Well folks, here we are into the third week since the highly touted, much anticipated opening of the federal and state exchanges for purposes of enrolling in a health care act compliant insurance plan for 2014. And guess what? While a few state exchanges are experiencing some, generally small, measure of success – the federal exchange, or Marketplace, remains a dismal failure. It is, however, an excellent painful and protracted self-flagellating exercise in frustration. For an analogy–imagine having a root canal absent anesthesia while listening to Debbie Boone’s, “You Light Up My Life” on a continuous sound track loop through the entire procedure. Just to make the comparison more accurate, imagine you are Dustin Hoffman’s character who is tortured with a dentist’s drill in the movie Marathon Man but your experience is enhanced as your hygienist pulls your toe nails out with a pair of needle nose pliers in order to distract you from your oral discomfort. And that, I believe, is a pretty fair comparison to the enjoyment of opening an account and obtaining quotes for health insurance in the Marketplace to date. The tax payer’s cost to deliver this electronic equivalent of a Halloween visit to a House of Horrors? Current estimates are over $500 million and growing as desperate measures are being made to fix all its glitches as this goes to press. This after the Department of Health and Human Services accepted the low bid of $55 million with a ceiling of $93.7 million from Canadian software company, CGI Federal. Canadian? Really? All that U.S. taxpayer money to a Canadian firm? (I’m not even going there.)

But relax, dear patient. Let’s apply a little Novocain to your orifice. Let’s give you a subsidy to help ease the pain you will suffer when you see the highly inflated cost of health insurance you are now commanded to purchase under threat of penalty.

