By Kenton Henry, Administrator

Let me preface this article with an admission. I am a health insurance broker and have been for 27 years. So consider that as you weigh the comparison suggested in the title of this piece.

Very shortly (October 1 to be exact) you are going to be able to enroll in a new Affordable Care Act (ACA) compliant health insurance plan to be effective January 1. Having health insurance at that time is no longer an option – it is a mandate. You probably know this by now and there is no need to review the details and I will not be addressing the penalties for not having coverage next year and beyond. Rather, I will be addressing your options for enrolling and factors you might want to weigh before electing the path you take to enrollment. I will strive to be as objective as possible in light of my preface.

First, let’s consider going through an insurance agent or broker like myself. Before I could consider selling my first health insurance policy back in 1986, I had to study for and pass my state’s insurance exam in order to obtain my license. I did this initially in Indiana and again in 1991 when I moved to Texas. While not the Bar Exam or Medical Board Exams – on both occasions they were comprehensive tests and I recall spending weeks of self-study in the quiet of the local library for the first and–after 5 years of experience–another week and a 40 hour prep course to boot for the second. They covered my knowledge of things not the benefit of common sense–and they were certainly not IQ tests–but measured my grasp of esoteric insurance laws, regulations, the principles and components of insurance and ethics among other topics. Next, I had to be appointed with an insurance company before I could represent their products. In addition to an application, an appointment entailed a thorough background and credit check. Approximately twenty years ago, every company with whom I applied to for an appointment made it mandatory I purchase errors and omissions coverage just as required of your attorney or doctor. Every person is fallible and the insurance makes certain an agent’s clients can be compensated for any negligence or unintentional mistake on the agent’s part resulting in the client’s harm. Fortunately, I have never had to file a claim with my E & O company nor have I had a complaint filed against me with a state insurance commission. I must also undergo and complete a minimum of 30 hours of continuing education every 24 months in order to keep my license. A record of this is made the State Insurance Commissioner. My license binds me to the same rules and regulations regarding my client’s privacy, confidentiality and personal information as the aforementioned professionals with whom you share the same type of information. Any compromise in it could result in revocation of my license not to mention civil liability on my part.

Who pays for these tests, licenses, continuing education and insurance? I do. It comes out of my personal income. Not to mention the cost of all my supplies, office overhead and gas utilized in seeing my clients at their convenience. Oh yeah . . . and I pay for my own health insurance. And I have never minded these expenses. These are merely the costs of doing business and I was happy to pay them when compared to the alternative which would have required being someone’s employee. So these are pretty much the facts as to my professional background, what is required of me and the protection afforded you by such.

Before contrasting this with the alternative – consider:

“The 2010 (ACA) law is intended to prod millions of Americans to buy health insurance, many for the first time. Those seeking coverage must provide details on citizenship, family size and income to determine whether they’re eligible for subsidies, and complete a form that can stretch to seven pages.” – Bloomberg 08.23.13

And the alternative to licensed agent or broker? As of October 1st, you will also have the option of going through a “Navigator” hired by your state and whose compensation will be subsidized with federal funds. (Clue: federal funds is code for your tax dollars). The Navigator’s job is to be educate you as to your options and help you elect one before being turned over to an enroller, otherwise known as a customer service representative. The latter will make this happen mechanically and it will most likely be accomplished by you going to a link and completing an electronic enrollment form estimated to be up to 21 pages or greater in length. (We don’t know yet. They and the premiums for coverage are yet to be released.)

While the requirements will vary from state to state, the federal requirements for Navigators are 20 hours of training. The federal health insurance exchange will apply in Texas, Indiana and Ohio. These are three of four states where I am licensed. There will be no background checks involved in the hiring process for Navigators as we are told there is no time for such. The administration says “we need to get as many people as possible to sign up as quickly as possible.” The Navigators will not be licensed. They will not pay for errors and omissions insurance. You will pay for their supplies, their insurance and their benefits.

I certainly don’t have to be your agent but these are factors you might want to consider before seeking assistance in enrolling in your new health insurance plan. If you feel I have unfairly or otherwise misrepresented things, please feel free to comment as much. In the feature articles below, some opposing or off-setting opinions are expressed–mostly by administration officials.

