every company doing business in Texas, you can acquire information on all of them with one call to me.

Again, Open Enrollment begins November 1st, and for coverage during the entirety of 2024, it ends December 15th. Unlike going to the marketplace (Healthcare.gov) you will get me each time you call my local office with questions and for assistance and service–as opposed to an 800 number where you will get a different individual each time you call. My service is much more personalized and detailed than that of an hourly worker at the end of that toll-free number. If I don’t provide you with the level of service you deserve, I don’t have a client. And if I don’t have a client, I don’t earn a living. And it costs you no more to go through me than directly to the company whose policy you ultimately acquire.

I look forward to working with you and providing the best of service. Please call me.

D. Kenton Henry

Office: 281-367-6565 Text me 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

This analysis of insurers’ preliminary rate filings shows that ACA Marketplace insurers are requesting a median premium increase of 6% for 2024. Insurers cite price increases for medical care and prescription drugs as a key driver of premium growth in 2024, In addition to inflation’s impact on medical costs, insurers point to growth in the utilization of health care, which fell in 2020 but has since returned to more normal levels.

Insurers’ proposed rate changes – most of which fall between 2% and 10% – may change during the review process. Although most Marketplace enrollees receive subsidies and are not expected to face these added costs, premium increases could result in higher federal spending on subsidies.

The analysis can be found on the Peterson-KFF Health System Tracker, an information hub dedicated to monitoring and assessing the performance of the U.S. health system.

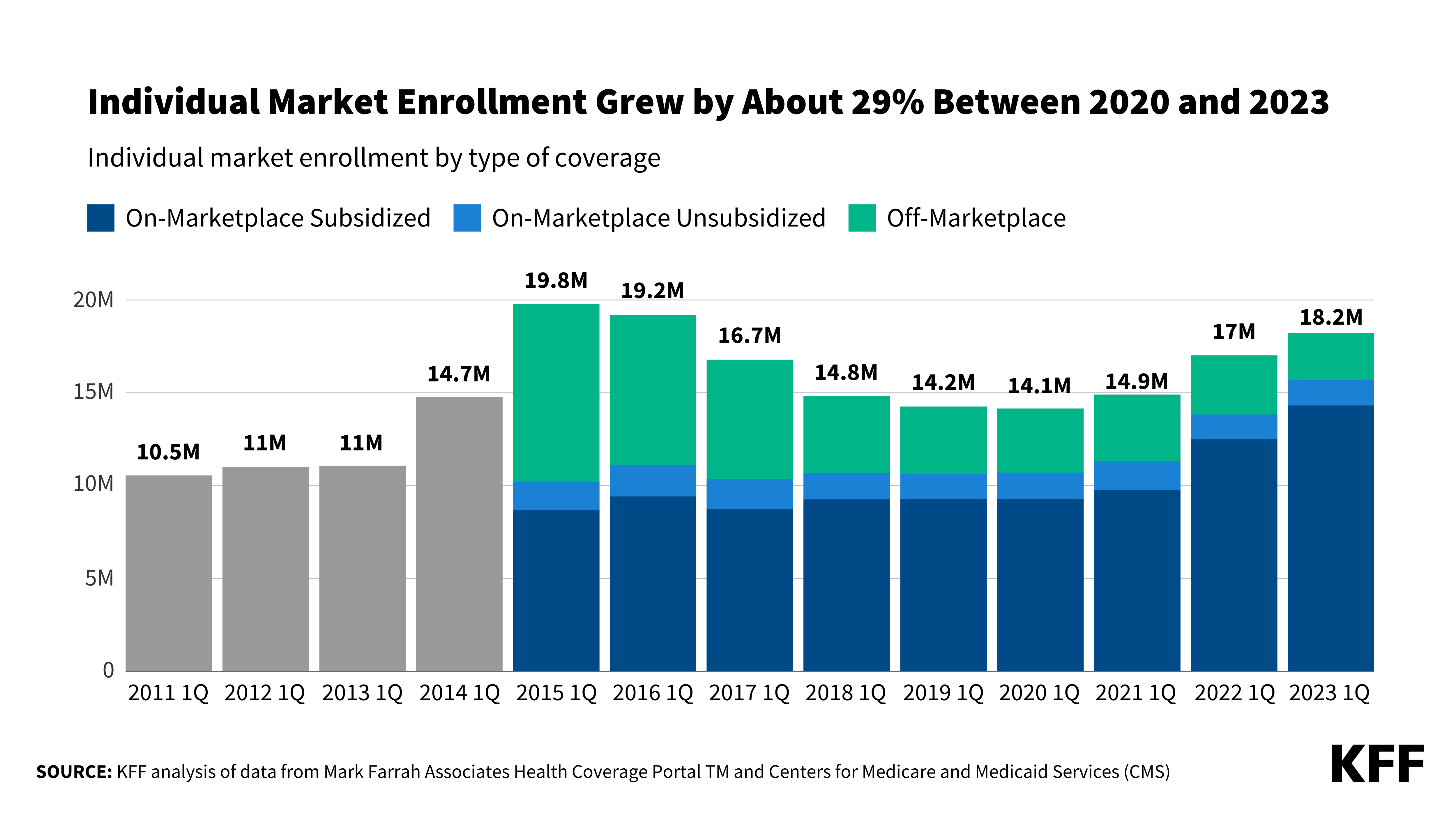

Enhanced Marketplace subsidies have continued to drive up enrollment in the individual market, and the loss of Medicaid coverage by millions of people could contribute to this trend, according to a new KFF analysis. Meanwhile, enrollment in non-ACA-compliant plans is at a record low.