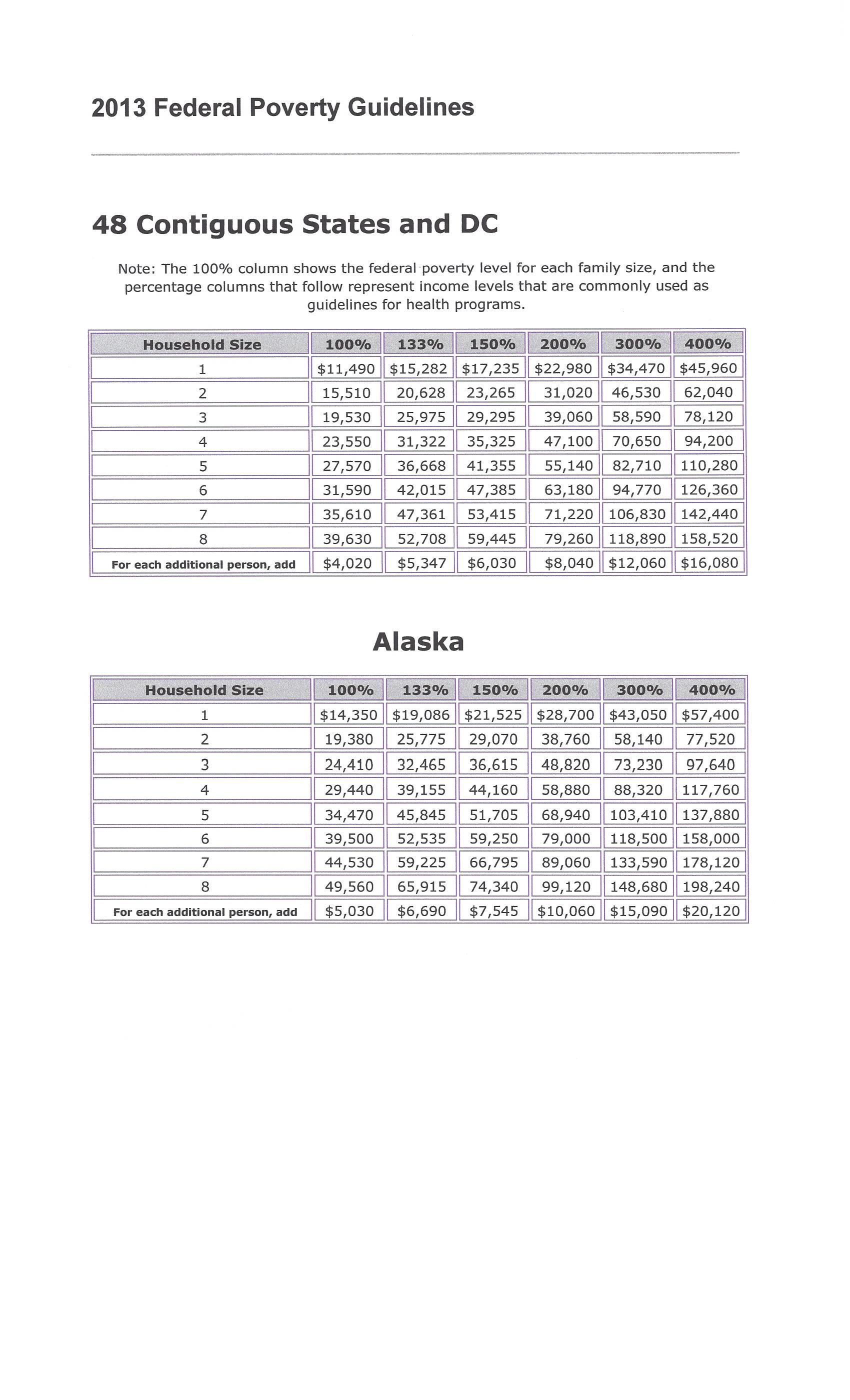

People making between 100 and 400 percent of federal poverty level can qualify for the premium tax credit health insurance subsidy. Federal poverty level changes every year, and is based on your income and family size.

Using 2013 FPL levels, you’ll qualify as an individual with an income range of $11,490-$45,960, a couple with an income of $15,510-$62,040, and a family of three earning $19,530-$78,120.

Just how do you calculate your subsidy?

In order to calculate how much your premium tax credit (subsidy) will be – you have to know 2 things:

(A) Your expected contribution toward the cost of your health insurance (available at the end of this article); and

(B) The cost of your BENCHMARK health plan. (Your health insurance exchange–assuming you succeed in opening an account and obtaining quotes–can tell you which plan this is and how much it costs. Your benchmark plan is the silver-tiered health plan with the second lowest monthly premiums in your area. The Affordable Care Act classifies health plans based on how much of your health care costs they’re expected to cover. A bronze health plan will cover about 60 percent of the average person’s health care costs. A silver health plan will cover about 70 percent.)

Your subsidy amount is the difference between your expected contribution and the cost of the benchmark plan. But just because the benchmark plan is used to calculate your subsidy doesn’t mean you have to buy the benchmark plan. You may buy any plan listed on your health insurance exchange, but your subsidy amount stays the same.

If you choose a more expensive plan, you’ll pay the difference plus your expected contribution. If you choose a plan that’s cheaper than the benchmark plan, you’ll pay less since the subsidy money will cover a larger portion of the monthly premium. If you choose a plan so cheap that costs less than your subsidy, you won’t have to pay anything for health insurance. However, you won’t get the excess subsidy back.

If you’re trying to save money so you choose a plan with a lower value, (like a bronze plan instead of a silver plan), you’ll likely have higher coinsurance and copays when you use your health insurance.

There’s another reason to choose a silver-tier plan. There’s a different subsidy that lowers copays, coinsurance, and deductibles for some low-income people. Eligible people can use it in addition to the premium tax credit subsidy. However, it’s only available to people who choose a silver-tier plan.

One question I am frequently asked is, “Do I have to wait until I file my income tax return in order to get the subsidy?”

Answer: “No”

You can get the premium tax credit in advance. If your income is so low you don’t have to file a tax return, you can still get the subsidy. But bear in mind–if you underestimate your income and take a subsidy–you will be forced to pay it back or, if you are due a refund, have it reduce such respectively when you file your return. (Income verification was put back in 2014 subsidy provisions after being suspended for one year along with the Administration’s one year suspension of the mandate that large employers must purchase health insurance for their employees. And remember–the IRS is in charge of monitoring your enrollment and expenditure.)

Consider opting to get the subsidy along with your tax refund if:

- Your income is very close to 400 percent of FPL.

- Your income varies from year to year so you’re not sure how much you’ll make.

When the subsidy is paid in advance, the amount of the subsidy is based on an estimate of your income for the coming year. If the estimate is wrong, the subsidy amount will be incorrect.

