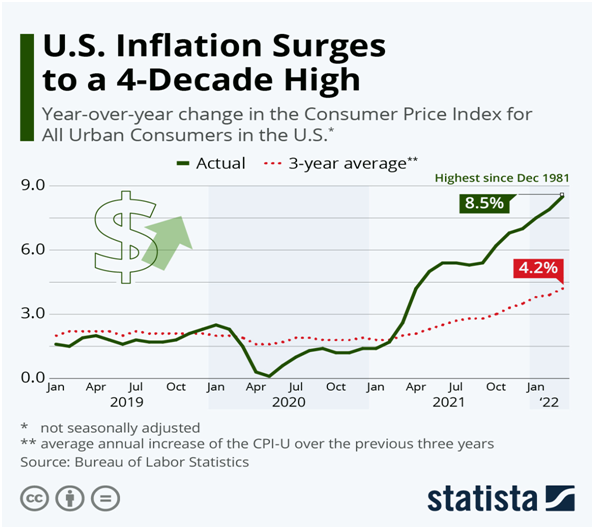

While inflation has costs for necessities, such as gas and food items, skyrocketing to an average of 8.5% in March and much higher for the aforementioned items – Social Security saw fit to only increase the Income Benefit to SSI recipients to 5.9%. Seniors, many of whom are subsisting on fixed incomes, might be able to cut their need for gasoline, but I do not know any who can get by without food, shelter, and electricity. Many are struggling to pay their bills already, and inflation shows little sign of abating.

This was only until 09/2021, at which time, apparently only apples inflated lower than our current rate of inflation.

But how about the argument that all this inflation is due to Putin and the war in Ukraine? Russia launched a full-scale assault on Ukraine February 22. One month after the end of the timeline in the chart below.

When was our current president inaugurated? . . . Answer: January 20, 2021. Take a look at the green line above charting the Consumer Price Index on that date. (I will leave it at that.)

To add insult to injury, the Centers for Medicare and Medicaid Services (CMS) increased Part B (outpatient care) premiums by 15% to a base premium -for those with an annual income of less than or equal to $91,000 – to $170.10 per month. Thank you very much!

However, as described in Feature Article 1 below, due in part to a 50% cut in the cost of a $56,000 Part D covered drug, CMS is considering reducing that Part B Premium. My experience is that the government seldom gives back what they are already receiving . . . but one can only hope.

For those involved in Marketplace medical coverage – health insurance for individuals and families under the age of 65 – the opposite action on the part of the Department of Health and Human Services may occur. Specifically, the extended enhanced premium tax credits made available by the American Rescue Plan, which enabled an additional 3 million Americans to receive a subsidy lowering their net monthly premium to as low as $0, are set to expire at the end of the year. As described in Feature Article 3 below, it is estimated 4.9 million more people will go uninsured if enhanced benefits are not extended. Never mind it is estimated the extension of such would increase the federal deficit by $305 billion dollars. Of course, the Treasury can simply print more money, further increasing inflation and diminishing the buying power of one’s paycheck or Social Security Income.

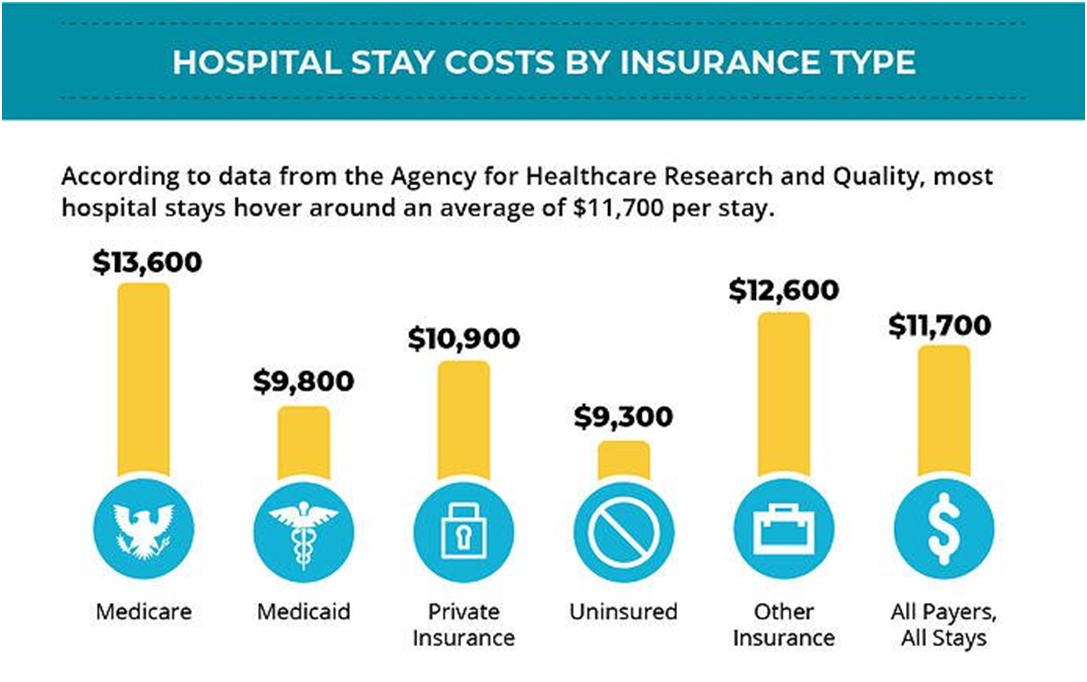

Lastly, medical expenses are no exception to inflation. If you wonder why health insurance premiums or out-of-pocket costs for healthcare are being affected, refer to article 3 below. They start high and increase as one goes from a doctor’s office to an Urgent Care facility to a hospital emergency room. Avoid the latter unless it is a true emergency because it will cost an average of $444 for low to moderate severity treatment. Heaven, forbid you have an overnight stay in a hospital without medical insurance because the average cost is $11,700. As cited in the chart below, it only goes up depending on the type of insurance you have.

Should your stay extend to three days, expect to cost to be an average of $30,000. And what if you don’t have health insurance? Here are the average costs of various treatments.

Take a look at what you might pay for each hospital bill without insurance:

*(Data from the Agency for Healthcare Research and Quality)

While I cannot guarantee we have seen the worst of inflation – let alone that the government is going to provide us any meaningful relief in the immediate future. But I am here to assist you in acquiring medical coverage, which gives you access to the care and treatment you need to regain or preserve your health without being financially ruined. I will do my best to help you maintain access to as many of your preferred medical doctors and hospitals as the present market allows. I do not charge a fee for my services. There is no additional cost for the insights and value of my 36 years of experience in the health and Medicare-related insurance market. Neither is there any additional cost in acquiring an insurance product through me than if you walked through the door of your preferred insurance company and purchased their product directly from them. There is no obligation to take my learned advice.

Please give me a call and let’s discuss your situation before the very busy “Open Enrollment” Periods are upon us and everyone is scrambling to mitigate what are almost certain to be the increasing costs of health care

AHIP applauded CMS for covering the drug and “related services such as PET scans if required b the trial protocol.”

Other stakeholders said that now the coverage decision has been finalized it is time for CMS to take action on lowering Part B premiums.

CMS has yet to announce any final decision on Part B premiums, which is increased by 15% for 2022. A key reason was the $56,000 price tag for Aduhelm.

However, Department of Health and Human Services Secretary Xavier Becerra announced in January that the agency was rethinking the 15% hike after Biogen halved the price of Aduhelm in December.

Becerra told reporters on Tuesday before the coverage decision that he was waiting to see what “CMS gives back to us in terms of their assessment and then once we get that information we will see where we go.”

CMS told Fierce Healthcare on Friday that it has yet to decide on a redetermination for the premium.

But advocates are hoping the agency moves faster on scaling back the premium hike.

“Medicare beneficiaries struggling to pay their bills need relief from this year’s premium increase as soon as possible,” said Max Richtman, president and CEO of the National Committee to Preserve Social Security and Medicare.

Pharma and Alzheimer’s disease patient advocacy groups slammed the decision, however, noting that it will hamper access to the drug.