As of early 2023, an estimated 18.2 million people have individual market coverage, the highest since 2016. Individual market enrollment grew by about 29% between early 2020 and early 2023 — a result of enhanced subsidies introduced by the Inflation Reduction Act, increased outreach, and an extended enrollment period.

This enrollment growth could continue in 2023 as states resume Medicaid disenrollments amid the unwinding of the continuous enrollment provision. Some of the people losing Medicaid coverage may be eligible for subsidies on the ACA Marketplaces.

Due in part to the enhanced subsidies, about 4 in 5 individual market enrollees have subsidized coverage — the highest share since the ACA was implemented.

The number of people in non-compliant plans has fallen each year and could decrease further due to the Biden Administration’s proposed rule that would reverse the expansion of short-term plans. An estimated 1.2 million people were in non-ACA-compliant plans in mid-2022, compared to 5.7 million in mid-2015. These short-term plans often do not include certain benefits or coverage for pre-existing conditions and can impose a dollar limit on insurance coverage.

If unsubsidized premiums rise in 2024 due to higher health care prices and utilization, enhanced subsidies could shield most individual market enrollees from increases in their monthly payments.

Are you recently faced with a choice between the high cost of COBRA or going without health insurance? Perhaps we can help.

As if the jobs lost due to lay-offs, furloughs, and the closing of businesses stemming from the coronavirus quarantine wasn’t bad enough, the concurrent and additional losses due to the precipitous drop in the price of oil, have made unemployment rates in Texas soar. For those, like myself, who were present at the time, the situation conjures memories of the oil bust of the 1980’s. The resulting home foreclosures, vehicle repossessions, and mass migration from our state were catastrophic, and our state didn’t fully recover until the mid-’90s. But, as terrible as things were, we never saw oil prices drop “to the negative” as they did a few short weeks ago. We can only hope and take heart in the reality that―because financial fundamentals were so strong prior to the pandemic―this crisis will be much shorter once herd immunity has turned the corner on it―and Saudi Arabia and Russia have ceased attempting to crush the market for the sake of driving out the competition.

UNEMPLOYMENT LINES IN WAKE OF CORONAVIRUS

Regardless, this mass unemployment has resulted in thousands losing their health insurance and has left them faced with accepting the high cost of COBRA or (if employed by companies with less than 20 employees) state-continuation health insurance. If accepting either, the former employee is typically responsible for 100% of the retail premium (inclusive of the portion previously paid by their employer) plus an administrative fee of 2%.

An alternative is to enter the “Individual and Family” health insurance market. If one applies within 60 days of losing their employer-based, credible coverage, they will be guaranteed approval and coverage for any pre-existing health conditions on the first of the month following application. You may obtain quotes for all credible ACA (Affordable Care Act) compliant individual and family plans available to you―as well as an estimate of any subsidy for which you may qualify―by clicking on the link below. Then call us for answers to your questions and assistance in applying for coverage*:

*(you do not need to log-in in order to obtain quotes)

Even when a subsidy is available, many find the premiums for these plans to be unaffordable. For those, “Short-Term” or “Temporary” health insurance may be the answer. As premiums for long-term health insurance continue to rise, more and more people find this to be the case. The advantages are, it can become effective immediately, and you can purchase it for periods up to just short of two years. Because the insurance company knows it will only be obligated to pay claims for a limited period―the premiums will be dramatically lower than those of long-term ACA health insurance. The disadvantage of short-term health insurance is that you first must be approved, and the coverage will not cover pre-existing health conditions. So, if you, or a family member, have any moderate to significant health conditions, you may be declined for coverage or find your pre-existing conditions waived for coverage. But, if you have no health issues or can be approved for coverage and can afford to self-insure for your conditions, you will find this coverage much more affordable!

Our feature article below outlines the trend toward purchasing Short-Term health insurance and the reasons for it. It also introduces a company the clients of TheWoodlandsTXHealthInsurance.com have turned to for years to acquire coverage. From the following link, you can choose from a multitude of deductibles and benefit levels to elect a plan specific to your needs and budget. Once you have narrowed your selection, please call us for answers to your questions and assistance in applying.

You may find you only require this coverage until this unprecedented coronavirus/oil market crisis is behind us or until you obtain your next job with benefits. Regardless, we are here to see you obtain the best coverage for your situation and the best of service thereafter.

CLICK HERE FOR SHORT-TERM HEALTH INSURANCE QUOTES:

For customized quotes with from a subsidiary of Unitedhealthcare, inclusive of:

· Enhanced Short Term Medical – with preventive care coverage on all plans, no limit on urgent care visits with a copay, and no application fees – are now available in 17 states!

· TriTerm Medical – nearly 3 years of continuous health insurance with coverage for doctor visits, prescriptions, and preventive care – now available to quote in 16 states.

· HealthiestYou by Teladoc® members now have access to behavioral health and dermatology services (for an additional per-use fee). Using the same convenient app and phone number, they can access these new services in addition to 24/7 access to doctors. *This product is not insurance.

Call us. We will help you sort through all your options in order to elect the best health insurance or your situation.

D. Kenton Henry Editor, Agent Broker TheWoodlandsTXHealthInsurance.com Office: 281-367-6565 Text My Cell 24/7 @ 713-907-7984

Survey: Short-Term Health Insurance Demand Increasings

Share to FacebookShare to TwitterShare to LinkedInShare to PrintShare to EmailShare to More30

Pivot Health, a division of HealthCare.com, which is a leader in technology-enabled health insurance solutions, has released new customer survey data that reveals 26% of short-term medical plan purchasers were long-time uninsured, while 29% had recently lost their insurance due to unemployment.