If you earn less than estimated, the advanced subsidy will be lower than it should have been. You’ll get the rest as a tax refund.

If you earn more than estimated, the government will send too much subsidy money to your health insurance company. You’ll have to pay back part or all of the excess subsidy money when you file your taxes. Even worse, if your actual income ended up more than 400 percent of FPL, you’ll have to pay back every penny of the subsidy. This could be thousands of dollars.

If you get your subsidy when you file your income taxes rather than in advance, you’ll get the correct subsidy amount because you’ll know exactly how much you earned that year. You won’t have to pay any of it back.

The Marketplace’s software will (supposedly) calculate your subsidy. Perhaps, as time goes by, it will even do so accurately. But for those of you who scored at least 600 on your high school SAT math test and enjoy such things – here is the exact formula for keeping the government honest:

- Figure out how your income compares to FPL.

- Find your expected contribution rate in the table below.

- Calculate the dollar amount you’re expected to contribute.

- Find your subsidy amount by subtracting your expected contribution from the cost of the benchmark plan.

Here is an example:

Mary is single with an income of $22,800 per year. FPL for 2013 is $11,490 for single people.

- To figure out how Mary’s income compares to FPL, use: income ÷ FPL x 100.

$22,800 ÷ $11,490 x 100 = 198.4.

Mary’s income is 198 percent of FPL. - Using the table below, Mary is expected to contribute 4-6.3 percent of her income. Since she’s almost at the top of her category in the table, she uses the 6.3 percent figure.

- To calculate how much Mary is expected to contribute, use this equation: 6.3 ÷ 100 x income.

6.3 ÷ 100 x $22,800 = $1,436.

Mary is expected to contribute $1,436 per year, or about $120 per month, toward the cost of her health insurance. The premium tax credit subsidy pays the rest of the cost of the benchmark health plan. - The benchmark health plan at Mary’s health insurance exchange costs $3,900 per year or $325 per month. Use this equation to figure out the subsidy amount: cost of the benchmark plan – expected contribution = amount of the subsidy.

$3,900 – $1,436 = $2,464.

Mary’s premium tax credit subsidy will be $2,464 per year or about $205 per month.

If Mary chooses the benchmark plan, or another $325 per month plan, she’ll pay $120 per month for her health insurance. If she chooses a plan costing $425 per month, she’ll pay $220 monthly for her health insurance. If she chooses a plan costing $225 per month, she’ll only pay $20 per month for her health insurance.

FEDERAL POVERTY LIMIT BASED ON NUMBER OF FAMILY IN HOUSEHOLD:

(Click on image to enlarge.)

Table of Your Expected Contribution Percentage:

|

If your income is |

Your expected contribution will be |

|

100%-133% of FPL |

2% of your income |

|

133%-150% of FPL |

3%-4% of your income |

|

150%-200% of FPL |

4%-6.3% of your income |

|

200%-250% of FPL |

6.3%-8.05% of your income |

|

250%-300% of FPL |

8.05%-9.5% of your income |

|

300%-400% of FPL |

9.5% of your income

|

I hope your weather is not as beautiful as it is here in my part of Texas on this Sunday afternoon. If so, you are probably regretting you took the time to get this far into this hopefully informative piece. If it is – do not blame me and certainly–do not shoot the messenger.

As for me, I’m getting out on my motor bike and will take my mind off this monumental cross I bear being . . .

Yours in disclosure,

Admin. – Kenton Henry

http://allplanhealthinsurance.com

****************************************************************

Feature Articles:

FORBES

10/14/2013 @ 11:39AM |1,067,949 views

Obamacare’s Website Is Crashing Because It Doesn’t Want You To Know How Costly Its Plans Are

Avik Roy, Contributor

The Healthcare.gov website requires that individuals looking for coverage enter personal information before comparing plans. IT experts believe that this requirement is causing the website to crash.

A growing consensus of IT experts, outside and inside the government, have figured out a principal reason why the website for Obamacare’s federally-sponsored insurance exchange is crashing. Healthcare.gov forces you to create an account and enter detailed personal information before you can start shopping. This, in turn, creates a massive traffic bottleneck, as the government verifies your information and decides whether or not you’re eligible for subsidies. HHS bureaucrats knew this would make the website run more slowly. But they were more afraid that letting people see the underlying cost of Obamacare’s insurance plans would scare people away.

