The analogy is irresistible and the comparison inescapable. Dr. Frankenstein experienced an epic epiphany when he realized his good intentions had gone awry and he was responsible for creating a monster which was a threat to the public’s health and welfare. And now the same realization has dawned on the White House and Democratic Senate. They ignored all the polls which have always indicated the majority of Americans are not in favor of Obamacare. They ignored the entreaties of the Republicans (not one of whom voted for the Act) to at first repeal; then later, to post-pone the individual mandate. Now, with November’s mid-term elections on the horizon, they are pressing the panic button and back-pedaling in an overtly political attempt to mitigate fallout at the polls. Last week they modified the individual mandate allowing those who like their non-compliant plan to keep their plan through 2016. But what went unnoticed and unreported by the media was their latest move (also last week) to destroy their own creation wherein they modified the hardship exemption. It now allows anyone whose health plan was canceled due to Obamacare to sign a form stating such–and that the act of purchasing ACA compliant coverage would be “hardship”– to opt out of a purchase with no financial repercussions. The details of the exemption are outlined in our feature article in The Wall Street Journal which concludes the exemption is essentially available to anyone who wants one.

In reality, the Democrats are realizing they are falling on their own sword. What was already a case of adverse selection in terms of the risk funneled into the new Affordable Care Act (ACA) compliant policies, has now been made a case of adverse selection on steroids. This editor’s concern is that the insurance companies will not be able to sustain the new block of compliant policies and will fail minus another massive government bailout. Like banks, they will be deemed “too big to fail” by the administration. For now. Of course, in good time (after Democrats succeed in maintaining control of things), the safety net will be removed and the liberals will rejoice as the companies fail. And left leaning Democrats will have the single-payer system they have long admitted was their prize objective. An accomplishment so necessary for them to control one sixth of our nation’s economy. This in spite of the fact that every major social welfare program this country has implemented is on the fast track to insolvency.

As Dr. Frankenstein worked to destroy his own signature creation, the President now works to gut his. And as always . . . for the sake of politics.

HHS quietly repeals the individual purchase rule for two more years.

Updated March 12, 2014 6:58 p.m. ETObamaCare’s implementers continue to roam the battlefield and shoot their own wounded, and the latest casualty is the core of the Affordable Care Act—the individual mandate. To wit, last week the Administration quietly excused millions of people from the requirement to purchase health insurance or else pay a tax penalty.

This latest political reconstruction has received zero media notice, and the Health and Human Services Department didn’t think the details were worth discussing in a conference call, press materials or fact sheet. Instead, the mandate suspension was buried in an unrelated rule that was meant to preserve some health plans that don’t comply with ObamaCare benefit and redistribution mandates. Our sources only noticed the change this week.

That seven-page technical bulletin includes a paragraph and footnote that casually mention that a rule in a separate December 2013 bulletin would be extended for two more years, until 2016. Lo and behold, it turns out this second rule, which was supposed to last for only a year, allows Americans whose coverage was cancelled to opt out of the mandate altogether.

In 2013, HHS decided that ObamaCare’s wave of policy terminations qualified as a “hardship” that entitled people to a special type of coverage designed for people under age 30 or a mandate exemption. HHS originally defined and reserved hardship exemptions for the truly down and out such as battered women, the evicted and bankrupts.

But amid the post-rollout political backlash, last week the agency created a new category: Now all you need to do is fill out a form attesting that your plan was cancelled and that you “believe that the plan options available in the [ObamaCare] Marketplace in your area are more expensive than your cancelled health insurance policy” or “you consider other available policies unaffordable.”

This lax standard—no formula or hard test beyond a person’s belief—at least ostensibly requires proof such as an insurer termination notice. But people can also qualify for hardships for the unspecified nonreason that “you experienced another hardship in obtaining health insurance,” which only requires “documentation if possible.” And yet another waiver is available to those who say they are merely unable to afford coverage, regardless of their prior insurance. In a word, these shifting legal benchmarks offer an exemption to everyone who conceivably wants one.

Keep in mind that the White House argued at the Supreme Court that the individual mandate to buy insurance was indispensable to the law’s success, and President Obama continues to say he’d veto the bipartisan bills that would delay or repeal it. So why are ObamaCare liberals silently gutting their own creation now?

The answers are the implementation fiasco and politics. HHS revealed Tuesday that only 940,000 people signed up for an ObamaCare plan in February, bringing the total to about 4.2 million, well below the original 5.7 million projection. The predicted “surge” of young beneficiaries isn’t materializing even as the end-of-March deadline approaches, and enrollment decelerated in February.

Meanwhile, a McKinsey & Company survey reports that a mere 27% of people joining the exchanges were previously uninsured through February. The survey also found that about half of people who shopped for a plan but did not enroll said premiums were too expensive, even though 80% of this group qualify for subsidies. Some substantial share of the people ObamaCare is supposed to help say it is a bad financial value. You might even call it a hardship.

HHS is also trying to pre-empt the inevitable political blowback from the nasty 2015 tax surprise of fining the uninsured for being uninsured, which could help reopen ObamaCare if voters elect a Republican Senate this November. Keeping its mandate waiver secret for now is an attempt get past November and in the meantime sign up as many people as possible for government-subsidized health care. Our sources in the insurance industry are worried the regulatory loophole sets a mandate non-enforcement precedent, and they’re probably right. The longer it is not enforced, the less likely any President will enforce it.

The larger point is that there have been so many unilateral executive waivers and delays that ObamaCare must be unrecognizable to its drafters, to the extent they ever knew what the law contained.

To say that President Obama is not an enthusiastic backer of the two Medicare programs that offer seniors private insurance options would be something of an understatement.

Over the years, Obama has repeatedly derided Medicare Advantage — the program that lets seniors enroll in subsidized, private insurance. He once called it “wasteful,” and said it amounted to “giveaways that boost insurance company profits but don’t make (seniors) any healthier.”

Obama has been equally harsh when it comes to Medicare Part D — the prescription drug benefit President Bush signed into law that relies on privately run plans.

In his 2006 book, “The Audacity of Hope,” Obama blasted the program, saying it “somehow managed to combine the worst aspects of the public and private sectors.” As president, he said it gave overly generous “taxpayer subsidies to prescription drug companies.”

Both programs, it turns out, have been wildly popular with seniors and, by most measures, big successes. But Obama nevertheless appears determined to undermine them with sharp cuts in payments and sweeping new regulations.

Started back in 1997 — and initially called Medicare+Choice — the Medicare Advantage program pays private insurers a set amount per enrollee to provide comprehensive benefits and anything else they can afford to offer.

The idea was that private insurers could better co-ordinate care and manage health costs than the old fee-for-service Medicare, and so provide more comprehensive benefits.

While enrollment in these private plans was flat for the first several years, it has skyrocketed since 2005, to the point where almost one in three seniors are covered by a private health plan. As long as it is affordable, this editor considers Medicare Supplement the ideal way for a Medicare recipient to be covered for medical expenses. Not because selection of Supplement Plan F or G will cover all or virtually all of your expenses but because ALL Medicare Supplement options allow you to visit any doctor, hospital or medical provider that sees Medicare Patient. This as opposed to Medicare Advantage Plans most of which have evolved to significantly limiting your choice of providers. This being said, Medicare Advantage has been a savior to those who simply cannot afford Medicare Supplement. And contrary to Obama’s claim, seniors selecting Medicare Advantage tend to get better quality health care than those in traditional Medicare.

Critics, however, point to studies showing that the government pays Medicare Advantage more per enrollee than it would cost if these seniors had enrolled in the old Medicare program.