Admin. – Kenton Henry

************************************

Coming Articles: Biggest Traps of the Affordable Care Act for Medicare Recipients

************************************

Feature Articles:

BLOOMBERG August 23, 2013

State Laws Hinder Obamacare Effort to Enroll Uninsured

By Alex Nussbaum & Alex Wayne – Aug 23, 2013 2:32 PM CT

New laws passed by a dozen Republican-led states, the latest in Missouri last month, may make that harder, imposing licensing exams, fines that can run as high as $1,000 and training that almost doubles the hours required by the federal government. Republicans say the measures will protect consumers. Obamacare supporters say they’ll undermine the effort to get as many people as possible enrolled.

The rules are “like voter intimidation,” said Sara Rosenbaum, a health law professor at George Washington University in Washington, D.C., who supports Obama’s act. “In many, many cases these laws may be a direct interference with outreach assistance and that’s going to be quite serious.”

The Obama administration awarded 105 grants last week, steering money to hospitals, social-service agencies, local clinics and other groups. The navigators are meant to offer “unbiased information” to help people through the complexities of the new system, with its deductibles, copays, provider networks and tax credits, according to an Aug. 15 statement from the U.S. Department of Health and Human Services.

October Deadline

The grants were issued barely a month before the online exchanges are scheduled to open for enrollment on Oct. 1. The administration has said about 7 million people may enroll next year and it needs to motivate millions of young, healthy customers to sign up to keep the markets financially stable.

The state laws may complicate that task. The restrictions go farthest in a handful of states like Georgia and Missouri, where Republican legislators have already refused to set up the new insurance websites or spend money to promote the law.

In Florida this week, Governor Rick Scott told a Miami audience that federal privacy protections for consumers working with navigators were “behind schedule and inadequate.” He urged people to use brokers and agents instead.

Georgia Governor Nathan Deal, a Republican, believes navigators need state regulation because they’ll give advice on “a highly complicated and highly important topic,” his spokesman, Brian Robinson, said in an e-mail. They will also handle personal information that is open to abuse.

Consumer Protection

“This is a consumer protection issue more than anything,” said Kenneth Statz, an insurance broker on the legislative council of the National Association of Health Underwriters, a Washington-based group representing agents and brokers. “We just want to make sure that somebody who is sitting down with a consumer, trying to help them make this major decision, is going to be properly prepared.”

The state laws have passed with the backing of insurance agents and brokers, who view the online exchanges as competition and navigators as potential rivals with an unfair advantage absent new rules.

States require agents to be licensed and undergo periodic training, said Statz, who’s based in Brecksville, Ohio. He also has to carry insurance to protect clients who may be hurt by bad advice or malpractice, he said.

The 2010 law is intended to prod millions of Americans to buy health insurance, many for the first time. Those seeking coverage must provide details on citizenship, family size and income to determine whether they’re eligible for subsidies, and complete a form that can stretch to seven pages.

Federal Requirements:

While states controlled by Democrats such as Maryland, New York, Minnesota and Illinois have also passed rules, these generally follow federal requirements, said Mark Dorley, a health-policy researcher at George Washington University.

Other states have been more restrictive.

Georgia’s navigators need a license from the insurance commissioner. Each person assisting the uninsured has to pay a $50 application fee, complete 35 hours of training — 15 more than the federal requirement — pass an exam, and complete a criminal background check. Licenses must be renewed every year, requiring another $50 and 15 more hours of training.

Missouri defines navigators more broadly than the federal government, said Andrea Routh, executive director of the Missouri Health Advocacy Alliance in Jefferson City. Violating certification requirements risks a $1,000 fine.

Seeking License

Routh’s group, which seeks to educate people on the health law, didn’t apply for a grant. It may seek a license just to be safe, she said.

“Anyone who does outreach and education, or anybody who assists anyone with enrollment had better be checking that law to see if they need to be licensed,” she said.

Missouri voters approved a ballot initiative last year barring Governor Jay Nixon, a Democrat, from setting up the exchange without the assent of the Republican-controlled legislature, which has declined to act so far.

The rules may scare off churches, clinics or others who want to help, said Cindy Zeldin, executive director of Georgians for a Healthy Future. The Atlanta-based nonprofit was part of a group that won a $2.1 million grant.

Georgia’s law implies “navigators are somehow problematic,” she said in a telephone interview, “rather than that they’re groups that likely have a history of working in communities and are trusted.”

‘In Conversations’

The Obama administration has been “in conversations with states” to ensure their laws don’t hinder the effort, said Chiquita Brooks-Lasure, a deputy director at the federal health department, in an Aug. 15 conference call with reporters.

The federal law doesn’t require background checks, though navigators must provide quarterly reports and can lose their grants in cases of fraud or abuse. The administration is requiring them to undergo an initial 20 hours of training.