Only 5% of purchasers had moved from an Obamacare plan to a short-term medical insurance plan. The survey also showed 75% of the people who lost employer coverage did not choose COBRA because of cost.

Nearly half (46%) of members selected a short-term plan because they didn’t qualify for a subsidy or they needed something quickly. The survey also found 21% of those who purchased a short-term health insurance plan were influenced by the global coronavirus pandemic.

When asked what is the greatest concern facing the health insurance market today, survey participants said out-of-pocket costs were the No. 1 issue they are concerned about when it came to healthcare.

· 64% are concerned about the high monthly cost of insurance.

· 51% worry about paying for medical bills out of pocket.

· 45% are concerned about high deductibles.

One customer said, “Most Americans cannot afford high-cost insurance. Anything over $100 a month is too much.”

“The survey data reveals that customers are more comfortable buying short-term health insurance plans than they ever have been,” said Jeff Smedsrud, chief executive officer of Pivot Health. “Since Congress has failed to pass legislation to subsidize COBRA plans, which put the entire financial burden on the employee, short-term health plans are becoming a general preference for individuals who need a budget-friendly healthcare solution as they maneuver through life transitions, unemployment or just need economical coverage.”

HealthCare.com is an online health insurance company providing a data-driven shopping platform that helps American consumers enroll in individual health insurance and Medicare plans. HealthCare.com also develops and markets a portfolio of proprietary, direct-to-consumer health insurance and supplemental insurance products under the name Pivot Health. Founded in 2014, the company is headquartered in New York City and is backed by PeopleFund and individual investors including current and former executives of Booking.com and Priceline. HealthCare.com is a 4-time honoree of the Inc. 5000 list of America’s fastest-growing companies and has been recognized by Deloitte as one of the fastest-growing technology companies in North America.

Op–Ed by D. Kenton Henry 01 October 2019 HealthandMedicare.com

VS.

I listened to the recent Democrat Presidential Primary Debates, as I listen to the daily sound bites in the media, as candidates try unabashedly to outdo each other. They do this in terms of the massive give-aways they promise us if elected in 2020. They promise these things not just to citizens, but everyone within the border of the United States. My incredulity, upon hearing such, exceeds even those bounds.

Their original promise is “free healthcare for all”. Healthcare free of premiums, deductibles, and copays. Medicare is the vehicle. To which I must ask myself, “Do these people even know the costs involved in Medicare?” “Do they really believe Medicare pays everything?” They would have you believe as much. They are counting on your naivety and lack of familiarity with the subject.

What makes Medicare a convenient and acceptable form of medical coverage for millions of people 65 and older (or disabled for 24 months or more) is it working in conjunction with private insurance plans. That, and thousands of licensed and “Certified” agents and brokers, helping to deliver comprehensive medical coverage at an affordable price. It is a hybrid package that provides as complete protection as available. The insurance plans would not exist without Medicare and, by itself, Medicare leaves the recipient/member exposed to significant liabilities.

Do these candidates, and the average voter know that in 2019:

A hospital admission requires the Medicare member to pay a $1,364 deductible each time they are admitted to the hospital as an inpatient for a separate medical condition, or the same medical condition separated by more than 60 days.

For days beyond 60, they pay $335 per day

Beyond day 90, they pay $682 per day

Eventually― say in the event of a stroke, paralysis, or being severely burned―they will pay all costs.

Part B Co-Insurance, Deductible and Premium

Relative to out-patient medical care, the Medicare member pays 20%, plus can be liable for excess charges above and beyond what Medicare deems “reasonable and customary”.

In addition, Medicare recipients pay an annual deductible of $185 for Medicare Part B (out-patient) medical care and a premium generally beginning at $135.50 per month and increasing to as high as $460.50. The latter depending on one’s adjusted gross income.

Perhaps most important, to take note of, in considering whether “Medicare For All” is even feasible, much less cost effective, is this. Medicare recipients have paid into the Medicare program their entire working careers via Medicare care taxes and payroll deductions. To qualify for Part A, (inpatient) coverage, they must have worked a minimum of 40 quarters or “buy in “with a premium as high as $422 per month.

So, you can see, Medicare is hardly free. And yet these candidates would have you believe it will be provided free of premiums, deductibles, and copays. (Now this is where even The Tooth Fairy raises her eyebrows!) It will be GIVEN, not to just those over 65, but to every man, woman, child, legal, and non-legal citizen or resident of the United States―whether they have paid a dime into the system or not.

Factor all that in and process this. Medicare now spends an average of about $13,600 a year per beneficiary, and in five years, the annual cost is expected to average more than $17,000, the report said.

According to CMS.gov (The Centers for Medicare & Medicaid Services ― refer to featured article 1 below*) The Medicare Board of Trustees predicts Medicare’s two trust funds, for Part A and Part B and D, respectively ― will go broke in 2026!

To put things in perspective, in 1960 there were about five workers for every Social Security beneficiary. The ratio of workers to beneficiaries fell to 3.3 in 2005 and then to 2.8 in 2016. It will decline further to about 2.2 by 2035, when most baby boomers will have retired, officials said.

The aging of the population is another factor in the growth of the two entitlement programs. The number of Medicare beneficiaries is expected to surge to 87 million in 2040, from 60 million this year, according to Medicare actuaries. And the number of people on Social Security is expected to climb to 90 million, from 62 million, in the same period.

