Healthandmedicareinsurance.com followers – I spent enough time responding to the left on my facebook posting – I thought the effort could serve double duty on this blog.

***************************************************************************************************

Before preparing for my trip, I would first like to respond to Kathy: No, I won’t be lobbying for an expansion of Medicaid in Indiana (or any other state for that matter) that has not already expanded it beyond 100% of the Federal Poverty Level. If Medicaid were expanded, it would be to include individuals up to and including those with an income of 133% of the FPL or a maximum income of $15,521 for 2014. Deserving or not aside – while these individuals currently do not qualify for Medicaid in Indiana or Texas – THEY DO qualify for a subsidy of approximately 88% of their health insurance premium. If they elect the plan recommended by the Department of Health and Human Services (“benchmark” plan) it will be the second lowest cost Silver Plan in their area. They are required to pay no more than $40.41 per month. No, I don’t feel sorry for them. They are certainly already receiving food stamps and government subsidized housing and Medicaid is already in financial trouble in most states without further expansion. (Of course I am aware financial feasibility and a balanced state or federal budget is not your concern.)

The person I feel sorry for is the poor working stiff who is making in the $50 – $60,000 dollar range and actually earning his or her income. They don’t qualify a health insurance premium subsidy. (Food stamps I’m not certain of because our government has made those available to virtually everyone including illegal aliens.) Because this responsible working person doesn’t qualify for a subsidy, they will be forced to pay 100% of the Silver plan premium–with an average annual cost of $4,113–entirely on their own. That amounts to 8% of their annual income (at $50k) before taxes which the entitlement person isn’t paying! That’s the person I feel sorry for! Then try providing them with a plan that has their doctor in the network and the benefits they would really like and their cost and that percentage soars! In summation – you keep lobbying for the entitlement class; I’ll keep lobbying for the working American.

Now to address Scott: Glad to see you are finally making a prediction which I feel is pretty much on target. As I’m the one on the front line signing people up for Obamacare, no one knows better the “adverse selection” (bad risk disproportionately selected for participation) than I. But I remember a few of my predictions you tried to dismiss. First – I said Barrack Obama would be elected in 2008. You said, “no”. In 2010 – I said the Patient Protection and Affordable Care Act (PPACA or ACA for short) would pass. You said, “no way!”. Then, in June of 2012 – I said the Supreme Court is going to find a way to uphold the ACA as “constitutional”. You said, “not to worry!” God! I hate being right. (Almost as much as you hate being wrong!)

Anyway, I’m glad you are finally smelling the coffee which probably got to a stench with your latest health insurance premium increase. And, as such, this begs many questions – two of which I will address at this point:

(1) If the federal government cannot build a functional website, to insure the estimated 30 million uninsured, with 3 years lead time – How long is it going to take them to transition us to a “Medicare like” social welfare health insurance program that insures all 300 million plus Americans. And . . .

(2) If Social Security is on track to insolvency and Medicare is predicted to be insolvent by 2023 (nine years from now, people) – how the hell are they going to finance and subsidize healthcare for everyone? Redistribution. Because it wasn’t fair you’ve been so successful, Scott.

In my next blog post, I will address what I see as the specifics of why these things regarding the ACA are destined to transpire. In the meantime, I’m still going to Washington because the one thing we do know is – the person that never gets in the ring has already lost. The real issues I would like to confront our elected officials with are my suggestions for workable healthcare reform which guarantees coverage for pre-existing conditions while being financially responsible and feasible; term limits (I know, I know – when hell freezes over); amnesty and targeting of conservative groups by the IRS. I know they’ll try to get me back on point (theirs) – but not until I’ve made them say, “next question!”

If the administration and main stream media will not tell you–I will:

You can go through me–or any licensed health insurance agent or broker to acquire health insurance. NOW. And this is whether you qualify for a subsidy or not. And, importantly, there will be no, I repeat – $0 difference in your cost (premium) for doing so vs. the government website Healthcare.gov or a private insurance company’s. Period. Now where have you heard “Period” before and it turned out to be true? Well . . . in this case it is.

There is only ONE reason to go to the still basically inoperable, security in doubt, aforementioned federal government health insurance website known as The Marketplace:

1) You qualify for a subsidy of your 2014 health insurance premium and you would like to take advantage of that subsidy as you pay your premiums. I.e., you qualify and would like the premium you pay to your insurance company to be reduced by the amount of your subsidy as you pay the premium. (This as opposed to paying the gross premium (cost before your subsidy is applied) then declaring your subsidy on your 2014 tax return and having your tax liability reduced accordingly.)

If you this does not describe you – there is absolutely no reason to go to healthcare.gov!

Neither do you need to go through a state appointed, federally funded Navigator, hired by the State and required to complete only 20 hours of online education and be subjected to no background check. Why replicate and risk the possible insecurity of your personal information which includes your address; birth date; social security number and reported income by going through someone not even vetted by the Department of Health and Human Services (HHS) or the Center for Medicare Services (CMS)? As the Secretary for HHS, Kathleen Sebelius, admitted under oath and questioning from Texas Senator John Cornyn during Congressional, hearings just last week – “It is possible (for a convicted felon to be hired as a Navigator and take your personal and vital information).”

This begs the question: Why is the administration and main stream media not advertising, and barely mentioning, that a health insurance shopper can go through a licensed and vetted insurance agent who has passed a background check with every company with whom they are appointed and do so at no additional cost? Or that the shopper can then have all the expertise that that agent’s time in the industry (27 years in my case) brings to bear on their needs and situation? Or how about a “go to” advocate in their behalf they can call whenever there is an issue relating to claims; rates or general service related issues such as changes in address or dependents. This as opposed to a different unknown service rep at the end of a toll free number each time they call an insurance company directly?

I will let you speculate on the answers to these questions but (while the purpose of this blog is to educate the follower on issues relating to health and Medicare insurance) indulge me while I for once engage in a little shameless self-promotion on behalf of myself and all licensed agents and brokers:

If you reside in Texas; Indiana; or Ohio – please visit my website at http://allplaninsurance.com and click on the bold red “Get A Quote!” button on the home page or–better yet–call me toll free @ 800.856.6556 and let’s have an intelligent dialogue about your true wants and needs relative to coverage and then get some meaningful quotes and information for you. All without submitting the equivalent of a home mortgage application!

If you reside in any other state – do yourself a favor and call a well recommended licensed health insurance agent or broker in your community.

Again, call me even if you do qualify for a subsidy. I can help you just the same and–as without a subsidy–your cost for insurance will be the same. If you do not want to take the subsidy now but would rather take it on your 2014 tax return (when you actually know what your income will have been) we can apply for you now and have your coverage issued immediately.

If you want the subsidy applied upfront, to reduce the premium you pay each month, we will still have to enter the healthcare.gov website. But we will do so only after we have obtained your gross quotes via my website. I know the formula and can do a pretty fair job of estimating your net premium (after your subsidy is applied). If this scenario describes you, as the federal website is still inoperable, we should wait and see if HHS and CMS have the site fixed and secure by November 30th as promised. Let’s keep our fingers crossed and–if so–we should sail (wink, wink) through the application and have your coverage issued by January 1. But remember, if all government deadlines remain as now, we will need to complete your application no later than December 15th!

