By D. Kenton Henry Broker, editor 19 April 2022

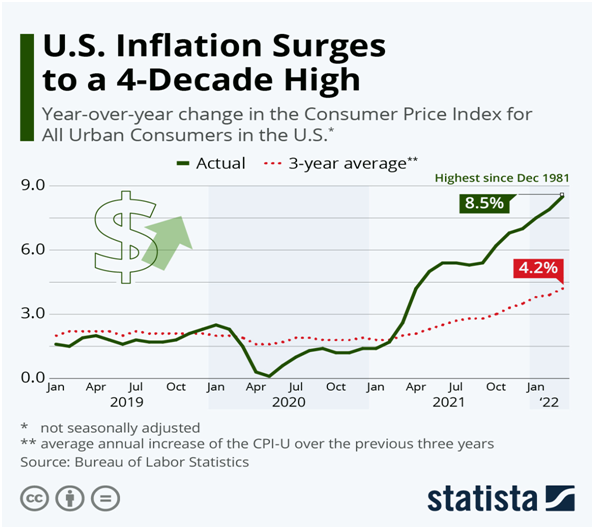

While inflation has costs for necessities, such as gas and food items, skyrocketing to an average of 8.5% in March and much higher for the aforementioned items – Social Security saw fit to only increase the Income Benefit to SSI recipients to 5.9%. Seniors, many of whom are subsisting on fixed incomes, might be able to cut their need for gasoline, but I do not know any who can get by without food, shelter, and electricity. Many are struggling to pay their bills already, and inflation shows little sign of abating.

This was only until 09/2021, at which time, apparently only apples inflated lower than our current rate of inflation.

But how about the argument that all this inflation is due to Putin and the war in Ukraine? Russia launched a full-scale assault on Ukraine February 22. One month after the end of the timeline in the chart below.

When was our current president inaugurated? . . . Answer: January 20, 2021. Take a look at the green line above charting the Consumer Price Index on that date. (I will leave it at that.)

To add insult to injury, the Centers for Medicare and Medicaid Services (CMS) increased Part B (outpatient care) premiums by 15% to a base premium -for those with an annual income of less than or equal to $91,000 – to $170.10 per month. Thank you very much!

However, as described in Feature Article 1 below, due in part to a 50% cut in the cost of a $56,000 Part D covered drug, CMS is considering reducing that Part B Premium. My experience is that the government seldom gives back what they are already receiving . . . but one can only hope.

For those involved in Marketplace medical coverage – health insurance for individuals and families under the age of 65 – the opposite action on the part of the Department of Health and Human Services may occur. Specifically, the extended enhanced premium tax credits made available by the American Rescue Plan, which enabled an additional 3 million Americans to receive a subsidy lowering their net monthly premium to as low as $0, are set to expire at the end of the year. As described in Feature Article 3 below, it is estimated 4.9 million more people will go uninsured if enhanced benefits are not extended. Never mind it is estimated the extension of such would increase the federal deficit by $305 billion dollars. Of course, the Treasury can simply print more money, further increasing inflation and diminishing the buying power of one’s paycheck or Social Security Income.