The United States Treasury: U.S. Debt And Deficit Grow As Some See Government As The “Be–All and End–All”.

All this and the candidates would have you believe our government can provide free health care to everyone? When it can’t even provide it to our current citizens who have paid into the system their entire working lives! And who exactly is the government? “We The People”. We the tax payers. You and I. Even some of the candidates, admit the proposal will call for more taxes from the middle class. More? Really! One projected cost for Medicare For All is 39 trillion dollars over the first ten year period. The national debt is currently $22 trillion and took since the end of President Andrew Jackson’s administration (1837 and the last time the national debt was fully paid-off) to accumulate that! The combined wealth of all American households is less than $99 trillion. One can only conclude that “Medicare For All” would be a “Welfare System For All”. It would push our country into a socialist economic system to a depth from which it would be impossible to extricate itself.

As a new Medicare recipient, myself, I find the combination of the government program and private insurance working very well for myself and clients, from an insured standpoint. The program’s, and our nation’s, fiscal concerns are a more substantial matter and a topic for another time. With Medicare “Open Enrollment” a mere 15 days away, I can only say, “I hope whoever is President, and controls Congress, in future administrations―while providing a safety net for all American citizens―first and foremost, provides the capable, responsible, American taxpayer quality medical coverage―free of rationing of treatment and access to providers. At an affordable cost.”

D. Kenton Henry, editor HealthandMedicareInsurance.com, Agent, Broker

Medicare Trustees Report shows Hospital Insurance Trust Fund will deplete in 7 years

Today, the Medicare Board of Trustees released their annual report for Medicare’s two separate trust funds — the Hospital Insurance (HI) Trust Fund, which funds Medicare Part A, and the Supplementary Medical Insurance (SMI) Trust Fund, which funds Medicare Part B and D.

The report found that the HI Trust Fund will be able to pay full benefits until 2026, the same as last year’s report.For the 75-year projection period, the HI actuarial deficit has increased to 0.91 percent of taxable payroll from 0.82 percent in last year’s report. The change in the actuarial deficit is due to several factors, most notably lower assumed productivity growth, as well as effects from slower projected growth in the utilization of skilled nursing facility services, higher costs and lower income in 2018 than expected, lower real discount rates, and a shift in the valuation period.

The Trustees project that total Medicare costs (including both HI and SMI expenditures) will grow from approximately 3.7 percent of GDP in 2018 to 5.9 percent of GDP by 2038, and then increase gradually thereafter to about 6.5 percent of GDP by 2093. The faster rate of growth in Medicare spending as compared to growth in GDP is attributable to faster Medicare population growth and increases in the volume and intensity of healthcare services.

The SMI Trust Fund, which covers Medicare Part B and D, had $104 billion in assets at the end of 2018. Part B helps pay for physician, outpatient hospital, home health, and other services for the aged and disabled who voluntarily enroll. It is expected to be adequately financed in all years because premium income and general revenue income are reset annually to cover expected costs and ensure a reserve for Part B costs. However, the aging population and rising health care costs are causing SMI projected costs to grow steadily from 2.1 percent of GDP in 2018 to approximately 3.7 percent of GDP in 2038. Part D provides subsidized access to drug insurance coverage on a voluntary basis for all beneficiaries, as well as premium and cost-sharing subsidies for low-income enrollees. Findings revealed that Part D drug spending projections are lower than in last year’s report because of slower price growth and a continuing trend of higher manufacturer rebates.

President Donald J. Trump’s Fiscal Year 2020 Budget, if enacted, would continue to strengthen the fiscal integrity of the Medicare program and extend its solvency. Under President Trump’s leadership, CMS has already introduced a number of initiatives to strengthen and protect Medicare and proposed and finalized a number of rules that advance CMS’ priority of creating a patient-driven healthcare system through competition. In particular, CMS is strengthening Medicare through increasing choice in Medicare Advantage and adding supplemental benefits to the program; offering more care options for people with diabetes; providing new telehealth services; and lowering prescription drug costs for seniors. CMS is also continuing work to advance policies to increase price transparency and help beneficiaries compare costs across different providers.

The Medicare Trustees are: Health and Human Services Secretary, Alex M. Azar; Treasury Secretary and Managing Trustee, Steven Mnuchin; Labor Secretary, Alexander Acosta; and Acting Social Security Commissioner, Nancy A. Berryhill. CMS Administrator Seema Verma is the secretary of the board.

Health insurers ramp up lobbying battle against Medicare-for-all

By Ana Radelat

The CT Mirror |

Aug 12, 2019 | 6:00 AM

Health insurers have joined forces with their longtime foe, the pharmaceutical industry, as well as partnering with the American Medical Association and the Federation of American Hospitals, to form a coalition to fight Medicare-for-all proposals and other Democratic plans to alter the nation’s health care.

As Democratic presidential candidates embrace changes to the nation’s health care system that could threaten Connecticut’s health insurers, the industry is hitting back.

Health insurers have joined forces with their longtime foe, the pharmaceutical industry, as well as partnering with the American Medical Association and the Federation of American Hospitals, to form a coalition to fight Medicare-for-all proposals and other Democratic plans to alter the nation’s health care.

The Partnership for America’s Health Care Future, funded by the insurance industry and its allies, is running digital and television ads aimed at undermining support for Medicare-for-all proposals and plans for a “public option,” a government-run health plan that would compete with private insurance plans.

The partnership was formed a little more than a year ago to protect the nation’s current health care programs, mainly the Affordable Care Act, Medicare and Medicaid.

