By D. Kenton Henry

As a health insurance broker the last thirty years, I have a vested interest in the state of the industry, and especially so since the Affordable Care Act (ACA) , commonly referred to as Obamacare, was passed in March of 2010. It has been a turbulent ride as I and my clients have struggled to adapt to each phase of the law’s implementation. This has been especially true, the previous three years, as I prepared―and now prepare again―for “Open Enrollment” (OE). OE is the period during which the Department of Health and Human Services allows people to acquire individual and family health insurance for the coming year. This year, it is scheduled to run from November the 1st through January 31st. I say “scheduled”, because they typically extend it in an effort to give people more time to enroll. And, apparently, the Department needs to give people as much time as possible because the latest numbers indicate Obamacare enrollment has fallen significantly short of expectations. (Refer to our feature article from The Washington Post below.) As it explains, enrollment in the exchanges is less than half initially predicted. The success of the exchanges was predicated on the young and healthy enrolling in numbers sufficient to offset the sick and elderly who would naturally submit more and higher claims to the insuring companies. The young and healthy have largely declined enrolling―presumably and primarily because, well―they’re young and healthy. Had they enrolled, the theory was they would have diluted the claims (losses) with positive (no losses) premium dollars. Additional factors are that, unless someone qualifies for a subsidy, the premiums are high and, for the most part, going higher. The only cases where premiums seem to have gone down are where the insured members are forced into Health Maintenance Organization (HMO) plans where they find their providers and treatment rationed. Furthermore, the penalties (“Shared Responsibility Tax”) for not having insurance, relative to the premiums for having it, are so small as to be largely ignored. Yes, the penalties are increasing but not in proportion to the premiums. And word is, the premiums are only going higher in 2017.

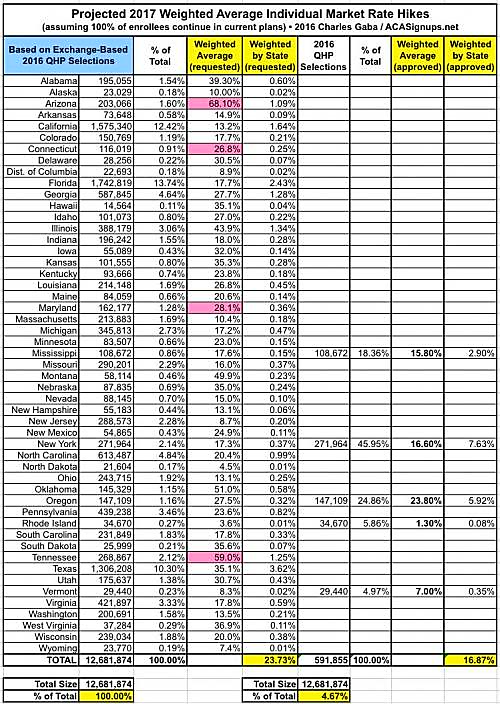

*(CLICK ON THE GRAPHIC TO ENLARGE STATE BY STATE PROJECTED 2017 PREMIUM INCREASES.)

As our feature article from the Wall Street Journal ( posted below) describes ―another factor detrimental to the success of the Act and the exchanges is decreasing competition among carriers. In spite of the high premiums they charge, insurers are experiencing losses too great to allow them to remain in the marketplace. As a result, they are dropping out in ever increasing numbers. These losses result, in part, because the government itself has cut the subsidies they originally promised insurance companies in order to offset the losses they anticipated. Obviously, companies have less money to pay the higher than expected claims they are experiencing. A Kaiser Family Foundation study, cited in the WSJ article, indicates exchange shoppers may have only one insurance company to choose from in 31% of the nation’s counties and the possibility of only two in another 31%. While many are quick to blame the “greedy” insurance companies, this editor feels the need to point out the reality that insurance companies are not charities. And even charities must operate in the black if they are to remain in existence. It is my opinion that only the government feels it is entitled to operate at a loss and, additionally, that, that is acceptable. Of course, when your are operating entirely with other people’s money―that is a much easier thing to do.

I will now put down my keyboard and go back to studying, testing and certifying to offer and provide the new Obamacare and Medicare related plans to both my clients and prospective clients for 2017. It amounts to an investment of many hours in order to remain informed and credible in an extremely complicated market. As in 2016, one key hurdle for those purchasing 2017 individual and family coverage will be to deal with the inability to find their doctors, and even their hospitals, in the HMO networks. I have developed a strategy for coping with this which I have utilized for myself. While it does not entirely eliminate the inconvenience of the aforementioned problem, it does soften the blow and in some cases―from a purely monetary standpoint―offset the loss in dollars a total and ideal solution would have cost. Please call me at 281.367.6565 to discuss this and other strategies designed to minimize the difficulties and accompanying stress of identifying and acquiring 2017 health insurance.

*****************************

FEATURE ARTICLES

Wall Street Journal

Health Insurers’ Pullback Threatens to Create Monopolies

Analysis suggests ACA exchanges are likely to offer just one coverage option in 31% of U.S. counties

By Anna Wilde Mathews and Stephanie Armour

Updated Aug. 28, 2016 7:47 p.m. ET

Nearly a third of the nation’s counties look likely to have just a single insurer offering health plans on the Affordable Care Act’s exchanges next year, according to a new analysis, an industry pullback that adds to the challenges facing the law.