“CMS has further complicated matters by taking the unprecedented step of applying different standards for coverage of medicines depending on the FDA approval pathway taken, undermining the scientific assessment by experts at FDA,” said Nicole Longo, spokeswoman for the Pharmaceutical Research and Manufacturers of America, in a statement.

End to ACA tax credits could leave 3 million uninsured

But extending the enhanced credits would increase the federal deficit by $305 billion over 10 years.

By Alan Goforth | April 08, 2022 at 09:32 AM

Congress would need to act by midsummer to give marketplaces, insurers and outreach programs time to prepare for the 2023 open enrollment period.

More than three million people could lose insurance coverage if enhanced premium tax credits included in the American Rescue Plan expire at the end of this year, according to a new report from the Urban Institute. The American Rescue Plan Act of 2021 increased credits for Marketplace insurance coverage and extended eligibility to more individuals.

“If Congress does not extend these benefits, marketplace enrollment will most likely fall and the number of people uninsured will increase,” said Jessica Banthin, senior fellow at the organization. “Our findings show that 4.9 million fewer people will be enrolled in subsidized Marketplace coverage in 2023 if the enhanced credits aren’t extended. This comes at a pivotal time when millions of people will be losing Medicaid as the public health emergency expires.

Average charges for 8 common procedures across ER, retail and urgent care settings

Alia Paavola – Wednesday, March 30th, 2022

In 2020, the median charge for a 30- to 44-minute new patient office visit ranged from $164 in a retail clinic to $234 in an urgent care center, according to a March report from Fair Health.

For the report, Fair Health, an independent nonprofit focused on enhancing transparency of healthcare costs and health insurance information, analyzed billions of private healthcare claims records from its database.

Below is the average charge for eight common procedures, as identified by CPT code, performed in retail, urgent care and emergency room settings:

TIME IS RUNNING OUT FOR A JANUARY 1 EFFECTIVE DATE!

Op-ed by D. Kenton Henry Editor, Broker 26 November 2021

In September, I learned Aetna and Unitedhealthcare would be reentering the Texas ACA Underage 65 health insurance market for the first time since 2015. Since then, BlueCross BlueShield has been the only “household name,” a large, financially sound insurance company in the southeast Texas market. This was most welcome news, and I was hopeful these additional peer companies would allow my clients and fellow Texans access to more doctors and hospitals. Finding my client’s preferred doctors and hospitals in a plan network has been my client’s and my greatest challenge since the departure of all PPO network options six years ago. Alas, the hoped-for provider expansion in 2022, at this point, has failed to materialize. From 2015 into 2021, the St. Lukes Hospital system has been the only major hospital system participating in most insurance companies’ HMO networks. Such will remain the case for 2022.

Additionally, the entry of Bright Insurance Company (for the first time) doesn’t even appear to do that. They will limit their policyholder’s access to hospitals will be limited to smaller HCA local community hospitals. At least for the time being.

Doctors have practicing privileges at one or more hospitals. Of course, it follows that when an insurance company has fewer hospitals in their network, they will have fewer participating doctors. And so it seems. Only one health insurance company in the southeast Texas ACA health insurance market allows its clients access to the three major hospital systems in the area. Those hospitals are St. Luke’s, Memorial Hermann, and Houston Methodist. And then, only if you acquire their more expensive Silver or Gold plans.

However, there is a bit of good news for all Americans in the “Individual and Family” health insurance market. The federal government’s American Rescue Plan has increased the amount of Advance Premium Tax Credit (subsidy) and Cost Sharing Reduction (reduction of deductibles, copays, and coinsurance) available to a household. It also expanded the eligibility for these subsidies. As the feature article below explains, this will qualify more people for both types of savings.

Furthermore, unemployment effects and increases your potential premium tax credit! The American Rescue Plan exempts up to $10,200 in UI benefits from federal income tax. People who receive UI benefits in 2020 will be able to reduce their adjusted gross income by up to that amount, and so reduce their federal income tax liability.

Please get in touch with me to learn the details on the aforementioned company providing the greatest access to providers and how the expanded subsidies and Cost-Sharing Reductions may improve your health insurance situation.

If you choose to be proactive and would like to do some reconnaissance before calling me for assistance and details, you may click on my quoting link immediately following. When the page opens, ignore the login button. You need not log in. Enter your information. I.e., birth date, zip code, etc. On the next page, click on the top box “SELECT ALL” to clear the selections. Then select “MEDICAL” only, to get started. Otherwise, you will be overwhelmed with options and information. You can always return for dental, etc.)

Click “YES” if you would like to estimate whether you qualify for a subsidy. If so, enter your estimated annual income in 2022 and click “CALCULATE”. It will estimate your subsidy. The estimates are usually accurate to within $3.00. From there, click “NEXT”. You will then see all your plan options and be able to LOOKUP PROVIDERS and see plan details. Or simply call me to do all this for you!

CLICK HERE TO SEE ALL YOUR ACA HEALTH INSURANCE OPTIONS (IF NECESSARY, COPY THE LINK IN YOUR BROWSER AND HIT ENTER):

As the cost for everything, including medical treatment, is going up, so too are Medicare’s premiums and deductibles. As our second feature article below illustrates, the Medicare Part B (outpatient) basic premium is going from $148.50 to $170.10 and it’s calendar year deductible is going from $203.00 to $233.00! You can do the math, but, needless to say, so much for 5% inflation rate projected by the current administration which also does not appear to apply to our cost for gasoline, meat, and energy and food, in general! You’ve already spent the increase in your Social Security Benefit!

The details of how your Medicare Part B basic premium will may titrate upward relative to your income are clearly outlined in Feature Article 2, just published by the Centers For Medicare and Medicaid Services.

Lastly, if you are making the decision whether to go with a Medicare Advantage Prescription Drug Health Plan vs. a Medicare Supplement policy coupled with a Part D Prescription Drug Plan – please read Feature Article 3 (say it ain’t so, Joe!) below, and carefully weigh your decision.

Again, please contact me for guidance in how to minimize the impact of these changes and maximize your both your access to providers and quality health care. My 35 years specializing in the health and Medicare related insurance industry have provided me insights beyond that of the average agent/broker/generalist; and my clients access to a far greater number of products and solutions.

Advanced Premium Tax Credits(APTC):Lowers the cost of premiums and can be used on any Marketplace plan except for catastrophic plans.

Cost Sharing Reductions(CSR):Lowers the cost of deductibles and can only be applied to Marketplace Silver plans.

This year, many people will qualify for both types of savings!

Why are subsidies more generous this year:

The American Rescue Plan Act increased the amount of APTC and CSR available to a household, and it also expanded the eligibility for these subsidies.

Silver plans vs. other metal levels:

All Marketplace health insurance plans are broken into five types: Platinum, Gold, Silver, Bronze and Catastrophic. You can expect the same level of care fromall metal levels. The difference is how your healthcare costs will be split between you and the insurance company. Metal levels Premium Platinum Highest Gold Silver Bronze Catastrophic Deductible Higher Middle Lower Lowest Lower Middle Higher Highest. If you are eligible for a CSR, you must choose a Silver plan!

On November 12, 2021, the Centers for Medicare & Medicaid Services (CMS) released the 2022 premiums, deductibles, and coinsurance amounts for the Medicare Part A and Part B programs, and the 2022 Medicare Part D income-related monthly adjustment amounts.

Medicare Part B Premium and Deductible

Medicare Part B covers physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A.

Each year the Medicare Part B premium, deductible, and coinsurance rates are determined according to the Social Security Act. The standard monthly premium for Medicare Part B enrollees will be $170.10 for 2022, an increase of $21.60 from $148.50 in 2021. The annual deductible for all Medicare Part B beneficiaries is $233 in 2022, an increase of $30 from the annual deductible of $203 in 2021.

The increases in the 2022 Medicare Part B premium and deductible are due to:

Rising prices and utilization across the health care system that drive higher premiums year-over-year alongside anticipated increases in the intensity of care provided.

Congressional action to significantly lower the increase in the 2021 Medicare Part B premium, which resulted in the $3.00 per beneficiary per month increase in the Medicare Part B premium (that would have ended in 2021) being continued through 2025.