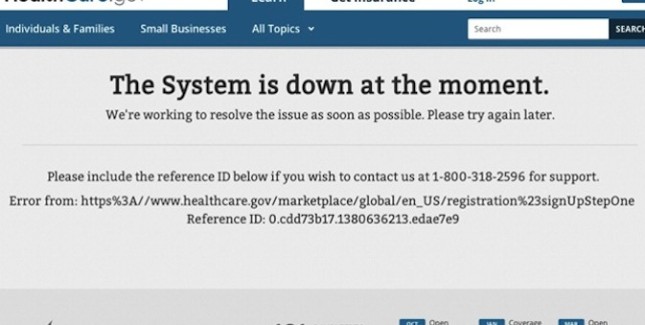

Well folks, here we are into the third week since the highly touted, much anticipated opening of the federal and state exchanges for purposes of enrolling in a health care act compliant insurance plan for 2014. And guess what? While a few state exchanges are experiencing some, generally small, measure of success – the federal exchange, or Marketplace, remains a dismal failure. It is, however, an excellent painful and protracted self-flagellating exercise in frustration. For an analogy–imagine having a root canal absent anesthesia while listening to Debbie Boone’s, “You Light Up My Life” on a continuous sound track loop through the entire procedure. Just to make the comparison more accurate, imagine you are Dustin Hoffman’s character who is tortured with a dentist’s drill in the movie Marathon Man but your experience is enhanced as your hygienist pulls your toe nails out with a pair of needle nose pliers in order to distract you from your oral discomfort. And that, I believe, is a pretty fair comparison to the enjoyment of opening an account and obtaining quotes for health insurance in the Marketplace to date. The tax payer’s cost to deliver this electronic equivalent of a Halloween visit to a House of Horrors? Current estimates are over $500 million and growing as desperate measures are being made to fix all its glitches as this goes to press. This after the Department of Health and Human Services accepted the low bid of $55 million with a ceiling of $93.7 million from Canadian software company, CGI Federal. Canadian? Really? All that U.S. taxpayer money to a Canadian firm? (I’m not even going there.)

But relax, dear patient. Let’s apply a little Novocain to your orifice. Let’s give you a subsidy to help ease the pain you will suffer when you see the highly inflated cost of health insurance you are now commanded to purchase under threat of penalty.

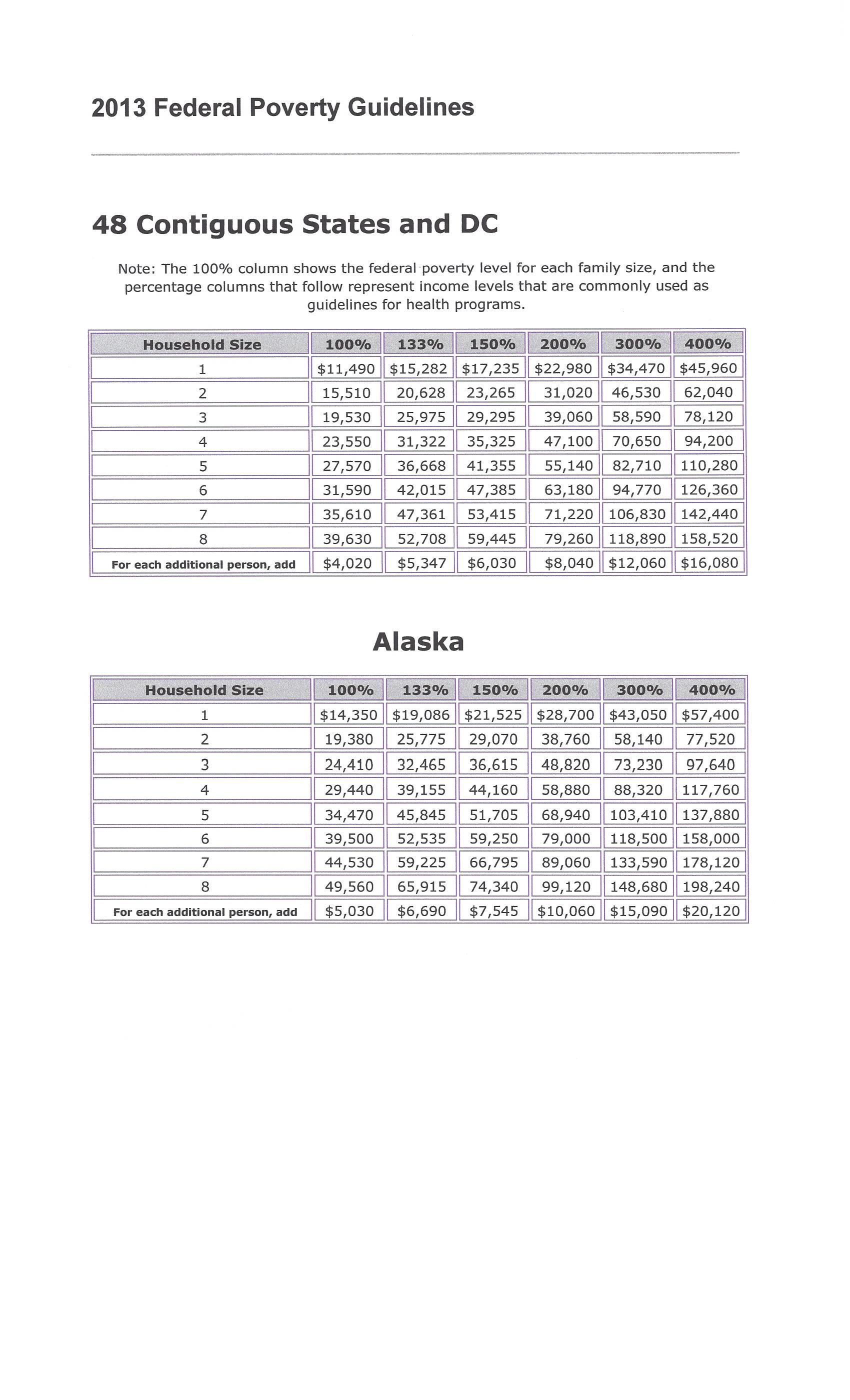

People making between 100 and 400 percent of federal poverty level can qualify for the premium tax credit health insurance subsidy. Federal poverty level changes every year, and is based on your income and family size.

Using 2013 FPL levels, you’ll qualify as an individual with an income range of $11,490-$45,960, a couple with an income of $15,510-$62,040, and a family of three earning $19,530-$78,120.

Just how do you calculate your subsidy?

In order to calculate how much your premium tax credit (subsidy) will be – you have to know 2 things:

(A) Your expected contribution toward the cost of your health insurance (available at the end of this article); and

(B) The cost of your BENCHMARK health plan. (Your health insurance exchange–assuming you succeed in opening an account and obtaining quotes–can tell you which plan this is and how much it costs. Your benchmark plan is the silver-tiered health plan with the second lowest monthly premiums in your area. The Affordable Care Act classifies health plans based on how much of your health care costs they’re expected to cover. A bronze health plan will cover about 60 percent of the average person’s health care costs. A silver health plan will cover about 70 percent.)

Your subsidy amount is the difference between your expected contribution and the cost of the benchmark plan. But just because the benchmark plan is used to calculate your subsidy doesn’t mean you have to buy the benchmark plan. You may buy any plan listed on your health insurance exchange, but your subsidy amount stays the same.

If you choose a more expensive plan, you’ll pay the difference plus your expected contribution. If you choose a plan that’s cheaper than the benchmark plan, you’ll pay less since the subsidy money will cover a larger portion of the monthly premium. If you choose a plan so cheap that costs less than your subsidy, you won’t have to pay anything for health insurance. However, you won’t get the excess subsidy back.

If you’re trying to save money so you choose a plan with a lower value, (like a bronze plan instead of a silver plan), you’ll likely have higher coinsurance and copays when you use your health insurance.

There’s another reason to choose a silver-tier plan. There’s a different subsidy that lowers copays, coinsurance, and deductibles for some low-income people. Eligible people can use it in addition to the premium tax credit subsidy. However, it’s only available to people who choose a silver-tier plan.

One question I am frequently asked is, “Do I have to wait until I file my income tax return in order to get the subsidy?”

Answer: “No”

You can get the premium tax credit in advance. If your income is so low you don’t have to file a tax return, you can still get the subsidy. But bear in mind–if you underestimate your income and take a subsidy–you will be forced to pay it back or, if you are due a refund, have it reduce such respectively when you file your return. (Income verification was put back in 2014 subsidy provisions after being suspended for one year along with the Administration’s one year suspension of the mandate that large employers must purchase health insurance for their employees. And remember–the IRS is in charge of monitoring your enrollment and expenditure.)

Consider opting to get the subsidy along with your tax refund if:

Your income is very close to 400 percent of FPL.

Your income varies from year to year so you’re not sure how much you’ll make.

When the subsidy is paid in advance, the amount of the subsidy is based on an estimate of your income for the coming year. If the estimate is wrong, the subsidy amount will be incorrect.

If you earn less than estimated, the advanced subsidy will be lower than it should have been. You’ll get the rest as a tax refund.

