Senate’s ACA Repeal and Replace Bill Up In Air

― op-ed by D. Kenton Henry

The passage of the Senate’s Affordable Care Act repeal and replace bill, prior to their scheduled July 4th recess, is as up in the air as the fireworks will be coinciding with that illustrious date. With five Republican and additional Democrat senators currently opposed, its passage appears tenuous at best. This, in spite of President Trump’s expressed confidence it will happen.

As a medical insurance broker the past 30 years, I have certainly have an opinion on, and a vested interest in, the passage (or failure) of the bill. The reality is, the Democrats own the current Patient and Protection Affordable Care Act (PPACA). Not one Republican voted for it. Therefore (if repeal fails), come 2018, it will be the Democrat’s law which, I believe, will result in an even greater increase in health insurance premiums we have already seen skyrocket since the Act’s passage. And be certain―we will see an even greater exodus of insurance carriers from the marketplace, leaving some counties―and possibly states―with only one carrier. Or, possibly, none. In which case, Trump and the Republicans can continue to tell the Democrats, “We told you so!”.

The problem for the Republicans is, they were elected on a platform of repeal and replace. As such, there are two ways Republicans can fail the people. The first is by not fulfilling that promise. The second―and quite possibly the larger failure― is to pass something which turns out to be an equal or greater debacle than the PPACA itself. As much as I want to see the Act replaced with something better, upon analysis, I find myself largely in agreement with Senator Rand Paul. This bill almost resembles Obamacare more than it does not. Not only does it continue subsidies based on income, but it maintains ten of the twelve mandated “essential coverage items” which forced premiums up in the first place! The primary objectives of repeal and replace were to give people more control over the coverage they purchase and reject, and to bring premiums down. To acquire just what they need and reject what they don’t, all at a lower cost. As it stands today, the Senate bill cannot accomplish either because the remaining forced mandates will force insurance companies to keep premiums high while rationalizing the subsidies allow enough people to pay them using “other people’s money”. When all is said and done, if the bill passes as is, those who don’t qualify for a subsidy will feel angry and betrayed and our twenty trillion dollar budget deficit will grow at even faster than its current, virtually criminal, rate of escalation. Couple doing away with the individual mandate to purchase and maintain coverage with allowing people to purchase it anytime of the year―in spite of the state of their health―and you have a recipe for absolute failure. Many will refrain from purchasing until they receive a dread diagnosis, then purchase the insurance to force the loss of huge medical claims on someone else! I.e., the insurance companies and those responsible insured members who pay their own premiums. If passed without restrictions on when insurance may be purchased (Open vs. Closed Enrollment), I predict this replacement will fail more quickly than Obamacare has failed.

Who will be the major losers if this bill passes as is? Those individuals who must pay their own premiums; the American taxpayer; and―when the healthy drop coverage because they are no longer forced by law to purchase it―me. Who are the major winners? Employers who will see the mandate to provide coverage for groups of 50 plus dropped, creating an incentive to hire; Medical Device companies who will see taxes on their products repealed, encouraging innovation; those individuals and families who have someone else paying all, or the majority, of their premium; and the insurance companies who continue to be subsidized and receive even greater premiums (subsidized or not) for somewhat diminished coverage. And―in the case of where a broker’s compensation is based on a percentage of premium―me.

Who knows how this will ultimately shake out. All I know is, whatever the result, it will be a mixed bag depending on your position in the equation. Stay tuned and―regardless the result―contact me at 281-267-6565. Whatever your options, unless agents and brokers fall on the chopping block, I intend to be here to assist you identifying and obtaining the option most beneficial to your physical and financial health.

https://healthandmedicareinsurance.com

http://thewoodlandstxhealthinsurance.com

*************************************************************

FEATURED ARTICLE:

Senate health-care draft repeals Obamacare taxes, provides bigger subsidies for low-income Americans than House bill

By Paige Winfield Cunningham By Paige Winfield Cunningham June 21

Senate leaders on Wednesday were putting the final touches on legislation that would reshape a big piece of the U.S. health-care system by dramatically rolling back Medicaid while easing the impact on Americans who stand to lose coverage under a new bill.

A discussion draft circulating Wednesday afternoon among aides and lobbyists would roll back the Affordable Care Act’s taxes, phase down its Medicaid expansion, rejigger its subsidies, give states wider latitude in opting out of its regulations and eliminate federal funding for Planned Parenthood.

