Op-Ed by Kenton Henry, Administrator

I have just completed my Affordable Care Act (ACA) training and certification in order to offer ACA compliant plans to my clients, and the public in general, beginning October 1. However, even in this final hour with only eight days until the new plans are to be available – the insurance companies have still not released the premiums the insure will pay for these options. “Any day now” is what I am being told. However, I will share with you a thing or two I do know based on what I have studied.

Most of it came as no surprise to me. One major company (whose name I cannot divulge as the information they provided was yet to be approved by the Department of Health and Human Services (HHS) who will be in charge of the Federal-Run Exchange–Marketplace–in Texas, Indiana and Ohio–where I have clients) previewed plans. The lowest plan deductible available was $1,500. All plans will be limited to a maximum out-of-pocket of $6,350 per individual and $12,700 per family. While older people will probably find a $1,500 deductible acceptable in terms of affordability, I am not certain how twenty year olds are going to feel about that. I certainly don’t think that and higher deductible options will be an incentive for them to enroll even with the convenience of doctor’s office co-pays and prescription drug cards. I can almost guarantee you that unless they receive a subsidy – they won’t be signing up.

Beyond that, the benefits sounded perfectly acceptable until I came to the part about “special care centers”. It turns out, at least with this company (which happens to be a very large, conspicuous player in the Texas health insurance market we’ll just refer to as company XYZ)when you are in need of a special surgical procedure such as a hip or knee replacement: “You may only receive one by going to an ‘XYZ Approved Hip and Knee Replacement Center'”. I have had a hip replacement and had it at the relatively young age of 49 and I don’t know about you but I didn’t want just anyone performing mine. I still had dreams of remaining very active and athletic to the point of partaking in very aggressive martial arts training among other activities such as mountain biking. Fortunately, I have been able to do so but would I had I gone to some “Preferred” (discount) provider who agreed to accept lesser fees for greater patient volume?

To underscore my concern relative to an obvious attempt to ration our selection of providers, if not the procedures themselves, I received an email today informing me the primary Medicare Advantage Plan I enrolled my clients in last year is having an inordinate number of Primary Care Physicians drop out of its network and that I should be prepared to re-shop their Advantage Plan. The problem is, if this very large nationally recognized plan is experiencing this kind of “provider drop-out” – what can I expect from smaller companies with less capital? Again, I have had to delete their name as the information was proprietary and for “agent use only” but the letter they sent their clients is attached below. If you are one of my current Medicare clients I placed with this plan – you may have already read this. Otherwise, I apologize for breaking the news to you like this.

Our feature article appeared in today’s New York Times (September 23rd) and describes how patient options will be restricted as a result of the ACA. Think about it. If the insurance companies have no choice in who they insure and must cover any and all pre-existing conditions . . . and if they are informed by the Department of Health and Human Services their profit and, more specifically, the ratio of claims they must pay relative to the premium they take in, i.e., 80% to 20% – how else can they manage losses except to restrict access to procedures, providers and what your providers are paid? Something had to give.

****************************************************************

Letter to Medicare Advantage Clients

Update to Physician Network Changes

At ————- , we manage the physician networks for our plans to help meet the evolving needs of health care consumers. This includes adjusting the size and composition of our physician network as we strive to meet the specific needs of Medicare Advantage and/or Medicaid plan members.

As a result, in the coming months, select physicians for one or more of your Medicare Advantage and/or Medicaid members will no longer participate in our Medicare and Medicaid plan networks. Please note: these changes do not affect members enrolled in Medicare Supplement or commercial plans.

Member transitions

We know that members are impacted when we make changes to our network, and are taking steps to support members with smooth transitions to new care providers as appropriate to help ensure continuity of care.

We will be sending letters to affected members to notify them of care providers that will no longer participate in the —————– Medicare and Medicaid plan network as early as January 1, 2014 (network changes for New Jersey Medicaid plans have an October, 2013 effective date.) When appropriate, letters will suggest new care providers for members to consider for their ongoing care. Members are encouraged to call the number on their member ID card if they need help with identifying a new care provider.