Obama tried to remedy this by cutting Medicare funding by $716 billion over the next ten years with payments to Medicare Advantage totaling $200 billion. The purpose of which is to help pay for ObamaCare (while providing “bonus” payments to plans that score high on a quality rating). An official analysis from Medicare’s actuary concluded, however, that such cuts would drive millions seniors out of their Advantage plans and back into the government-run program.

Recognizing political risks of these payment cuts, the administration put them off until AFTER the presidential elections, shoveling $8 billion into a bogus “demonstration project” that offset almost all the scheduled Medicare Advantage cuts implemented in 2012.

Question: What are your thoughts about President Obama’s cuts to the Medicare Advantage and Part D Prescription Drug Programs?

Republican Senate leaders criticized the Obama administration Tuesday for proposed changes to Medicare Advantage (MA) and Part D they say would weaken the two programs.

Led by Minority Leader Mitch McConnell (R-Ky.), the lawmakers called on Health and Human Services (HHS) Secretary Kathleen Sebelius to suspend proposed cuts to Medicare Advantage and reforms in Part D that would allow regulators to participate in negotiations between insurance companies and pharmacies for the first time.

“Unlike ObamaCare, the Medicare prescription drug benefit is wildly popular and it has cost less than initial projections,” the letter stated.

“At a time when HHS is struggling on basic implementation tasks on many fronts, we cannot understand the logic behind the department’s interest in further undermining one of the few success stories under its purview.”

The administration argues that cuts in Medicare Advantage would reduce waste within the program and bring its per-patient funding in line with traditional Medicare, which currently receives less money on average.

In Part D, federal health officials say regulators need new authority to ensure the market for prescription drugs works well for seniors.

The proposed rules would also open drug plans’ preferred networks to a wider range of pharmacies, limit plan bids within a region and remove “protected class” designations for certain types of drugs.

But Republicans say the changes will harm Medicare Advantage beneficiaries and potentially raise premiums on Part D plans or force seniors out of their current coverage.

Both issues are rearing their heads in the midterm elections, as the GOP seeks to broaden its healthcare attacks to include more than ObamaCare.

Tuesday’s letter to Sebelius was signed by McConnell, GOP Whip John Cornyn (Texas), GOP Conference Chairman John Thune (S.D.), GOP Policy Committee Chairman John Barrasso (Wyo.), Conference Vice Chair Roy Blunt (Mo.) and National Republican Senatorial Committee Chairman Jerry Moran (Kan.).

The White House has doubled down on the Republican’s November request to delay the “Individual Mandate” of the Affordable Care Act.

At least a major portion of it.

The only thing predictable about implementation of the Affordable Care Act is that . . . nothing is predictable. On Wednesday, the Obama Administration played “tooth fairy” to Democrat candidates up for re-election this November and gave American individuals and families with pre-2014 health insurance policies a reprieve on the mandate to purchase ACA compliant coverage for two years through 2016. Last fall the House argued and passed a bill allowing American individuals and families who liked their current health plan – to keep their health plan. As the President had originally promised they could do. But for just one year. Now, in what appears to be an entirely self-serving and purely political move to mitigate a loss of Democratic seats in the up-coming mid-term elections, the Administration Obama says . . . “Errrr – of course! You can keep your plan for two more years!” It is quite apparent the Democrats have correctly determined the backlash from plan cancellations mandated by law could be devastating in terms of their election. Therefore, they speculate, with this aspect of the law deferred they will fair much better at the polls.

As a health insurance broker, I must admit I feel this is something of reprieve for myself and many of my clients. My clients can keep their lower cost plans which, in Texas, average approximately 40% higher than pre-compliant plans (approximately 80% higher in Indiana and Ohio – not to mention a dearth of PPO options as opposed to the restrictive HMO options). As for me, I can cease worrying, for now, about losing clients en masse who would otherwise be forced off their existing plans and might go elsewhere for replacement coverage. I can also anticipate obtaining entirely new clients who choose to elect a new plan in order to cover a pre-existing condition or just to comply with the law. And therein lies the rub. Just because the White House says those who have a plan can keep their plan, does not mean the individual states or the insurance companies will agree to this. And for many, it is far too late – their policies already having been canceled. But–furthermore–this reprieve apparently does not carry over to those who have no coverage whatsoever. They must still acquire coverage by March 31st or be assessed the penalty and locked out of insurance for the remainder of 2014. (Unless, of course, they are also eventually granted clemency by the President.)

And how does your editor feel about this from an actuarial standpoint relative to the insurance companies and the ACA itself? In four words: “Politically Pragmatic Voodoo Economics”. Even Obamacare architect Ezikiel Emanuel, stated Wednesday while on MSNBC, that while he denounced the policy implications of yet another Obamacare delay, “for the political gain, it’s worth it”. Unabashedly self-serving.

If the insurance companies comply, they are once again forced to flex at the last minute and be left with two separate blocks of business. One old block containing less claim’s risk. And one new block where the only motivation to insure oneself will be to transfer personally large risk to the insurance company. This will be in terms of pre-existing conditions which were previously manageable or that arise for the first time. As evidence of this, in an attempt to limit the disruption to the insurance industry precipitated by this latest modification, the Department of Health and Human Services also announced yesterday that the “risk corridor” program (which has been described as a bailout to insurers) would be further modified to channel more money to the insurers in states affected by the change. This only reinforces my opinion that those behind this bill are not economists and never cared about the financial viability of this law. They are, however, very concerned with maintaining their political lives at all cost.

WASHINGTON — The Obama administration, grappling with continued political fallout over its health care law, said Wednesday that it would allow consumers to renew health insurance policies that did not comply with the new law for two more years, pushing the issue well beyond this fall’s midterm elections.

The reprieve was the latest in a series of waivers, deadline extensions and unilateral actions by the administration that have drawn criticism from the law’s opponents and supporters, many saying President Obama was testing the limits of his powers.

The action reflects the difficulties Mr. Obama has faced in trying to build support for the Affordable Care Act and the uproar over his promise — which he later acknowledged had been overstated — that people who liked their insurance plans could keep them, no matter what.

Under pressure from Democratic candidates, who are struggling to defend the president’s signature domestic policy, Mr. Obama in November announced a one-year reprieve for insurance plans that did not meet the minimum coverage requirements of the 2010 health care law.

The Times would like to hear from Americans who have signed up for health care under the Affordable Care Act.

Wednesday’s action goes much further, essentially stalling for two more years one of the central tenets of the much-debated law, which was supposed to eliminate what White House officials called substandard insurance and junk policies.

The extension could help Democrats in tight midterm election races because it may avoid the cancellation of policies that would otherwise have occurred at the height of the political campaign season this fall.

In announcing the new transition policy, the Department of Health and Human Services said it had been devised “in close consultation with members of Congress,” and it gave credit to a number of Democrats in competitive races, including Senators Mary L. Landrieu of Louisiana, Jeanne Shaheen of New Hampshire and Mark Udall of Colorado.

Kathleen Sebelius, the secretary of health and human services, said Mr. Obama was trying to “smooth the transition” to a new system, using flexibility that exists under the law.

The move reflects the administration’s view that a divided Congress would not be willing to make changes to the law, but lawyers questioned the legitimacy of the action and said it could have unintended consequences in the long run.

“I support national health care, but what the president is doing is effectively amending or negating the federal law to fit his preferred approach,” said Jonathan Turley, a law professor at George Washington University. “Democrats will rue the day if they remain silent in the face of this shift of power to the executive branch.”

Mr. Turley said Mr. Obama was setting precedents that could be used by future presidents to delay other parts of the health care law or to suspend laws dealing with taxes, civil rights or protection of the environment.

Republicans said the move confirmed their contention that parts of the health care law were ill conceived and unworkable.