The organization’s executive director, Lauren Crawford Shaver, said diverse groups in the coalition found a common cause in 2017 — opposing an attempt by congressional Republicans to repeal the Affordable Care Act.

“We came together to protect the law of the land,” she said.

That battle was won. Coalition members determined they should continue to band together to ward off other political dangers.

“There’s a lot of things we might fight about, but there’s a lot we can agree on,” Crawford Shaver said.

Sens. Bernie Sanders of Vermont and Elizabeth Warren of Massachusetts have called for a Medicare-for-all through a single-payer system, in which all Americans would be enrolled automatically in a government plan.

Warren was among several candidates during the most recent Democratic debates who took aim at health insurers.

“These insurance companies do not have a God-given right to make $23 billion in profits and suck it out of our health care system,” she said.

Other candidates prefer a more modest approach, offering a “public option” or Medicare buy-in plan that would allow Americans to purchase government-run coverage, but unlike Medicare-for-all would not eliminate the role of private insurers.

That split among Democrats also runs through Connecticut’s congressional delegation, with Sen. Richard Blumenthal, D-Conn., and Rep. Jahana Hayes, D-5th District, endorsing Medicare-for-all plans and the other lawmakers supporting Medicare buy-in or public option plans.

The nation’s health insurers oppose all of the Democratic proposals discussed during the two nights of debates.

The insurers’ message is simple: The Affordable Care Act is working reasonably well and should be improved, not repealed by Republicans or replaced by Democrats with a big new public program. Further, they say, more than 155 million Americans have employer-sponsored health coverage and should be allowed to keep it.

Insurers also say that public option and Medicare buy-in plans would lead the nation down the path of a one-size-fits-all health care system run by bureaucrats in Washington D.C.

Advertisement

They say offering a public option or a Medicare buy-in would prompt employers to drop coverage for their workers and starve hospitals, especially those in rural areas, since government-run health plans usually reimburse doctors and hospitals less for medical services than private insurers. They also say Medicare-for-all and other Democratic proposals will lead to huge tax increases to pay for the plans.

“Whether it’s called Medicare for all, Medicare buy-in or the public option, the results will be the same: Americans will be forced to pay more and wait longer for worse care,” said Crawford Shaver.

The Partnership for America’s Health Care Future ran its first television ad on CNN just before and after the cable channel ran last week’s debates.

The commercial showed several “ordinary Americans” at home and work decrying “one-size fits-all” health plans and “bureaucrats and politicians” determining care.

“We need to fix what’s broken, not start over,” the final speaker says.

Members of the Partnership for America’s Health Care Future have a lot of money and influence to wield on Capitol Hill. They spent a combined $143 million lobbying in 2018 alone, according to data from the Center for Responsive Politics.

And coalition members appear eager to spend even more lobbying money this year.

In the first six months of this year, America’s Health Insurance Plan, a health insurer industry group and member of the partnership, spent more than $5 million on lobbying expenses, and is on the way to surpassing the $6.7 million it spent in lobbying last year.

To underscore the health insurance industries’ importance to local economies, AHIP releases a state-by-state data book each year that details coverage, employment and taxes paid.

In Connecticut, the industry employs 12,296 workers directly and generates another 13,586 jobs indirectly, AHIP says. The payroll for both these groups of workers totals over $3.8 billion a year, AHIP says, and the average annual salary in the business is $112,770. The Connecticut Association of Health Plans puts the number higher, saying Connecticut has 25,000 direct jobs related to the health insurance industry, and another 24,000 indirect jobs.

AHIP also estimates that Connecticut collects nearly $200 million a year in premium taxes on health care policies sold in the state.

Connecticut’s reliance on health insurers – and their continuing influence – was on full display during the last legislative session when the insurance companies, led by Bloomfield-based Cigna, derailed

“Is dental insurance really worth the premium I pay?” is one question I am asked frequently. It is often followed, almost instantly, by―”Or am I simply paying for my dental work on a time a payment plan?”

My answer to both questions is a definitive, “Maybe.”

If you, as the majority do, have dental insurance through your employer, that employer is subsidizing all or part of your premium. This convenience makes for a solution to the equation, more favorable to you. In contrast―if you are self-employed, retired, or otherwise personally have to pay the full amount of a dental insurance premium―the opposite may be true. That is unless you take some straightforward advice, I am about to provide. If you do not, you most likely will only be spreading your cost for dental work over time. Even worse, dental insurance could prove to be a “loss item” in that you will have paid more in premiums than you will ever receive in benefits.

Short of taking a long drive and crossing the Rio Grande into Mexico to obtain your dental work, what can you do to offset the cost of say, a dental implant, which, on this side of the border, is going to run from $3,500 to $7,000?

Let me preface this by with a premise or three:

#1) With no insurance company is “the sky the limit”. I’m referring to the fee they are going to pay a dentist for a particular dental procedure. For example, no insurance company is going to accept a fee of $10,000 for a single porcelain crown. Not even their share of that cost, which is typically 50%. So what is the limit of a fee the insurance company will cover? That limit must be contractually defined, and the limit most insurance companies abide by is, “reasonable and customary” or “reasonable, usual, and customary”. These are empirical standards an insurance company uses to determine whether to pay a fee. Or how much of a fee to pay. If the dentist charges the general prevailing rate in your geographical area, they are going to pay the portion for which they are contractually obligated. Basically, it’s the average charged in your neighborhood. You will be charged more in Beverly Hills, California and less in Brenham, Texas “where the cows think it’s heaven”. Additionally, if “usual” is part of the definition, the fee has to be in line with what this particular dentist charges for a particular procedure. If fee is disproportionate either, or, both, ways―the maximum amount paid by the insurance company will be the limit set in their fee schedule.