******************************

THE WASHINGTON POST

Health-care exchange sign-ups fall far short of forecasts

August 27 at 8:10 p.m.

Enrollment in the insurance exchanges for President Obama’s signature health-care law is less than half the initial forecast, pushing several major insurance companies to stop offering health plans in certain markets because of significant financial losses.

As a result, the administration’s promise of a menu of health-plan choices has been replaced by a grim, though preliminary, forecast: Next year, more than 1 in 4 counties are at risk of having a single insurer on its exchange, said Cynthia Cox, who studies health reform for the Kaiser Family Foundation.

The debate over how perilous the predicament is for the Affordable Care Act, commonly called Obamacare, is nearly as partisan as the divide over the law itself. But at the root of the problem is this: The success of the law depends fundamentally on the exchanges being profitable for insurers — and that requires more people to sign up.

In February 2013, the Congressional Budget Office predicted that 24 million people would buy health coverage through the federally and state-operated online exchanges by this year. Just 11.1 million people were signed up as of late March.

Exchanges are marketplaces where people who do not receive health benefits through a job can buy private insurance, often with government subsidies.

Aetna, the nation’s third-largest health insurer, announced that it will pull back from Obamacare exchanges citing losses of more than $430 million since January 2014. (Daron Taylor/The Washington Post)

Aetna, the nation’s third-largest health insurer, announced that it will pull back from Obamacare exchanges citing losses of more than $430 million since January 2014. Aetna, the nation’s third-largest health insurer, announced that it will pull back from Obamacare exchanges citing losses of more than $430 million since 2014. (Daron Taylor/The Washington Post)

“Enrollment is key, first and foremost,” said Sara R. Collins, a vice president at the Commonwealth Fund, a nonpartisan foundation that funds health-care research. “They have to have this critical mass of people so that, by the law of averages, you’re going to get a mix of healthy and less healthy people.”

A big reason the CBO projections were so far off is that the agency overestimated how many people would lose insurance through their employers, which would force them into the exchanges. But there have been challenges getting the uninsured to sign up, too.

The law requires every American to get health coverage or pay a penalty, but the penalty hasn’t been high enough to persuade many Americans to buy into the health plans. Even those who qualify for subsidized premiums sometimes balk at the high deductibles on some plans.

And people who do outreach to the uninsured say the enrollment process itself has been more complex and confusing than Obama’s initial comparison to buying a plane ticket.

“This exchange will allow you to ‘one-stop’ shop for a health-care plan, compare benefits and prices, and choose a plan that’s best for you and your family,” Obama said in a speech in 2009. “You will have your choice of a number of plans that offer a few different packages, but every plan would offer an affordable, basic package.”

In some markets, a shortfall in enrollment is testing insurers’ ability to balance the medical claims they pay out with income from premiums. In an announcement curtailing its involvement in the exchanges this month, Aetna cited financial losses traced to too many sick people signing up for care and not enough healthy ones.

The health-care law has been a political lightning rod from the beginning, and Republican legislators have used insurance companies’ withdrawals from the exchanges to reignite calls for the law’s repeal.

Kaiser tracks public data on insurer participation in the exchanges to project how many options counties will have, but the numbers are not final. This year, exchanges in about 7 percent of counties had just one insurer. Earlier this month, Aetna announced that it will pull out of 11 of the 15 states where it offers coverage on the health-care exchanges. Humana made a similar decision weeks earlier, planning to exit several states. And last spring, UnitedHealth Group said it would remain in three or fewer exchanges next year.

Obama has used the health-care law’s challenges to issue a new call for a public insurance option.

“Congress should revisit a public plan to compete alongside private insurers in areas of the country where competition is limited,” he wrote in an essay published in the Journal of the American Medical Association. “Adding a public plan in such areas would strengthen the Marketplace approach, giving consumers more affordable options while also creating savings for the federal government.”

Chicago resident Eva Saur, 32, is exactly the kind of healthy person insurers would like to have on their rolls. Saur hasn’t had coverage in nearly a decade, but she takes good care of her health. For the handful of times she’s been sick, a walk-in clinic at a pharmacy has been sufficient.

“I was raised — not against the system — but we had a doctor who would prescribe us herbs before a prescription” medication, Saur said. “For me, monetarily, it makes way more sense to do this.”

Saur’s tax penalty for being uninsured was a bit more than $600 last year, while the cheapest health plan she examined cost about as much for three months in premiums — and came with a $7,000 deductible.

The penalty for not signing up is increasing. Still, some policy experts insist it is not enough motivation to buy insurance.

“It was basically no stick at all. This is the classic case of where Johnny marked crayon on the wall, his mother said, ‘Don’t do that,’ and then slapped his hand a day later,” said Joseph Antos, a resident fellow at the American Enterprise Institute. “The connection between the offense and the penalty is a little remote.”