The number of people with noncompliant coverage is not known. Insurers sent out perhaps 4.5 million cancellation notices last fall, but some of the policyholders have bought new coverage that complies with the law. Administration officials said that the number of people with noncompliant policies would shrink by attrition in the next two years.The health care law sets dozens of federal standards for insurance, requiring coverage of services in 10 specific areas and providing many consumer protections not found in older policies.Under the transition policy announced by Mr. Obama in November, insurers “may choose to continue coverage that would otherwise be terminated or canceled.” Insurers were allowed to renew existing policies even if they did not provide the “essential health benefits” prescribed by law. In addition, the administration said, insurers could continue charging women more than men for those policies and could charge higher premiums based on a person’s health status, in violation of the new law.

A White House official said Wednesday that it would allow insurers to continue existing policies with renewals as late as Oct. 1, 2016, so individuals and small businesses could have noncompliant coverage well into 2017.

Under another policy announced by the administration on Wednesday, certain health plans will be exempt from new fees imposed on insurance companies and on many self-insured group health plans. Labor unions had been lobbying for such an exemption, saying the fees could be “highly disruptive” to Taft-Hartley plans administered jointly by labor and management representatives in construction, entertainment and other industries.

The Times would like to hear from Americans who have signed up for health care under the Affordable Care Act.

Wednesday’s action goes much further, essentially stalling for two more years one of the central tenets of the much-debated law, which was supposed to eliminate what White House officials called substandard insurance and junk policies.

The extension could help Democrats in tight midterm election races because it may avoid the cancellation of policies that would otherwise have occurred at the height of the political campaign season this fall.

In announcing the new transition policy, the Department of Health and Human Services said it had been devised “in close consultation with members of Congress,” and it gave credit to a number of Democrats in competitive races, including Senators Mary L. Landrieu of Louisiana, Jeanne Shaheen of New Hampshire and Mark Udall of Colorado.

Kathleen Sebelius, the secretary of health and human services, said Mr. Obama was trying to “smooth the transition” to a new system, using flexibility that exists under the law.

The move reflects the administration’s view that a divided Congress would not be willing to make changes to the law, but lawyers questioned the legitimacy of the action and said it could have unintended consequences in the long run.

“I support national health care, but what the president is doing is effectively amending or negating the federal law to fit his preferred approach,” said Jonathan Turley, a law professor at George Washington University. “Democrats will rue the day if they remain silent in the face of this shift of power to the executive branch.”

Mr. Turley said Mr. Obama was setting precedents that could be used by future presidents to delay other parts of the health care law or to suspend laws dealing with taxes, civil rights or protection of the environment.

Republicans said the move confirmed their contention that parts of the health care law were ill conceived and unworkable.

But Republicans denounced the change. “The administration’s decision to carve out its union cronies from the Obamacare fee is beyond egregious and will leave others with self-insured plans on the hook to foot the bill,” said Senator John Thune, Republican of South Dakota.

Robert Laszewski, a consultant who works closely with insurers, said the reprieve for noncompliant policies “tends to undermine the sustainability of Obamacare” by reducing the number of people who will buy insurance through the exchanges.

The administration acknowledged that its transition policy could lead to “higher average claims costs” for people who buy insurance that complies with the Affordable Care Act. But health officials said the 2010 law provided several “shock absorbers” to help stabilize premiums.

Late last week I returned from the National Association of Health Underwriters Capitol Conference 2014 in our nation’s capitol. Our group stayed in the shadow of the Capitol at the Capitol Hill Hyatt two blocks from where our laws or bills are created and passed. Our primary objective this year would be to address the ramifications of what is arguably the biggest Act ever in terms of its impact on all America. It was my first meeting to attend at a national level and I am grateful for the warm welcome provided me by the Houston, Texas Chapter and the entire experience. I express particular thanks to Lonnie Klene for facilitating my attendance and Malcolm Browne, Sibony-Trevino Toth, Jo Middleton and Jeffrey Bacot for their engaging conversation which made the informal time much more enjoyable.

The overall goal of the conference was to represent the interests of health insurance agents and brokers in their role of assisting the public in the administration’s goal of acquiring quality, affordable health insurance. Of course, because of what we now know are the results of the Patient Protection and Affordable Care Act, this seems something of a daunting, if not failed, mission in terms for many of the stated beneficiaries at this point. Still, it was the Association’s stance that the bill is law and for now is the system we have to work with. As much as I would have liked to have protested and lobbied for solutions to our nation’s debt crisis; its lack of a viable energy policy and justice for the victims of Fort Hood and Benghazi – this was not the purpose of our attendance as a group nor the reason the Houston Chapter sponsored my presence at the conference. Those are issues which I will have to address through correspondence with the contacts I made and indirectly at the poll booth in the coming mid-term election.

The issues which our group did address with our respective Representatives were, among others:

1) The need for involvement of professionally licensed benefit specialists, i.e., agents and brokers (as opposed to unlicensed, unvetted navigators) to help consumers before, during and–most importantly–after the sale of private health insurance coverage and, of course, our opposition to their exclusion in this process.

2) Our concern over the inability of many employers to afford to offer coverage to their employees and the negative effect this has on our nation’s current economic uncertainty and limited job growth.

3) Our support of a comprehensive bill to rectify provisions of the law and new regulatory requirements that are creating compliance burdens for businesses and conflict with time tested employee benefit practices.

4) Our opposition to changes to time tested traditional definitions of small and large employers and full-time and part-time employees, this last of which has resulted in employers cutting employees to 29 hours thus making them part-time employees pursuant to the new definition (30 Hour Work Week) and contributing to under-employment.

5) Our opposition to age banding which unfairly discriminates against the young and does not accurately assign cost relative to risk.

6) Eliminating the national premium tax projected to add an average of $500 of costs to a typical family policy in 2014 and more thereafter.

For Seniors:

1) Our support of efforts to preserve Medicare options flexibility for recipients and restore the long-term financial health of the program.

2) Our opposition to funding the costs of the Affordable Care Act on the backs of our nation’s senior citizens. Specifically, cuts to Medicare Advantage and Part D Prescription Drug Plans.

3) Providing new financial incentives to encourage and make possible the purchase of long-term care insurance for our exploding senior population. (an average of 10,000 boomers turn age 65 every day)

Day 1 of the conference consisted in part of a break-out session covering the current state of the employer mandate; Private Exchanges for Employers; Medicaid 101 and Compliance.

Day 2 Addressed The Political Impact of Health Reform; The Future of the Marketplace (federal and state exchanges) followed by lobbying on Capitol Hill. It was at this point Lonnie Klene, Sibony Trevino-Toth and myself met briefly with our District 8 Representative, Kevin Brady and longer with his assistant, Andriu Colgan. Like most aides, Andriu was young, bright and responsive to our concerns (as outlined above) and assured us Congressman Brady was sympathetic to these. In his brief time with us, he confirmed such.

Your blog editor outside Representative Brady’s Office in the Cannon Building.

That evening, I was one of a group of Texans privileged to attend a 3.5 hour tour of the Capitol hosted by Texas District One Republican Representative Louie Gohmert, from a boyhood home of mine, Tyler Texas. He insisted he knew some of my cousins, but there was no doubt he knew an incredible amount of our nation and its leader’s history which he very generously shared with us. He is a remarkable story teller with a keen sense of humor and the tour he hosted for us, most of whom will never have occasion to vote for him, proved to be one of the most memorable experiences of my life. My appreciation of our nation’s history and heritage (which was already tremendous) is even greater thanks to him. And he made no bones–he’s with me on the issues! If I lived in his district, he’d certainly have my vote!

U.S. Representative, Texas First Congressional District, Louis B. Gohmert, Jr.

Day 3 consisted of a panel of physicians discussing Health Cost Transparency; “The Marketplace Transformed” hosted by Representative Renee Elmers (R-NC); Jennifer Duffy, Senior Editor, The Cook Political Report and Representative Jim Matheson (D-UT).