Additional contingency reserves due to the uncertainty regarding the potential use of the Alzheimer’s drug, Aduhelm™, by people with Medicare. In July 2021, CMS began a National Coverage Determination analysis process to determine whether and how Medicare will cover Aduhelm™ and similar drugs used to treat Alzheimer’s disease. As that process is still underway, there is uncertainty regarding the coverage and use of such drugs by Medicare beneficiaries in 2022. While the outcome of the coverage determination is unknown, our projection in no way implies what the coverage determination will be, however, we must plan for the possibility of coverage for this high cost Alzheimer’s drug which could, if covered, result in significantly higher expenditures for the Medicare program.

Medicare Open Enrollment and Medicare Savings Programs

Medicare Open Enrollment for 2022 began on October 15, 2021, and ends on December 7, 2021. During this time, people eligible for Medicare can compare 2022 coverage options between Original Medicare, and Medicare Advantage, and Part D prescription drug plans. In addition to the recently released premiums and cost sharing information for 2022 Medicare Advantage and Part D plans, the Fee-for-Service Medicare premiums and cost sharing information released today will enable people with Medicare to understand all their Medicare coverage options for the year ahead. Medicare health and drug plan costs and covered benefits can change from year to year, so people with Medicare should look at their coverage choices annually and decide on the options that best meet their health needs.

To help with their Medicare costs, low-income seniors and adults with disabilities may qualify to receive financial assistance from the Medicare Savings Programs (MSPs). The MSPs help millions of Americans access high-quality health care at a reduced cost, yet only about half of eligible people are enrolled. The MSPs help pay Medicare premiums and may also pay Medicare deductibles, coinsurance, and copayments for those who meet the conditions of eligibility. Enrolling in an MSP offers relief from these Medicare costs, allowing people to spend that money on other vital needs, including food, housing, or transportation. People with Medicare interested in learning more can visit: https://www.medicare.gov/your-medicare-costs/get-help-paying-costs/medicare-savings-programs.

Medicare Part B Income-Related Monthly Adjustment Amounts

Since 2007, a beneficiary’s Part B monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 7 percent of people with Medicare Part B. The 2022 Part B total premiums for high-income beneficiaries are shown in the following table:

Beneficiaries who file individual tax returns with modified adjusted gross income:

Beneficiaries who file joint tax returns with modified adjusted gross income:

Income-related monthly adjustment amount

Total monthly premium amount

Less than or equal to $91,000

Less than or equal to $182,000

$0.00

$170.10

Greater than $91,000 and less than or equal to $114,000

Greater than $182,000 and less than or equal to $228,000

68.00

238.10

Greater than $114,000 and less than or equal to $142,000

Greater than $228,000 and less than or equal to $284,000

170.10

340.20

Greater than $142,000 and less than or equal to $170,000

Greater than $284,000 and less than or equal to $340,000

272.20

442.30

Greater than $170,000 and less than $500,000

Greater than $340,000 and less than $750,000

374.20

544.30

Greater than or equal to $500,000

Greater than or equal to $750,000

408.20

578.30

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

Beneficiaries who are married and lived with their spouses at any time during the year, but who file separate tax returns from their spouses, with modified adjusted gross income:

Income-related monthly adjustment amount

Total monthly premium amount

Less than or equal to $91,000

$0.00

$170.10

Greater than $91,000 and less than $409,000

374.20

544.30

Greater than or equal to $409,000

408.20

578.30

Medicare Part A Premium and Deductible

Medicare Part A covers inpatient hospital, skilled nursing facility, hospice, inpatient rehabilitation, and some home health care services. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

The Medicare Part A inpatient hospital deductible that beneficiaries pay if admitted to the hospital will be $1,556 in 2022, an increase of $72 from $1,484 in 2021. The Part A inpatient hospital deductible covers beneficiaries’ share of costs for the first 60 days of Medicare-covered inpatient hospital care in a benefit period. In 2022, beneficiaries must pay a coinsurance amount of $389 per day for the 61st through 90th day of a hospitalization ($371 in 2021) in a benefit period and $778 per day for lifetime reserve days ($742 in 2021). For beneficiaries in skilled nursing facilities, the daily coinsurance for days 21 through 100 of extended care services in a benefit period will be $194.50 in 2022 ($185.50 in 2021).

Part A Deductible and Coinsurance Amounts for Calendar Years 2021 and 2022 by Type of Cost Sharing

2021

2022

Inpatient hospital deductible

$1,484

$1,556

Daily coinsurance for 61st-90th Day

$371

$389

Daily coinsurance for lifetime reserve days

$742

$778

Skilled Nursing Facility coinsurance

$185.50

$194.50

Enrollees age 65 and over who have fewer than 40 quarters of coverage and certain persons with disabilities pay a monthly premium in order to voluntarily enroll in Medicare Part A. Individuals who had at least 30 quarters of coverage or were married to someone with at least 30 quarters of coverage may buy into Part A at a reduced monthly premium rate, which will be $274 in 2022, a $15 increase from 2021. Certain uninsured aged individuals who have less than 30 quarters of coverage and certain individuals with disabilities who have exhausted other entitlement will pay the full premium, which will be $499 a month in 2022, a $28 increase from 2021.

Medicare Part D Income-Related Monthly Adjustment Amounts

Since 2011, a beneficiary’s Part D monthly premium is based on his or her income. These income-related monthly adjustment amounts affect roughly 8 percent of people with Medicare Part D. These individuals will pay the income-related monthly adjustment amount in addition to their Part D premium. Part D premiums vary from plan to plan and roughly two-thirds are paid directly to the plan, with the remaining deducted from Social Security benefit checks. The Part D income-related monthly adjustment amounts are all deducted from Social Security benefit checks. The 2022 Part D income-related monthly adjustment amounts for high-income beneficiaries are shown in the following table:

Beneficiaries who file individual tax returns with modified adjusted gross income:

Beneficiaries who file joint tax returns with modified adjusted gross income:

Income-related monthly adjustment amount

Less than or equal to $91,000

Less than or equal to $182,000

$0.00

Greater than $91,000 and less than or equal to $114,000

Greater than $182,000 and less than or equal to $228,000

12.40

Greater than $114,000 and less than or equal to $142,000

Greater than $228,000 and less than or equal to $284,000

32.10

Greater than $142,000 and less than or equal to $170,000

Greater than $284,000 and less than or equal to $340,000

51.70

Greater than $170,000 and less than $500,000

Greater than $340,000 and less than $750,000

71.30

Greater than or equal to $500,000

Greater than or equal to $750,000

77.90

Premiums for high-income beneficiaries who are married and lived with their spouse at any time during the taxable year, but file a separate return, are as follows:

Beneficiaries who are married and lived with their spouses at any time during the year, but file separate tax returns from their spouses, with modified adjusted gross income:

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

He’s one of a slew of pitchmen and women selling Medicare Advantage plans to the more than 54 million Americans 65 or over eligible for Medicare. That includes more than 100,000 of us in Orange, Ulster and Sullivan counties.

Joe Namath may have delivered the New York Jets’ last Super Bowl championship, but the old quarterback is throwing a bunch of bull on his TV commercials for private Medicare plans.

Those pitches, which also flood our mailboxes during this enrollment period that ends Dec. 7, complicate what can be a mind-boggling array of insurance choices.

First, some basic facts:

Medicare Advantage is the all-in-one alternative to original Medicare health insurance. Original Medicare includes coverage for hospitalization (Part A), medical visits and procedures (Part B) and, at additional cost, prescription drugs (Part D). Before you enroll in Advantage plans, you must have original Medicare, and you still must pay the Part B premium of $148.50 (in 2021). While Medicare Advantage plans include medical, hospital and drug coverage, they can also feature extra benefits not offered by traditional Medicare, such as dental, hearing and vision coverage with no additional premium.

Especially in those pitches from celebrities like Namath, William Shatner and Jimmie Walker, they can also promise everything from free meal delivery to money deposited in your Social Security account.

But …

“Buyer beware,” says Erinn Braun, Orange County Office for the Aging’s Health Insurance Counseling and Assistance Program coordinator. She provided much information for this column.

Pitches like Namath’s can be misleading or downright deceptive, starting with the red, white and blue colors that insinuate the ads are from the government, as do the state logos on some mailers. While the plans themselves are perfectly legal and may be great for many of the 27 million Americans enrolled in them, they often don’t deliver everything those pitches seem to promise. Plus, those pitches don’t come close to telling the full story of the benefits of those plans – many of which aren’t even offered in your area.