The bill largely mirrors the House measure that narrowly passed last month but with some significant changes aimed at pleasing moderates. While the House legislation tied federal insurance subsidies to age, the Senate bill would link them to income, as the ACA does. The Senate proposal cuts off Medicaid expansion more gradually than the House bill,\ but would enact deeper long-term cuts to the health-care program for low-income Americans. It also removes language restricting federally subsidized health plans from covering abortions, which may have run afoul of complex budget rules.

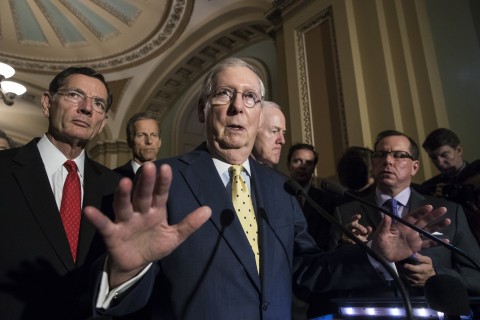

Senate Majority Leader Mitch McConnell (R-Ky.) intends to present the draft to wary GOP senators at a meeting Thursday morning. McConnell has vowed to hold a vote before senators go home for the July 4 recess, but he is still seeking the 50 votes necessary to pass the major legislation under arcane budget rules. A handful of senators, from conservatives to moderates, are by no means persuaded that they can vote for the emerging measure.

Aides stress that the GOP plan is likely to undergo more changes to garner the 50 votes Republicans need to pass it. Moderate senators are concerned about cutting off coverage too quickly for those who gained it under the ACA, also known as Obamacare, while conservatives don’t want to leave big parts of the ACA in place.

As a nod to conservatives, the Senate bill would give states more leeway in opting out of the ACA’s insurance regulations through expanding the use of so-called “1332” waivers already embedded within the law, according to the draft proposal. States could use the waivers to make federal subsidies available even off the marketplaces — but they couldn’t go so far as to lift ACA protections for patients with preexisting conditions.

But it may prove trickier to get moderates on board. Senate leaders are hoping the big draw for them lies in the bill’s more generous income-based approach to insurance subsidies, which closely mirror the subsidies offered under Obamacare.

Subsidies are available to Americans earning between 100 percent and 400 percent of the federal poverty level. Starting in 2020, under the Senate bill, this assistance would be capped for those earning up to 350 percent — but anyone below that line could get the subsidies if they’re not eligible for Medicaid.

The subsidies would also mirror the ACA in that they would be pegged to a benchmark insurance plan each year, ensuring that the assistance grows enough to keep coverage affordable for customers.

The Senate bill would also keep the ACA’s Medicaid expansion around for longer, gradually phasing it out over three years, starting in 2021.

Despite these shifts, moderates are likely to be turned off by how the bill cuts Medicaid more deeply than the House version. But the biggest cuts wouldn’t take effect for seven years, a time frame that could be more politically palatable for members like Sens. Rob Portman (R-Ohio) and Shelley Moore Capito (R-W.Va.).

Under the Senate draft, federal Medicaid spending would remain as is for three years. Then in 2021 it would be transformed from an open-ended entitlement to a system based on per capita enrollment. Starting in 2025, the measure would tie federal spending on the program to an even slower growth index, which in turn could prompt states to reduce the size of their Medicaid programs.

In a move that is likely to please conservatives, the draft also proposes repealing all of the ACA taxes except for its so-called “Cadillac tax” on high-cost health plans in language similar to the House version. Senators had previously toyed with the idea of keeping some of the ACA’s taxes.

The Senate bill would also provide funding in 2018 and 2019 for extra Obamacare subsidies to insurers to cover the cost-sharing discounts they’re required to give the lowest-income patients. Insurers have been deeply concerned over whether the subsidies will continue, as the Trump administration has refused to say whether it will keep funding them in the long run.

The House had a difficult time passing its own measure after a roller-coaster attempt, with the first version being pulled before reaching the floor after House Speaker Paul D. Ryan (R-Wis.) determined he did not have the votes. House Republicans went back to the drawing board and passed their own measure — which would more quickly kill Medicaid expansion and provide less-generous federal subsidies — on May 4.

Even if the Senate measure does pass the upper chamber, it will still have to pass muster with the more conservative House before any legislation could be enacted.

Juliet Eilperin and Amy Goldstein contributed to this report.