#2) A dental insurance plan is either a provider network plan or a non-network plan. If it is a network plan, it is usually either a Dental Preferred Provider Organization (DPPO) Plan or a Dental Health Maintenance Organization (DHMO) Plan. If it is the first, you may go outside the network of dentists with which the insurance company has contracted but will most likely pay a higher cost for doing so. With the latter, you must remain within the network of dentists or, you have no insurance coverage whatsoever. For either of these options, you pay a lower premium than if you purchase a non-network or “any dentist” plan. The reason is that you agree to utilize or, at least, consider utilizing a dentist with whom the insurance company has contracted to charge you a lower fee than they would without the contract. This limits the insurance companies losses and brings increased traffic to the dentist.

#3) This is perhaps the most important part. If you purchase a non-network dental insurance plan, you can, almost, be assured you will be charged more than the insurance company deems acceptable. Additionally, you will be responsible for any dollar amount above their “reasonable and customary” rate. However, if you purchase a network plan, and go within the network of dentists, you will not be held responsible for any “excess” charges. Any charges above the reasonable and customary rate, the dentist will be forced to “write off”. In this situation, you will never have to worry about a surprise bill or claim. If a policy says your share of the bill is 20% or 50%, it will be that and not 20% or 50% plus any excess charges.

Assuming you accept you must acquire a network plan, in order to limit you own losses and surprise dental bills, the challenge becomes, “How do you find a quality dentist willing to accept a lower fee for treating you?” The typical HMO dental provider is typically someone straight out of dental school or who otherwise needs to build their patient base. In return for sending patients their way, the dentist is willing to accept a meaningfully lower fee. If the dentist is a PPO provider, they may have been in business longer, have more experience, and perhaps a reputation for having better skills. But they are willing to accept a somewhat lower fee in return from the many employees a large company may send their way. The dentist who isn’t willing to participate in any network apparently feels they have all the clients they need. That or their reputation is so great it will draw all the traffic they require.

The problem is, unlike a large oil company, as an individual, or family, you don’t bring enough “volume” to the table to bargain for a lower dental fee. At least not by yourself. Therefore, you have to identify and purchase your dental insurance from an insurance company which has the reputation of insuring a large number of employees of that oil company. As well as having a reputation for paying their claims in a timely and efficient manner. A manner such that the dentist wants to be contracted with them. From your standpoint, you want that insurance company to have a reputation for the same when it comes to you and not have to worry about claim disputes.

Another challenge is, at $6,000 for a dental implant, your dental benefit may not go too far. Secondly, does your insurance plan cover implants in the first place? Again, the sky is not the limit. The average dental plan covers a maximum of $1,000 of dental treatment per year. You can pay a higher premium for incremental benefits up to a maximum of $5,000. But a policy which pays that much in year one would cost a fortune and there is typically a twelve-month wait for major dental work to be covered. As such, you may want to find a plan which increases to that limit with each passing year and is available at what you consider a reasonable cost.

How do you find a dental policy which does not subject you to “excess” costs; allows you to see a highly skilled dentist, utilizing the latest technology and performing the most advanced form of treatment; all at a competitive premium? And this from a company which pays the claims they are contractually obligated to pay while doing so in a timely fashion?

This is where I, and my thirty-three years experience in the medical and dental insurance business, come in. My experience as a patient and consumer is even longer. After being in braces for eight years, I had all my front teeth knocked out in an auto accident when they impacted the steering wheel. I was wearing a seat belt, which saved my life, but not a shoulder strap. I’ve had to have the dental work replaced on three occasions since that senior year of high school. This year, I proceeded with what will be one double crown and, ultimately, two implants. (Ouch, is right!) I was not willing to accept this type of work from a mediocre dentist―and certainly did not care to pay cash for it! So I found a policy, issued by a large, financially sound insurance company, with a reputation for excellent customer and claim service. Then I found a policy which ultimately pays the maximum $5,000 annual benefit. In order for it to be affordable to me, it started, December 1 of 2018, at a calendar year benefit of $1,500―immediately went to $2,500 January 1, of this year―and will go to a $5,000 benefit this coming January. So I only paid for a $1,500 benefit for one month before it jumped to a $2,500 benefit! During this year I acquired the double porcelain crown and the bone graft and post for one dental implant. In 2020, I will have the crown for the implant post attached, when my calendar year benefit is $5,000. The second implant is optional, and I will probably have that work done in 2021 when my benefit remains $5K.

Once I knew what company to go with, the final step in selecting my dental insurance policy required finding the right dentist. I reviewed the insurance company’s list of network providers and researched the dentist’s reputation via credentials and reviews. I won’t belabor that but, suffice it to say, I found a dentist who met my requirements. He is very conveniently located relative to any resident of The Woodlands or Spring and, in my opinion, is well worth going to if you reside anywhere in Montgomery County or Northwest Harris County. He utilizes the latest technology, has a great and skilled staff, and a decent, very professional, if not overly effusive, chairside manner.*

In summation, in order to make dental insurance worth your while, you need to:

1) accept you need to acquire a “network provider” dental plan

2) find a policy which pays a reasonable benefit based on your foreseeable need, at an affordable premium and

3) allows you to go to a skilled dentist convenient to you

I have done all the homework for you. For over three decades, I have specialized in medical, Medicare-related, and dental insurance. I provide objective quotes from established “A” rated companies and quality customer service. Among the companies I represent are Aetna, Ameritas, Anthem, BlueCross BlueShield, Cigna, Delta Dental, Humana, and UnitedHealthcare. I am located in the heart of The Woodlands and am accessible from my websites Allplanhealthinsurance.com and TheWoodlandsTXHealthInsurance.com. You may also feel free to contact me at my numbers below.