For instance:

Unlike original Medicare, which is accepted by virtually all doctors and hospitals, Medicare Advantage plans include a network of doctors and hospitals you must visit to be insured. So if you hear about a great gastroenterologist in New York City and she isn’t in your Advantage plan’s network, your insurance may not cover your visit. Plus, unlike original Medicare, you may need prior approval for coverage of a medical procedure or equipment such as insulin pumps.

And while the dental and vision coverage of Medicare Advantage plans sounds great, some plans in your area may only include routine visits, not more expensive items like dental implants and eyeglasses. Plus, the average yearly coverage limit of Advantage dental plans ranges from about $1,000 to $1,300, according to the Kaiser Family Foundation. The dentists and eye doctors you visit must also be in the plan’s networks – meaning your eye doctor or dentist may not accept your plan.

Steve Israel

As for those meals and money Joe Willie is pitching?

Again, buyer beware.

A few Advantage plans may offer meal delivery for the qualified but only one or two plans in your county may offer those benefits. And your doctors or hospital may not accept those plans. Same thing goes for that money Namath says could go into your Social Security account. Not only does that money go toward the required payment for Part B of original Medicare, very few plans – if any – in your area may feature that benefit, and those plans may not include your doctors.

Finally, when you call the number provided by Namath and other pitch folks, you’ll reach a salesperson who’s in business to … you guessed it … sell you a Medicare Advantage plan.

For help selecting the right Medicare plan for you, contact your county’s Office of the Aging. Orange: 845-615-3710, Sullivan: 845-807-0241, Ulster: 845-340-3456. A trusted health insurance agent can also help. Medicare.gov and 1-800-Medicare provide a wealth of information.

(AETNA AND UNITEDHEALTHCARE RE-ENTER THE ACA INDIVIDUAL AND FAMILY HEALTH INSURANCE MARKET)

By Editor, Agent, Broker

D. Kenton Henry

It is that time of year and, once more, we find ourselves on the cusp of the “Annual Election Period” for Medicare Advantage and Part D Prescription Drug Plans. This is the period when any Medicare recipient may enroll or change their Advantage and / or drug plans for a January 1 effective date. The period runs from October 15th through December 7th.

As if this was not a busy enough time for Medicare insurance product brokers, many of us (like myself) must do “double duty”, during the holidays. This is because the “Open Enrollment Period” for those “Under the Age Of 65“, in need of Individual and Family health insurance, begins November 1 and runs through January 15th. This a one month extension from previous years. However, those wishing to have new coverage effective by January 1 must still enroll by December 15th.

In addition to the extension of the ACA enrollment period, an interesting and positive turn is that Aetna and Unitedhealthcare are re-entering the marketplace in SE Texas for 2022 after a six year hiatus! This brings welcome competition to a market which was vacated by every major carrier – other than BlueCross BlueShield – in January of 2016. While we will not have insight into the details of their health plan options until just before November 1, their names and reputation should garner a lot of attention, not only from consumers but medical providers. It is my hope that more high quality doctors and hospitals will elect to participate in the insurance companies’ provider networks. With Preferred Provider Organization (PPO) network plans eliminated, Health Maintenance Organization (HMO) network plans have been the consumer’s only option since 2016. And with the expansion in the availability of the Advance Premium Tax Credit and Cost Share Reductions, for many, their greatest challenge is no longer being able to afford health insurance but finding their providers in an insurance plan’s network.

And it is the same for me. As an agent / broker with 34 years in medical insurance, my greatest challenge isn’t finding a plan the consumer can afford or the benefits they’re seeking. It’s finding my client’s, and prospective client’s, medical providers participating in a network. While this isn’t a major issue to those new to the area, those of us who have resided here for years, have long established relationships with providers we are reluctant to part with.

I would be extremely pleased if some of the companies in the marketplace elect to offer PPO plans in 2022. But make no mistake, I in no way expect this to happen. The problem for a company considering offering PPO coverage is that if all their peers do not also, they “adversely select” against themselves. In other words, if they are the “only game in town” when it comes to PPO plans, they are going to attract, and garner, an inordinate number of “bad risks”. In other words, insured members with serious pre-existing conditions who need access to a greater number of providers will flock to them vs the insurance company offering access to an HMO network only. They will submit higher and more frequent claims, thereby compounding the potential for “loss” to the insurance company. This is why insurance companies ceased, in unison, offering PPO coverage, in most regions of the United States, in 2016. They want to limit your access to providers, and thereby limit your access to what is likely to be more expensive treatment. Enrolling people in HMO plans is the easiest way to do this. Regardless, my duty, as your agent, is to do my best to find your providers participating in the network of a plan whose benefits meet your needs.

The good news is – two new major carriers will uncertainly increase the number of options available to the consumer in terms of premiums, benefits, and providers. Additionally, several of the insurance companies are lowering copays and deductibles and the Department of Health and Human Services, which oversees the sale of all ACA health insurance, has made it much easier to qualify for a “subsidy” to reduce the policyholder’s share of the premium due, especially for anyone who claimed unemployment benefits any time during 2021.

In the Medicare related insurance market, increases in variables for 2022 are estimated to be higher than in recent years. Some were not definite as of the end of September. The Part A In-patient deductible is projected to increase but, as of this date, I have no definitive cost. The Part B Out-patient deductible is estimated to be going from $203 to $217 per calendar year and it’s premium is projected to go from $148.50 to $158.50 per month.

There are currently 30 different Part D Drug plans for Texans to choose from. Each covers some drugs but not others. The plan which is best for you is entirely dependent on the drugs you use. Not the drugs your spouse, neighbor, or I use – but the ones you use. The Part D deductible is going from $445 to $480 for the calendar year. A drug plan may choose to have deductible ranging from $0 all the way to$480 before your drugs become available for a copay. With many plans, the deductible will not apply to Tier 1 and Tier 2 generic drugs. The threshold for entering the “GAP” will occur when the member and plan have paid $4,430. During this time, the member will pay 25% of the cost of their drugs. They will cross over into “CATASTROPHIC COVERAGE” if, and when, the member has personally expended $7,050. At this point, a member will pay $3.95 for a generic drug and $9.85 or 5% of the cost of a brand name drug – whichever is higher.

As a broker for my clients, and prospective clients, my goal is to identify the Medicare Plan, whether Medicare Supplement, Advantage or Part D Drug Plan which is most likely to result in their lowest total out of pocket cost for the calendar year while providing them access to all their providers. The “total cost” is the sum of their premium, any applicable deductible or deductibles, and copays or coinsurance. Our objective is the lowest sum and that plan, or plans, will usually be my recommendation.

To this end, I encourage anyone interested in enlisting my help, to contact me. If you would like me to identify your lowest total cost drug plan for 2022, based on your current or anticipated drug use, email me a list of your Rx drugs and, preferably, the dosages. The latter can make a difference. If you know you want Medicare Advantage, send me a list of doctors and hospitals you feel you must have access to. Please recall that with Medicare Supplement coverage you may obtain treatment from any doctor, hospital, lab, or medical provider, that sees Medicare patients. There are no networks with which to concern yourself. However, with Supplement, unlike most Medicare Advantage plans, you will have to acquire a Part D Prescription Drug Plan to accompany it. For those using little or only low cost generic drugs, the lowest premium plan for Texans in 2022 will be $6.90 per month.

*(READ FEATURED ARTICLE BELOW ON WASHINGTON’S EFFORTS TO LOWER RX DRUG COST FOR MEDICARE RECIPIENTS)

The name of my insurance agency I opened in 1991, after being in the medical and life insurance industry since 1986, is All Plan Med Quote. It is located in The Woodlands, Texas. In 1995, I created one of the first websites in the country to market health insurance via the internet. It still exists as Allplanhealthinsurance.com. In 2015, I expanded my web presence with TheWoodlandsTXHealthInsurance.com. The primary objective in naming the first two was to convey that (while I work, for the consumer) I am appointed (contracted) with virtually every “A” rated, major and minor insurance company doing business in your geographic region. But the insurance companies do not pay me a guaranteed wage or salary. They compensate me fairly if, and only if, you elect to go through me to acquire their products. But, without my clients, I have no income. So certainly my clients are my priority. Not the insurance companies. And, as my client, you are charged no more by going through me to obtain their product then if you walked through their front door and acquired it directly from them.