In some plans, members may choose to continue seeing their current care providers on an out-of-network basis, in accordance with their out-of-network benefits. These changes have no impact on plan benefits, and members undergoing a treatment plan will be able to continue seeing out-of-network care providers consistent with federal requirements.

Provider directories

These network changes will be reflected in our online provider directory as of October 1, 2013. It is highly encouraged to refer to the online provider directory in all cases to confirm care provider network and panel status for all potential enrollees, as changes may not be reflected in previously printed and/or downloaded directories.

It is important to note that when searching for an in-network provider on the online directory, a provider’s “Accepting New Patients” status must indicate “OPEN“, even if the potential enrollee is an existing patient.

Talking points for member inquiries

Please refer to the Physician Network Changes – Frequently Asked Questions for Member Discussions that provide additional information and may be used in the event you receive any member inquiries.

****************************************************************

Lower Health Insurance Premiums to Come at Cost of Fewer Choices

By ROBERT PEAR

Published: September 22, 2013

WASHINGTON — Federal officials often say that health insurance will cost consumers less than expected under President Obama’s health care law. But they rarely mention one big reason: many insurers are significantly limiting the choices of doctors and hospitals available to consumers.

From California to Illinois to New Hampshire, and in many states in between, insurers are driving down premiums by restricting the number of providers who will treat patients in their new health plans.

When insurance marketplaces open on Oct. 1, most of those shopping for coverage will be low- and moderate-income people for whom price is paramount. To hold down costs, insurers say, they have created smaller networks of doctors and hospitals than are typically found in commercial insurance. And those health care providers will, in many cases, be paid less than what they have been receiving from commercial insurers.

Some consumer advocates and health care providers are increasingly concerned. Decades of experience with Medicaid, the program for low-income people, show that having an insurance card does not guarantee access to specialists or other providers.

Consumers should be prepared for “much tighter, narrower networks” of doctors and hospitals, said Adam M. Linker, a health policy analyst at the North Carolina Justice Center, a statewide advocacy group.

“That can be positive for consumers if it holds down premiums and drives people to higher-quality providers,” Mr. Linker said. “But there is also a risk because, under some health plans, consumers can end up with astronomical costs if they go to providers outside the network.”

Insurers say that with a smaller array of doctors and hospitals, they can offer lower-cost policies and have more control over the quality of health care providers. They also say that having insurance with a limited network of providers is better than having no coverage at all.

Cigna illustrates the strategy of many insurers. It intends to participate next year in the insurance marketplaces, or exchanges, in Arizona, Colorado, Florida, Tennessee and Texas.

“The networks will be narrower than the networks typically offered to large groups of employees in the commercial market,” said Joseph Mondy, a spokesman for Cigna.

The current concerns echo some of the criticism that sank the Clinton administration’s plan for universal coverage in 1993-94. Republicans said the Clinton proposals threatened to limit patients’ options, their access to care and their choice of doctors.

At the same time, House

Republicans are continuing to attack the new health law and are threatening to hold up a spending bill unless money is taken away from the health care program.

Dr. Bruce Siegel, the president of America’s Essential Hospitals, formerly known as the National Association of Public Hospitals and Health Systems, said insurers were telling his members: “We don’t want you in our network. We are worried about having your patients, who are sick and have complicated conditions.”

In some cases, Dr. Siegel said, “health plans will cover only selected services at our hospitals, like trauma care, or they offer rock-bottom payment rates.”

In New Hampshire, Anthem Blue Cross and Blue Shield, a unit of WellPoint, one of the nation’s largest insurers, has touched off a furor by excluding 10 of the state’s 26 hospitals from the health plans that it will sell through the insurance exchange.

Christopher R. Dugan, a spokesman for Anthem, said that premiums for this “select provider network” were about 25 percent lower than they would have been for a product using a broad network of doctors and hospitals.