I look forward to working with and assisting you in acquiring any of the above referenced products.

*(Neither I nor my agency and websites are affiliated in any way with a particular dentist or dental office. Neither do we receive compensation from the same for any recommendation we may make.)

By D. Kenton Henry Editor, Agent, Broker 29 October 2018

The media is proffering all manner of good news when it comes to the Open Enrollment Period for purchasing 2019 individual and family health insurance, just three days away. The doors open this Thursday, November 1st and will remain so through December 15th. During this time you, the consumer, will be able to review your options and make a decision to renew your existing policy or select a new one to become effective January 1. Whichever, that policy will cover you the coming calendar year.

The feature article appearing below, states there will be ” . . . fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.” To wit, it cites, the budget for insurance counselors, known as navigators, has been cut by 80%, leaving over one-third of navigators in 2,400 counties served by Healthcare.gov, unfunded. Thank you very much, New York Times. Somehow, they neglected to consult with me and my agency, ALL PLAN MED QUOTE. Reading the article in full, one can infer they feel the only meaningful assistance can come from the government (at taxpayers’ expense) and fail to credit the private industry, which has provided counsel and enrollment assistance within the domestic insurance industry some two hundred years plus. One token sentence in the article acknowledges the private industry’s presence to assist the consumer with procuring health insurance. In my estimation, this reflects the media’s general opinion and thesis that the government is the end-all solution to every conceivable personal financial issue. Which, again, in the mind of this editor, is precisely the philosophy, the perpetuation of which got us into this fix in the first place. Moreover, what exactly is that fix?

Current pre-midterm election media coverage informs us premiums have stabilized and are, in many cases, going down in 2019. While that may be true in some localities, the recently released premiums in southeast Texas reflect increases of 20% or more. If you obtain a subsidy, wherein you get a tax credit for a portion of your premium, the subsidy itself may be larger, but the balance may be as well. Also, for those not obtaining a subsidy (the vast majority of us) the increase will be born entirely by ourselves. The situation has made healthcare the number one concern of Americans heading into next week’s midterm elections according to a Fox News Poll.

For the record, ALL PLAN MED QUOTE and I have never been subsidized by taxpayer dollars. As an independent, self-employed broker/agent I am compensated when I successfully enroll someone in health insurance. I am not compensated when I fail at such. That is fine by me. In spite of continual cuts in agent compensation. I prefer autonomy to bureaucracy. My advice and guidance are objective. My goal is to succeed it getting you enrolled in a policy which makes sure you have access to the care and treatment you need, when you need it and are not financially devastated in the process. All this for the lowest possible premium. I do not care which insurance company you contract with, as long as you are satisfied you have obtained the best coverage for your given situation and needs. Ideally, it would also provide you access to all the doctors and medical providers you choose to utilize. Regrettably, that latter objective has become my biggest challenge and is one every insurance agent and counselor faces. To say it can be overcome in every instance would be misleading but I do my best. All 2019 individual and family options are Health Maintenance Organizations (HMO) policies, and this has been so since 2016. The HMO networks are narrow in comparison to what one may typically have experienced with employer-based HMO coverage. However, there are a very few plans (3 in my primary region) which operate very similar to a traditional Exclusive Provider Organization (EPO) policy in that they do cover treatment at a provider outside the network. Benefits are paid up to a limited percentage, and there is no cap on your maximum annual out-of-pocket but―for someone who wants to be assured they can obtain coverage from the provider of their choice―it is better than no coverage whatsoever. If you feel you must learn more about this option, please contact me.

To assist me in these ends, I am appointed with every company providing Patient Protection and Affordable Care Act-compliant health insurance company doing business in Montgomery, Harris, Fort Bend, and Galveston counties. BlueCross BlueShield of Texas (to my knowledge) does business in every corner of Texas, and I have been appointed with them twenty-seven years. In addition to Texas, I am licensed in Indiana, Michigan, and Ohio.

I offer short-term health insurance for those who do not get a subsidy and those who, whether they do or not, cannot afford credible health insurance. However, I do not represent it as covering pre-existing health conditions, as it does not. Nor do I represent it as a substitute for credible, compliant coverage. It is a short-term bridge to a long-term solution.

As always, the Open Enrollment Period will be a very busy and hectic time for anyone in my profession. To make things proceed more smoothly, I would appreciate you visit my quoting site to obtain spreadsheet comparison of your options from all the health insurance companies offering coverage in your county. Attempt to narrow your selection down to those plans you feel most closely approximate the coverage you need. You can search for in-network providers from the search button directly next to the premium quoted. If you are so confident a plan is right for you, please feel free to apply straight from the quote. However, many of you will have questions or appreciate my insight and experience with the plan details and application process. Those in need of a subsidy will find my assistance especially helpful. If this is you, please do not hesitate to contact me.

Again, for quotes and applications, you may go to my website at Http://TheWoodlandsTXHealthInsurance.com and click on “Health” in the top menu.