Here is a partial list of the companies whose products may, or may not, be appropriate for you, I may introduce to you:

AARP Unitedhealthcare

Aetna

Ambetter

Anthem

BlueCross BlueShield of Texas

Caresource

Cigna

Community Health Choice

Friday

Humana

KelseyCare Advantage

Molina

Mutual of Omaha

Oscar

Scott and White

Unitedhealthcare

Wellcare

D. Kenton Henry Office: 281-367-6565 Text my cell 24/7: 713-907-7984 Email: Allplanhealthinsurance.com@gmail.com

Democrats’ signature legislation to lower drug prices was defeated in a House committee on Wednesday as three moderate Democrats voted against their party.

Reps. Kurt Schrader (D-Ore.), Scott Peters (D-Calif.), and Kathleen Rice (D-N.Y.) voted against the measure to allow the secretary of Health and Human Services to negotiate lower drug prices, a long-held goal of Democrats.

The vote is a striking setback for Democrats’ $3.5 trillion package. Drug pricing is intended to be a key way to pay for the package. Leadership can still add a version of the provision back later in the process, but the move shows the depth of some moderate concerns.

The three moderates said they worried the measure would harm innovation from drug companies and pushed a scaled-back rival measure. The pharmaceutical industry has also attacked Democratic leaders’ measure, known as H.R. 3, as harming innovation.

The three lawmakers had long signaled their concerns with the drug pricing measure, but actually voting it down in the House Energy and Commerce Committee is an escalation.

A separate committee, the House Ways and Means Committee, did advance the drug pricing measures on Wednesday, keeping the provisions in play for later in the process.

Energy and Commerce Committee Chairman Frank Pallone Jr. (D-N.J.) had implored the three lawmakers to vote in favor of the measure to at least keep the process going.

“Vote to move forward today,” he said to the moderates in his party. “Vote to continue the conversation.”

Still, Pallone said he is confident that some form of measure to lower drug prices will make it into the final package. The House legislation was already expected to change before the final version, given moderate Democratic concerns in the Senate as well. Senate Democrats are working on their own bill, which is not yet finalized but is expected to be less far-reaching.

“I know it is going to have drug pricing reform,” Pallone said of the final bill, noting that negotiations with the Senate would continue over the coming weeks.

Still, the move on Wednesday is a show of force from the moderates.

Henry Connelly, a spokesman for Speaker Nancy Pelosi (D-Calif.), said Democrats were not giving up on including drug pricing measures.

“Polling consistently shows immense bipartisan support for Democrats’ drug price negotiation legislation, including overwhelming majorities of Republicans and independents who are fed up with Big Pharma charging Americans so much more than they charge for the same medicines overseas,” he said in a statement after the vote. “Delivering lower drug costs is a top priority of the American people and will remain a cornerstone of the Build Back Better Act as work continues between the House, Senate and White House on the final bill.”

Peters and Schrader both cited concerns about harming drug companies’ ability to develop new drugs, citing the industry’s record during the COVID-19 crisis.

Peters warned that “government-dictated prices” under the bill would cause harm to the “private investment” that backs drug development.

Schrader said the bill would mean “killing jobs and innovation that drives cures for these rare diseases.”

Advocates said the lawmakers were simply beholden to the pharmaceutical industry.

“Reps. Peters, Rice, and Schrader are prioritizing drug company profits over lower drug prices for the American people, particularly for patients with chronic conditions such as diabetes and multiple sclerosis,” said Patrick Gaspard, president of the left-leaning Center for American Progress. “To the contrary of what they contend, their opposition to the drugs proposal threatens the entirety of President Joe Biden’s Build Back Better agenda, which Democrats have campaigned on for years and that they previously voted for.”

Savings from the drug pricing provisions are a key way of paying for other health care priorities in the $3.5 trillion package, including expanding Medicaid in the 12 GOP-led states that have so far refused, expanding financial assistance under ObamaCare, and adding dental, vision, and hearing benefits to Medicare.

The Congressional Budget Office found that H.R. 3 would save about $500 billion over 10 years. Depending on what Senate Democrats can find agreement on, the final drug pricing legislation is expected to be less far-reaching, meaning it will result in fewer savings, though how much less is unclear.

The Senate bill would still allow Medicare to negotiate lower drug prices, but it is expected not to include another provision that would cap drug prices based on the lower prices paid in other wealthy countries. That provision has drawn particular pushback from some moderate Democrats.

Allowing Medicare to negotiate drug prices is extremely popular with voters, with almost 90 percent support in a Kaiser Family Foundation poll earlier this year. Many vulnerable House Democrats support the idea.

Are you recently faced with a choice between the high cost of COBRA or going without health insurance? Perhaps we can help.

As if the jobs lost due to lay-offs, furloughs, and the closing of businesses stemming from the coronavirus quarantine wasn’t bad enough, the concurrent and additional losses due to the precipitous drop in the price of oil, have made unemployment rates in Texas soar. For those, like myself, who were present at the time, the situation conjures memories of the oil bust of the 1980’s. The resulting home foreclosures, vehicle repossessions, and mass migration from our state were catastrophic, and our state didn’t fully recover until the mid-’90s. But, as terrible as things were, we never saw oil prices drop “to the negative” as they did a few short weeks ago. We can only hope and take heart in the reality that―because financial fundamentals were so strong prior to the pandemic―this crisis will be much shorter once herd immunity has turned the corner on it―and Saudi Arabia and Russia have ceased attempting to crush the market for the sake of driving out the competition.

UNEMPLOYMENT LINES IN WAKE OF CORONAVIRUS

Regardless, this mass unemployment has resulted in thousands losing their health insurance and has left them faced with accepting the high cost of COBRA or (if employed by companies with less than 20 employees) state-continuation health insurance. If accepting either, the former employee is typically responsible for 100% of the retail premium (inclusive of the portion previously paid by their employer) plus an administrative fee of 2%.

An alternative is to enter the “Individual and Family” health insurance market. If one applies within 60 days of losing their employer-based, credible coverage, they will be guaranteed approval and coverage for any pre-existing health conditions on the first of the month following application. You may obtain quotes for all credible ACA (Affordable Care Act) compliant individual and family plans available to you―as well as an estimate of any subsidy for which you may qualify―by clicking on the link below. Then call us for answers to your questions and assistance in applying for coverage*:

*(you do not need to log-in in order to obtain quotes)

Even when a subsidy is available, many find the premiums for these plans to be unaffordable. For those, “Short-Term” or “Temporary” health insurance may be the answer. As premiums for long-term health insurance continue to rise, more and more people find this to be the case. The advantages are, it can become effective immediately, and you can purchase it for periods up to just short of two years. Because the insurance company knows it will only be obligated to pay claims for a limited period―the premiums will be dramatically lower than those of long-term ACA health insurance. The disadvantage of short-term health insurance is that you first must be approved, and the coverage will not cover pre-existing health conditions. So, if you, or a family member, have any moderate to significant health conditions, you may be declined for coverage or find your pre-existing conditions waived for coverage. But, if you have no health issues or can be approved for coverage and can afford to self-insure for your conditions, you will find this coverage much more affordable!

Our feature article below outlines the trend toward purchasing Short-Term health insurance and the reasons for it. It also introduces a company the clients of TheWoodlandsTXHealthInsurance.com have turned to for years to acquire coverage. From the following link, you can choose from a multitude of deductibles and benefit levels to elect a plan specific to your needs and budget. Once you have narrowed your selection, please call us for answers to your questions and assistance in applying.

You may find you only require this coverage until this unprecedented coronavirus/oil market crisis is behind us or until you obtain your next job with benefits. Regardless, we are here to see you obtain the best coverage for your situation and the best of service thereafter.

CLICK HERE FOR SHORT-TERM HEALTH INSURANCE QUOTES:

For customized quotes with from a subsidiary of Unitedhealthcare, inclusive of:

· Enhanced Short Term Medical – with preventive care coverage on all plans, no limit on urgent care visits with a copay, and no application fees – are now available in 17 states!