The health-care law has had unequivocal successes. In some areas, lots of insurers compete on the exchanges, which helps keep premiums low. In Cleveland and Los Angeles, the average premium for a benchmark health plan actually declined in 2016. The number of uninsured Americans continues to shrink, hitting 9.1 percent last year — the lowest level ever.

The average premium for the people who receive tax credits – 85 percent of the people signed up through the exchanges — is just $106 per month. People who qualify for the income-based tax credits are largely sheltered from premium increases.

The first people to sign up for insurance through the exchanges were expected to be those with chronic diseases and high medical costs. Because insurers could no longer discriminate against those people, the law built in three mechanisms for the government to redistribute money from plans with healthier patients to those with sicker ones. Two of those programs expire at the end of the year. The third, called the “risk adjustment” program, transferred $4.6 billion between insurers in 2014.

Critics say there’s a fundamental problem with the system, and the risk-adjustment program needs to be fixed. But supporters of the law argue that the problem is temporary, the natural evolution of a nascent free-market system. Some of the first companies to enter the market made bad bets on how healthy customers would be, resulting in unprofitable health plans. Proponents say it’s natural for new entrants to replace them, with better information and more competitive plans.

Cigna, for example, has said it has filed to enter exchanges in three new states next year.

“There’s no bottleneck, this is just the natural growth pains of a new market,” said Jonathan Gruber, an economist at the Massachusetts Institute of Technology. “What happened is they set up this new market where insurers didn’t have experience; insurers made an estimate as to what people would cost and their estimate turned out to be too low.”

Supporters point to a recent government analysis that suggests the “risk pool” — the number of high-cost sick customers relative to healthy ones — is not worsening and could even be improving. Medical costs per enrollee in the marketplaces fell by 0.1 percent in 2015, while medical costs for people in the broader health-insurance market grew by at least 3 percent. In states with strong enrollment growth, there were greater reductions in members’ costs.

Everyone agrees that more healthy people need to sign up.

In June, the Obama administration unveiled its plan to target younger and healthier adults, including direct outreach to individuals and families who paid the penalty. It also released new guidance, encouraging insurance companies to communicate more with young adults being kicked off their family’s plan when they turn 26 years old.

Even older adults are taking their chances without health-care coverage.

Donte Fitzhugh, 55, of Charlotte was laid off last year from a job as a call-center operations manager. COBRA, which allows former workers to extend their employer-provided health insurance if they pay the full premium, was expensive, and Fitzhugh didn’t sign up for the exchanges for very human reasons: He figured he’d find a job faster than he did. He thought every penny counted when he was unemployed. He didn’t have major health problems, and he got a coupon to help cover the costs of his hypertension medicine.

As the window to sign up for health insurance passed without a new job, he kept procrastinating. Although health insurance from a new job will begin in October, he faces a penalty that will cost him hundreds of dollars.

“I believe in Obamacare. As an American, it’s my responsibility to have health insurance,” Fitzhugh said. “Since I didn’t have it, it’s going to impact me financially.”

Such are the barriers to insurance: Remaining uninsured can be more attractive or just easier than signing up to pay hundreds of dollars a month for something that many people don’t think they need.

Judy Robinson, a health insurance support specialist at the Charlottesville Free Clinic, has counseled hundreds of patients who are eligible for subsidized insurance on the exchanges but ultimately decide not to sign up. She said the subsidized insurance on the marketplace tends to be a good deal for those who make between 100 and 150 percent of the poverty level. But those who make more often are faced with large deductibles that don’t seem like a good deal to many people.

Beyond the sticker price, she said it can require a lot of paperwork to demonstrate the annual income required to qualify for tax credits if people are juggling multiple part-time jobs. And sometimes, people are simply mistrustful.

“There’s a lot of people that live sort of off the grid, sort of semi-off the grid and they just don’t go to the doctor,” Robinson said. “The hospital is the place where you go to die, and doctors are just going to try and make you do procedures and get money out of you. That’s how they think.”

There are also those who want insurance but are struggling — and find themselves trapped by the high cost of health care.

Donna Privigyi, 49, of Charlottesville has looked into insurance through the exchanges a few times. But over the past few years, much of her modest child-care salary and effort went toward trying to help support her adult son, Mark, who hadn’t been the same since the death of his younger brother. Donna was focused on trying to support her son. Health insurance — even rent — was an afterthought.

“With supporting my son, it didn’t matter,” Privigyi said. “I was just like, I can barely get by, just juggling the bills and taking care of him.”

Late last year, Mark died of a drug overdose, and Privigyi — consumed by grief — wasn’t thinking about insurance when the window to sign up opened and closed.

Then, in June, she got appendicitis. Her bills from two hospitals were $33,000.

The argument for having health insurance is the pile of bills she has been collecting — now with late fees added. The obstacle to getting health insurance is that same stack of bills.

“It’s such a gamble, you know, until I figure out what to do with these medical bills,” Privigyi said. “They’re just adding on late fees. How can I even afford to sign up?”

Juliet Eilperin contributed to this report.

*************************************************************************************************

https://healthandmedicareinsurance.com