If you earn more than estimated, the government will send too much subsidy money to your health insurance company. You’ll have to pay back part or all of the excess subsidy money when you file your taxes. Even worse, if your actual income ended up more than 400 percent of FPL, you’ll have to pay back every penny of the subsidy. This could be thousands of dollars.

If you get your subsidy when you file your income taxes rather than in advance, you’ll get the correct subsidy amount because you’ll know exactly how much you earned that year. You won’t have to pay any of it back.

The Marketplace’s software will (supposedly) calculate your subsidy. Perhaps, as time goes by, it will even do so accurately. But for those of you who scored at least 600 on your high school SAT math test and enjoy such things – here is the exact formula for keeping the government honest:

Figure out how your income compares to FPL.

Find your expected contribution rate in the table below.

Calculate the dollar amount you’re expected to contribute.

Find your subsidy amount by subtracting your expected contribution from the cost of the benchmark plan.

Here is an example:

Mary is single with an income of $22,800 per year. FPL for 2013 is $11,490 for single people.

To figure out how Mary’s income compares to FPL, use: income ÷ FPL x 100.

$22,800 ÷ $11,490 x 100 = 198.4.

Mary’s income is 198 percent of FPL.

Using the table below, Mary is expected to contribute 4-6.3 percent of her income. Since she’s almost at the top of her category in the table, she uses the 6.3 percent figure.

To calculate how much Mary is expected to contribute, use this equation: 6.3 ÷ 100 x income.

6.3 ÷ 100 x $22,800 = $1,436.

Mary is expected to contribute $1,436 per year, or about $120 per month, toward the cost of her health insurance. The premium tax credit subsidy pays the rest of the cost of the benchmark health plan.

The benchmark health plan at Mary’s health insurance exchange costs $3,900 per year or $325 per month. Use this equation to figure out the subsidy amount: cost of the benchmark plan – expected contribution = amount of the subsidy.

$3,900 – $1,436 = $2,464.

Mary’s premium tax credit subsidy will be $2,464 per year or about $205 per month.

If Mary chooses the benchmark plan, or another $325 per month plan, she’ll pay $120 per month for her health insurance. If she chooses a plan costing $425 per month, she’ll pay $220 monthly for her health insurance. If she chooses a plan costing $225 per month, she’ll only pay $20 per month for her health insurance.

FEDERAL POVERTY LIMIT BASED ON NUMBER OF FAMILY IN HOUSEHOLD:

(Click on image to enlarge.)

Table of Your Expected Contribution Percentage:

If your income is

Your expected contribution will be

100%-133% of FPL

2% of your income

133%-150% of FPL

3%-4% of your income

150%-200% of FPL

4%-6.3% of your income

200%-250% of FPL

6.3%-8.05% of your income

250%-300% of FPL

8.05%-9.5% of your income

300%-400% of FPL

9.5% of your income

I hope your weather is not as beautiful as it is here in my part of Texas on this Sunday afternoon. If so, you are probably regretting you took the time to get this far into this hopefully informative piece. If it is – do not blame me and certainly–do not shoot the messenger.

As for me, I’m getting out on my motor bike and will take my mind off this monumental cross I bear being . . .

The Healthcare.gov website requires that individuals looking for coverage enter personal information before comparing plans. IT experts believe that this requirement is causing the website to crash.

A growing consensus of IT experts, outside and inside the government, have figured out a principal reason why the website for Obamacare’s federally-sponsored insurance exchange is crashing. Healthcare.gov forces you to create an account and enter detailed personal information before you can start shopping. This, in turn, creates a massive traffic bottleneck, as the government verifies your information and decides whether or not you’re eligible for subsidies. HHS bureaucrats knew this would make the website run more slowly. But they were more afraid that letting people see the underlying cost of Obamacare’s insurance plans would scare people away.

HHS didn’t want users to see Obamacare’s true costs

“Healthcare.gov was initially going to include an option to browse before registering,” report Christopher Weaver and Louise Radnofsky in the Wall Street Journal. “But that tool was delayed, people familiar with the situation said.” Why was it delayed? “An HHS spokeswoman said the agency wanted to ensure that users were aware of their eligibility for subsidies that could help pay for coverage, before they started seeing the prices of policies.” (Emphasis added.)

As you know if you’ve been following this space, Obamacare’s bevy of mandates, regulations, taxes, and fees drives up the cost of the insurance plans that are offered under the law’s public exchanges. A Manhattan Institute analysis I helped conduct found that, on average, the cheapest plan offered in a given state, under Obamacare, will be 99 percent more expensive for men, and 62 percent more expensive for women, than the cheapest plan offered under the old system. And those disparities are even wider for healthy people.

That raises an obvious question. If 50 million people are uninsured today, mainly because insurance is too expensive, why is it better to make coverage even costlier?

Political objectives trumped operational objectives

The answer is that Obamacare wasn’t designed to help healthy people with average incomes get health insurance. It was designed to force those people to pay more for coverage, in order to subsidize insurance for people with incomes near the poverty line, and those with chronic or costly medical conditions.

But the laws’ supporters and enforcers don’t want you to know that, because it would violate the President’s incessantly repeated promise that nothing would change for the people that Obamacare doesn’t directly help. If you shop for Obamacare-based coverage without knowing if you qualify for subsidies, you might be discouraged by the law’s steep costs.

So, by analyzing your income first, if you qualify for heavy subsidies, the website can advertise those subsidies to you instead of just hitting you with Obamacare’s steep premiums. For example, the site could advertise plans that cost “$0″ or “$30″ instead of explaining that the plan really costs $200, and that you’re getting a subsidy of $200 or $170. But you’ll have to be at or near the poverty line to gain subsidies of that size; most people will either not qualify for a subsidy, or qualify for a small one that, net-net, doesn’t make up for the law’s cost hikes.

This political objective—masking the true underlying cost of Obamacare’s insurance plans—far outweighed the operational objective of making the federal website work properly. Think about it the other way around. If the “Affordable Care Act” truly did make health insurance more affordable, there would be no need to hide these prices from the public.

Subsidy verification created a traffic bottleneck

Comparable private-sector e-commerce sites, like eHealthInsurance.com, allow you to shop for plans and compare prices simply by entering your age and your ZIP code. After you’ve selected a plan you like, you fill out an on-line application. That substantially winnows down the number of people who rely on the site for network-intensive tasks.

The federal government’s decision to force people to apply before shopping, Weaver and Radnofsky write, “proved crucial because, before users can begin shopping for coverage, they must cross a busy digital junction in which data are swapped among separate computer systems built or run by contractors including CGI Group Inc., the healthcare.gov developer, Quality Software Services Inc., a UnitedHealth Group Inc. unit; and credit-checker Experian PLC. If any part of the web of systems fails to work properly, it could lead to a traffic jam blocking most users from the marketplace.”

Jay Angoff, a former federal official at the agency that oversees the exchange, told the Journal that he was surprised by the decision. “People should be able to get quotes” without entering all of that information upfront.

Weaver and Radnofsky say that the core problem stems from “the slate of registration systems [that] intersect with Oracle Identity Manager, a software component embedded in a government identity-checking system.” The main Healthcare.gov web page collects information using the CGI Group technology. Then that data is transferred to a system built by Quailty Software Services. QSS then sends data to Experian, the credit-history firm. But the key “identity management system” employed by QSS was designed by Oracle, and according to the Journal’s sources, the Oracle software isn’t playing nicely with the other information systems.

Oracle hotly denies these claims. “Our software is the identical product deployed in most of the world’s most complex systems…our software is running properly,” said an Oracle spokeswoman in a statement.

‘It’s awful, just awful’

Robert Pear and colleagues at the New York Times have a piece up today detailing the serious problems with the federal exchange, problems that may get worse, not better. They confirm what we already knew: that the Obama administration refused to delay the implementation of the exchanges, despite the well-known problems, because they were afraid of the political blowback. “Former government officials say the White House, which was calling the shots, feared that any backtracking would further embolden Republican critics who were trying to repeal the health care law.”

As I documented last week, IT and insurance experts have been saying for at least eight months that implementation of the exchanges was going badly, that as early as February officials were warning of a “third world experience.” The Times’ sources are just as blunt. “These are not glitches,” said one insurance executive. “The extent of the problems is pretty enormous. At the end of our [conference calls with the administration], people say, ‘It’s awful, just awful.’”