Some people opposed to Obama’s overhaul “want to see it fail,” said Missouri Health’s Routh. “If you put a lot of barriers in place that make it tough for nonprofits to go out and educate people and assist them in understanding the exchange, that may be one way to have it fail.”

******************************

The Washington Post

Health and Science

States scramble to get health-care law’s insurance marketplaces up and running

By Sarah Kliff and Sandhya Somashekhar, Published: August 24

With a key deadline approaching, state officials across the country are scrambling to get the Affordable Care Act’s complex computer systems up and running, reviewing contingency plans and, in some places, preparing for delays.

Oct. 1 is the scheduled launch date for the health-care law’s insurance marketplaces — online sites where uninsured people will be able to shop for coverage, sometimes using a government subsidy to purchase a plan. An estimated 7 million people are expected to use these portals to purchase health coverage in 2014.

The task is unprecedented in its complexity, requiring state and federal data systems to transmit reams of information between one another. Some officials in charge of setting up the systems say that the tight deadlines have forced them to take shortcuts when it comes to testing and that some of the bells and whistles will not be ready.

“There’s a certain level of panic about how much needs to be accomplished but a general sense that the bare minimum to get the system functional will be done,” said Matt Salo, executive director of the National Association of Medicaid Directors. “It will by no means be as smooth and as seamless as people expected.”

Oregon announced this month that it will delay consumers’ direct access to its marketplace, opening the Web site only to brokers and consumer-assistance agents in order to shield consumers from opening-day glitches.

“Even though we’re testing now, once you actually have the system up, you don’t know what the bugs will be,” said Amy Fauver, spokeswoman for Cover Oregon, the state agency implementing the law there.

In California, which has the nation’s largest uninsured population, health officials have begun hinting that they may have a similar problem.

“It’s a complex system, and there’s a lot of navigation that needs to happen,” said Oscar Hidalgo, a spokesman for Covered California. He said the agency will know by early September whether the system will be ready in time.

If not, he said, customers will still be able to log on to the Web site and peruse insurance plans and view prices. When they get to the final step, however, they will not be able to sign up. They will have to contact a customer service representative to complete the final enrollment step.

Officials with the District of Columbia’s Health Link decided to put off building a Spanish version of its Web site until later this year, giving its staff bandwidth to complete other tasks they see more critical to the launch.

Until then, the District will have bilingual call-center workers and in-person helpers who will be able to help Spanish speakers navigate the site.

The hiccups are troubling to advocates, who worry that there will be mistakes that result in people being erroneously rejected by Medicaid or denied subsidies to which they are entitled. They are concerned that impediments will discourage the uninsured from signing up for coverage.

“There will be something up and running, but there will be serious, serious difficulties with it” that could result in delays and errors initially, said Robert H. Bonthius Jr., a lawyer at the Legal Aid Society of Cleveland. “It’s an extremely ambitious program, well-intentioned, that is going to be very difficult to accomplish, and it’s going to be months and maybe years before it really gets sorted out.”

With a key deadline approaching, state officials across the country are scrambling to get the Affordable Care Act’s complex computer systems up and running, reviewing contingency plans and, in some places, preparing for delays.

Oct. 1 is the scheduled launch date for the health-care law’s insurance marketplaces — online sites where uninsured people will be able to shop for coverage, sometimes using a government subsidy to purchase a plan. An estimated 7 million people are expected to use these portals to purchase health coverage in 2014.

See how the states have sided on some of the key provisions of the Affordable Care Act:

The task is unprecedented in its complexity, requiring state and federal data systems to transmit reams of information between one another. Some officials in charge of setting up the systems say that the tight deadlines have forced them to take shortcuts when it comes to testing and that some of the bells and whistles will not be ready.

“There’s a certain level of panic about how much needs to be accomplished but a general sense that the bare minimum to get the system functional will be done,” said Matt Salo, executive director of the National Association of Medicaid Directors. “It will by no means be as smooth and as seamless as people expected.”

Oregon announced this month that it will delay consumers’ direct access to its marketplace, opening the Web site only to brokers and consumer-assistance agents in order to shield consumers from opening-day glitches.

“Even though we’re testing now, once you actually have the system up, you don’t know what the bugs will be,” said Amy Fauver, spokeswoman for Cover Oregon, the state agency implementing the law there.

In California, which has the nation’s largest uninsured population, health officials have begun hinting that they may have a similar problem.

“It’s a complex system, and there’s a lot of navigation that needs to happen,” said Oscar Hidalgo, a spokesman for Covered California. He said the agency will know by early September whether the system will be ready in time.