· TriTerm Medical – nearly 3 years of continuous health insurance with coverage for doctor visits, prescriptions, and preventive care – now available to quote in 16 states.

· HealthiestYou by Teladoc® members now have access to behavioral health and dermatology services (for an additional per-use fee). Using the same convenient app and phone number, they can access these new services in addition to 24/7 access to doctors. *This product is not insurance.

Call us. We will help you sort through all your options in order to elect the best health insurance or your situation.

D. Kenton Henry Editor, Agent Broker TheWoodlandsTXHealthInsurance.com Office: 281-367-6565 Text My Cell 24/7 @ 713-907-7984

Survey: Short-Term Health Insurance Demand Increasings

Share to FacebookShare to TwitterShare to LinkedInShare to PrintShare to EmailShare to More30

Pivot Health, a division of HealthCare.com, which is a leader in technology-enabled health insurance solutions, has released new customer survey data that reveals 26% of short-term medical plan purchasers were long-time uninsured, while 29% had recently lost their insurance due to unemployment.

Only 5% of purchasers had moved from an Obamacare plan to a short-term medical insurance plan. The survey also showed 75% of the people who lost employer coverage did not choose COBRA because of cost.

Nearly half (46%) of members selected a short-term plan because they didn’t qualify for a subsidy or they needed something quickly. The survey also found 21% of those who purchased a short-term health insurance plan were influenced by the global coronavirus pandemic.

When asked what is the greatest concern facing the health insurance market today, survey participants said out-of-pocket costs were the No. 1 issue they are concerned about when it came to healthcare.

· 64% are concerned about the high monthly cost of insurance.

· 51% worry about paying for medical bills out of pocket.

· 45% are concerned about high deductibles.

One customer said, “Most Americans cannot afford high-cost insurance. Anything over $100 a month is too much.”

“The survey data reveals that customers are more comfortable buying short-term health insurance plans than they ever have been,” said Jeff Smedsrud, chief executive officer of Pivot Health. “Since Congress has failed to pass legislation to subsidize COBRA plans, which put the entire financial burden on the employee, short-term health plans are becoming a general preference for individuals who need a budget-friendly healthcare solution as they maneuver through life transitions, unemployment or just need economical coverage.”

HealthCare.com is an online health insurance company providing a data-driven shopping platform that helps American consumers enroll in individual health insurance and Medicare plans. HealthCare.com also develops and markets a portfolio of proprietary, direct-to-consumer health insurance and supplemental insurance products under the name Pivot Health. Founded in 2014, the company is headquartered in New York City and is backed by PeopleFund and individual investors including current and former executives of Booking.com and Priceline. HealthCare.com is a 4-time honoree of the Inc. 5000 list of America’s fastest-growing companies and has been recognized by Deloitte as one of the fastest-growing technology companies in North America.

By D. Kenton Henry Editor, Agent, Broker 29 October 2018

The media is proffering all manner of good news when it comes to the Open Enrollment Period for purchasing 2019 individual and family health insurance, just three days away. The doors open this Thursday, November 1st and will remain so through December 15th. During this time you, the consumer, will be able to review your options and make a decision to renew your existing policy or select a new one to become effective January 1. Whichever, that policy will cover you the coming calendar year.

The feature article appearing below, states there will be ” . . . fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.” To wit, it cites, the budget for insurance counselors, known as navigators, has been cut by 80%, leaving over one-third of navigators in 2,400 counties served by Healthcare.gov, unfunded. Thank you very much, New York Times. Somehow, they neglected to consult with me and my agency, ALL PLAN MED QUOTE. Reading the article in full, one can infer they feel the only meaningful assistance can come from the government (at taxpayers’ expense) and fail to credit the private industry, which has provided counsel and enrollment assistance within the domestic insurance industry some two hundred years plus. One token sentence in the article acknowledges the private industry’s presence to assist the consumer with procuring health insurance. In my estimation, this reflects the media’s general opinion and thesis that the government is the end-all solution to every conceivable personal financial issue. Which, again, in the mind of this editor, is precisely the philosophy, the perpetuation of which got us into this fix in the first place. Moreover, what exactly is that fix?

Current pre-midterm election media coverage informs us premiums have stabilized and are, in many cases, going down in 2019. While that may be true in some localities, the recently released premiums in southeast Texas reflect increases of 20% or more. If you obtain a subsidy, wherein you get a tax credit for a portion of your premium, the subsidy itself may be larger, but the balance may be as well. Also, for those not obtaining a subsidy (the vast majority of us) the increase will be born entirely by ourselves. The situation has made healthcare the number one concern of Americans heading into next week’s midterm elections according to a Fox News Poll.

For the record, ALL PLAN MED QUOTE and I have never been subsidized by taxpayer dollars. As an independent, self-employed broker/agent I am compensated when I successfully enroll someone in health insurance. I am not compensated when I fail at such. That is fine by me. In spite of continual cuts in agent compensation. I prefer autonomy to bureaucracy. My advice and guidance are objective. My goal is to succeed it getting you enrolled in a policy which makes sure you have access to the care and treatment you need, when you need it and are not financially devastated in the process. All this for the lowest possible premium. I do not care which insurance company you contract with, as long as you are satisfied you have obtained the best coverage for your given situation and needs. Ideally, it would also provide you access to all the doctors and medical providers you choose to utilize. Regrettably, that latter objective has become my biggest challenge and is one every insurance agent and counselor faces. To say it can be overcome in every instance would be misleading but I do my best. All 2019 individual and family options are Health Maintenance Organizations (HMO) policies, and this has been so since 2016. The HMO networks are narrow in comparison to what one may typically have experienced with employer-based HMO coverage. However, there are a very few plans (3 in my primary region) which operate very similar to a traditional Exclusive Provider Organization (EPO) policy in that they do cover treatment at a provider outside the network. Benefits are paid up to a limited percentage, and there is no cap on your maximum annual out-of-pocket but―for someone who wants to be assured they can obtain coverage from the provider of their choice―it is better than no coverage whatsoever. If you feel you must learn more about this option, please contact me.

To assist me in these ends, I am appointed with every company providing Patient Protection and Affordable Care Act-compliant health insurance company doing business in Montgomery, Harris, Fort Bend, and Galveston counties. BlueCross BlueShield of Texas (to my knowledge) does business in every corner of Texas, and I have been appointed with them twenty-seven years. In addition to Texas, I am licensed in Indiana, Michigan, and Ohio.

I offer short-term health insurance for those who do not get a subsidy and those who, whether they do or not, cannot afford credible health insurance. However, I do not represent it as covering pre-existing health conditions, as it does not. Nor do I represent it as a substitute for credible, compliant coverage. It is a short-term bridge to a long-term solution.

As always, the Open Enrollment Period will be a very busy and hectic time for anyone in my profession. To make things proceed more smoothly, I would appreciate you visit my quoting site to obtain spreadsheet comparison of your options from all the health insurance companies offering coverage in your county. Attempt to narrow your selection down to those plans you feel most closely approximate the coverage you need. You can search for in-network providers from the search button directly next to the premium quoted. If you are so confident a plan is right for you, please feel free to apply straight from the quote. However, many of you will have questions or appreciate my insight and experience with the plan details and application process. Those in need of a subsidy will find my assistance especially helpful. If this is you, please do not hesitate to contact me.

Again, for quotes and applications, you may go to my website at Http://TheWoodlandsTXHealthInsurance.com and click on “Health” in the top menu.

Alternatively, you may go directly to my spreadsheet quotes and an application by clicking on this link: https://allplanhealthinsurance.insxcloud.com

*(it is not necessary to log in or register to obtain quotes or apply)

**(if these links do not function from this text, please copy and paste or type in your browser and hit enter)

If you apply for coverage through these links, I will be your agent and available to assist and commit to providing the best of service throughout the year. I bring my entire thirty-two years in medical insurance to bear for this purpose. I look forward to hearing from you and assisting you. Regardless, I hope you succeed in obtaining health insurance which suffices until Congress puts their heads together and provides us with more reasonable options.