Anthem is the only commercial carrier offering health plans in the New Hampshire exchange.

Peter L. Gosline, the chief executive of Monadnock Community Hospital in Peterborough, N.H., said his hospital had been excluded from the network without any discussions or negotiations.

“Many consumers will have to drive 30 minutes to an hour to reach other doctors and hospitals,” Mr. Gosline said. “It’s very inconvenient for patients, and at times it’s a hardship.”

State Senator Andy Sanborn, a Republican who is chairman of the Senate Commerce Committee, said, “The people of New Hampshire are really upset about this.”

Many physician groups in New Hampshire are owned by hospitals, so when an insurer excludes a hospital from its network, it often excludes the doctors as well.

David Sandor, a vice president of the Health Care Service Corporation, which offers Blue Cross and Blue Shield plans in Illinois, Montana, New Mexico, Oklahoma and Texas, said: “In the health insurance exchange, most individuals will be making choices based on costs. Our exchange products will have smaller provider networks that cost less than bigger plans with a larger selection of doctors and hospitals.”

Premiums will vary across the country, but federal officials said that consumers in many states would be able to buy insurance on the exchange for less than $300 a month — and less than $100 a month per person after taking account of federal subsidies.

“Competition and consumer choice are actually making insurance affordable,” Mr. Obama said recently.

Many insurers are cutting costs by slicing doctors’ fees.

Dr. Barbara L. McAneny, a cancer specialist in Albuquerque, said that insurers in the New Mexico exchange were generally paying doctors at Medicare levels, which she said were “often below our cost of doing business, and definitely below commercial rates.”

Outsiders might expect insurance companies to expand their networks to treat additional patients next year. But many insurers see advantages in narrow networks, saying they can steer patients to less expensive doctors and hospitals that provide high-quality care.

Even though insurers will be forbidden to discriminate against people with pre-existing conditions, they could subtly discourage the enrollment of sicker patients by limiting the size of their provider networks.

“If a health plan has a narrow network that excludes many doctors, that may shoo away patients with expensive pre-existing conditions who have established relationships with doctors,” said Mark E. Rust, the chairman of the national health care practice at Barnes & Thornburg, a law firm. “Some insurers do not want those patients who, for medical reasons, require a broad network of providers.”

In a new study, the Health Research Institute of PricewaterhouseCoopers, the consulting company, says that “insurers passed over major medical centers” when selecting providers in California, Illinois, Indiana, Kentucky and Tennessee, among other states.

“Doing so enables health plans to offer lower premiums,” the study said. “But the use of narrow networks may also lead to higher out-of-pocket expenses, especially if a patient has a complex medical problem that’s being treated at a hospital that has been excluded from their health plan.”

In California, the statewide Blue Shield plan has developed a network specifically for consumers shopping in the insurance exchange.

Juan Carlos Davila, an executive vice president of Blue Shield of California, said the network for its exchange plans had 30,000 doctors, or 53 percent of the 57,000 doctors in its broadest commercial network, and 235 hospitals, or 78 percent of the 302 hospitals in its broadest network.

Mr. Davila said the new network did not include the five medical centers of the University of California or the Cedars-Sinai Medical Center near Beverly Hills.

“We expect to have the broadest and deepest network of any plan in California,” Mr. Davila said. “But not many folks who are uninsured or near the poverty line live in wealthy communities like Beverly Hills.”

Daniel R. Hawkins Jr., a senior vice president of the National Association of Community Health Centers, which represents 9,000 clinics around the country, said: “We serve the very population that will gain coverage — low-income, working class uninsured people. But insurers have shown little interest in including us in their provider networks.”