If not, he said, customers will still be able to log on to the Web site and peruse insurance plans and view prices. When they get to the final step, however, they will not be able to sign up. They will have to contact a customer service representative to complete the final enrollment step.

Officials with the District of Columbia’s Health Link decided to put off building a Spanish version of its Web site until later this year, giving its staff bandwidth to complete other tasks they see more critical to the launch.

Until then, the District will have bilingual call-center workers and in-person helpers who will be able to help Spanish speakers navigate the site.

The hiccups are troubling to advocates, who worry that there will be mistakes that result in people being erroneously rejected by Medicaid or denied subsidies to which they are entitled. They are concerned that impediments will discourage the uninsured from signing up for coverage.

“There will be something up and running, but there will be serious, serious difficulties with it” that could result in delays and errors initially, said Robert H. Bonthius Jr., a lawyer at the Legal Aid Society of Cleveland. “It’s an extremely ambitious program, well-intentioned, that is going to be very difficult to accomplish, and it’s going to be months and maybe years before it really gets sorted out.”

******************************************************************************

http://allplanhealthinsurance.com

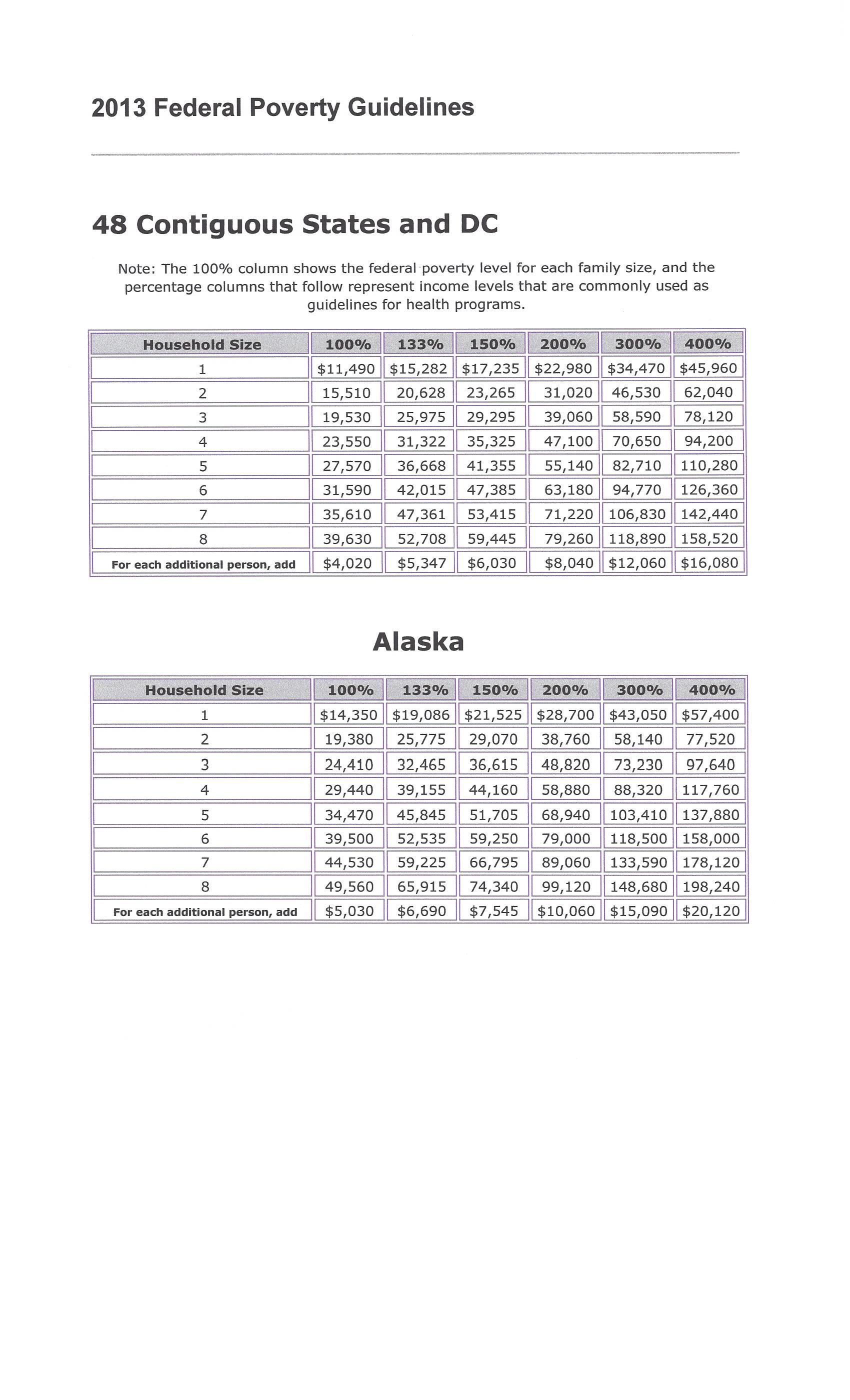

(CLICK ON IMAGE TO ENLARGE)