“We foresee a train wreck,” said another executive in a February interview with the Times. “We don’t have the IT specifications. The level of angst in health plans is growing by leaps and bounds. The political people in the administration do not understand how far behind they are.” Richard Foster, the former chief actuary at the Centers for Medicare and Medicaid Services, said last week that “so much testing of the new system was so far behind schedule, I was not confident it would work well.”

Henry Chao, the deputy chief information officer at CMS who made the “third world experience” comment, was told by his superiors that failure to meet the October 1 launch deadline “was not an option,” according to the Times.

White House knowingly chose to court disaster

Think about it. It’s quite possible that much of this disaster could have been avoided if the Obama administration had been willing to be open with the public about the degree to which Obamacare escalates the cost of health insurance. If they had, then a number of the problems with the exchange’s software architecture would never have arisen. But that would require admitting that the “Affordable Care Act” was not accurately named.

The White House knew that its people on the front lines, people like Henry Chao, were worried that the exchanges would get botched. They saw the Congressional Research Service memorandum detailing that the administration has missed half of the statutory deadlines assigned by the law. But they were more afraid of the P.R. disaster of disclosing Obamacare’s high premiums than they were of the P.R. disaster of crashing websites. What you see is the result.

************************

Tech experts: Health exchange site needs total overhaul

Kelly Kennedy, USA TODAY 5:36 p.m. EDT October 17, 2013Health and Human Services Secretary Kathleen Sebelius calls the rollout of the health care exchanges rocky. (Photo: Jose Luis Magana, AP)

WASHINGTON — The federal health care exchange was built using 10-year-old technology that may require constant fixes and updates for the next six months and the eventual overhaul of the entire system, technology experts told USA TODAY.

The site could be perfect, but if the systems from which it draws data are not up to speed, it doesn’t matter, said John Engates, chief technology officer at Rackspace, a cloud computer service provider.

“It is a core problem in the sense of it’s fundamental to this thing actually working, but it’s not necessarily a problem that the people who wrote HealthCare.gov can get to,” Engates said. “Even if they had a perfect system, it still won’t work.”

Recent changes have made the exchanges easier to use, but they still require clearing the computer’s cache several times, stopping a pop-up blocker, talking to people via Web chat who suggest waiting until the server is not busy, opening links in new windows and clicking on every available possibility on a page in the hopes of not receiving an error message. With those changes, it took one hour to navigate the HealthCare.gov enrollment process Wednesday.

“I have never seen a website — in the last five years — require you to delete the cache in an effort to resolve errors,” said Dan Schuyler, a director at Leavitt Partners, a health care group by former Health and Human Services secretary Mike Leavitt. “This is a very early Web 1.0 type of fix.”

“The application could be fundamentally flawed,” said Jeff Kim, president of CDNetworks, a content-delivery network. “They may be using 1990s technology in 2.0 world.”

Outsiders acknowledged they can’t see the whole system, but they said they feared HHS built a system that will need an expensive overhaul that would cause more headaches for people trying to buy insurance.

“I will be the first to tell you that the website launch was rockier than we wanted it to be,” HHS Secretary Kathleen Sebelius said Wednesday at Cincinnati State Technical and Community College, adding that people have until Dec. 15 to enroll to ensure coverage beginning Jan. 1.

HHS officials did not respond to a request about the nature of the problems. However, they reiterated that wait times have been reduced or even eliminated as they continue to work to fix the system. As of Thursday, the site had received 17 million unique visitors.

“We continue to work around the clock to improve the consumer experience on HealthCare.gov,” HHS spokeswoman Joanne Peters said. “We are seeing progress: wait times to begin the online process have been virtually eliminated, and more consumers are creating accounts, completing applications and ultimately enrolling in coverage if they choose to do so at this time. However, we will not stop addressing issues and improving the system until the doors to HealthCare.gov are wide open.”

Engates said HHS has been opaque about the problems, and the tech industry doesn’t know the extent of the issues. “There’s no secrets leaking out,” he said. “I’m sure everyone’s looking for something to change the direction of the conversation, but it’s just not there.”

“I think it’s a data problem,” Kim said. “It always comes down to that.”

And if that’s the case, the problems are beyond “rocky,” he said. Instead, it would require a “fundamental re-architecture.” In the meantime, “I think they’re just trying to shore up as quickly as possible. They don’t have time to start from scratch.”

“If I was them, and I’m just conjecturing, I would probably come up with some manual way of saying, ‘Only people with the last name starting with ‘A’ can sign up today,” he said.

But come March 31, when the first enrollment period ends, the “shore up” period may become a “re-architecting” period, Kim said.

On a good note, he said, after looking at available code, the site is “very secure.”

Clearing the cache, which has helped make it easier for some people to enroll, could ultimately strain the system more, Kim said. That’s because a “cookie” is stored on a person’s computer that contains data, such as the person’s name and address, that can then be quickly accessed when that person gets on the website again instead of having to be retrieved from the government’s server.

But as HHS fixes errors, the cookies may not correspond with the updated website, so rather than allowing someone to quickly log in, they instead cause an error message. And every time a person clears his computer’s cache, the government’s website has to work that much harder to grab more data.

Requiring people who may not be Web savvy to use the site in any way other than a step-by-step easy process defeats the point of the whole system, Schuyler said. That includes laws mandating that insurers provide clear explanations about policies to people may make sound decisions and understand what they’re buying.

“Most consumers will have no idea what ‘clearing the cache’ is and this will just cause more confusion and frustration,” he said.

So far, the site’s problems have not driven away potential customers, according to a poll conducted by uSamp — United Sample Inc. The survey found that among the 832 people who attempted to log in, 38% received an error message, 50% were asked to try again later, 25% were unable to create an account, 31% were told the system was down, and 19% had no problems. About 83% said they would try again later, while 15% said they would wait until they heard the website was working well. About 70% of those who said they had no issues said they still waited to enroll because they want to think about their options.

Engates said he believes most of the problems are caused by systems integration with other sites, such as the IRS. And that could be causing some of the problems people see as they make it past the initial application process. It’s a series of questions meant to verify a person’s identity and income. But after that questionnaire, visitors often encounter a series of error messages, or the page a person tries to click to doesn’t come up. The data requests to other sites could be causing those problems, Engates said, which would mean the problem isn’t with the HHS site itself.

“Maybe the site is submitting a request for more data, and that puts you in that trap again,” he said. “It’s a giant integration problem that they have to solve.”

And as they try to fix those problems, there’s another issue lurking in the background: Some HHS personnel were named essential, and not subject to furloughs because of the government shutdown. But that didn’t apply to the other organizations they were working with, Engates said. So as HHS techs work around the clock to fix the problems, IRS techs may be prohibited from working at all.

In the meantime, HHS personnel can’t say anything about the situation, it can be played politically as “bad,” he said. If they say it will take two weeks to fix, they will be criticized because it’s taking too long. But he expects that it’s a problem that will be resolved soon, especially as the volume of visitors goes down.

“If you can get the system below some sort of threshold, it will perform as it’s supposed to,” Engates said. “It won’t get any worse. It’s going to get better little by little by little.”

As a licensed agent in Texas, Indiana, Ohio and Michigan I am certified with the Department of Health and Human Service through the Center for Medicare Service to enroll residents of those states in health insurance plans for 2014. This is whether they qualify for a subsidy or not. Premiums are the same whether you go through me, the Marketplace (Federal Exchange) or a Navigator. And I would like to assist you. Problem is – 5 days into the enrollment phase of the Affordable Care Act (ACA) I still have not succeeded in being able to create even my own account to see what all my options are. I have seen many of my options outside the Marketplace–in the private market–and my quoted premium is approximately 33% higher than my current premium for comparable coverage! I have read all news articles relative to enrollment numbers and although the White House says people are enrolling in the Marketplace (which is where residents of these states go for quotes unless coming to me) and–as of yesterday–no journalist has been successful in finding and interviewing one individual who has successfully purchased health insurance in the Marketplace! One individual, Chad Henderson, reported he and his father had but when swarmed by journalist and asked for details – his father said neither he or his son had. Turns out Chad was a campaign worker for the Obama administration last year and an active volunteer for Organizing for Action, the former campaign organization that now advocates for the President’s legislative agenda. You figure it out. This much I know – if you already know that based on your estimated income for 2014 you will not qualify for a subsidy – you should apply for coverage through me and avoid the wait (however long) on the Marketplace website. You can see your options and go directly into your chosen health insurance companies application for the plan you select.