All sessions were followed by a fairly extensive, cogent question and answer period.

This last day ended with a special presentation entitled “Taking It All Home” by Dan Clark, motivational speaker and author of, among other works, the “Chicken Soup for The Soul” series. I must say that after the stress of all the change the Affordable Care Act has brought to this agent, and the others in attendance, we were in need of his inspirational soup and it proved very therapeutic.

All in all I came home with more knowledge and ideas of how to assist my clients in dealing with the reality and mandates of the Patient Protection and Affordable Care Act as it stands for now.

Healthandmedicareinsurance.com followers – I spent enough time responding to the left on my facebook posting – I thought the effort could serve double duty on this blog.

***************************************************************************************************

Before preparing for my trip, I would first like to respond to Kathy: No, I won’t be lobbying for an expansion of Medicaid in Indiana (or any other state for that matter) that has not already expanded it beyond 100% of the Federal Poverty Level. If Medicaid were expanded, it would be to include individuals up to and including those with an income of 133% of the FPL or a maximum income of $15,521 for 2014. Deserving or not aside – while these individuals currently do not qualify for Medicaid in Indiana or Texas – THEY DO qualify for a subsidy of approximately 88% of their health insurance premium. If they elect the plan recommended by the Department of Health and Human Services (“benchmark” plan) it will be the second lowest cost Silver Plan in their area. They are required to pay no more than $40.41 per month. No, I don’t feel sorry for them. They are certainly already receiving food stamps and government subsidized housing and Medicaid is already in financial trouble in most states without further expansion. (Of course I am aware financial feasibility and a balanced state or federal budget is not your concern.)

The person I feel sorry for is the poor working stiff who is making in the $50 – $60,000 dollar range and actually earning his or her income. They don’t qualify a health insurance premium subsidy. (Food stamps I’m not certain of because our government has made those available to virtually everyone including illegal aliens.) Because this responsible working person doesn’t qualify for a subsidy, they will be forced to pay 100% of the Silver plan premium–with an average annual cost of $4,113–entirely on their own. That amounts to 8% of their annual income (at $50k) before taxes which the entitlement person isn’t paying! That’s the person I feel sorry for! Then try providing them with a plan that has their doctor in the network and the benefits they would really like and their cost and that percentage soars! In summation – you keep lobbying for the entitlement class; I’ll keep lobbying for the working American.

Now to address Scott: Glad to see you are finally making a prediction which I feel is pretty much on target. As I’m the one on the front line signing people up for Obamacare, no one knows better the “adverse selection” (bad risk disproportionately selected for participation) than I. But I remember a few of my predictions you tried to dismiss. First – I said Barrack Obama would be elected in 2008. You said, “no”. In 2010 – I said the Patient Protection and Affordable Care Act (PPACA or ACA for short) would pass. You said, “no way!”. Then, in June of 2012 – I said the Supreme Court is going to find a way to uphold the ACA as “constitutional”. You said, “not to worry!” God! I hate being right. (Almost as much as you hate being wrong!)

Anyway, I’m glad you are finally smelling the coffee which probably got to a stench with your latest health insurance premium increase. And, as such, this begs many questions – two of which I will address at this point:

(1) If the federal government cannot build a functional website, to insure the estimated 30 million uninsured, with 3 years lead time – How long is it going to take them to transition us to a “Medicare like” social welfare health insurance program that insures all 300 million plus Americans. And . . .

(2) If Social Security is on track to insolvency and Medicare is predicted to be insolvent by 2023 (nine years from now, people) – how the hell are they going to finance and subsidize healthcare for everyone? Redistribution. Because it wasn’t fair you’ve been so successful, Scott.

In my next blog post, I will address what I see as the specifics of why these things regarding the ACA are destined to transpire. In the meantime, I’m still going to Washington because the one thing we do know is – the person that never gets in the ring has already lost. The real issues I would like to confront our elected officials with are my suggestions for workable healthcare reform which guarantees coverage for pre-existing conditions while being financially responsible and feasible; term limits (I know, I know – when hell freezes over); amnesty and targeting of conservative groups by the IRS. I know they’ll try to get me back on point (theirs) – but not until I’ve made them say, “next question!”

Not content to sit passively on the side lines while Washington dictates to him, his clients and fellow citizens – Kenton Henry, agent, owner of Allplanhealthinsurance.com in The Woodlands, will voices his–and your–concerns in our nation’s Capitol.

It is my privilege to soon be attending the annual legislative conference for my professional association, the National Association of Health Underwriters, from February 24-26 in Washington, D.C. Representing influential professionals in my industry, I will take this opportunity to present meaningful solutions to our national policymakers to improve the cost and quality of health insurance while reducing the burdens the Patient Protection and Affordable Care Act has placed on businesses and individuals across the United States.

As the regulations and requirements of the health reform law continue to evolve, it is extremely important that our representatives in Washington, D.C., hear what is going on with you; your families; employers and employees. Our representatives on Capitol Hill need to hear a common-sense perspective from the average citizen’s point of view along with consumer inspired solutions. I will attend meetings on Capitol Hill with Senators, Representatives and their staff and would be happy to pass along any thoughts about health reform you, my valued friends and clients, may have. I have requested an appointment with Texas District 8 Congressman Kevin Brady, among others. Please contact me at Quote@Allplaninsurance.com to share your message with them. Share with me your greatest problems and concerns with health care and health insurance and what solutions you may have in mind. I promise your story will be told and commit to being your voice among those who represent us.

In addition to talking to our elected representatives, I will be attending educational sessions about benefit and policy trends that will include:

• Key briefings from the national policy staff and association leadership.

• Panel discussions on health cost transparency, innovations in coverage and delivery systems, and policy trends relative to cost containment.

• Updates on the latest developments regarding the new health insurance marketplaces (exchanges).

• Presentations from congressional and Administration health policy leaders including updates about potential changes to the law and new evolving regulatory guidance.

• A session about using the political dynamics of healthcare to transform business.

• Breakout meetings that will cover innovative solutions to address the employer reporting requirements, shared responsibility requirements, self-funding options in a reformed health system, private and public exchanges, small group market trends and much more!

The future of healthcare reform is ever changing and the impact of this law will affect us all in many different ways across the country. I believe that my voice and your voice truly do make a difference. I look forward to sharing our stories as I lobby on Capitol Hill. Upon my return, I will share with you what I hope will be encouraging news of coming improvements to the present state of healthcare and health insurance in Texas and the rest of America.

If the administration and main stream media will not tell you–I will:

You can go through me–or any licensed health insurance agent or broker to acquire health insurance. NOW. And this is whether you qualify for a subsidy or not. And, importantly, there will be no, I repeat – $0 difference in your cost (premium) for doing so vs. the government website Healthcare.gov or a private insurance company’s. Period. Now where have you heard “Period” before and it turned out to be true? Well . . . in this case it is.

There is only ONE reason to go to the still basically inoperable, security in doubt, aforementioned federal government health insurance website known as The Marketplace:

1) You qualify for a subsidy of your 2014 health insurance premium and you would like to take advantage of that subsidy as you pay your premiums. I.e., you qualify and would like the premium you pay to your insurance company to be reduced by the amount of your subsidy as you pay the premium. (This as opposed to paying the gross premium (cost before your subsidy is applied) then declaring your subsidy on your 2014 tax return and having your tax liability reduced accordingly.)

If you this does not describe you – there is absolutely no reason to go to healthcare.gov!