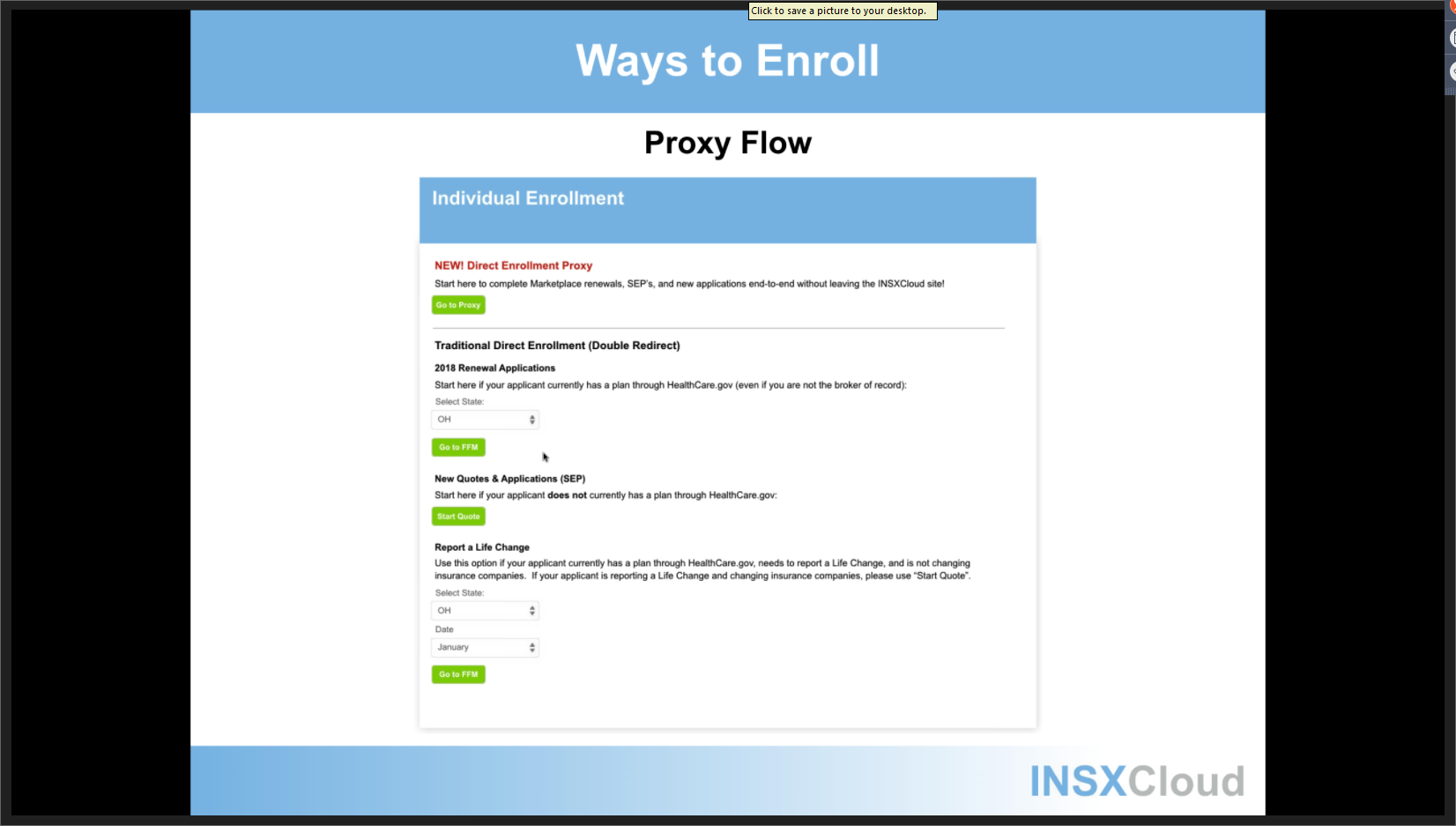

(CLICK ON IMAGE TO ENLARGE)