Just Practical Information On What is Coming with Your Health Insurance Between Now and January 1!

08.12.2013

This is not an editorial. Today’s post is simply non-political, practical information regarding coming changes in health insurance between now and 2016 and beyond. The Patient Protection and Affordable Care Act (PPACA) is law and is on schedule to be fully implemented (for all but groups of 50+) January 1, 2014. For this reason it is my responsibility to inform my clients – and followers of this blog – of what they can expect in the coming months. Specifically, their insurance options and the mechanics involved in transitioning to health plans that provide minimum “essential benefits” that are in compliance with the PPACA. In this post, I will be addressing individuals and families which includes the self-employed and those who have a personal policy because their employer does not provide coverage. All others, including those covered by group plans for less than 50 employees will be addressed in subsequent posts.

First – those of you who currently have a personal or family policy will be allowed to keep your policy until your policy anniversary in 2014. You should check your anniversary date or–if you are my client–call me. Many companies have changed your anniversary date to December 1. This allows you to keep your current plan until December 1, 2014. After that, you must convert to a health care “compliant” plan which will be described below. I can simplify and assist you in this process when the time comes.

If you do not currently have health insurance you must purchase a health policy to be effective January 1 or pay a penalty on your tax return for 2014 and beyond. Another reason you may want to purchase a plan is if you have previously been unable to acquire a policy which covers your pre-existing health condition(s). Your new compliant plan must cover them and health issues will not factor into your cost.