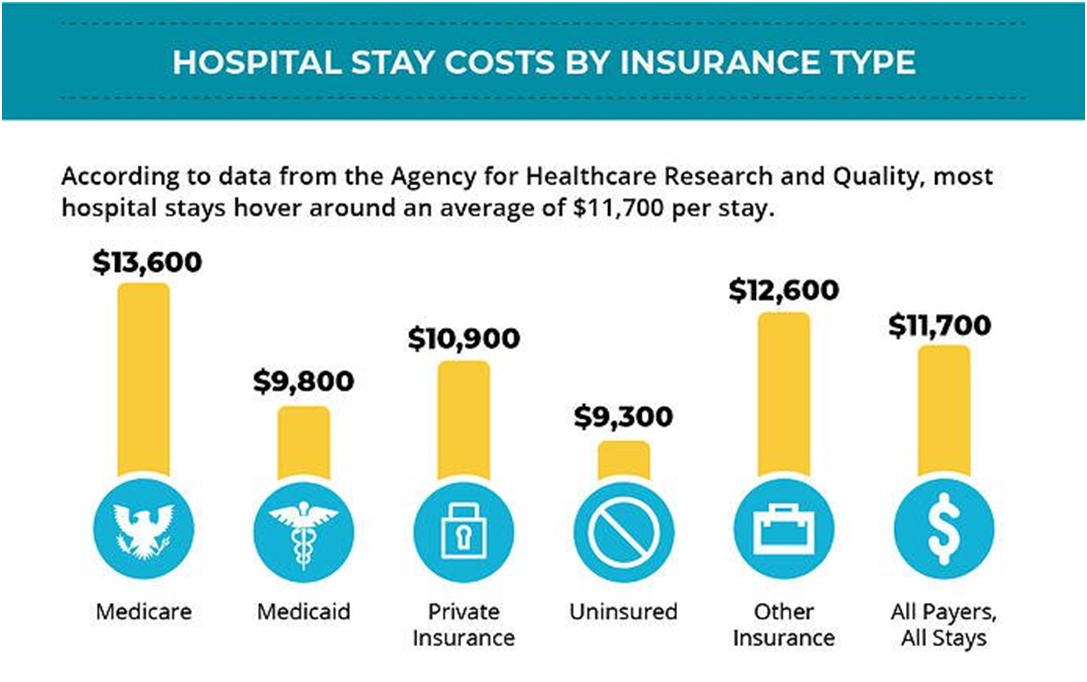

Lastly, medical expenses are no exception to inflation. If you wonder why health insurance premiums or out-of-pocket costs for healthcare are being affected, refer to article 3 below. They start high and increase as one goes from a doctor’s office to an Urgent Care facility to a hospital emergency room. Avoid the latter unless it is a true emergency because it will cost an average of $444 for low to moderate severity treatment. Heaven, forbid you have an overnight stay in a hospital without medical insurance because the average cost is $11,700. As cited in the chart below, it only goes up depending on the type of insurance you have.

Should your stay extend to three days, expect to cost to be an average of $30,000. And what if you don’t have health insurance? Here are the average costs of various treatments.

Take a look at what you might pay for each hospital bill without insurance:

*(Data from the Agency for Healthcare Research and Quality)

While I cannot guarantee we have seen the worst of inflation – let alone that the government is going to provide us any meaningful relief in the immediate future. But I am here to assist you in acquiring medical coverage, which gives you access to the care and treatment you need to regain or preserve your health without being financially ruined. I will do my best to help you maintain access to as many of your preferred medical doctors and hospitals as the present market allows. I do not charge a fee for my services. There is no additional cost for the insights and value of my 36 years of experience in the health and Medicare-related insurance market. Neither is there any additional cost in acquiring an insurance product through me than if you walked through the door of your preferred insurance company and purchased their product directly from them. There is no obligation to take my learned advice.

Please give me a call and let’s discuss your situation before the very busy “Open Enrollment” Periods are upon us and everyone is scrambling to mitigate what are almost certain to be the increasing costs of health care

.

Office: 291-367-6565 Text my cell 24/7 @ 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com Https://TheWoodlandsTXHealthInsurance.com Https://Allplanhealthinsurance.com

*********************************************************************************************************

FEATURED ARTICLE 1

FIERCE HEALTHCARE

CMS, FDA present united front against criticism of Aduhelm coverage decision

AHIP applauded CMS for covering the drug and “related services such as PET scans if required b the trial protocol.”

Other stakeholders said that now the coverage decision has been finalized it is time for CMS to take action on lowering Part B premiums.

CMS has yet to announce any final decision on Part B premiums, which is increased by 15% for 2022. A key reason was the $56,000 price tag for Aduhelm.

However, Department of Health and Human Services Secretary Xavier Becerra announced in January that the agency was rethinking the 15% hike after Biogen halved the price of Aduhelm in December.