If, ultimately, you qualify for a subsidy – you may be relatively satisfied with your premium but it looks like (in order for that to be the case) you will have to accept a deductible much higher than what you anticipated. If you do not qualify for a subsidy – prepare for what in all likelihood will be sticker shock.

Regardless, I have made about 15 unsuccessful attempts, consuming hours of wait time the last 5 days to open an account in the Marketplace and–for research purposes– obtain my own quotes and see what subsidy options look like. Even Chad Henderson claimed it took him 3 hours to create an account–and this allegedly took place at 3 a.m. in the morning! How am I supposed to take my clients who will qualify for a subsidy from my quoting engine into the online Marketplace and have us succeed in staying with each other while we wait hours for us to set up their account? Of course, these wait times will surely decrease over time, right? Errrrr . . . right?

UPDATED at 2.54pm ET:Scroll to end of this article for the latest development in this story. After speaking directly with Chad Henderson, The Washington Post has confirmed that he has not in fact enrolled in a health-care plan.

Chad Henderson is the media’s poster boy for Obamacare. Reporters struggled this week to find individuals who said they had been able to enroll in one of the law’s 36 federally run health-insurance exchanges.

That changed yesterday, when they found Henderson, a 21-year-old student and part-time child-care worker who lives in Georgia and says that he successfully enrolled himself and his father Bill in insurance plans via the online exchange administered at healthcare.gov.

But in an exclusive phone interview this morning with Reason, Chad’s father Bill contradicted virtually every major detail of the story the media can’t get enough of. What’s more, some of the details that Chad has released are also at odds with published rate schedules and how Obamacare officials say the enrollment system works.

The coverage of Chad Henderson has been massive. He was featured in The Washington Post Thursday as “the Obamacare enrollee that tons of reporters are calling.” He was also profiled in The Huffington Post as someone who “beat the glitches to sign up for Obamacare.” He was interviewed by Politico, multiple local news organizations, and, according to his Facebook feed, was asked to be part of a conference call hosted by the Department of Health and Human Services.

Chad’s story was tweeted out by the official Obamacare Twitter feed. It was promoted to the media by Enroll America, a health-care activist group headed by a former White House communications staffer, as a sign of Obamacare’s success. Henderson told reporters at multiple news outlets that after a three-hour wait to sign up online, he enrolled around 3 a.m. Tuesday morning in an unsubsidized private insurance plan that would cost him about $175 a month. He also said that his father enrolled in separate coverage plan that would cost about $250 a month after factoring in the subsidies for which his father qualified on his approximately $24,000 annual income.

Chad’s decision to purchase his own, separate plan might surprise some.A monthly premium of $175 would represent about 30 percent of his pre-tax take home pay—about $583 a month on the $7,000 part-time income he claimed. And he could have chosen to be covered by his father’s plan, which, under the Affordable Care Act, would have been required to cover dependents up to the age of 26. Chad said his father encouraged him to be covered under his own plan, even though the cost was higher. “He’s old school, so he wants me to take responsibility,” Chad toldThe Huffington Post.

Henderson’s story was promoted as proof that the new health law can work for individuals. That was exactly how Chad intended it. He was a volunteer with President Obama’s campaign last year, and his LinkedIn page still lists him as an active volunteer with Organizing for Action, the former campaign organization which now advocates for the president’s legislative agenda.

He told The Washington Post that he was sharing his story because he wanted the new health law to succeed.

“I’ve read a few articles about how young people are very critical to the law’s success,” he said to The Post. “I really just wanted to do my part to help out with the entire process.”

But details of Chad’s story proved difficult to verify. And in a phone interview conducted this morning, Chad’s father Bill contradicted major details of Chad’s story. I reached Bill Henderson by following a series of links at Chad’s Facebook page, through which I was able to speak directly to the father.

Bill Henderson told me that both he and his son were interested in getting coverage, but that he had not enrolled in any plan yet, and to his knowledge, neither had his son. He also said that when they do enroll, getting the most coverage for the least money would be the goal, and that he expects that he and his son will get coverage under the same plan.

Bill told me that Chad had been looking into plans online. “He told me that there’s different plans. And we haven’t decided which plans to enroll in yet.”

I asked him whether he and his son had talked about going on separate plans, and he told me that, “We’ll probably go on the same plan, more than likely.”

I have just completed my Affordable Care Act (ACA) training and certification in order to offer ACA compliant plans to my clients, and the public in general, beginning October 1. However, even in this final hour with only eight days until the new plans are to be available – the insurance companies have still not released the premiums the insure will pay for these options. “Any day now” is what I am being told. However, I will share with you a thing or two I do know based on what I have studied.

Most of it came as no surprise to me. One major company (whose name I cannot divulge as the information they provided was yet to be approved by the Department of Health and Human Services (HHS) who will be in charge of the Federal-Run Exchange–Marketplace–in Texas, Indiana and Ohio–where I have clients) previewed plans. The lowest plan deductible available was $1,500. All plans will be limited to a maximum out-of-pocket of $6,350 per individual and $12,700 per family. While older people will probably find a $1,500 deductible acceptable in terms of affordability, I am not certain how twenty year olds are going to feel about that. I certainly don’t think that and higher deductible options will be an incentive for them to enroll even with the convenience of doctor’s office co-pays and prescription drug cards. I can almost guarantee you that unless they receive a subsidy – they won’t be signing up.

Beyond that, the benefits sounded perfectly acceptable until I came to the part about “special care centers”. It turns out, at least with this company (which happens to be a very large, conspicuous player in the Texas health insurance market we’ll just refer to as company XYZ)when you are in need of a special surgical procedure such as a hip or knee replacement: “You may only receive one by going to an ‘XYZ Approved Hip and Knee Replacement Center'”. I have had a hip replacement and had it at the relatively young age of 49 and I don’t know about you but I didn’t want just anyone performing mine. I still had dreams of remaining very active and athletic to the point of partaking in very aggressive martial arts training among other activities such as mountain biking. Fortunately, I have been able to do so but would I had I gone to some “Preferred” (discount) provider who agreed to accept lesser fees for greater patient volume?

To underscore my concern relative to an obvious attempt to ration our selection of providers, if not the procedures themselves, I received an email today informing me the primary Medicare Advantage Plan I enrolled my clients in last year is having an inordinate number of Primary Care Physicians drop out of its network and that I should be prepared to re-shop their Advantage Plan. The problem is, if this very large nationally recognized plan is experiencing this kind of “provider drop-out” – what can I expect from smaller companies with less capital? Again, I have had to delete their name as the information was proprietary and for “agent use only” but the letter they sent their clients is attached below. If you are one of my current Medicare clients I placed with this plan – you may have already read this. Otherwise, I apologize for breaking the news to you like this.

Our feature article appeared in today’s New York Times (September 23rd) and describes how patient options will be restricted as a result of the ACA. Think about it. If the insurance companies have no choice in who they insure and must cover any and all pre-existing conditions . . . and if they are informed by the Department of Health and Human Services their profit and, more specifically, the ratio of claims they must pay relative to the premium they take in, i.e., 80% to 20% – how else can they manage losses except to restrict access to procedures, providers and what your providers are paid? Something had to give.

At ————- , we manage the physician networks for our plans to help meet the evolving needs of health care consumers. This includes adjusting the size and composition of our physician network as we strive to meet the specific needs of Medicare Advantage and/or Medicaid plan members.

As a result, in the coming months, select physicians for one or more of your Medicare Advantage and/or Medicaid members will no longer participate in our Medicare and Medicaid plan networks. Please note: these changes do not affect members enrolled in Medicare Supplement or commercial plans.

Member transitions We know that members are impacted when we make changes to our network, and are taking steps to support members with smooth transitions to new care providers as appropriate to help ensure continuity of care.

We will be sending letters to affected members to notify them of care providers that will no longer participate in the —————– Medicare and Medicaid plan network as early as January 1, 2014 (network changes for New Jersey Medicaid plans have an October, 2013 effective date.) When appropriate, letters will suggest new care providers for members to consider for their ongoing care. Members are encouraged to call the number on their member ID card if they need help with identifying a new care provider.