Neither do you need to go through a state appointed, federally funded Navigator, hired by the State and required to complete only 20 hours of online education and be subjected to no background check. Why replicate and risk the possible insecurity of your personal information which includes your address; birth date; social security number and reported income by going through someone not even vetted by the Department of Health and Human Services (HHS) or the Center for Medicare Services (CMS)? As the Secretary for HHS, Kathleen Sebelius, admitted under oath and questioning from Texas Senator John Cornyn during Congressional, hearings just last week – “It is possible (for a convicted felon to be hired as a Navigator and take your personal and vital information).”

This begs the question: Why is the administration and main stream media not advertising, and barely mentioning, that a health insurance shopper can go through a licensed and vetted insurance agent who has passed a background check with every company with whom they are appointed and do so at no additional cost? Or that the shopper can then have all the expertise that that agent’s time in the industry (27 years in my case) brings to bear on their needs and situation? Or how about a “go to” advocate in their behalf they can call whenever there is an issue relating to claims; rates or general service related issues such as changes in address or dependents. This as opposed to a different unknown service rep at the end of a toll free number each time they call an insurance company directly?

I will let you speculate on the answers to these questions but (while the purpose of this blog is to educate the follower on issues relating to health and Medicare insurance) indulge me while I for once engage in a little shameless self-promotion on behalf of myself and all licensed agents and brokers:

If you reside in Texas; Indiana; or Ohio – please visit my website at http://allplaninsurance.com and click on the bold red “Get A Quote!” button on the home page or–better yet–call me toll free @ 800.856.6556 and let’s have an intelligent dialogue about your true wants and needs relative to coverage and then get some meaningful quotes and information for you. All without submitting the equivalent of a home mortgage application!

If you reside in any other state – do yourself a favor and call a well recommended licensed health insurance agent or broker in your community.

Again, call me even if you do qualify for a subsidy. I can help you just the same and–as without a subsidy–your cost for insurance will be the same. If you do not want to take the subsidy now but would rather take it on your 2014 tax return (when you actually know what your income will have been) we can apply for you now and have your coverage issued immediately.

If you want the subsidy applied upfront, to reduce the premium you pay each month, we will still have to enter the healthcare.gov website. But we will do so only after we have obtained your gross quotes via my website. I know the formula and can do a pretty fair job of estimating your net premium (after your subsidy is applied). If this scenario describes you, as the federal website is still inoperable, we should wait and see if HHS and CMS have the site fixed and secure by November 30th as promised. Let’s keep our fingers crossed and–if so–we should sail (wink, wink) through the application and have your coverage issued by January 1. But remember, if all government deadlines remain as now, we will need to complete your application no later than December 15th!

Well folks, here we are into the third week since the highly touted, much anticipated opening of the federal and state exchanges for purposes of enrolling in a health care act compliant insurance plan for 2014. And guess what? While a few state exchanges are experiencing some, generally small, measure of success – the federal exchange, or Marketplace, remains a dismal failure. It is, however, an excellent painful and protracted self-flagellating exercise in frustration. For an analogy–imagine having a root canal absent anesthesia while listening to Debbie Boone’s, “You Light Up My Life” on a continuous sound track loop through the entire procedure. Just to make the comparison more accurate, imagine you are Dustin Hoffman’s character who is tortured with a dentist’s drill in the movie Marathon Man but your experience is enhanced as your hygienist pulls your toe nails out with a pair of needle nose pliers in order to distract you from your oral discomfort. And that, I believe, is a pretty fair comparison to the enjoyment of opening an account and obtaining quotes for health insurance in the Marketplace to date. The tax payer’s cost to deliver this electronic equivalent of a Halloween visit to a House of Horrors? Current estimates are over $500 million and growing as desperate measures are being made to fix all its glitches as this goes to press. This after the Department of Health and Human Services accepted the low bid of $55 million with a ceiling of $93.7 million from Canadian software company, CGI Federal. Canadian? Really? All that U.S. taxpayer money to a Canadian firm? (I’m not even going there.)

But relax, dear patient. Let’s apply a little Novocain to your orifice. Let’s give you a subsidy to help ease the pain you will suffer when you see the highly inflated cost of health insurance you are now commanded to purchase under threat of penalty.

People making between 100 and 400 percent of federal poverty level can qualify for the premium tax credit health insurance subsidy. Federal poverty level changes every year, and is based on your income and family size.

Using 2013 FPL levels, you’ll qualify as an individual with an income range of $11,490-$45,960, a couple with an income of $15,510-$62,040, and a family of three earning $19,530-$78,120.

Just how do you calculate your subsidy?

In order to calculate how much your premium tax credit (subsidy) will be – you have to know 2 things:

(A) Your expected contribution toward the cost of your health insurance (available at the end of this article); and

(B) The cost of your BENCHMARK health plan. (Your health insurance exchange–assuming you succeed in opening an account and obtaining quotes–can tell you which plan this is and how much it costs. Your benchmark plan is the silver-tiered health plan with the second lowest monthly premiums in your area. The Affordable Care Act classifies health plans based on how much of your health care costs they’re expected to cover. A bronze health plan will cover about 60 percent of the average person’s health care costs. A silver health plan will cover about 70 percent.)

Your subsidy amount is the difference between your expected contribution and the cost of the benchmark plan. But just because the benchmark plan is used to calculate your subsidy doesn’t mean you have to buy the benchmark plan. You may buy any plan listed on your health insurance exchange, but your subsidy amount stays the same.

If you choose a more expensive plan, you’ll pay the difference plus your expected contribution. If you choose a plan that’s cheaper than the benchmark plan, you’ll pay less since the subsidy money will cover a larger portion of the monthly premium. If you choose a plan so cheap that costs less than your subsidy, you won’t have to pay anything for health insurance. However, you won’t get the excess subsidy back.

If you’re trying to save money so you choose a plan with a lower value, (like a bronze plan instead of a silver plan), you’ll likely have higher coinsurance and copays when you use your health insurance.

There’s another reason to choose a silver-tier plan. There’s a different subsidy that lowers copays, coinsurance, and deductibles for some low-income people. Eligible people can use it in addition to the premium tax credit subsidy. However, it’s only available to people who choose a silver-tier plan.

One question I am frequently asked is, “Do I have to wait until I file my income tax return in order to get the subsidy?”

Answer: “No”

You can get the premium tax credit in advance. If your income is so low you don’t have to file a tax return, you can still get the subsidy. But bear in mind–if you underestimate your income and take a subsidy–you will be forced to pay it back or, if you are due a refund, have it reduce such respectively when you file your return. (Income verification was put back in 2014 subsidy provisions after being suspended for one year along with the Administration’s one year suspension of the mandate that large employers must purchase health insurance for their employees. And remember–the IRS is in charge of monitoring your enrollment and expenditure.)

Consider opting to get the subsidy along with your tax refund if:

Your income is very close to 400 percent of FPL.

Your income varies from year to year so you’re not sure how much you’ll make.

When the subsidy is paid in advance, the amount of the subsidy is based on an estimate of your income for the coming year. If the estimate is wrong, the subsidy amount will be incorrect.

If you earn less than estimated, the advanced subsidy will be lower than it should have been. You’ll get the rest as a tax refund.

If you earn more than estimated, the government will send too much subsidy money to your health insurance company. You’ll have to pay back part or all of the excess subsidy money when you file your taxes. Even worse, if your actual income ended up more than 400 percent of FPL, you’ll have to pay back every penny of the subsidy. This could be thousands of dollars.

If you get your subsidy when you file your income taxes rather than in advance, you’ll get the correct subsidy amount because you’ll know exactly how much you earned that year. You won’t have to pay any of it back.

The Marketplace’s software will (supposedly) calculate your subsidy. Perhaps, as time goes by, it will even do so accurately. But for those of you who scored at least 600 on your high school SAT math test and enjoy such things – here is the exact formula for keeping the government honest:

Figure out how your income compares to FPL.

Find your expected contribution rate in the table below.

