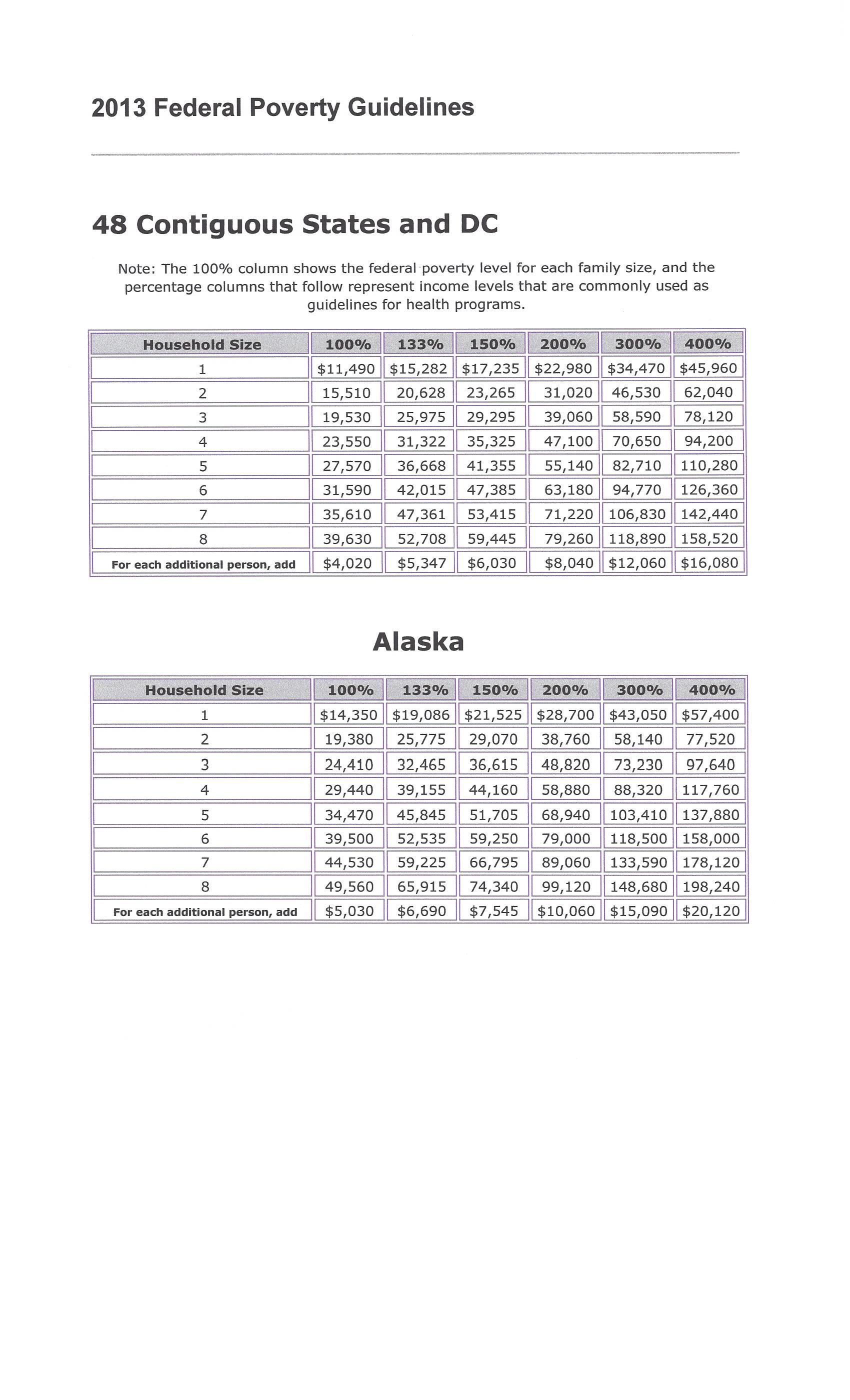

As a licensed agent in Texas, Indiana, Ohio and Michigan I am certified with the Department of Health and Human Service through the Center for Medicare Service to enroll residents of those states in health insurance plans for 2014. This is whether they qualify for a subsidy or not. Premiums are the same whether you go through me, the Marketplace (Federal Exchange) or a Navigator. And I would like to assist you. Problem is – 5 days into the enrollment phase of the Affordable Care Act (ACA) I still have not succeeded in being able to create even my own account to see what all my options are. I have seen many of my options outside the Marketplace–in the private market–and my quoted premium is approximately 33% higher than my current premium for comparable coverage! I have read all news articles relative to enrollment numbers and although the White House says people are enrolling in the Marketplace (which is where residents of these states go for quotes unless coming to me) and–as of yesterday–no journalist has been successful in finding and interviewing one individual who has successfully purchased health insurance in the Marketplace! One individual, Chad Henderson, reported he and his father had but when swarmed by journalist and asked for details – his father said neither he or his son had. Turns out Chad was a campaign worker for the Obama administration last year and an active volunteer for Organizing for Action, the former campaign organization that now advocates for the President’s legislative agenda. You figure it out. This much I know – if you already know that based on your estimated income for 2014 you will not qualify for a subsidy – you should apply for coverage through me and avoid the wait (however long) on the Marketplace website. You can see your options and go directly into your chosen health insurance companies application for the plan you select.