D. Kenton Henry All Plan Med Quote Office: 281.367.6565 Text my cell @ 713.907.7984 Email: Allplanhealthinsurance.com For the latest in health and Medicare-related insurance, news go to Https://HealthandMedicareInsurance.com

************************************************************************************************ FEATURED ARTICLE

The New York Times By Robert Pear Oct. 27, 2018

Shopping for Insurance? Don’t Expect Much Help Navigating Plans

Affordable Care Act navigators helping patients during an enrollment event in 2016 at Southwest General Hospital in San Antonio.CreditCreditEric Gay/Associated Press

WASHINGTON — When the annual open enrollment period begins in a few days, consumers across the country will have more choices under the Affordable Care Act, but fewer sources of unbiased advice and assistance to guide them through the labyrinth of health insurance.

The Trump administration has opened the door to aggressive marketing of short-term insurance plans, which are not required to cover pre-existing medical conditions. Insurers are entering or returning to the Affordable Care Act marketplace, expanding their service areas and offering new products. But the budget for the insurance counselors known as navigators has been cut more than 80 percent, and in nearly one-third of the 2,400 counties served by HealthCare.gov, no navigators have been funded by the federal government.

“There is likely to be a lot of consumer confusion about the various plan options that may be available this year,” said Sabrina Corlette, a research professor at Georgetown University’s Health Policy Institute. “It will be a bit of a Wild West — buyer beware!”

“Obamacare health plans,” short-term plans and “Christian health sharing plans” are all displayed on the same page of some shopping sites like Affordable-Health-Insurance-Plans.org, which describes itself as a free referral service for insurance shoppers.

ADVERTISEMENT

Consumers may have difficulty sorting through their options after the administration sliced the budget last summer for insurance navigators to $10 million this year, from $36 million in 2017 and nearly $63 million in 2016.

“Navigators play a vital role in helping consumers prepare applications to establish eligibility and enroll in coverage through the marketplaces,” the Department of Health and Human Services says on its website.

But 797 counties served by HealthCare.gov will not have any navigators this year, according to a tabulation of federal data by the Kaiser Family Foundation. That is a sharp increase from 2016, when 127 counties lacked such assistance.

“If you are confused and you want somebody’s help to try to figure out what’s right for you — what’s junk and what is legitimate — there will be fewer people to help you in most states,” Ms. Corlette said.

Federal officials said they were not providing funds for navigators in Iowa, Montana or New Hampshire because no organizations had applied for the money in those states.

Cleveland, Dallas and large areas of Michigan and other states will also be without navigators.

Texas will be hit hard. The state has the largest number and the highest percentage of people who are uninsured, with 4.8 million people, or 17 percent of residents, lacking coverage, according to the Census Bureau.

“North Texas remains one of the most uninsured areas in the country,” said the chief executive of Dallas County, Judge Clay Lewis Jenkins. “The administration’s decision to defund all navigators across North Texas will hurt our ability to enroll individuals in health insurance and result in some working families losing coverage. Only 45 of Texas’ 254 counties have any navigator coverage.”

Seema Verma, the administrator of the Centers for Medicare and Medicaid Services, defended the cuts.

After five years, she said, “the public is more aware of the options for private coverage” available through the marketplace, so “it is appropriate to scale down the navigator program.” In addition, she said, information and assistance are available from other sources, including insurance agents and brokers.

Consumers can sign up for health insurance under the Affordable Care Act starting Thursday. Last year, 8.7 million people enrolled at HealthCare.gov, and three million more selected plans on insurance exchanges run by states.

Consumers can go without insurance next year without fear of a penalty, as Congress repealed the unpopular tax surcharge imposed on people who lack coverage.

Many health policy experts say that federal financial assistance is more important than the individual mandate in inducing people to buy insurance. Those subsidies will still be available to low- and moderate-income people for insurance that complies with the Affordable Care Act and is purchased through the public marketplace. The subsidies cannot be used for short-term policies.

The vast majority of the people we serve, over 90 percent, are motivated to have insurance because they want coverage for their family and themselves,” said Matthew Slonaker, the executive director of the Utah Health Policy Project, a nonprofit. “It’s not because they otherwise would have to pay a penalty.”

Average premiums for the most popular types of insurance purchased by individuals and families will be relatively stable next year and, in some states, will actually decline, the administration says.

Under new standards issued by the administration, navigators this year are encouraged to inform consumers of the full range of coverage options, including short-term plans that do not provide all of the benefits and consumer protections required by the Affordable Care Act.

President Trump has promoted the short-term policies as an inexpensive alternative to the Affordable Care Act, and he said those plans would be “much more widely available” as a result of an executive order he signed last year to overturn restrictions imposed by President Barack Obama.

Democrats have made health care a major theme in midterm election campaigns, and they say the short-term policies show how the Trump administration threatens protections for people with pre-existing conditions.

Short-term policies, which can extend up to 364 days and then be renewed for two additional years, often provide no coverage for pre-existing conditions, prescription drugs, pregnancy, maternity care or the treatment of mental disorders and drug abuse.

Indeed, Mr. Trump said, the short-term plans are cheaper because they are “not subject to any very expansive and expensive Obamacare coverage mandates and rules.”

ADVERTISEMENT

But, said Kirsten A. Sloan, a vice president of the American Cancer Society Cancer Action Network: “People may be attracted to short-term plans without understanding that the lower premiums come with less coverage. These plans may not cover the doctors and hospitals and drugs you need if you get sick.”

In another challenge this year, consumers may be deluged with robocalls offering cheap insurance.

Alex Quilici, the chief executive of YouMail, a company that offers software to combat robocalls, said he was seeing a huge increase in health insurance scams.

“Callers say ‘it’s open enrollment’ or ‘we can get you a better deal by looking at all the health insurance plans,’” Mr. Quilici said. “Callers ask for lots of personal information, and the unwitting consumer often gives their birth date, Social Security number and information for everybody in the family, in order to get a great deal. In reality, it’s identity theft or payment theft or both.”

Mr. Quilici’s company has recorded hundreds of robocalls. A typical call says that, with enrollment just “around the corner,” Mr. Trump has created short-term coverage options lasting up to three years, “so you and your family can get a great insurance plan at the price you can afford.”

It is difficult to identify the source of the robocalls, Mr. Quilici said, because callers often falsify information displayed on caller ID.

(A version of this article appears in print on Oct. 27, 2018, on Page A25 of the New York edition with the headline: Shopping for Health Insurance: Many Options but Little Guidance. Order Reprints | Today’s Paper | Subscribe)

Last evening I began to receive texts and messages inquiring how President Trump’s executive order (EO) on Thursday, October 12th, would impact both the near and long-term future of Obamacare. Before retiring for the evening, I responded – “In the long run, dramatically. But in the short run, not so much because it will take quite awhile for the insurance industry to respond appropriately.” At that time, all I had learned was, the President ordered regulators to allow consumers to shop across state lines for health insurance along with the ability individuals of like professions, careers, and risk profiles, to band together in associations for the purpose of acquiring individual and family health insurance. Theoretically, the first would allow the consumer to shop for their best value among a far greater number of companies and plans, thus restoring competition to the market. The second would allow pooling a large number of people, and the resulting volume would lower risk to the insurance companies, thus allowing them to charge lower premiums to the members. The same principle and effect currently available to employer groups. And that was all I was aware of regarding the EO. Additionally, the EO loosens the restrictions on “Short-Term” health insurance, allowing it to serve as a viable alternative to long-term coverage for the young and/or healthy.

Today, I awakened to learn the Department of Health and Human Services announced late last night that the EO includes the cessation of federal payments for Cost-Sharing Reductions (CSRs) to insurance companies. “Immediately.” This, according to Secretary Eric Hargan and Medicare administrator, Seema Verma. And―with that―all bets are off! The Administration claims this can be done because Congress never appropriated funds for the CSRs. These funds were used to reimburse insurers for the CSRs which result in reductions in deductibles, copays, and out-of-pocket maximums for eligible individuals. However, while the insurers will lose these subsidies (amounting to $7 billion this year), they remain obligated to continue offering them to eligible customers! Eligible customers mostly include those qualifying for subsidies and electing “Silver” plans through the Marketplace, Healthcare.gov. At the very least, halting the payments could trigger a spike in premiums, at some point, for the coming year, unless Congress authorizes the money. The next payments are due around October 20th. The Congressional Budget Office estimates, without the subsidies, premiums could go up by as much as 20%. That is on top of the 15-20% average increase anticipated with the subsidies in place! Nearly 3 in 5 Healthcare.gov customers qualify for help. If you qualify for a premium subsidy, the increase will simply be paid for by your fellow taxpayers as it has the last four years. The person or family who does not qualify will have to pay for it entirely out of their own pocket. As always, it is the hard working middle class who could be hurt the most. Those who make just enough to get by, but a little too much to qualify for government assistance.