Calculate the dollar amount you’re expected to contribute.

Find your subsidy amount by subtracting your expected contribution from the cost of the benchmark plan.

Here is an example:

Mary is single with an income of $22,800 per year. FPL for 2013 is $11,490 for single people.

To figure out how Mary’s income compares to FPL, use: income ÷ FPL x 100.

$22,800 ÷ $11,490 x 100 = 198.4.

Mary’s income is 198 percent of FPL.

Using the table below, Mary is expected to contribute 4-6.3 percent of her income. Since she’s almost at the top of her category in the table, she uses the 6.3 percent figure.

To calculate how much Mary is expected to contribute, use this equation: 6.3 ÷ 100 x income.

6.3 ÷ 100 x $22,800 = $1,436.

Mary is expected to contribute $1,436 per year, or about $120 per month, toward the cost of her health insurance. The premium tax credit subsidy pays the rest of the cost of the benchmark health plan.

The benchmark health plan at Mary’s health insurance exchange costs $3,900 per year or $325 per month. Use this equation to figure out the subsidy amount: cost of the benchmark plan – expected contribution = amount of the subsidy.

$3,900 – $1,436 = $2,464.

Mary’s premium tax credit subsidy will be $2,464 per year or about $205 per month.

If Mary chooses the benchmark plan, or another $325 per month plan, she’ll pay $120 per month for her health insurance. If she chooses a plan costing $425 per month, she’ll pay $220 monthly for her health insurance. If she chooses a plan costing $225 per month, she’ll only pay $20 per month for her health insurance.

FEDERAL POVERTY LIMIT BASED ON NUMBER OF FAMILY IN HOUSEHOLD:

(Click on image to enlarge.)

Table of Your Expected Contribution Percentage:

If your income is

Your expected contribution will be

100%-133% of FPL

2% of your income

133%-150% of FPL

3%-4% of your income

150%-200% of FPL

4%-6.3% of your income

200%-250% of FPL

6.3%-8.05% of your income

250%-300% of FPL

8.05%-9.5% of your income

300%-400% of FPL

9.5% of your income

I hope your weather is not as beautiful as it is here in my part of Texas on this Sunday afternoon. If so, you are probably regretting you took the time to get this far into this hopefully informative piece. If it is – do not blame me and certainly–do not shoot the messenger.

As for me, I’m getting out on my motor bike and will take my mind off this monumental cross I bear being . . .

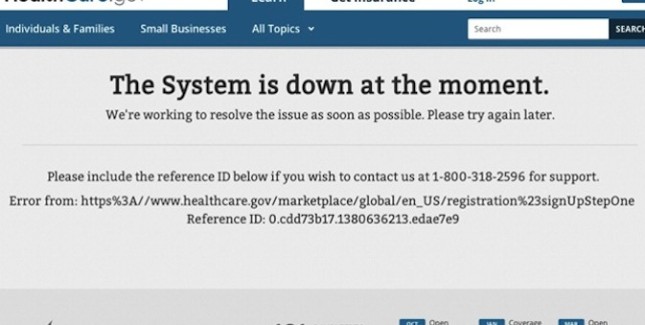

The Healthcare.gov website requires that individuals looking for coverage enter personal information before comparing plans. IT experts believe that this requirement is causing the website to crash.

A growing consensus of IT experts, outside and inside the government, have figured out a principal reason why the website for Obamacare’s federally-sponsored insurance exchange is crashing. Healthcare.gov forces you to create an account and enter detailed personal information before you can start shopping. This, in turn, creates a massive traffic bottleneck, as the government verifies your information and decides whether or not you’re eligible for subsidies. HHS bureaucrats knew this would make the website run more slowly. But they were more afraid that letting people see the underlying cost of Obamacare’s insurance plans would scare people away.

HHS didn’t want users to see Obamacare’s true costs

“Healthcare.gov was initially going to include an option to browse before registering,” report Christopher Weaver and Louise Radnofsky in the Wall Street Journal. “But that tool was delayed, people familiar with the situation said.” Why was it delayed? “An HHS spokeswoman said the agency wanted to ensure that users were aware of their eligibility for subsidies that could help pay for coverage, before they started seeing the prices of policies.” (Emphasis added.)

As you know if you’ve been following this space, Obamacare’s bevy of mandates, regulations, taxes, and fees drives up the cost of the insurance plans that are offered under the law’s public exchanges. A Manhattan Institute analysis I helped conduct found that, on average, the cheapest plan offered in a given state, under Obamacare, will be 99 percent more expensive for men, and 62 percent more expensive for women, than the cheapest plan offered under the old system. And those disparities are even wider for healthy people.

That raises an obvious question. If 50 million people are uninsured today, mainly because insurance is too expensive, why is it better to make coverage even costlier?

Political objectives trumped operational objectives

The answer is that Obamacare wasn’t designed to help healthy people with average incomes get health insurance. It was designed to force those people to pay more for coverage, in order to subsidize insurance for people with incomes near the poverty line, and those with chronic or costly medical conditions.

But the laws’ supporters and enforcers don’t want you to know that, because it would violate the President’s incessantly repeated promise that nothing would change for the people that Obamacare doesn’t directly help. If you shop for Obamacare-based coverage without knowing if you qualify for subsidies, you might be discouraged by the law’s steep costs.

So, by analyzing your income first, if you qualify for heavy subsidies, the website can advertise those subsidies to you instead of just hitting you with Obamacare’s steep premiums. For example, the site could advertise plans that cost “$0″ or “$30″ instead of explaining that the plan really costs $200, and that you’re getting a subsidy of $200 or $170. But you’ll have to be at or near the poverty line to gain subsidies of that size; most people will either not qualify for a subsidy, or qualify for a small one that, net-net, doesn’t make up for the law’s cost hikes.

This political objective—masking the true underlying cost of Obamacare’s insurance plans—far outweighed the operational objective of making the federal website work properly. Think about it the other way around. If the “Affordable Care Act” truly did make health insurance more affordable, there would be no need to hide these prices from the public.

Subsidy verification created a traffic bottleneck

Comparable private-sector e-commerce sites, like eHealthInsurance.com, allow you to shop for plans and compare prices simply by entering your age and your ZIP code. After you’ve selected a plan you like, you fill out an on-line application. That substantially winnows down the number of people who rely on the site for network-intensive tasks.

The federal government’s decision to force people to apply before shopping, Weaver and Radnofsky write, “proved crucial because, before users can begin shopping for coverage, they must cross a busy digital junction in which data are swapped among separate computer systems built or run by contractors including CGI Group Inc., the healthcare.gov developer, Quality Software Services Inc., a UnitedHealth Group Inc. unit; and credit-checker Experian PLC. If any part of the web of systems fails to work properly, it could lead to a traffic jam blocking most users from the marketplace.”

Jay Angoff, a former federal official at the agency that oversees the exchange, told the Journal that he was surprised by the decision. “People should be able to get quotes” without entering all of that information upfront.

Weaver and Radnofsky say that the core problem stems from “the slate of registration systems [that] intersect with Oracle Identity Manager, a software component embedded in a government identity-checking system.” The main Healthcare.gov web page collects information using the CGI Group technology. Then that data is transferred to a system built by Quailty Software Services. QSS then sends data to Experian, the credit-history firm. But the key “identity management system” employed by QSS was designed by Oracle, and according to the Journal’s sources, the Oracle software isn’t playing nicely with the other information systems.

Oracle hotly denies these claims. “Our software is the identical product deployed in most of the world’s most complex systems…our software is running properly,” said an Oracle spokeswoman in a statement.