In some plans, members may choose to continue seeing their current care providers on an out-of-network basis, in accordance with their out-of-network benefits. These changes have no impact on plan benefits, and members undergoing a treatment plan will be able to continue seeing out-of-network care providers consistent with federal requirements.

Provider directories These network changes will be reflected in our online provider directory as of October 1, 2013. It is highly encouraged to refer to the online provider directory in all cases to confirm care provider network and panel status for all potential enrollees, as changes may not be reflected in previously printed and/or downloaded directories.

It is important to note that when searching for an in-network provider on the online directory, a provider’s “Accepting New Patients” status must indicate “OPEN“, even if the potential enrollee is an existing patient.

WASHINGTON — Federal officials often say that health insurance will cost consumers less than expected under President Obama’s health care law. But they rarely mention one big reason: many insurers are significantly limiting the choices of doctors and hospitals available to consumers.

From California to Illinois to New Hampshire, and in many states in between, insurers are driving down premiums by restricting the number of providers who will treat patients in their new health plans.

When insurance marketplaces open on Oct. 1, most of those shopping for coverage will be low- and moderate-income people for whom price is paramount. To hold down costs, insurers say, they have created smaller networks of doctors and hospitals than are typically found in commercial insurance. And those health care providers will, in many cases, be paid less than what they have been receiving from commercial insurers.

Some consumer advocates and health care providers are increasingly concerned. Decades of experience with Medicaid, the program for low-income people, show that having an insurance card does not guarantee access to specialists or other providers.

Consumers should be prepared for “much tighter, narrower networks” of doctors and hospitals, said Adam M. Linker, a health policy analyst at the North Carolina Justice Center, a statewide advocacy group.

“That can be positive for consumers if it holds down premiums and drives people to higher-quality providers,” Mr. Linker said. “But there is also a risk because, under some health plans, consumers can end up with astronomical costs if they go to providers outside the network.”

Insurers say that with a smaller array of doctors and hospitals, they can offer lower-cost policies and have more control over the quality of health care providers. They also say that having insurance with a limited network of providers is better than having no coverage at all.

Cigna illustrates the strategy of many insurers. It intends to participate next year in the insurance marketplaces, or exchanges, in Arizona, Colorado, Florida, Tennessee and Texas.

“The networks will be narrower than the networks typically offered to large groups of employees in the commercial market,” said Joseph Mondy, a spokesman for Cigna.

The current concerns echo some of the criticism that sank the Clinton administration’s plan for universal coverage in 1993-94. Republicans said the Clinton proposals threatened to limit patients’ options, their access to care and their choice of doctors.

At the same time, House

Republicans are continuing to attack the new health law and are threatening to hold up a spending bill unless money is taken away from the health care program.

Dr. Bruce Siegel, the president of America’s Essential Hospitals, formerly known as the National Association of Public Hospitals and Health Systems, said insurers were telling his members: “We don’t want you in our network. We are worried about having your patients, who are sick and have complicated conditions.”

In some cases, Dr. Siegel said, “health plans will cover only selected services at our hospitals, like trauma care, or they offer rock-bottom payment rates.”

In New Hampshire, Anthem Blue Cross and Blue Shield, a unit of WellPoint, one of the nation’s largest insurers, has touched off a furor by excluding 10 of the state’s 26 hospitals from the health plans that it will sell through the insurance exchange.

Christopher R. Dugan, a spokesman for Anthem, said that premiums for this “select provider network” were about 25 percent lower than they would have been for a product using a broad network of doctors and hospitals.

Anthem is the only commercial carrier offering health plans in the New Hampshire exchange.

Peter L. Gosline, the chief executive of Monadnock Community Hospital in Peterborough, N.H., said his hospital had been excluded from the network without any discussions or negotiations.

“Many consumers will have to drive 30 minutes to an hour to reach other doctors and hospitals,” Mr. Gosline said. “It’s very inconvenient for patients, and at times it’s a hardship.”

State Senator Andy Sanborn, a Republican who is chairman of the Senate Commerce Committee, said, “The people of New Hampshire are really upset about this.”

Many physician groups in New Hampshire are owned by hospitals, so when an insurer excludes a hospital from its network, it often excludes the doctors as well.

David Sandor, a vice president of the Health Care Service Corporation, which offers Blue Cross and Blue Shield plans in Illinois, Montana, New Mexico, Oklahoma and Texas, said: “In the health insurance exchange, most individuals will be making choices based on costs. Our exchange products will have smaller provider networks that cost less than bigger plans with a larger selection of doctors and hospitals.”

Premiums will vary across the country, but federal officials said that consumers in many states would be able to buy insurance on the exchange for less than $300 a month — and less than $100 a month per person after taking account of federal subsidies.

“Competition and consumer choice are actually making insurance affordable,” Mr. Obama said recently.

Many insurers are cutting costs by slicing doctors’ fees.

Dr. Barbara L. McAneny, a cancer specialist in Albuquerque, said that insurers in the New Mexico exchange were generally paying doctors at Medicare levels, which she said were “often below our cost of doing business, and definitely below commercial rates.”

Outsiders might expect insurance companies to expand their networks to treat additional patients next year. But many insurers see advantages in narrow networks, saying they can steer patients to less expensive doctors and hospitals that provide high-quality care.

Even though insurers will be forbidden to discriminate against people with pre-existing conditions, they could subtly discourage the enrollment of sicker patients by limiting the size of their provider networks.

“If a health plan has a narrow network that excludes many doctors, that may shoo away patients with expensive pre-existing conditions who have established relationships with doctors,” said Mark E. Rust, the chairman of the national health care practice at Barnes & Thornburg, a law firm. “Some insurers do not want those patients who, for medical reasons, require a broad network of providers.”

In a new study, the Health Research Institute of PricewaterhouseCoopers, the consulting company, says that “insurers passed over major medical centers” when selecting providers in California, Illinois, Indiana, Kentucky and Tennessee, among other states.

“Doing so enables health plans to offer lower premiums,” the study said. “But the use of narrow networks may also lead to higher out-of-pocket expenses, especially if a patient has a complex medical problem that’s being treated at a hospital that has been excluded from their health plan.”

In California, the statewide Blue Shield plan has developed a network specifically for consumers shopping in the insurance exchange.

Juan Carlos Davila, an executive vice president of Blue Shield of California, said the network for its exchange plans had 30,000 doctors, or 53 percent of the 57,000 doctors in its broadest commercial network, and 235 hospitals, or 78 percent of the 302 hospitals in its broadest network.

Mr. Davila said the new network did not include the five medical centers of the University of California or the Cedars-Sinai Medical Center near Beverly Hills.

“We expect to have the broadest and deepest network of any plan in California,” Mr. Davila said. “But not many folks who are uninsured or near the poverty line live in wealthy communities like Beverly Hills.”

Daniel R. Hawkins Jr., a senior vice president of the National Association of Community Health Centers, which represents 9,000 clinics around the country, said: “We serve the very population that will gain coverage — low-income, working class uninsured people. But insurers have shown little interest in including us in their provider networks.”

Please correct me if I am wrong, but I recall that ever since President Obama took office in 2009–in the midst of the housing crisis; failed savings and loans and with the legacy of Enron still looming fresh in the memories of stockholders everywhere– he has said more government regulation through stricter laws and scrutiny (among a host of other burdensome and expensive supposed remedies) was necessary to protect the consumer and public in general. Now–in a narrative of unabashed hypocrisy his administration speaks out and intervenes to prevent Texas’s Governor Rick Perry from doing that very thing.

Perry directed the Texas Department of Insurance to establish strict rules to regulate Navigators trained to help Texans purchase health insurance under the Affordable Care Act (ACA). (These rules are outlined in our feature article below.) Remember – when you go through one these Navigators to enroll in an ACA compliant health plan for an effect date of January 1 – you will be required to divulge your income; your birth date; social security number; address; credit card and checking account information. Do you really want just anyone taking this information? Do you really want the person taking it to not be subject to criminal and financial background checks? Insurance agents licensed in the State of Texas are subject to all these requirements. Why would the administration which always argues for more protection of the individual from the misfeasance, malfeasance and just plain greed of the big corporations, e.g., health insurance companies – now be opposed to such? Why is this regulation so suddenly a liability? Please weigh in and help me understand this. The arguments presented by the fed below do not.