Will this break Obamacare altogether and, if so, when? What impact will it have on 2018 individual and family health insurance premiums? Rates had to be (and were) submitted to state health insurance commissioners, as required, on September 30th. Can insurance companies pull out of the market at this point? Will they? Apparently, Premium Subsidies (separate from CSRs), designed to lower premiums, per se, for qualified individuals – as well as though qualifying for tax credits upon filing – will not be affected. However, here is what the Washington Post (article below) had to say about the cessation of CSR subsidies, alone: “Ending the payments is grounds for any insurer to back out of its federal contract to sell health plans for 2018. Some state’ regulators directed ACA insurers to add a surcharge in case the payments were not made, but insurers elsewhere could be left in a position in which they still must give consumers the discounts but will not be reimbursed.” In my opinion, it is too late to submit new rates for approval in time for Open Enrollment, just around the corner. But it is not too late for an insurance company to pull out of the market altogether. What options will that leave the consumer, including my clients, for coverage in 2018 and beyond?

I agree with the administration; this is their move to force the hand of Congress to reverse the policies of Obamacare, restore competition and consumer choice, to the market. It will allow elements of a free market to regulate the variables, most important of which are, benefits, choice of provider, and premium. How long it will take for this action on the part of the Trump to accomplish this, I can’t say. The Executive Order is almost certain to be challenged by state Attorney Generals and litigated in federal courts. This could take months, or more, to play out, and probably will.

I apologize that, at this point, I have more questions than answers. In the meantime, I, and, my clients have yet to learn what our 2018 health options and premiums would be (or would have been) without the ramifications of the Executive Order. Rest assured, I will be watching in earnest for the details as this situation evolves.

As always, please feel free to phone me at 281.367.6565; text me at 713.907.7984 or email me at allplanhealthinsurance.com@gmail.com. The closer we get to November 1, the more I will know. And whatever is available to you, I will have. Along with your best option. Bear in mind, “best” is a relative term.

*************************************************************************************************** Featured article:

WASHINGTON POST

By Amy Goldstein and Juliet Eilperin By Amy Goldstein and Juliet Eilperin

Health & Science

October 13 at 9:42 AM

President Trump is throwing a bomb into the insurance marketplaces created under the Affordable Care Act, choosing to end critical payments to health insurers that help millions of lower-income Americans afford coverage. The decision coincides with an executive order on Thursday to allow alternative health plans that skirt the law’s requirements.

The White House confirmed late Thursday that it would halt federal payments for cost-sharing reductions, although a statement did not specify when. Another statement a short time later by top officials at the Health and Human Services Department said the cutoff would be immediate. The subsidies total about $7 billion this year.

Trump has threatened for months to stop the payments, which go to insurers that are required by the law to help eligible consumers afford their deductibles and other out-of-pocket expenses. But he held off while other administration officials warned him such a move would cause an implosion of the ACA marketplaces that could be blamed on Republicans, according to two individuals briefed on the decision.

Health insurers and state regulators have been in a state of high anxiety over the prospect of the marketplaces cratering because of such White House action. The fifth year’s open-enrollment season for consumers to buy coverage through ACA exchanges will start in less than three weeks, and insurers have said that stopping the cost-sharing payments would be the single greatest step the Trump administration could take to damage the marketplaces — and the law.

Ending the payments is grounds for any insurer to back out of its federal contract to sell health plans for 2018. Some states’ regulators directed ACA insurers to add a surcharge in case the payments were not made, but insurers elsewhere could be left in a position in which they still must give consumers the discounts but will not be reimbursed.

A spokeswoman for America’s Health Insurance Plans, an industry trade group that has been warning for months of adverse effects if the payments ended, immediately denounced the president’s decision. “Millions of Americans rely on these benefits to afford their coverage and care,” Kristine Grow said.

And California Attorney General Xavier Becerra (D), who has been trying to preserve the payments through litigation, said the president’s action “would be sabotage.” Becerra said late Thursday that he was prepared to fight the White House. “We’ve taken the Trump Administration to court before and won, and we’re ready to do it again if necessary,” he said in a statement.

Trump’s move comes even as bipartisan negotiations continue on one Senate committee over ways to prop up the ACA marketplaces. Both Sens. Lamar Alexander (R-Tenn.) and Patty Murray (D-Wash.) have publicly said the payments should not end immediately, though they differ over how long these subsidies should be guaranteed.

The cost-sharing reductions — or CSRs, as they are known — have long been the subject of a political and legal seesaw. Congressional Republicans argued that the sprawling 2010 health-care law that established them does not include specific language providing appropriations to cover the government’s cost. House Republicans sued HHS over the payments during President Barack Obama’s second term. A federal court agreed that they were illegal, and the case has been pending before the U.S. Court of Appeals for the D.C. Circuit.

President Trump signed an executive order on the Affordable Care Act on Oct. 12. With the order, he directed federal agencies to rewrite regulations on selling a certain type of health insurance across state lines. President Trump signed an executive order on the Affordable Care Act on Oct. 12. (Photo: Jabin Botsford/The Washington Post)

President Trump signed an executive order on the Affordable Care Act on Oct. 12. With the order, he directed federal agencies to rewrite regulations on selling a certain type of health insurance across state lines. (The Washington Post)

“The bailout of insurance companies through these unlawful payments is yet another example of how the previous administration abused taxpayer dollars and skirted the law to prop up a broken system,” a statement from the White House said. “Congress needs to repeal and replace the disastrous Obamacare law and provide real relief to the American people.”

In a filing Friday morning, the administration informed the court that HHS had “directed that cost-sharing reduction payments be stopped because it has determined that those payments are not funded by the permanent appropriation.”

House Speaker Paul D. Ryan (R-Wis.) said in a statement that the administration was dropping its appeal of the lawsuit — something the White House did not mention in its announcement. Ryan called the move to end to the court case “a monumental affirmation of Congress’s authority and the separation of powers.”

Meanwhile, the top two congressional Democrats, House Minority Leader Nancy Pelosi (Calif.) and Senate Minority Leader Charles E. Schumer (N.Y.), excoriated the president’s decision. “It is a spiteful act of vast, pointless sabotage leveled at working families and the middle class in every corner of America,” they said in a joint statement. “Make no mistake about it, Trump will try to blame the Affordable Care Act, but this will fall on his back and he will pay the price for it.”

For months, administration officials have debated privately about what to do. The president has consistently pushed to stop the payments, according to officials and advisers who spoke on the condition of anonymity to discuss private conversations. Some top health officials within the administration, including former HHS secretary Tom Price, cautioned that this could exacerbate already escalating ACA plan premiums, these Republicans said. But some government lawyers argued that the payments were not authorized under the existing law, according to one administration official, and would be difficult to keep defending in court.

Acting HHS secretary Eric Hargan and Seema Verma, administrator of the department’s Centers for Medicare and Medicaid Services, said they were stopping the payments based on a legal opinion by Attorney General Jeff Sessions. “It has been clear for many years that Obamacare is bad policy. It is also bad law,” their statement says. “The Obama Administration unfortunately went ahead and made CSR payments to insurance companies after requesting — but never ultimately receiving — an appropriation from Congress as required by law.”

While the administration will now argue that Congress should appropriate the funds if it wants them to continue, such a proposal will face a serious hurdle on Capitol Hill. In a recent interview, Rep. Tom Cole (R-Okla.), who chairs the House Appropriations Subcommittee overseeing HHS, said it would be difficult to muster support for such a move among House conservatives.

One person familiar with the president’s decision said HHS officials and Trump’s domestic policy advisers had urged him to continue the payments at least through the end of the year.

The cost-sharing payments are separate from a different subsidy that provides federal assistance with premiums to more than four-fifths of the 10 million Americans with ACA coverage.