HHS didn’t want users to see Obamacare’s true costs

“Healthcare.gov was initially going to include an option to browse before registering,” report Christopher Weaver and Louise Radnofsky in the Wall Street Journal. “But that tool was delayed, people familiar with the situation said.” Why was it delayed? “An HHS spokeswoman said the agency wanted to ensure that users were aware of their eligibility for subsidies that could help pay for coverage, before they started seeing the prices of policies.” (Emphasis added.)

Move up http://i.forbesimg.com t Move down

How Obamacare’s Exchanges Turned Into A ‘Third World Experience’ Avik Roy Contributor

Double Down: Obamacare Will Increase Avg. Individual-Market Insurance Premiums By 99% For Men, 62% For Women Avik Roy Contributor

CMS on Obamacare’s Health Insurance Exchanges: ‘Let’s Just Make Sure It’s Not a Third-World Experience’ Avik Roy Contributor

Enrollment In Obamacare’s Federal Exchange, So Far, May Only Be In ‘Single Digits’ Avik Roy Contributor

As you know if you’ve been following this space, Obamacare’s bevy of mandates, regulations, taxes, and fees drives up the cost of the insurance plans that are offered under the law’s public exchanges. A Manhattan Institute analysis I helped conduct found that, on average, the cheapest plan offered in a given state, under Obamacare, will be 99 percent more expensive for men, and 62 percent more expensive for women, than the cheapest plan offered under the old system. And those disparities are even wider for healthy people.

That raises an obvious question. If 50 million people are uninsured today, mainly because insurance is too expensive, why is it better to make coverage even costlier?

Political objectives trumped operational objectives

The answer is that Obamacare wasn’t designed to help healthy people with average incomes get health insurance. It was designed to force those people to pay more for coverage, in order to subsidize insurance for people with incomes near the poverty line, and those with chronic or costly medical conditions.

But the laws’ supporters and enforcers don’t want you to know that, because it would violate the President’s incessantly repeated promise that nothing would change for the people that Obamacare doesn’t directly help. If you shop for Obamacare-based coverage without knowing if you qualify for subsidies, you might be discouraged by the law’s steep costs.

So, by analyzing your income first, if you qualify for heavy subsidies, the website can advertise those subsidies to you instead of just hitting you with Obamacare’s steep premiums. For example, the site could advertise plans that cost “$0″ or “$30″ instead of explaining that the plan really costs $200, and that you’re getting a subsidy of $200 or $170. But you’ll have to be at or near the poverty line to gain subsidies of that size; most people will either not qualify for a subsidy, or qualify for a small one that, net-net, doesn’t make up for the law’s cost hikes.

This political objective—masking the true underlying cost of Obamacare’s insurance plans—far outweighed the operational objective of making the federal website work properly. Think about it the other way around. If the “Affordable Care Act” truly did make health insurance more affordable, there would be no need to hide these prices from the public.

Subsidy verification created a traffic bottleneck

Comparable private-sector e-commerce sites, like eHealthInsurance.com, allow you to shop for plans and compare prices simply by entering your age and your ZIP code. After you’ve selected a plan you like, you fill out an on-line application. That substantially winnows down the number of people who rely on the site for network-intensive tasks.

The federal government’s decision to force people to apply before shopping, Weaver and Radnofsky write, “proved crucial because, before users can begin shopping for coverage, they must cross a busy digital junction in which data are swapped among separate computer systems built or run by contractors including CGI Group Inc., the healthcare.gov developer, Quality Software Services Inc., a UnitedHealth Group Inc. unit; and credit-checker Experian PLC. If any part of the web of systems fails to work properly, it could lead to a traffic jam blocking most users from the marketplace.”

Jay Angoff, a former federal official at the agency that oversees the exchange, told the Journal that he was surprised by the decision. “People should be able to get quotes” without entering all of that information upfront.