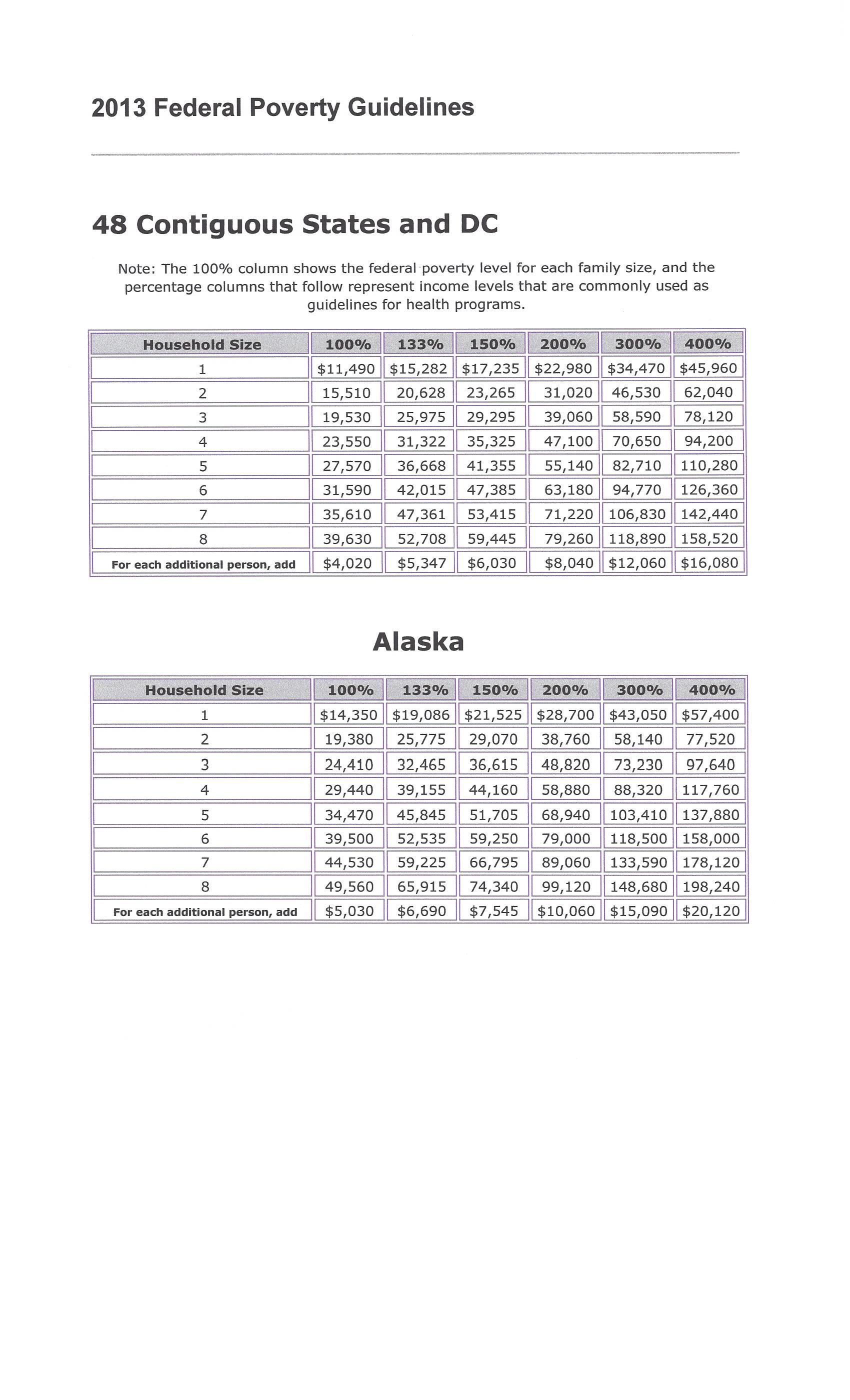

When October 1 arrives (the earliest date you may apply for compliant coverage) I will provide you a link where you will enter your estimated income for 2014. It will instantly tell you whether you qualify for a subsidy. If you do – you are going to want to choose from and apply for plan options in your state health insurance exchange. If your state has not established a state exchange (as is the case in Texas) – you will select from plans in the Federal Health Insurance Exchange. If you do not qualify for a subsidy (which is the case if your income is 400% or greater than the Federal Poverty Level*) – you are probably going to choose a policy offered outside an exchange and direct from an insurance company. The reason being, it is anticipated these plans will offer the same benefits at a lower cost. I can assist you with this option as well.

Below, I will offer further and detailed information on exchanges, plan options and more. Please do not hesitate to call me for clarification or to discuss this information.

Admin. – Kenton Henry

*

http://allplanhealthinsurance.com

*************************************

STEP 1:

Note these key dates and deadlines in your calendar:

If your employer offers health insurance, get key dates from your HR department. These are key dates if you’re planning to buy health care through your state’s Marketplace, which is available through a web site, a call, or an in-person visit.

• Oct. 1, 2013: First day you can enroll in a health plan on your state’s Marketplace

• Dec. 31, 2013: Last day you can enroll in a health plan and have your coverage start Jan. 1, 2014

• Jan. 1, 2014: First day you have insurance coverage if you buy a plan in the Marketplace — if, of course, you buy before this date

• March 31, 2014: The last date you can enroll in a plan on your state’s Marketplace to be covered for part of 2014

*************************************

Requirements:

* Be a citizen or legal resident.

• Buy your coverage through your state’s or Federal new health insurance Marketplace, also called an “Exchange”.

• Make about $11,490 to $45,960 a year if you are single – or $23,550 to $94,200 a year if you are in a family of four.

If you make less than the lowest amount, you may be eligible for Medicaid. Medicaid will cost you less than you’d save with a tax credit.

Unfortunately, if your state is not expanding Medicaid based on the guidelines in the Affordable Care Act, you may not be able to enroll in Medicaid or be able to get a tax credit. It’s possible that if you make less than $11,490 in 2013, which is the poverty level, you may not qualify for Medicaid if you live in a state that isn’t expanding Medicaid.

In general, you’re not eligible for the tax credits if you could get coverage through a workplace. However, the coverage offered by your employer must be considered affordable. If your company offers a plan that costs more than 9.5% of your income, or that does not cover at least 60% of the cost of covered benefits, you can look for a more affordable plan through your state’s Marketplace and may receive tax credits to lower your costs.

********************************

Insurance Exchanges

State Didn’t Set Up a Marketplace? Relax

You may have heard that not all states will have their own health insurance Marketplace, also called an Exchange. If your state doesn’t set up a Marketplace, what does that mean for you?

Rest assured that no matter which state you live in, you can buy insurance through a Marketplace starting October 2013.

The way you use the Marketplace will be similar in every state. You’ll access a web site, or call, or see someone in person. And you’ll have tools to compare health plans.

But Marketplaces won’t all be the same in every state. There are three ways your state’s Marketplace can be managed — and this affects your choice of health plans and coverage.

1) State-run Marketplaces

Seventeen states are creating their own Marketplaces. These states will have a lot of local control.

Each state will decide which insurance companies can sell policies on its Marketplace.

States also choose the core benefits each plan has to offer. They can set extra requirements for health plans, like benefits that are more generous or more affordable limits on your out-of-pocket costs.

The state is also in charge of getting people to use the Marketplace.

*Indiana and Ohio will have their own State Exchange. Residents of these states should call Kenton Henry @ 800.856.6556

2) Partnerships Between a State and the Government

A few states are teaming up with the federal government to develop Marketplaces.