Admin. – Kenton Henry

****************************************************

Feature Article The Texas Tribune Wednesday, September 18, 2013 Perry Directs TDI to Regulate Federal Navigator Program

Gov. Rick Perry has directed the Texas Department of Insurance to establish strict rules to regulate so-called navigators trained to help Texans purchase health coverage under Obamacare.

While the governor says the extra regulations will ensure that people handling Texans’ private financial and health information are properly trained and qualified, the rules could present a significant roadblock to organizations helping to implement the federal Affordable Care Act.

“This is blatant attempt to add cumbersome requirements to the navigator program and deter groups from working to inform Americans about their new health insurance options and help them enroll in coverage,” Fabien Levy, a spokesman for the U.S. Department of Health and Human Services, said in an email.

Along with many other provisions in President Obama’s signature health reform law, the individual mandate to purchase health insurance is set to take effect on Jan. 1. Texas’ Republican majority, which vehemently opposes the federal health law, declined to establish a state-based insurance marketplace. The federal government is doing it instead, launching an Orbitz-like online insurance exchange starting Oct. 1. That exchange will require individuals to input sensitive tax information, including their Social Security numbers and estimated annual income, to determine whether they qualify for tax credits to purchase coverage.

To help uninsured Texans use the complicated new system, the federal government awarded nearly $11 million in August to local organizations charged with hiring and training navigators, who will help consumers input their financial information and pick a health plan through in the exchange, must undergo 20 to 30 hours of training, pass a certification test and renew their certification annually, according to the U.S. Department of Health and Human Services.

For Perry, those ground rules are not enough.

“The U.S. Department of Health and Human Services has repeatedly delayed explaining how its navigators were going to be created, how they were going to operate and how they were going to be regulated,” Perry wrote in a letter to Insurance Commissioner Julia Rathgeber. “Because of the nature of navigators’ work and because they will be collecting confidential information, including birth dates, social security numbers and financial information, it is imperative that Texas train navigators on the collection and security of such data.”

In the letter, Perry specifically directed TDI to establish rules that require navigators to complete at minimum of 40 hours of state training in addition to the federal training requirements. He also demanded that navigators pass a rigorous exam based on that training, refrain from influencing a consumer’s insurance choice by recommending a specific plan or comparing benefits offered by different plans, and submit to periodic background and regulatory checks and show state identification while on the job.

He also directed TDI to maintain a database of registered navigators, including background checks and fingerprints; set limits on when and where navigators can enroll people in the exchange; charge fees to provide navigator training and registration; and establish the department’s authority to suspend or revoke navigators’ registration for failing to comply with state requirements.

“TDI agrees that the navigators in Texas have to be well trained and competent in what they’re doing,” said Ben Gonzalez, an agency spokesman. “Our goal is for them to be accountable and be conscientious about the confidential information that they’re going to be collecting.”

Federal officials said some of the rules Perry ordered the state insurance department to implement are forbidden under U.S. law. For example, navigators are not allowed to retain or report information on consumers who sign up for coverage through the exchange; therefore, they could not submit that information to TDI, as Perry has requested. The federal agency also emphasized that navigators are not allowed to access consumers’ information after it has been submitted to the exchange.

Levy said the U.S. government has similar programs already set up to help counsel people applying for Medicare, and that those have “never faced this kind of bullying from Texas.”

“This is clearly an ideologically-driven attempt to prevent the uninsured from gaining health coverage,” Levy said. “But despite the state’s attempts, we are confident that navigators will still be able to help Texans enroll in quality, affordable health coverage when open enrollment begins on Oct. 1.”

Given the governor’s directive, the department will begin putting together the rules with some urgency, Gonzalez added. The rule-making process can take several weeks, as the state is required to hold public meetings and solicit stakeholder input before the rules are drafted. After a draft is approved, the rules must be posted on the Texas Register to receive official comment before they can be codified.

“It’s our expectation the rules and training be in place by Jan. 1, when insurance can be purchased through the exchange,” Rich Parsons, a spokesman for the governor’s office, said via email.

The federal health exchange has a six-month open enrollment period — from Oct. 1 to March 31 — in which navigators can help the uninsured find health coverage to comply with the insurance mandate. Individuals who do not purchase insurance during the open enrollment period could be subject to federal tax penalties. If the state’s regulations take effect on Jan. 1, the navigators will be required to undergo additional training during the open enrollment period, which could present significant challenges.

To address the privacy concerns raised about the navigator program, some grant recipients are already requiring navigators to undergo additional training on privacy protection. United Way of Tarrant County, in collaboration with 17 other organizations, received $5.8 million, the largest federal navigator grant in Texas. Tim McKinney, the organization’s chief executive officer, said the organization is requiring navigators to undergo an additional hour-and-a-half of training on how to comply with the federal privacy law HIPAA.

Lawmakers signed off on Perry’s call for greater regulation of the navigator program in the last legislative session when they passed Senate Bill 1795, which authorizes TDI “to regulate navigators if it determined that federal standards did not ensure they were qualified to perform their duties or avoid conflicts of interest,” according to a legislative report. The new state law allows the department to enact rules that protect patient privacy and prohibit navigators from accepting payments from health insurance companies or posing as an insurance agent. At least 16 other states have also enacted or are considering laws to regulate navigators, according to a USA Today report.

Texas Attorney General Greg Abbott and 12 other state attorneys general have also raised concerns that the federal navigator program could pose risks to patients’ privacy. In a letter sent to U.S. Health and Human Services Secretary Kathleen Sebelius in August, the attorneys general asserted that the federal government’s screening process does not require uniform background or fingerprint checks, meaning convicted criminals or identity thieves could become navigators. They also expressed concerns that navigators would not undergo sufficient training.

Some medical professionals and advocates have objected to the privacy concerns raised by conservatives, suggesting they are politically motivated. For example, navigators must already comply with state and federal laws governing the privacy of sensitive medical information. If they do not adhere to strict security and privacy standards, including how to handle and safeguard consumers’ Social Security numbers and identifiable information, they are subject to criminal and civil penalties at both the federal and state level. The federal government imposes up to a $25,000 civil penalty for violating its privacy and security standards.

This story was produced in partnership with Kaiser Health News, an editorially independent program of the Henry J. Kaiser Family Foundation, a nonprofit, nonpartisan health policy research and communication organization not affiliated with Kaiser Permanente.

It seems to me, Medicare recipients are forfeiting the most benefit and assuming the greatest liability as a direct result of the Patient Protection and Affordable Care Act (ACA) of any group of Americans. This opinion is based, in part, on two traps recipients can fall into which can significantly compromise their financial and physical well-being. To appreciate them, you must first understand:

What is this new Center for Medicare Services Re-admission program and what is the purpose of it?

The Affordable Care Act of 2010 requires HHS to establish a readmission reduction program. This program, effective October 1, 2012, was designed to provide incentives for hospitals to implement strategies to reduce the number of costly and unnecessary hospital readmissions. CMS defines a readmission in this context as “an admission to a subsection(d) hospital within 30 days of a discharge from the same or another subsection(d) hospital.” Subsection(d) hospitals, per the Social Security Act, include short term inpatient acute care hospitals excluding critical access, psychiatric, rehabilitation, long term care, children’s, and cancer hospitals. http://www.acep.org/Legislation-and-Advocacy/Practice-Management-Issues/Physician-Payment-Reform/Medicare-s-Hospital-Readmission-Reduction-Program-FAQ/

What this gets down to is–if a hospital readmits a patient within 30 days of a prior hospitalization–they pay a penalty. What is the Center’s motivation? We already know that last year the administration authorized the transfer of approximately $716 billion from Medicare to fund Obamacare. Medicare is projected to be on the path to insolvency around 2023. A Medicare recipient (or his private insurance plan) is charged a $1,184 deductible per hospital stay for each medical condition or for the same medical condition separated by 60 days or more. Therefore, if a patient is readmitted within 30 days for the same medical condition – no deductible is due. Medicare pays the full cost for the stay. On track to be broke (and having shifted dollars to those under the age of 65 in need of health care) Medicare has created a disincentive to readmit patients by fining the hospital when this takes place. The objective is to encourage alternative methods and venues for treatment.