Weaver and Radnofsky say that the core problem stems from “the slate of registration systems [that] intersect with Oracle Identity Manager, a software component embedded in a government identity-checking system.” The main Healthcare.gov web page collects information using the CGI Group technology. Then that data is transferred to a system built by Quailty Software Services. QSS then sends data to Experian, the credit-history firm. But the key “identity management system” employed by QSS was designed by Oracle, and according to the Journal’s sources, the Oracle software isn’t playing nicely with the other information systems.

Oracle hotly denies these claims. “Our software is the identical product deployed in most of the world’s most complex systems…our software is running properly,” said an Oracle spokeswoman in a statement.

‘It’s awful, just awful’

Robert Pear and colleagues at the New York Times have a piece up today detailing the serious problems with the federal exchange, problems that may get worse, not better. They confirm what we already knew: that the Obama administration refused to delay the implementation of the exchanges, despite the well-known problems, because they were afraid of the political blowback. “Former government officials say the White House, which was calling the shots, feared that any backtracking would further embolden Republican critics who were trying to repeal the health care law.”

As I documented last week, IT and insurance experts have been saying for at least eight months that implementation of the exchanges was going badly, that as early as February officials were warning of a “third world experience.” The Times’ sources are just as blunt. “These are not glitches,” said one insurance executive. “The extent of the problems is pretty enormous. At the end of our [conference calls with the administration], people say, ‘It’s awful, just awful.’”

“We foresee a train wreck,” said another executive in a February interview with the Times. “We don’t have the IT specifications. The level of angst in health plans is growing by leaps and bounds. The political people in the administration do not understand how far behind they are.” Richard Foster, the former chief actuary at the Centers for Medicare and Medicaid Services, said last week that “so much testing of the new system was so far behind schedule, I was not confident it would work well.”

Henry Chao, the deputy chief information officer at CMS who made the “third world experience” comment, was told by his superiors that failure to meet the October 1 launch deadline “was not an option,” according to the Times.

White House knowingly chose to court disaster

Think about it. It’s quite possible that much of this disaster could have been avoided if the Obama administration had been willing to be open with the public about the degree to which Obamacare escalates the cost of health insurance. If they had, then a number of the problems with the exchange’s software architecture would never have arisen. But that would require admitting that the “Affordable Care Act” was not accurately named.

The White House knew that its people on the front lines, people like Henry Chao, were worried that the exchanges would get botched. They saw the Congressional Research Service memorandum detailing that the administration has missed half of the statutory deadlines assigned by the law. But they were more afraid of the P.R. disaster of disclosing Obamacare’s high premiums than they were of the P.R. disaster of crashing websites. What you see is the result.

************************

Tech experts: Health exchange site needs total overhaul

SHARE 7929 CONNECT 866 TWEET 298 COMMENTEMAILMORE

WASHINGTON — The federal health care exchange was built using 10-year-old technology that may require constant fixes and updates for the next six months and the eventual overhaul of the entire system, technology experts told USA TODAY.

The site could be perfect, but if the systems from which it draws data are not up to speed, it doesn’t matter, said John Engates, chief technology officer at Rackspace, a cloud computer service provider.

“It is a core problem in the sense of it’s fundamental to this thing actually working, but it’s not necessarily a problem that the people who wrote HealthCare.gov can get to,” Engates said. “Even if they had a perfect system, it still won’t work.”

Recent changes have made the exchanges easier to use, but they still require clearing the computer’s cache several times, stopping a pop-up blocker, talking to people via Web chat who suggest waiting until the server is not busy, opening links in new windows and clicking on every available possibility on a page in the hopes of not receiving an error message. With those changes, it took one hour to navigate the HealthCare.gov enrollment process Wednesday.

Those steps shouldn’t be necessary, experts said.

AFFORDABLE CARE ACT: What does it mean for you?

“I have never seen a website — in the last five years — require you to delete the cache in an effort to resolve errors,” said Dan Schuyler, a director at Leavitt Partners, a health care group by former Health and Human Services secretary Mike Leavitt. “This is a very early Web 1.0 type of fix.”

“The application could be fundamentally flawed,” said Jeff Kim, president of CDNetworks, a content-delivery network. “They may be using 1990s technology in 2.0 world.”

Outsiders acknowledged they can’t see the whole system, but they said they feared HHS built a system that will need an expensive overhaul that would cause more headaches for people trying to buy insurance.