The federal government:

• Sets up the Marketplace web site and in-person sites

• Decides which health plans will be sold in the partner state

• Sets the benefit levels

• Runs the Marketplace

The states:

• Monitor health plans

• Help people find the best insurance for their needs *(Call Kenton Henry @ 800.856.6556)

• Handle complaints

Federal-run Marketplaces

Some states decided not to set up their own Marketplaces. In those states, the federal government will step in to run the marketplaces directly. It will make all the decisions: how the Marketplace will work, what plans are sold, and how to promote the Marketplace. Each state is considered separately and has its own Marketplace web site. (Texas residents call Kenton Henry @ 800.856.6556)

**********************************************

Your Insurance Choices in a Marketplace: FAQ

A health insuranceMarketplace, also known as an Exchange, is a one-stop shop for affordable insurance in your state. Your state’s Marketplace has tools to make it easy for you to compare your choices and pick the best for your needs.

On a state Marketplace site, health plans are grouped by levels of coverage — how much the plan will pay for your health care and what services are covered.

Each level is named after a type of metal:

• Bronze

• Silver

• Gold

• Platinum

Bronze plans offer the least coverage and platinum plans offer the most.

How do the bronze, silver, gold, and platinum levels differ?

The metal plans vary by the percentage of costs you have to pay on average toward the health care you receive.

Here are the percentages of health care costs you pay for each type of plan:

• Bronze plan: 40%

• Silver plan: 30%

• Gold plan: 20%

• Platinum plan: 10% of your health care costs.

The way you pay your portion of these costs is in deductibles and copayments or co-insurance.

In general, the more you are willing and able to pay each time for health care service or a prescription, the lower your premium. A premium is your monthly payment to have insurance.

As an example, when you compare the bronze and platinum plans:

With a bronze plan: You pay the most each time you see your doctor or get a medicine. This is also called having higher “out-of-pocket” costs. But in a bronze plan you pay the least premium each month.

With a platinum plan: You pay the least each time you see your doctor or get a medicine. But in a platinum plan you pay the highest premium each month.

How does coverage from a metal plan compare to my current insurance?

The bronze through platinum coverage levels are new. So you probably don’t know how the benefits of the plan you use today compare to them. The coverage level you have now depends on whether you bought your plan:

• From an employer: Your coverage level is likely between a gold and platinum level.

• On your own: Your coverage level is likely between a bronze and silver level.

Having a sense of how the insurance you’re used to compares with the new plans will help you decide on a plan. You should compare the out-of pocket costs you are currently paying, the services provided (including prescription drugs), and anticipated changes in your health.

If you shop for insurance on your state’s Marketplace, you’ll see the health plans organized in this way:

• 1st by metal level: Bronze, silver, gold, or platinum

• 2nd by brand, such as Blue Cross, Cigna, Humana, Kaiser, United, and others

• 3rd by type of health plan, such as HMO, PPO, POS, or high-deductible plans with a health savings account.

The type of health plan affects how much choice you have in providers, the amount of paperwork you have, and your out-of-pocket costs.

**************************************

Tax Penalty At-a-Glance: Who Will Pay The Penalty & How Much Is It?

By law, you need to have health insurance by 2014. If you already get insurance through your employer or your partner’s employer, you’re all set. But what happens if you don’t follow this requirement from the Affordable Care Act?

If you can afford health insurance and don’t buy it, you’ll pay a fine when you file your 2013 income taxes in April 2014.

For the first year of the new law, 2014, the fine for not having insurance is the lowest it will be. After that, it goes up steeply in 2015 and again in 2016.

In 2014: There are two ways the government calculates what you owe. You have to pay whichever amount is higher.

• One way is to charge you $95 for each adult and $47.50 for each child, but not more than $285 total per family.

• The other way is to fine you 1% of your family income. If your family makes $50,000 a year, the fine will be $500.

In 2015: There will still be two ways to calculate what you owe. You have to pay whichever amount is higher.

• One way is to charge you $325 for each adult and $162.50 for each child, but no more than $975 total per family.

• The other way is 2% of your family income. If your family makes $50,000 a year, the fine will be $1,000.

In 2016 and beyond: There will still be two ways to calculate what you owe. You have to pay whichever amount is higher.

• One way is to charge you $695 for each adult and $347.50 for each child, but no more than $2,085 per family.

• The other calculation is 2.5% of your family income. If your family makes $50,000 a year, the fine will be $1,250.

http://allplanhealthinsurance.com