Becerra told reporters on Tuesday before the coverage decision that he was waiting to see what “CMS gives back to us in terms of their assessment and then once we get that information we will see where we go.”

CMS told Fierce Healthcare on Friday that it has yet to decide on a redetermination for the premium.

But advocates are hoping the agency moves faster on scaling back the premium hike.

“Medicare beneficiaries struggling to pay their bills need relief from this year’s premium increase as soon as possible,” said Max Richtman, president and CEO of the National Committee to Preserve Social Security and Medicare.

Pharma and Alzheimer’s disease patient advocacy groups slammed the decision, however, noting that it will hamper access to the drug.

“CMS has further complicated matters by taking the unprecedented step of applying different standards for coverage of medicines depending on the FDA approval pathway taken, undermining the scientific assessment by experts at FDA,” said Nicole Longo, spokeswoman for the Pharmaceutical Research and Manufacturers of America, in a statement.

*********************************************************************************************************

FEATURED ARTICLE 2

BENEFITSPRO.COM

End to ACA tax credits could leave 3 million uninsured

But extending the enhanced credits would increase the federal deficit by $305 billion over 10 years.

By Alan Goforth | April 08, 2022 at 09:32 AM

Congress would need to act by midsummer to give marketplaces, insurers and outreach programs time to prepare for the 2023 open enrollment period.

More than three million people could lose insurance coverage if enhanced premium tax credits included in the American Rescue Plan expire at the end of this year, according to a new report from the Urban Institute. The American Rescue Plan Act of 2021 increased credits for Marketplace insurance coverage and extended eligibility to more individuals.

“If Congress does not extend these benefits, marketplace enrollment will most likely fall and the number of people uninsured will increase,” said Jessica Banthin, senior fellow at the organization. “Our findings show that 4.9 million fewer people will be enrolled in subsidized Marketplace coverage in 2023 if the enhanced credits aren’t extended. This comes at a pivotal time when millions of people will be losing Medicaid as the public health emergency expires.

*********************************************************************************************************

FEATURED ARTICLE 3

Average charges for 8 common procedures across ER, retail and urgent care settings

Alia Paavola – Wednesday, March 30th, 2022

In 2020, the median charge for a 30- to 44-minute new patient office visit ranged from $164 in a retail clinic to $234 in an urgent care center, according to a March report from Fair Health.

For the report, Fair Health, an independent nonprofit focused on enhancing transparency of healthcare costs and health insurance information, analyzed billions of private healthcare claims records from its database.

Below is the average charge for eight common procedures, as identified by CPT code, performed in retail, urgent care and emergency room settings:

Retail

- Office outpatient visit 20-29 minutes (99213): $114

- Streptococcus test (87880): $36

- Immunization administration (90471): $33

- Office outpatient visit 30-39 minutes (99214): $159

- Office outpatient, new, 30-44 minutes (99203): $164

- Flu test (87804): $42

- Office outpatient, new, 15-29 minutes (99202): $131

- Flu vaccination (90686): $31

Urgent care

- Office outpatient visit 30-39 minutes (99214): $232

- Office outpatient visit 20-29 minutes (99213): $174

- Office outpatient, new, 30-44 minutes (99203): $234

- Streptococcus test (87880): $43

- Office outpatient, new, 45-59 minutes (99204): $313

- Flu test (87804): $46

- Therapeutic, prophylactic or diagnostic injection (96372): $59

- Office outpatient visit, new, 15-29 minutes (99202): 178

Emergency room

- Emergency department visit — high severity/life-threatening (99285): $1,262

- Emergency department visit — high/urgent severity (99284): $919

- Emergency department visit — moderate severity (99283): $624

- Electrocardiogram (93010): $54

- Single-view chest X-ray (71045): $58

- CT head/brain without contrast material (70450): $323

- Two-view chest X-ray (71046): $69

- Emergency department visit — low/moderate severity (99282): $444