“I will be the first to tell you that the website launch was rockier than we wanted it to be,” HHS Secretary Kathleen Sebelius said Wednesday at Cincinnati State Technical and Community College, adding that people have until Dec. 15 to enroll to ensure coverage beginning Jan. 1.

HHS officials did not respond to a request about the nature of the problems. However, they reiterated that wait times have been reduced or even eliminated as they continue to work to fix the system. As of Thursday, the site had received 17 million unique visitors.

“We continue to work around the clock to improve the consumer experience on HealthCare.gov,” HHS spokeswoman Joanne Peters said. “We are seeing progress: wait times to begin the online process have been virtually eliminated, and more consumers are creating accounts, completing applications and ultimately enrolling in coverage if they choose to do so at this time. However, we will not stop addressing issues and improving the system until the doors to HealthCare.gov are wide open.”

OBAMACARE: A tough sell for Native Americans

Engates said HHS has been opaque about the problems, and the tech industry doesn’t know the extent of the issues. “There’s no secrets leaking out,” he said. “I’m sure everyone’s looking for something to change the direction of the conversation, but it’s just not there.”

“I think it’s a data problem,” Kim said. “It always comes down to that.”

And if that’s the case, the problems are beyond “rocky,” he said. Instead, it would require a “fundamental re-architecture.” In the meantime, “I think they’re just trying to shore up as quickly as possible. They don’t have time to start from scratch.”

“If I was them, and I’m just conjecturing, I would probably come up with some manual way of saying, ‘Only people with the last name starting with ‘A’ can sign up today,” he said.

But come March 31, when the first enrollment period ends, the “shore up” period may become a “re-architecting” period, Kim said.

On a good note, he said, after looking at available code, the site is “very secure.”

Clearing the cache, which has helped make it easier for some people to enroll, could ultimately strain the system more, Kim said. That’s because a “cookie” is stored on a person’s computer that contains data, such as the person’s name and address, that can then be quickly accessed when that person gets on the website again instead of having to be retrieved from the government’s server.

But as HHS fixes errors, the cookies may not correspond with the updated website, so rather than allowing someone to quickly log in, they instead cause an error message. And every time a person clears his computer’s cache, the government’s website has to work that much harder to grab more data.

Requiring people who may not be Web savvy to use the site in any way other than a step-by-step easy process defeats the point of the whole system, Schuyler said. That includes laws mandating that insurers provide clear explanations about policies to people may make sound decisions and understand what they’re buying.

“Most consumers will have no idea what ‘clearing the cache’ is and this will just cause more confusion and frustration,” he said.

So far, the site’s problems have not driven away potential customers, according to a poll conducted by uSamp — United Sample Inc. The survey found that among the 832 people who attempted to log in, 38% received an error message, 50% were asked to try again later, 25% were unable to create an account, 31% were told the system was down, and 19% had no problems. About 83% said they would try again later, while 15% said they would wait until they heard the website was working well. About 70% of those who said they had no issues said they still waited to enroll because they want to think about their options.

Engates said he believes most of the problems are caused by systems integration with other sites, such as the IRS. And that could be causing some of the problems people see as they make it past the initial application process. It’s a series of questions meant to verify a person’s identity and income. But after that questionnaire, visitors often encounter a series of error messages, or the page a person tries to click to doesn’t come up. The data requests to other sites could be causing those problems, Engates said, which would mean the problem isn’t with the HHS site itself.

“Maybe the site is submitting a request for more data, and that puts you in that trap again,” he said. “It’s a giant integration problem that they have to solve.”

And as they try to fix those problems, there’s another issue lurking in the background: Some HHS personnel were named essential, and not subject to furloughs because of the government shutdown. But that didn’t apply to the other organizations they were working with, Engates said. So as HHS techs work around the clock to fix the problems, IRS techs may be prohibited from working at all.

In the meantime, HHS personnel can’t say anything about the situation, it can be played politically as “bad,” he said. If they say it will take two weeks to fix, they will be criticized because it’s taking too long. But he expects that it’s a problem that will be resolved soon, especially as the volume of visitors goes down.

“If you can get the system below some sort of threshold, it will perform as it’s supposed to,” Engates said. “It won’t get any worse. It’s going to get better little by little by little.”