If you are, or will someday be, a Medicare recipient – how do you feel about this? If you think you really would like to be more closely monitored because of your fragile heart – do you really want your provider saying, “There is a pill for that!” and sending you home with your spouse? Certainly readmissions have been unnecessary in the past. Certainly, some were ill advised. But don’t you think the decision whether to readmit you should be left to your doctor free of considerations of poor job performance. Free of concern about the hospital blaming him or her for any penalties they must pay? The second trap lies in failure to know whether your hospital admission is classified as for “medical observation” or “in-patient”?

The difference in terminology is not a mere technicality. The distinction can make all the difference in terms of your financial liability and leave you with a huge hospital bill. The trap is set when the hospital does not inform you or your guardian of your status upon admission. If you are not an in-patient–guess what? You are an out-patient. Without supplemental coverage, you will be responsible for the 20% (plus excess charges) of your out-patient medical expenses Medicare does not pay. People kept in the hospital beyond the usual 24-48 hours for observation can find themselves responsible for tens of thousands of dollars depending on the length of their stay.

Now . . . follow the bouncing ball on this. If a hospital does not code a stay an admission – it does not get penalized if, within 30 days, it then does admit the patient. Hence, a hospital has in essence double dipped. It’s billed you and Medicare both as an out-patient and an in-patient while avoiding penalties. Is it simply smart business or do the Medicare regulations and their accompanying financial incentives / disincentives affect the decision making process of your doctor? A more detailed analysis of these issues is outlined in the feature articles below. Mine is just an opinion piece but . . . methinks something may be rotten in Denmark.

Your counter points are welcomed.

****************************************************************

FEATURE ARTICLES:

NEW BEDFORD (MA) STANDARD TIMES

By BEVERLY FORD

NEW ENGLAND CENTER FOR INVESTIGATIVE REPORTING

August 25, 2013 12:00 AM

Massachusetts hospitals will lose millions of dollars in funding this year — and perhaps tens of millions more in the future — because of penalties imposed by the federal Medicare program on hospitals that excessively readmit some of the state’s sickest patients, the New England Center for Investigative Reporting has found.

“In Massachusetts, we’re facing approximately $5 billion in cuts to Medicare over 10 years,” said Tim Gens, executive vice president with the Massachusetts Hospital Association. Add to that an anticipated $1.5 billion in sequestration cutbacks due to be imposed in January along with other potential funding cuts, and “it’s a very scary time for hospitals,” Gens notes.

A provision of the Affordable Care Act of 2012, the Hospital Readmission Reduction Program was designed to force hospitals to change the way they treat elderly patients by keeping them out of the hospital and in their own homes. To realize that goal, Medicare imposed penalties that increase annually from less than one percent in fiscal 2012 to a top rate of three percent by 2014, based on a hospital’s total Medicare payments

“In the long run, it will reduce per patient cost because if a patient isn’t going back into the hospital to have the same treatment done, we’re not going to be paying for those same treatments twice,” Ray Hurd, regional administrator of the Centers for Medicare and Medicaid Services, said of the penalties.

It’s not that Medicare is against readmissions, Hurd said. Patients who need hospital care will still be able to get it. The policy only aims to cut unnecessary readmissions.

With Medicare’s penalty program in its early stages, however, it’s still too soon to tell whether reducing readmissions will actually result in better patient care, said Katherine Baicker, a professor of Health Economics at Harvard.

“The goal is to reduce patients from coming back to hospitals because it’s not good for patients and it’s not good for Medicare,” said Baicker.

Nationally, one in five Medicare patients is readmitted to a hospital annually at an estimated cost of $17.5 billion. Under its new program, Medicare expects to save about $280 million in the first year alone.

In Massachusetts, of the 61 hospitals that accept Medicare payments, 54, or 88 percent, were penalized during fiscal 2012 under the readmission reduction program, according to Medicare statistics. That program targets seniors who are most likely to be re-hospitalized within 30 days for pneumonia, heart failure and heart attacks, the three ailments Washington claims are responsible for 30 percent of all elderly readmissions.

Of those 54 penalized hospitals, 12 received the severest penalties which require them to pay back between 0.90 and 1 percent of all Medicare funds received during fiscal 2012. Many of those penalties, health officials said, were imposed against “safety net hospitals” that treat poor and minority communities and teaching hospitals, where mortality rates are often low.

“We all agree readmissions are an important thing we need to work on, but the concern about the penalty is that it really penalizes hospitals for things that are out of their control,” said Karen Joynt a cardiologist and instructor in health policy at Harvard School of Public Health who has studied readmission rates.

The data, she says, shows outside factors such as access to outpatient care, patients with mental health or substance abuse issues, seniors with chronic health conditions and a transient patient population dramatically affect the number of patients hospitals readmit.

Yet, while many larger hospitals are feeling the pinch, others aren’t getting penalized at all, Joynt said.

“The bad part is that the penalties seem so unfair,” she said.

The Massachusetts Hospital Association agrees.

“The penalties are flawed,” said Gens, whose organization has been working with Bay State hospitals to reduce readmission rates since 2009. “The time has come for policymakers to realize this (policy) was not a good decision.”

A congressional advisory committee concurred.

In June the Medicare Payment Advisory Committee suggested that Congress change the penalty formula by setting annual target readmission rates and exempt from penalties those hospitals that reach those targets.

Dr. Robert Klugman, chief quality officer for UMass Memorial Health Care system, the largest healthcare system in Central and Western Massachusetts, said the real worry, however, is that the pressure put on hospitals will cause some medical facilities to turn away patients that really do need to be readmitted.

“We clearly have to change the trajectory of healthcare costs,” Klugman said. “The problem is when you look at Medicare, they place rules to penalize the bad people but sometimes it hurts the innocent people too.”

Whether the penalties are unfair or not, hospitals still find them to be burdensome, taking away money that would generally be used for equipment, programs and treatments that could benefit Medicare patients and others as well.

At Beth Israel Deaconess Medical Center in Boston, Dr. Kenneth Sands, senior vice president of Health Care Quality, said the hospital expects to lose $2 million in Medicare funding in the fiscal year that began Oct. 1, 2012.

“It’s a relatively big portion of our budget,” Sands said of the Harvard-affiliated teaching hospital, one of several teaching facilities affected by the Medicare penalties. Because Beth Israel Deaconess operates on “very low margins” of about 2 percent annually, the impact is noticeable, Sands said.

It also means there will be less money for capital outlay, infrastructure improvements and new programs — “all the things that keep us one of the better medical centers nationally,” he said, adding that the cutbacks should have no affect on patient care or result in additional patient charges.

Klugman said he too worries that the $1.5 million in penalties imposed on the UMass Memorial Health Care system this fiscal year may impact the six hospitals served under the UMass system.

“If we have less income, we can’t invest in necessary equipment. We’ll be forced to reduce programs and services,” Klugmen said.

Toby Edelman, a senior policy attorney for the non-profit Center for Medical Advocacy in Washington, DC, says Medicare’s mandate may also be too daunting for some hospitals, forcing them to look to alternative measures to meet the government’s new standards.

To skirt Medicare’s readmission rules, she said, more hospitals may begin classifying returning patients as “outpatients” even though the patients may spend the same amount of time in the hospital and get the same tests, medications and other care given to admitted patients.

The problem with outpatient status, however, is that patients who need additional care outside of a hospital — in a nursing home for example — may end up paying for that care out of their own pocket since Medicare reimburses for outside costs only when admitted patients transition into a nursing home or rehabilitation center setting, Edelman explained. Patients classified as “outpatients” just don’t qualify.

Take, for example, the 86-year-old woman who was listed as an outpatient during her hospital stay and ended up with a nursing home bill of more than $17,000. Another family cashed in an elderly relative’s life insurance policy to pay for nursing home care after their loved one was hospitalized as an outpatient instead of being listed as admitted.

“It’s very frightening,” said Edelman. “People assume when they’re in a hospital bed they’re an admitted patient. (But) a lot of people are listed as observation status for much of their stay.”

Yet, hospitals say they are making progress.