***************************************************************************************************

http://allplanhealthinsurance.com

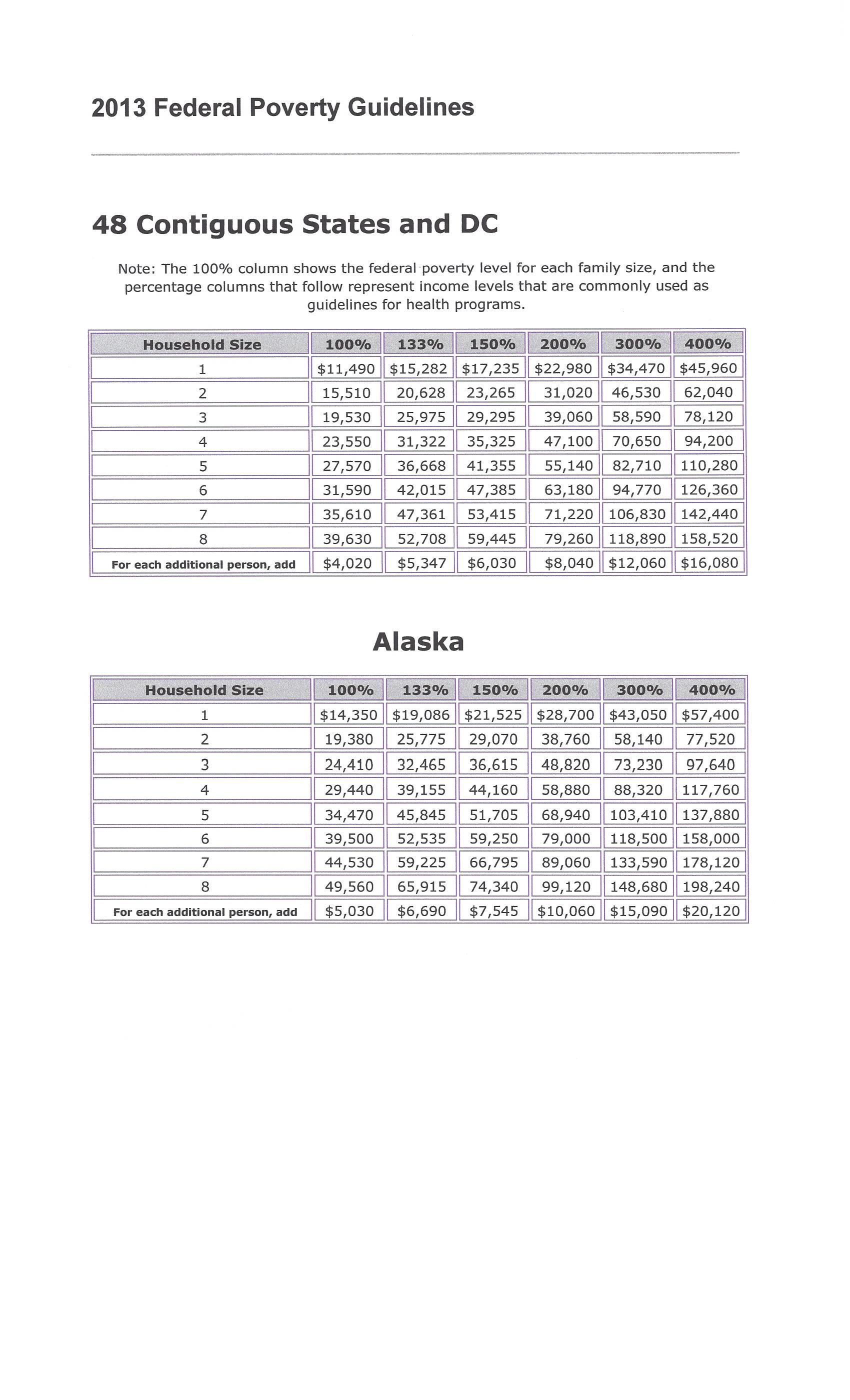

(CLICK ON IMAGE TO ENLARGE)