Alternatively, you may go directly to my spreadsheet quotes and an application by clicking on this link: https://allplanhealthinsurance.insxcloud.com

*(it is not necessary to log in or register to obtain quotes or apply)

**(if these links do not function from this text, please copy and paste or type in your browser and hit enter)

If you apply for coverage through these links, I will be your agent and available to assist and commit to providing the best of service throughout the year. I bring my entire thirty-two years in medical insurance to bear for this purpose. I look forward to hearing from you and assisting you. Regardless, I hope you succeed in obtaining health insurance which suffices until Congress puts their heads together and provides us with more reasonable options.

D. Kenton Henry All Plan Med Quote Office: 281.367.6565 Text my cell @ 713.907.7984 Email: Allplanhealthinsurance.com For the latest in health and Medicare-related insurance, news go to Https://HealthandMedicareInsurance.com

************************************************************************************************ FEATURED ARTICLE

The New York Times By Robert Pear Oct. 27, 2018

Shopping for Insurance? Don’t Expect Much Help Navigating Plans

Affordable Care Act navigators helping patients during an enrollment event in 2016 at Southwest General Hospital in San Antonio.CreditCreditEric Gay/Associated Press

WASHINGTON — When the annual open enrollment period begins in a few days, consumers across the country will have more choices under the Affordable Care Act, but fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.

The Trump administration has opened the door to aggressive marketing of short-term insurance plans, which are not required to cover pre-existing medical conditions. Insurers are entering or returning to the Affordable Care Act marketplace, expanding their service areas and offering new products. But the budget for the insurance counselors known as navigators has been cut more than 80 percent, and in nearly one-third of the 2,400 counties served by HealthCare.gov, no navigators have been funded by the federal government.

“There is likely to be a lot of consumer confusion about the various plan options that may be available this year,” said Sabrina Corlette, a research professor at Georgetown University’s Health Policy Institute. “It will be a bit of a Wild West — buyer beware!”

“Obamacare health plans,” short-term plans and “Christian health sharing plans” are all displayed on the same page of some shopping sites like Affordable-Health-Insurance-Plans.org, which describes itself as a free referral service for insurance shoppers.

ADVERTISEMENT

Consumers may have difficulty sorting through their options after the administration sliced the budget last summer for insurance navigators to $10 million this year, from $36 million in 2017 and nearly $63 million in 2016.

“Navigators play a vital role in helping consumers prepare applications to establish eligibility and enroll in coverage through the marketplaces,” the Department of Health and Human Services says on its website.

But 797 counties served by HealthCare.gov will not have any navigators this year, according to a tabulation of federal data by the Kaiser Family Foundation. That is a sharp increase from 2016, when 127 counties lacked such assistance.

“If you are confused and you want somebody’s help to try to figure out what’s right for you — what’s junk and what is legitimate — there will be fewer people to help you in most states,” Ms. Corlette said.

Federal officials said they were not providing funds for navigators in Iowa, Montana or New Hampshire because no organizations had applied for the money in those states.

Cleveland, Dallas and large areas of Michigan and other states will also be without navigators.

Texas will be hit hard. The state has the largest number and the highest percentage of people who are uninsured, with 4.8 million people, or 17 percent of residents, lacking coverage, according to the Census Bureau.

“North Texas remains one of the most uninsured areas in the country,” said the chief executive of Dallas County, Judge Clay Lewis Jenkins. “The administration’s decision to defund all navigators across North Texas will hurt our ability to enroll individuals in health insurance and result in some working families losing coverage. Only 45 of Texas’ 254 counties have any navigator coverage.”

Seema Verma, the administrator of the Centers for Medicare and Medicaid Services, defended the cuts.

After five years, she said, “the public is more aware of the options for private coverage” available through the marketplace, so “it is appropriate to scale down the navigator program.” In addition, she said, information and assistance are available from other sources, including insurance agents and brokers.

Consumers can sign up for health insurance under the Affordable Care Act starting Thursday. Last year, 8.7 million people enrolled at HealthCare.gov, and three million more selected plans on insurance exchanges run by states.

Consumers can go without insurance next year without fear of a penalty, as Congress repealed the unpopular tax surcharge imposed on people who lack coverage.

Many health policy experts say that federal financial assistance is more important than the individual mandate in inducing people to buy insurance. Those subsidies will still be available to low- and moderate-income people for insurance that complies with the Affordable Care Act and is purchased through the public marketplace. The subsidies cannot be used for short-term policies.

The vast majority of the people we serve, over 90 percent, are motivated to have insurance because they want coverage for their family and themselves,” said Matthew Slonaker, the executive director of the Utah Health Policy Project, a nonprofit. “It’s not because they otherwise would have to pay a penalty.”

Average premiums for the most popular types of insurance purchased by individuals and families will be relatively stable next year and, in some states, will actually decline, the administration says.

Under new standards issued by the administration, navigators this year are encouraged to inform consumers of the full range of coverage options, including short-term plans that do not provide all of the benefits and consumer protections required by the Affordable Care Act.

President Trump has promoted the short-term policies as an inexpensive alternative to the Affordable Care Act, and he said those plans would be “much more widely available” as a result of an executive order he signed last year to overturn restrictions imposed by President Barack Obama.

Democrats have made health care a major theme in midterm election campaigns, and they say the short-term policies show how the Trump administration threatens protections for people with pre-existing conditions.

Short-term policies, which can extend up to 364 days and then be renewed for two additional years, often provide no coverage for pre-existing conditions, prescription drugs, pregnancy, maternity care or the treatment of mental disorders and drug abuse.

Indeed, Mr. Trump said, the short-term plans are cheaper because they are “not subject to any very expansive and expensive Obamacare coverage mandates and rules.”

ADVERTISEMENT