‘It’s awful, just awful’

Robert Pear and colleagues at the New York Times have a piece up today detailing the serious problems with the federal exchange, problems that may get worse, not better. They confirm what we already knew: that the Obama administration refused to delay the implementation of the exchanges, despite the well-known problems, because they were afraid of the political blowback. “Former government officials say the White House, which was calling the shots, feared that any backtracking would further embolden Republican critics who were trying to repeal the health care law.”

As I documented last week, IT and insurance experts have been saying for at least eight months that implementation of the exchanges was going badly, that as early as February officials were warning of a “third world experience.” The Times’ sources are just as blunt. “These are not glitches,” said one insurance executive. “The extent of the problems is pretty enormous. At the end of our [conference calls with the administration], people say, ‘It’s awful, just awful.’”

“We foresee a train wreck,” said another executive in a February interview with the Times. “We don’t have the IT specifications. The level of angst in health plans is growing by leaps and bounds. The political people in the administration do not understand how far behind they are.” Richard Foster, the former chief actuary at the Centers for Medicare and Medicaid Services, said last week that “so much testing of the new system was so far behind schedule, I was not confident it would work well.”

Henry Chao, the deputy chief information officer at CMS who made the “third world experience” comment, was told by his superiors that failure to meet the October 1 launch deadline “was not an option,” according to the Times.

White House knowingly chose to court disaster

Think about it. It’s quite possible that much of this disaster could have been avoided if the Obama administration had been willing to be open with the public about the degree to which Obamacare escalates the cost of health insurance. If they had, then a number of the problems with the exchange’s software architecture would never have arisen. But that would require admitting that the “Affordable Care Act” was not accurately named.

The White House knew that its people on the front lines, people like Henry Chao, were worried that the exchanges would get botched. They saw the Congressional Research Service memorandum detailing that the administration has missed half of the statutory deadlines assigned by the law. But they were more afraid of the P.R. disaster of disclosing Obamacare’s high premiums than they were of the P.R. disaster of crashing websites. What you see is the result.

************************

Tech experts: Health exchange site needs total overhaul

Kelly Kennedy, USA TODAY 5:36 p.m. EDT October 17, 2013Health and Human Services Secretary Kathleen Sebelius calls the rollout of the health care exchanges rocky. (Photo: Jose Luis Magana, AP)

WASHINGTON — The federal health care exchange was built using 10-year-old technology that may require constant fixes and updates for the next six months and the eventual overhaul of the entire system, technology experts told USA TODAY.

The site could be perfect, but if the systems from which it draws data are not up to speed, it doesn’t matter, said John Engates, chief technology officer at Rackspace, a cloud computer service provider.

“It is a core problem in the sense of it’s fundamental to this thing actually working, but it’s not necessarily a problem that the people who wrote HealthCare.gov can get to,” Engates said. “Even if they had a perfect system, it still won’t work.”

Recent changes have made the exchanges easier to use, but they still require clearing the computer’s cache several times, stopping a pop-up blocker, talking to people via Web chat who suggest waiting until the server is not busy, opening links in new windows and clicking on every available possibility on a page in the hopes of not receiving an error message. With those changes, it took one hour to navigate the HealthCare.gov enrollment process Wednesday.

“I have never seen a website — in the last five years — require you to delete the cache in an effort to resolve errors,” said Dan Schuyler, a director at Leavitt Partners, a health care group by former Health and Human Services secretary Mike Leavitt. “This is a very early Web 1.0 type of fix.”

“The application could be fundamentally flawed,” said Jeff Kim, president of CDNetworks, a content-delivery network. “They may be using 1990s technology in 2.0 world.”

Outsiders acknowledged they can’t see the whole system, but they said they feared HHS built a system that will need an expensive overhaul that would cause more headaches for people trying to buy insurance.

“I will be the first to tell you that the website launch was rockier than we wanted it to be,” HHS Secretary Kathleen Sebelius said Wednesday at Cincinnati State Technical and Community College, adding that people have until Dec. 15 to enroll to ensure coverage beginning Jan. 1.

HHS officials did not respond to a request about the nature of the problems. However, they reiterated that wait times have been reduced or even eliminated as they continue to work to fix the system. As of Thursday, the site had received 17 million unique visitors.

“We continue to work around the clock to improve the consumer experience on HealthCare.gov,” HHS spokeswoman Joanne Peters said. “We are seeing progress: wait times to begin the online process have been virtually eliminated, and more consumers are creating accounts, completing applications and ultimately enrolling in coverage if they choose to do so at this time. However, we will not stop addressing issues and improving the system until the doors to HealthCare.gov are wide open.”

Engates said HHS has been opaque about the problems, and the tech industry doesn’t know the extent of the issues. “There’s no secrets leaking out,” he said. “I’m sure everyone’s looking for something to change the direction of the conversation, but it’s just not there.”

“I think it’s a data problem,” Kim said. “It always comes down to that.”

And if that’s the case, the problems are beyond “rocky,” he said. Instead, it would require a “fundamental re-architecture.” In the meantime, “I think they’re just trying to shore up as quickly as possible. They don’t have time to start from scratch.”

“If I was them, and I’m just conjecturing, I would probably come up with some manual way of saying, ‘Only people with the last name starting with ‘A’ can sign up today,” he said.

But come March 31, when the first enrollment period ends, the “shore up” period may become a “re-architecting” period, Kim said.

On a good note, he said, after looking at available code, the site is “very secure.”

Clearing the cache, which has helped make it easier for some people to enroll, could ultimately strain the system more, Kim said. That’s because a “cookie” is stored on a person’s computer that contains data, such as the person’s name and address, that can then be quickly accessed when that person gets on the website again instead of having to be retrieved from the government’s server.

But as HHS fixes errors, the cookies may not correspond with the updated website, so rather than allowing someone to quickly log in, they instead cause an error message. And every time a person clears his computer’s cache, the government’s website has to work that much harder to grab more data.

Requiring people who may not be Web savvy to use the site in any way other than a step-by-step easy process defeats the point of the whole system, Schuyler said. That includes laws mandating that insurers provide clear explanations about policies to people may make sound decisions and understand what they’re buying.

“Most consumers will have no idea what ‘clearing the cache’ is and this will just cause more confusion and frustration,” he said.

So far, the site’s problems have not driven away potential customers, according to a poll conducted by uSamp — United Sample Inc. The survey found that among the 832 people who attempted to log in, 38% received an error message, 50% were asked to try again later, 25% were unable to create an account, 31% were told the system was down, and 19% had no problems. About 83% said they would try again later, while 15% said they would wait until they heard the website was working well. About 70% of those who said they had no issues said they still waited to enroll because they want to think about their options.

Engates said he believes most of the problems are caused by systems integration with other sites, such as the IRS. And that could be causing some of the problems people see as they make it past the initial application process. It’s a series of questions meant to verify a person’s identity and income. But after that questionnaire, visitors often encounter a series of error messages, or the page a person tries to click to doesn’t come up. The data requests to other sites could be causing those problems, Engates said, which would mean the problem isn’t with the HHS site itself.

“Maybe the site is submitting a request for more data, and that puts you in that trap again,” he said. “It’s a giant integration problem that they have to solve.”

And as they try to fix those problems, there’s another issue lurking in the background: Some HHS personnel were named essential, and not subject to furloughs because of the government shutdown. But that didn’t apply to the other organizations they were working with, Engates said. So as HHS techs work around the clock to fix the problems, IRS techs may be prohibited from working at all.

In the meantime, HHS personnel can’t say anything about the situation, it can be played politically as “bad,” he said. If they say it will take two weeks to fix, they will be criticized because it’s taking too long. But he expects that it’s a problem that will be resolved soon, especially as the volume of visitors goes down.

“If you can get the system below some sort of threshold, it will perform as it’s supposed to,” Engates said. “It won’t get any worse. It’s going to get better little by little by little.”