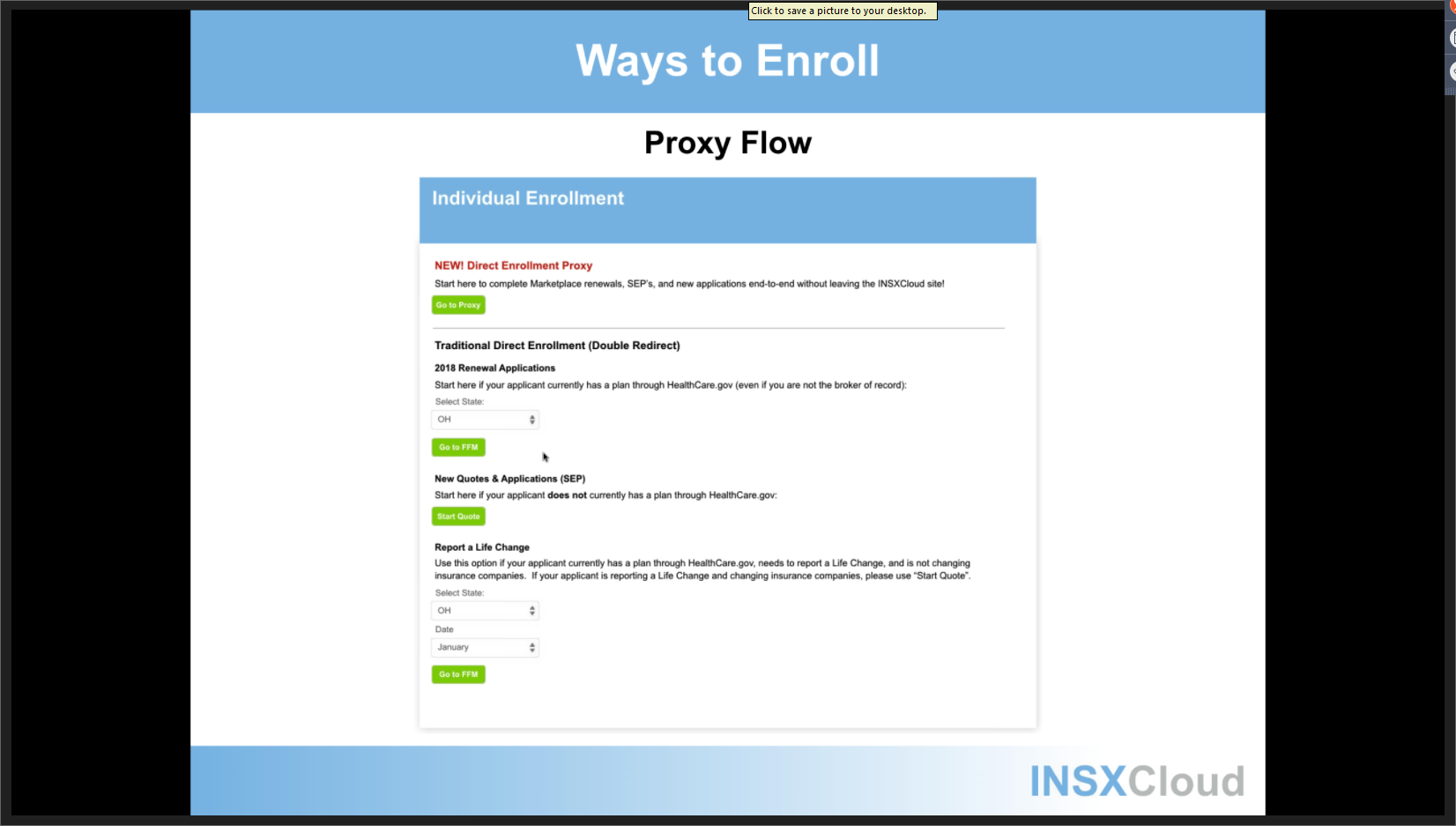

(CLICK ON IMAGE TO ENLARGE)