If, ultimately, you qualify for a subsidy – you may be relatively satisfied with your premium but it looks like (in order for that to be the case) you will have to accept a deductible much higher than what you anticipated. If you do not qualify for a subsidy – prepare for what in all likelihood will be sticker shock.

Regardless, I have made about 15 unsuccessful attempts, consuming hours of wait time the last 5 days to open an account in the Marketplace and–for research purposes– obtain my own quotes and see what subsidy options look like. Even Chad Henderson claimed it took him 3 hours to create an account–and this allegedly took place at 3 a.m. in the morning! How am I supposed to take my clients who will qualify for a subsidy from my quoting engine into the online Marketplace and have us succeed in staying with each other while we wait hours for us to set up their account? Of course, these wait times will surely decrease over time, right? Errrrr . . . right?

Admin. – Kenton Henry

****************************************************************

FEATURE ARTICLE

UPDATED: Obamacare Poster Boy Chad Henderson and His Dad Didn’t Really Buy Insurance

An exclusive Reason.com interview with Bill Henderson.

Peter Suderman | October 4, 2013

UPDATED at 2.54pm ET: Scroll to end of this article for the latest development in this story. After speaking directly with Chad Henderson, The Washington Post has confirmed that he has not in fact enrolled in a health-care plan.

Chad Henderson is the media’s poster boy for Obamacare. Reporters struggled this week to find individuals who said they had been able to enroll in one of the law’s 36 federally run health-insurance exchanges.

That changed yesterday, when they found Henderson, a 21-year-old student and part-time child-care worker who lives in Georgia and says that he successfully enrolled himself and his father Bill in insurance plans via the online exchange administered at healthcare.gov.

But in an exclusive phone interview this morning with Reason, Chad’s father Bill contradicted virtually every major detail of the story the media can’t get enough of. What’s more, some of the details that Chad has released are also at odds with published rate schedules and how Obamacare officials say the enrollment system works.

The coverage of Chad Henderson has been massive. He was featured in The Washington Post Thursday as “the Obamacare enrollee that tons of reporters are calling.” He was also profiled in The Huffington Post as someone who “beat the glitches to sign up for Obamacare.” He was interviewed by Politico, multiple local news organizations, and, according to his Facebook feed, was asked to be part of a conference call hosted by the Department of Health and Human Services.

Chad’s story was tweeted out by the official Obamacare Twitter feed. It was promoted to the media by Enroll America, a health-care activist group headed by a former White House communications staffer, as a sign of Obamacare’s success. Henderson told reporters at multiple news outlets that after a three-hour wait to sign up online, he enrolled around 3 a.m. Tuesday morning in an unsubsidized private insurance plan that would cost him about $175 a month. He also said that his father enrolled in separate coverage plan that would cost about $250 a month after factoring in the subsidies for which his father qualified on his approximately $24,000 annual income.

Chad’s decision to purchase his own, separate plan might surprise some. A monthly premium of $175 would represent about 30 percent of his pre-tax take home pay—about $583 a month on the $7,000 part-time income he claimed. And he could have chosen to be covered by his father’s plan, which, under the Affordable Care Act, would have been required to cover dependents up to the age of 26. Chad said his father encouraged him to be covered under his own plan, even though the cost was higher. “He’s old school, so he wants me to take responsibility,” Chad told The Huffington Post.

Henderson’s story was promoted as proof that the new health law can work for individuals. That was exactly how Chad intended it. He was a volunteer with President Obama’s campaign last year, and his LinkedIn page still lists him as an active volunteer with Organizing for Action, the former campaign organization which now advocates for the president’s legislative agenda.

He told The Washington Post that he was sharing his story because he wanted the new health law to succeed.

“I’ve read a few articles about how young people are very critical to the law’s success,” he said to The Post. “I really just wanted to do my part to help out with the entire process.”

But details of Chad’s story proved difficult to verify. And in a phone interview conducted this morning, Chad’s father Bill contradicted major details of Chad’s story. I reached Bill Henderson by following a series of links at Chad’s Facebook page, through which I was able to speak directly to the father.

Bill Henderson told me that both he and his son were interested in getting coverage, but that he had not enrolled in any plan yet, and to his knowledge, neither had his son. He also said that when they do enroll, getting the most coverage for the least money would be the goal, and that he expects that he and his son will get coverage under the same plan.

Bill told me that Chad had been looking into plans online. “He told me that there’s different plans. And we haven’t decided which plans to enroll in yet.”

I asked him whether he and his son had talked about going on separate plans, and he told me that, “We’ll probably go on the same plan, more than likely.”

******************************************************************************************************