As a licensed agent in Texas, Indiana, Ohio and Michigan I am certified with the Department of Health and Human Service through the Center for Medicare Service to enroll residents of those states in health insurance plans for 2014. This is whether they qualify for a subsidy or not. Premiums are the same whether you go through me, the Marketplace (Federal Exchange) or a Navigator. And I would like to assist you. Problem is – 5 days into the enrollment phase of the Affordable Care Act (ACA) I still have not succeeded in being able to create even my own account to see what all my options are. I have seen many of my options outside the Marketplace–in the private market–and my quoted premium is approximately 33% higher than my current premium for comparable coverage! I have read all news articles relative to enrollment numbers and although the White House says people are enrolling in the Marketplace (which is where residents of these states go for quotes unless coming to me) and–as of yesterday–no journalist has been successful in finding and interviewing one individual who has successfully purchased health insurance in the Marketplace! One individual, Chad Henderson, reported he and his father had but when swarmed by journalist and asked for details – his father said neither he or his son had. Turns out Chad was a campaign worker for the Obama administration last year and an active volunteer for Organizing for Action, the former campaign organization that now advocates for the President’s legislative agenda. You figure it out. This much I know – if you already know that based on your estimated income for 2014 you will not qualify for a subsidy – you should apply for coverage through me and avoid the wait (however long) on the Marketplace website. You can see your options and go directly into your chosen health insurance companies application for the plan you select.

If, ultimately, you qualify for a subsidy – you may be relatively satisfied with your premium but it looks like (in order for that to be the case) you will have to accept a deductible much higher than what you anticipated. If you do not qualify for a subsidy – prepare for what in all likelihood will be sticker shock.

Regardless, I have made about 15 unsuccessful attempts, consuming hours of wait time the last 5 days to open an account in the Marketplace and–for research purposes– obtain my own quotes and see what subsidy options look like. Even Chad Henderson claimed it took him 3 hours to create an account–and this allegedly took place at 3 a.m. in the morning! How am I supposed to take my clients who will qualify for a subsidy from my quoting engine into the online Marketplace and have us succeed in staying with each other while we wait hours for us to set up their account? Of course, these wait times will surely decrease over time, right? Errrrr . . . right?

UPDATED at 2.54pm ET:Scroll to end of this article for the latest development in this story. After speaking directly with Chad Henderson, The Washington Post has confirmed that he has not in fact enrolled in a health-care plan.

Chad Henderson is the media’s poster boy for Obamacare. Reporters struggled this week to find individuals who said they had been able to enroll in one of the law’s 36 federally run health-insurance exchanges.

That changed yesterday, when they found Henderson, a 21-year-old student and part-time child-care worker who lives in Georgia and says that he successfully enrolled himself and his father Bill in insurance plans via the online exchange administered at healthcare.gov.

But in an exclusive phone interview this morning with Reason, Chad’s father Bill contradicted virtually every major detail of the story the media can’t get enough of. What’s more, some of the details that Chad has released are also at odds with published rate schedules and how Obamacare officials say the enrollment system works.

The coverage of Chad Henderson has been massive. He was featured in The Washington Post Thursday as “the Obamacare enrollee that tons of reporters are calling.” He was also profiled in The Huffington Post as someone who “beat the glitches to sign up for Obamacare.” He was interviewed by Politico, multiple local news organizations, and, according to his Facebook feed, was asked to be part of a conference call hosted by the Department of Health and Human Services.

Chad’s story was tweeted out by the official Obamacare Twitter feed. It was promoted to the media by Enroll America, a health-care activist group headed by a former White House communications staffer, as a sign of Obamacare’s success. Henderson told reporters at multiple news outlets that after a three-hour wait to sign up online, he enrolled around 3 a.m. Tuesday morning in an unsubsidized private insurance plan that would cost him about $175 a month. He also said that his father enrolled in separate coverage plan that would cost about $250 a month after factoring in the subsidies for which his father qualified on his approximately $24,000 annual income.

Chad’s decision to purchase his own, separate plan might surprise some.A monthly premium of $175 would represent about 30 percent of his pre-tax take home pay—about $583 a month on the $7,000 part-time income he claimed. And he could have chosen to be covered by his father’s plan, which, under the Affordable Care Act, would have been required to cover dependents up to the age of 26. Chad said his father encouraged him to be covered under his own plan, even though the cost was higher. “He’s old school, so he wants me to take responsibility,” Chad toldThe Huffington Post.

Henderson’s story was promoted as proof that the new health law can work for individuals. That was exactly how Chad intended it. He was a volunteer with President Obama’s campaign last year, and his LinkedIn page still lists him as an active volunteer with Organizing for Action, the former campaign organization which now advocates for the president’s legislative agenda.

He told The Washington Post that he was sharing his story because he wanted the new health law to succeed.

“I’ve read a few articles about how young people are very critical to the law’s success,” he said to The Post. “I really just wanted to do my part to help out with the entire process.”

But details of Chad’s story proved difficult to verify. And in a phone interview conducted this morning, Chad’s father Bill contradicted major details of Chad’s story. I reached Bill Henderson by following a series of links at Chad’s Facebook page, through which I was able to speak directly to the father.

Bill Henderson told me that both he and his son were interested in getting coverage, but that he had not enrolled in any plan yet, and to his knowledge, neither had his son. He also said that when they do enroll, getting the most coverage for the least money would be the goal, and that he expects that he and his son will get coverage under the same plan.

Bill told me that Chad had been looking into plans online. “He told me that there’s different plans. And we haven’t decided which plans to enroll in yet.”

I asked him whether he and his son had talked about going on separate plans, and he told me that, “We’ll probably go on the same plan, more than likely.”

Two days ago, I contacted most every major health insurance carrier anticipated to continue operating in the Texas individual and family health insurance market and the Federally-Run Marketplace (Exchange) that people will go to in order to purchase their policy to be effective January 1. When I noted that they had not yet released premiums for these plans to be available October 1st and asked if they could disclose them to me – without exception they said they could not and, when I inquired why, they told me, “I cannot answer that”. I said, you realize we only have six days until you expect me to offer these to my clients and the public. They responded, “We understand”. When I asked if premiums would be available by October 1, I was told they hoped they would be.

Yesterday I heard a very popular talk show host theorize as to why this was the case and one of today’s feature articles from Politico, September 25th (below) comments on this issue. It says a report by the Department of Health and Human Services was issued to news organizations on Wednesday under a “strict embargo, with specific instructions not to share the information with anyone else, like outside health insurance experts (such as this blog’s friendly and not the least frustrated administrator) who might be able to provide more analysis of the numbers” to an exceptionally intelligent and curious public such as followers of this blog.

(Obviously, all the major insurance carriers got word of this and that Kenton Henry would apparently be contacting them on this matter, as they were certainly prepared with a script designed with me (or the likes) of me in mind.)

However, “apparently the word leaked out” as the article goes on to say the report released premiums based on the national benchmark “Silver” Plan with an (average) premium of $328. Both the CNN Money and Washington Post articles below go on to describe in more detail 47 state and the District of Columbia premiums which were used to arrive at these averages. CNN paints a more positive picture of these numbers however the Politico article makes it clear it believes the numbers released are designed to creative the most positive impression of premiums prior to their ultimate and full release next Tuesday, October 1. They go on to fault the administration not for telling what premiums will be in an ideal situation when the client is young and healthy or qualifies for a subsidy, but for not disclosing what they will be for the rest of us.

For complete disclosure, assuming the insurance companies are not forced to give government Navigators a head start by turning them loose in the Marketplace October 1 while continuing to withhold premiums, links and enrollment materials from licensed agents like myself until some later date – check back with me next Tuesday. Hopefully I will not awaken to find my insurance license revoked and my internet cut off.